String Lights Market Synopsis:

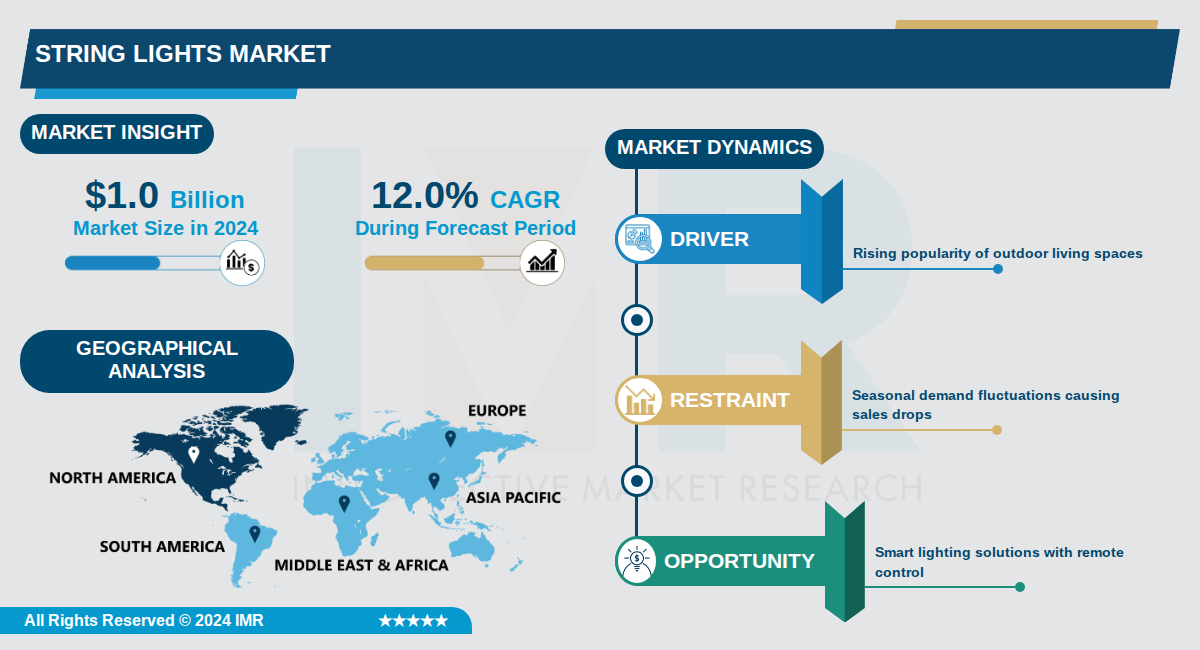

String Lights Market Size Was Valued at USD 1.0 Billion in 2024, and is Projected to Reach USD 4.0 Billion by 2035, Growing at a CAGR of 12.0% From 2024-2035.

The global String Lights Market, valued at $1.0 billion in 2024, is projected to reach $4.0 billion by 2035, growing at a compound annual growth rate (CAGR) of 12.0%. This robust expansion reflects increasing consumer demand for decorative lighting solutions in residential, commercial, and event settings, driven by trends in home décor and outdoor living spaces.

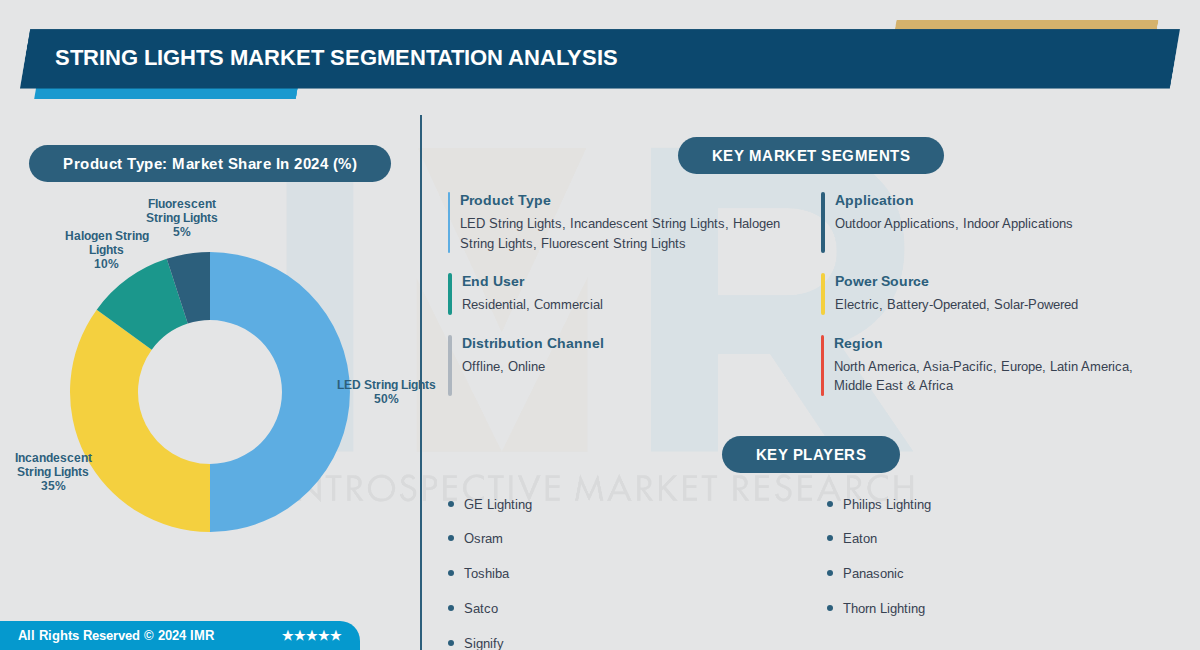

LED string lights dominate the market, capturing approximately 50% share due to their energy efficiency, consuming up to 80% less energy than traditional bulbs, and longevity compared to incandescent options. Outdoor applications account for around 60% of usage, with strong preferences for durable, weather-resistant designs in patios, gardens, and festive installations.

Regionally, North America leads with about 35% market share, fueled by holiday celebrations, weddings, and the popularity of outdoor living, while Asia Pacific is poised for the fastest growth at 35-38% share, supported by urbanization, rising incomes, and e-commerce accessibility. Europe maintains a solid 17-25% position, emphasizing energy-efficient and smart lighting adoption.

String Lights Market Trend Analysis:

Dominance of LED String Lights

- LED string lights dominate the market with roughly 50% share among product type segments, reflecting strong consumer preference for their energy efficiency that consumes up to 80% less energy than traditional bulbs. According to the U.S. Department of Energy, decorative LED lighting penetration increased from 7.9% to 16% between 2016 and 2018, showcasing expanded adoption in string lights. The LED segment's outdoor variants represent about 55% of the share, highlighting their high usage in external decor.

- Prices of LED string lights are coming down while offering advantages like longer lifespan, wider variety of colors, and effects, making them commonplace in homes, gardens, and events. Key players like Philips Lighting and GE Lighting lead this segment with energy-efficient options. The global string lights market, valued at USD 0.64 billion in 2026, is projected to reach USD 1.02 billion by 2035 at a 6% CAGR, largely driven by LED adoption.

- In Asia Pacific, LED string lights account for 35-38% of regional share, fueled by rapid urbanization and rising disposable incomes. This growth supports sustained demand in residential and commercial settings across patios and cafes.

Rise of Smart and Connected String Lights

- Technological advancements are introducing smart string lights controllable via mobile apps and home automation systems like those from Philips Lighting, enhancing user experience with customization and connectivity. Innovations include smart connectivity alongside energy-efficient LED technology and solar or battery-powered designs, improving durability and energy performance. Westinghouse Lighting's April 2025 acquisition of Benson Lights expands its smart outdoor lighting portfolio, accelerating market entry.

- These smart features appeal to modern consumers seeking integration with broader home systems, particularly in North America where the region holds 20-35% of global revenue share due to decorative and smart lighting trends. Europe follows with 17-25% share, driven by energy-efficient adoption. This trend boosts residential and commercial applications for holidays and events.

Expansion into Outdoor Living Spaces

- The growing popularity of outdoor living spaces like patios, decks, and gardens is fueling demand for durable, weather-resistant outdoor string lights, representing 55% of the LED segment. Consumers invest in creating inviting environments for backyard gatherings and barbecues, with North America dominating due to rising outdoor living trends holding 20-35% market share. Asia Pacific leads overall growth with 26-38% share from urbanization.

- COVID-19 lockdowns increased demand for home designs and outdoor lighting as people turned backyards into recreational spaces, boosting string lights for ambiance. Seasonal spikes, especially November holidays, amplify this, with companies like Briignite and Ecolight prioritizing outdoor variants. The steady baseline interest year-round supports ongoing home improvement projects.

String Lights Market Segment Analysis:

String Lights Market is Segmented on the basis of By Product Type, By Application, By End User

By Product Type, LED String Lights segment is expected to dominate the market during the forecast period

- LED string lights dominate with 50% market share due to their energy efficiency, consuming up to 80% less energy than traditional bulbs, and offering longer lifespans and versatile color options that appeal to modern consumers.

- LEDs have become the industry standard as manufacturers and consumers increasingly prioritize sustainability and cost savings, with LED technology representing the fastest-growing segment across residential and commercial applications.

By Application, Outdoor Applications segment is expected to dominate the market during the forecast period

- Outdoor applications account for approximately 60% of total string lights usage, driven by the rising popularity of outdoor living spaces, garden parties, and commercial venue decoration in restaurants and cafes.

- Outdoor LED string lights represent about 55% of the LED segment share specifically, highlighting exceptionally high demand for external décor in both residential patios and commercial hospitality settings.

By End User, Residential segment is expected to dominate the market during the forecast period

- The residential sector is the largest end-user segment, driven by increasing trends in home décor, holiday decorations during Christmas and Diwali, and the growing consumer desire to enhance ambiance in living spaces, bedrooms, and dining areas.

- Residential consumers account for the majority of market demand as they seek affordable, versatile decorative lighting solutions for both indoor and outdoor use, particularly during festive seasons and for weddings and garden events.

By Power Source, Electric segment is expected to dominate the market during the forecast period

- Electric-powered string lights dominate with 60% share due to their reliable performance, consistent brightness, and established infrastructure in both residential and commercial settings where continuous power supply is available.

- Solar-powered and battery-operated variants are growing rapidly as consumers increasingly seek eco-friendly, energy-efficient alternatives that reduce electricity costs and enable flexible installation in areas without direct power access.

By Distribution Channel, Offline segment is expected to dominate the market during the forecast period

- Offline channels maintain 55% market share as consumers prefer physical inspection of string lights before purchase to assess quality, design, and color options, with strong retail presence in hardware stores and specialty lighting retailers.

- Online distribution is rapidly growing at 45% share, driven by convenience, wider product selection, competitive pricing, and the ability to compare multiple brands and designs from home.

By Region, Asia-Pacific segment is expected to dominate the market during the forecast period

- Asia-Pacific leads with 32% regional share driven by rapid urbanization, rising disposable incomes, expanding middle-class populations, and increasing adoption of Western-style décor trends in countries like China, India, and Southeast Asian nations.

- North America holds 30% market share supported by strong culture of outdoor living spaces, established holiday decoration traditions, and high consumer spending on home décor, making it a mature and consistently robust market.

String Lights Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast Period

- North America dominates the string lights market, holding approximately 35% of the global share, with the U.S. and Canada as key contributors due to high consumer adoption for indoor and outdoor decorative uses. This leadership is driven by strong demand during holidays, weddings, and garden events, where energy-efficient LED options are particularly popular. Mexico also plays a role, supported by established retail networks.

- The region benefits from advanced infrastructure, including widespread retail distribution and high disposable incomes that enable aesthetic home enhancements. Rising popularity of outdoor living spaces and stringent energy-efficiency regulations further boost adoption of LED string lights. Seasonal demand for decorations creates consistent market performance despite fluctuations.

- Major players leverage North America's mature market with innovations in smart and LED technologies, focusing on durability and customization. Recent developments include expanded product lines for commercial and residential applications, with U.S.-based firms leading in sales. Growth is projected through 2035, fueled by consumer trends toward sustainable lighting.

Active Key Players in the String Lights Market:

- GE Lighting (USA)

- Philips Lighting (Netherlands)

- Osram (Germany)

- Eaton (USA)

- Toshiba (Japan)

- Panasonic (Japan)

- Satco (USA)

- Thorn Lighting (UK)

- Signify (Netherlands)

- Acuity Brands (USA)

- Cree Lighting (USA)

- Hubbell (USA)

- Kichler (USA)

- Hinkley (USA)

- Syska Led Lights (India)

- Zumtobel Group (Austria)

- Dialight (UK)

- Bajaj Electricals (India)

- Opple Lighting (China)

- Other Active Players

|

String Lights Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 1.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

12.0 % |

Market Size in 2035: |

USD 4.0 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Application |

|

||

|

By End User |

|

||

|

By Power Source |

|

||

|

By Distribution Channel |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: String Lights Market by Product Type (2017-2035)

4.1 String Lights Market Snapshot and Growth Engine

4.2 Market Overview

4.3 LED String Lights

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Incandescent String Lights

4.5 Halogen String Lights

4.6 Fluorescent String Lights

Chapter 5: String Lights Market by Application (2017-2035)

5.1 String Lights Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Outdoor Applications

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Indoor Applications

Chapter 6: String Lights Market by End User (2017-2035)

6.1 String Lights Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Residential

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Commercial

Chapter 7: String Lights Market by Power Source (2017-2035)

7.1 String Lights Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Electric

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Battery-Operated

7.5 Solar-Powered

Chapter 8: String Lights Market by Distribution Channel (2017-2035)

8.1 String Lights Market Snapshot and Growth Engine

8.2 Market Overview

8.3 Offline

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

8.3.3 Key Market Trends, Growth Factors, and Opportunities

8.3.4 Geographic Segmentation Analysis

8.4 Online

Chapter 9: String Lights Market by Region (2017-2035)

9.1 String Lights Market Snapshot and Growth Engine

9.2 Market Overview

9.3 North America

9.3.1 Introduction and Market Overview

9.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

9.3.3 Key Market Trends, Growth Factors, and Opportunities

9.3.4 Geographic Segmentation Analysis

9.4 Asia-Pacific

9.5 Europe

9.6 Latin America

9.7 Middle East & Africa

Chapter 10: Company Profiles and Competitive Analysis

10.1 Competitive Landscape

10.1.1 Competitive Benchmarking

10.1.2 String Lights Market Share by Manufacturer/Service Provider (2024)

10.1.3 Industry BCG Matrix

10.1.4 Partnerships, Mergers & Acquisitions

10.2 GE LIGHTING

10.2.1 Company Overview

10.2.2 Key Executives

10.2.3 Company Snapshot

10.2.4 Role of the Company in the Market

10.2.5 Sustainability and Social Responsibility

10.2.6 Operating Business Segments

10.2.7 Product Portfolio

10.2.8 Business Performance

10.2.9 Recent News & Developments

10.2.10 SWOT Analysis

10.3 PHILIPS LIGHTING

10.4 OSRAM

10.5 EATON

10.6 TOSHIBA

10.7 PANASONIC

10.8 SATCO

10.9 THORN LIGHTING

10.10 SIGNIFY

10.11 ACUITY BRANDS

10.12 CREE LIGHTING

10.13 HUBBELL

10.14 KICHLER

10.15 HINKLEY

10.16 SYSKA LED LIGHTS

10.17 ZUMTOBEL GROUP

10.18 DIALIGHT

10.19 BAJAJ ELECTRICALS

10.20 OPPLE LIGHTING

Chapter 11: Global String Lights Market By Region

11.1 Overview

11.2. North America String Lights Market

11.2.1 Key Market Trends, Growth Factors and Opportunities

11.2.2 Top Key Companies

11.2.3 Historic and Forecasted Market Size by Segments

11.2.4 Historic and Forecast Market Size by Country

11.3. Eastern Europe String Lights Market

11.3.1 Key Market Trends, Growth Factors and Opportunities

11.3.2 Top Key Companies

11.3.3 Historic and Forecasted Market Size by Segments

11.3.4 Historic and Forecast Market Size by Country

11.4. Western Europe String Lights Market

11.4.1 Key Market Trends, Growth Factors and Opportunities

11.4.2 Top Key Companies

11.4.3 Historic and Forecasted Market Size by Segments

11.4.4 Historic and Forecast Market Size by Country

11.5. Asia Pacific String Lights Market

11.5.1 Key Market Trends, Growth Factors and Opportunities

11.5.2 Top Key Companies

11.5.3 Historic and Forecasted Market Size by Segments

11.5.4 Historic and Forecast Market Size by Country

11.6. Middle East & Africa String Lights Market

11.6.1 Key Market Trends, Growth Factors and Opportunities

11.6.2 Top Key Companies

11.6.3 Historic and Forecasted Market Size by Segments

11.6.4 Historic and Forecast Market Size by Country

11.7. South America String Lights Market

11.7.1 Key Market Trends, Growth Factors and Opportunities

11.7.2 Top Key Companies

11.7.3 Historic and Forecasted Market Size by Segments

11.7.4 Historic and Forecast Market Size by Country

Chapter 12: Analyst Viewpoint and Conclusion

Chapter 13: Research Methodology

13.1 Research Process

13.2 Primary Research

13.3 Secondary Research

Chapter 14: Case Study

Chapter 15: Appendix

15.1 Sources

15.2 List of Tables and Figures

15.3 Short Forms and Citations

15.4 Assumption and Conversion

15.5 Disclaimer

|

String Lights Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 1.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

12.0 % |

Market Size in 2035: |

USD 4.0 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Application |

|

||

|

By End User |

|

||

|

By Power Source |

|

||

|

By Distribution Channel |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||