Wood Preservative Market Synopsis:

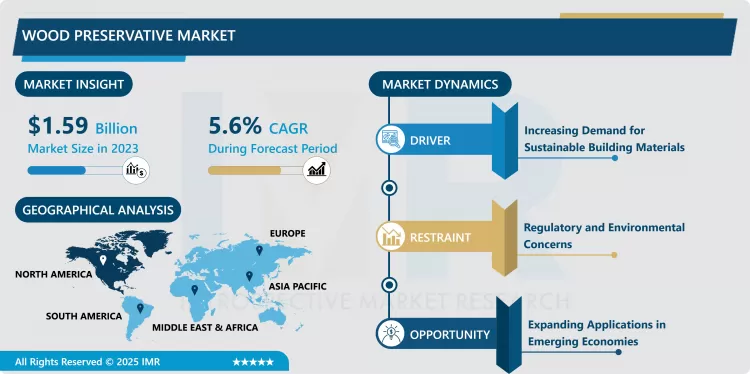

Wood Preservative Market Size Was Valued at USD 1.59 Billion in 2023, and is Projected to Reach USD 2.60 Billion by 2032, Growing at a CAGR of 5.6% From 2024-2032.

Wood preservative industry entails the manufacture and sale of chemicals and other substances that prevent wooden products from degrading through natural forces, rotting, termite attacks and mould formation. These preservatives are used on wooden material for purposes of increasing the durability, anti-gravity effects from natural forces and to give them strength in their usage in construction of homes, offices, industries, and any other place they are required. The wood preservatives are generally known to be oil-borne and water-borne, as well as solvent-borne products, depending on the wood type and the proposed application.

The Wood Preservative Market is on the growth path due to ever-growing demand for wooden products in constructions, furniture as well as other industrial uses. These include ecologicalpción of wood through pests, fungi, and other agents, wood preservatives play a significant role balancing the lifespan /durability of the material. As there are more developments in construction and real estate businesses and especially throughout the growth regions of the world, the utilization of wood preservative products is set to increase.

Housing, landscaping and domestic uses require several wood preservatives because decks, fences and sidings are exposed and affected by harsh weather and moisture. Secondly, bio-based constructions demand new water born and low toxic preservers which are more environmental safe as replaceability of the oil born preservatives. Legal requirements and other environmental factors are becoming more stringent to force manufacturers to work for getting better preservatives with less hazardous and environmentally intolerant chemicals added into them.

Wood preservatives have utility in a wide range of commercial and industrial projects including in furniture manufacturing and the preservation of wood used in agricultural buildings. For instance in a farming community timber is used in the construction of stores, grain silos, bams and other structures which have to be shielded against termite attacks and fungal deterioration. Other industrial applications comprise utility poles, rail sleepers, and other structures that are basic to industrial operations. The growing cognition in the long-term advantages of conserving wood is expected to increase the size of the market for wooden preservers.

Wood Preservative Market Trend Analysis:

Eco-friendly Wood Preservatives

- One emerging pattern in the Wood Preservative Market is for green, low tox or sustainable preservative products. This is due to rising awareness on the environmental impacts of chemical products and the current legislation that demands that manufactures provide harmless chemicals for use. People and companies shopping for preservatives have become more aware of the environmental consequences they are likely to cause to the environment, and are in turn, looking for preservatives that are biodegradable and are derived from renewable resources. It is not only a regulatory requirement, although this has been the case in many parts of the world, but client requests to implement environmentally sustainable construction.

- As a result of this trend, the wood preservative industry is likely to experience the development of more organic/natural preservatives such as plant extract and bio- chemicals. It means the work presented here focuses on providing biodegradable remedies to decay, insects, and fungi that are similar to surged chemicals, but less harmful to the environment. Since sustainability issues creep into the general value equation when determining the end consumer’s willingness to purchase a product, manufacturers invest heavily in product development to produce better, safer and more efficient wood treatment items that are ecologically friendly in line with other connected moves such as the increase in green consumerism and green building certification programmes.

Expanding Applications in Emerging Economies

- The Wood Preservative Market can look forward to a promising future in the emerging countries’ Construction & Infrastructure Industry. Currently, there is immense construction in Asia-Pacific, Latin America, and parts of Africa cities where people use wood as their major construction material due to their fast-growing cities. Since these regions are growing, so the demand for wood preservation to meet the requirement on buildings, bridges and other structures in different projects will also rise. An increase in clients’ disposable income as well as better standards of living is also putting pressure on the use of more durable and more aesthetically pleasing wood products in residential areas especially those areas that are in the forming stage.

- Besides the construction industry, the furniture industry is also growing in these emergent markets due to the rising usage requirements for wooden furniture goods in homes and enterprises. Thus, the market for the manufacturers of wood preservatives is opened to introduce their products and to meet the continually increasing demand for the long-lasting wood solutions. These preservative trends suggest that targeted capital investments alongside the requisite cost-efficient and locally specific preservative products enable enterprise to secure market share and profitability by leveraging on industrialization and continuing economic growth within these regions.

Wood Preservative Market Segment Analysis:

Wood Preservative Market is Segmented on the basis of Type, Formulation, Application, End User, And Region

By Type, Oil-based Wood Preservatives segment is expected to dominate the market during the forecast period

- Oil based preservatives are most widely used due to their excellent performance in exterior finishing applications where issues concerning durability and moisture resistance are paramount. They are most sought-after for times when construction wood has to be treated especially for wooden structures exposed externally such as floor decks, poles, and fences. The nature of oil-based preservatives is long-lasting and thus appropriate for areas where frequent application would prove expensive. But seriously, environmental pollution and health hazards attributed to these products have gradually forced the search for environmentally friendly substitutes.

- Aqueous based preservatives are rapidly growing as industry pressure for efficiency and environmental suitability rises. Residential uses of these preservatives have recently become more popular; especially in areas that have stringent environmental policies. Water-based systems may have some disadvantages, such as less levels of durability than oil-based protective treatments in some instances, but due to the environment friendly and less toxic nature, more markets are adopting them. Besides, an increasing trend towards ecologicalv purchases and policies stimulating construction companies to seek for green accreditation will continue to boost the market for water-based preservers in the future.

By Application, Residential segment expected to held the largest share

- In the residential sector, the primary driver of the demand of the wood preservatives is due to the growing fancy for wooden decks, furniture and floorings that are immune to severe environmental conditions and deterioration as a result of general and normal wear. Customers are now seeking long-lasting finishes that provide value in maintaining wooden structures; wood preservatives provide an economical means to give value to wooden products. This segment is expected to increase with the current business of home renovation and remodeling.

- The commercial segment takes a large portion of the market since such customers focus on beautiful and durable woody products. Here, protective chemicals are used to treat the wooden products to increase their life span as used in making furniture, flooring and ornaments in offices, hotel and retail shops. As long as companies will keep putting emphasis on the quality as well as durability of structures incorporated with woods, there will be increased need for wood preservatives.

Wood Preservative Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

- North America is the largest area on the Wood Preservative Market level because of the developed construction sector and the increased application of wooden materials in residential and non-residential use. The norms and code of the area largely ensure an efficient preservation of wood and includes strict measures towards environmental conservation. This has resulted into high demand of green, or low toxicity preservative treatment especially for uses in construction in dwellings and other structures.

- Apart from the regulatory factors, North America has strong economy, as well as a high level of construction and renovation works. As shown by the customer demand of durable and persistent wood like products, there is a need for a proper preservation technique to increase the useful life of such material. In addition, North American region has also witnessed increasing market of sustainable or green building that is promoting use of environment friendly preservatives. It is foreseen to remain so due to the increasing building and property industries in this area primarily the U.S and Canada.

Active Key Players in the Wood Preservative Market:

- BASF (Germany)

- Lonza Group (Switzerland)

- Koppers Holdings Inc. (USA)

- Rentokil Initial (UK)

- The Sherwin-Williams Company (USA)

- UPM-Kymmene Corporation (Finland)

- Arch Wood Protection (USA)

- McFarland Cascade (USA)

- NicoJack (Germany)

- Viance LLC (USA)

- Osmose, Inc. (USA)

- The Osmose Wood Preserving Company (USA)

- Other Active Players

|

Global Wood Preservative Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 1.59 Billion |

|

Forecast Period 2024-32 CAGR: |

5.6% |

Market Size in 2032: |

USD 2.60 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Wood Preservative Market by Type (2018-2032)

4.1 Wood Preservative Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Oil-based Wood Preservatives

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Water-based Wood Preservatives

4.5 Solvent-based Wood Preservatives

Chapter 5: Wood Preservative Market by Application (2018-2032)

5.1 Wood Preservative Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Residential

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Commercial

5.5 Industrial

Chapter 6: Company Profiles and Competitive Analysis

6.1 Competitive Landscape

6.1.1 Competitive Benchmarking

6.1.2 Wood Preservative Market Share by Manufacturer (2024)

6.1.3 Industry BCG Matrix

6.1.4 Heat Map Analysis

6.1.5 Mergers and Acquisitions

6.2 BASF (GERMANY)

6.2.1 Company Overview

6.2.2 Key Executives

6.2.3 Company Snapshot

6.2.4 Role of the Company in the Market

6.2.5 Sustainability and Social Responsibility

6.2.6 Operating Business Segments

6.2.7 Product Portfolio

6.2.8 Business Performance

6.2.9 Key Strategic Moves and Recent Developments

6.2.10 SWOT Analysis

6.3 LONZA GROUP (SWITZERLAND)

6.4 KOPPERS HOLDINGS INC. (USA)

6.5 RENTOKIL INITIAL (UK)

6.6 THE SHERWIN-WILLIAMS COMPANY (USA)

6.7 UPM-KYMMENE CORPORATION (FINLAND)

6.8 ARCH WOOD PROTECTION (USA)

6.9 MCFARLAND CASCADE (USA)

6.10 NICOJACK (GERMANY)

6.11 VIANCE LLC (USA)

6.12 OSMOSE INC. (USA)

6.13 THE OSMOSE WOOD PRESERVING COMPANY (USA)

6.14 OTHER ACTIVE PLAYERS

Chapter 7: Global Wood Preservative Market By Region

7.1 Overview

7.2. North America Wood Preservative Market

7.2.1 Key Market Trends, Growth Factors and Opportunities

7.2.2 Top Key Companies

7.2.3 Historic and Forecasted Market Size by Segments

7.2.4 Historic and Forecasted Market Size by Type

7.2.4.1 Oil-based Wood Preservatives

7.2.4.2 Water-based Wood Preservatives

7.2.4.3 Solvent-based Wood Preservatives

7.2.5 Historic and Forecasted Market Size by Application

7.2.5.1 Residential

7.2.5.2 Commercial

7.2.5.3 Industrial

7.2.6 Historic and Forecast Market Size by Country

7.2.6.1 US

7.2.6.2 Canada

7.2.6.3 Mexico

7.3. Eastern Europe Wood Preservative Market

7.3.1 Key Market Trends, Growth Factors and Opportunities

7.3.2 Top Key Companies

7.3.3 Historic and Forecasted Market Size by Segments

7.3.4 Historic and Forecasted Market Size by Type

7.3.4.1 Oil-based Wood Preservatives

7.3.4.2 Water-based Wood Preservatives

7.3.4.3 Solvent-based Wood Preservatives

7.3.5 Historic and Forecasted Market Size by Application

7.3.5.1 Residential

7.3.5.2 Commercial

7.3.5.3 Industrial

7.3.6 Historic and Forecast Market Size by Country

7.3.6.1 Russia

7.3.6.2 Bulgaria

7.3.6.3 The Czech Republic

7.3.6.4 Hungary

7.3.6.5 Poland

7.3.6.6 Romania

7.3.6.7 Rest of Eastern Europe

7.4. Western Europe Wood Preservative Market

7.4.1 Key Market Trends, Growth Factors and Opportunities

7.4.2 Top Key Companies

7.4.3 Historic and Forecasted Market Size by Segments

7.4.4 Historic and Forecasted Market Size by Type

7.4.4.1 Oil-based Wood Preservatives

7.4.4.2 Water-based Wood Preservatives

7.4.4.3 Solvent-based Wood Preservatives

7.4.5 Historic and Forecasted Market Size by Application

7.4.5.1 Residential

7.4.5.2 Commercial

7.4.5.3 Industrial

7.4.6 Historic and Forecast Market Size by Country

7.4.6.1 Germany

7.4.6.2 UK

7.4.6.3 France

7.4.6.4 The Netherlands

7.4.6.5 Italy

7.4.6.6 Spain

7.4.6.7 Rest of Western Europe

7.5. Asia Pacific Wood Preservative Market

7.5.1 Key Market Trends, Growth Factors and Opportunities

7.5.2 Top Key Companies

7.5.3 Historic and Forecasted Market Size by Segments

7.5.4 Historic and Forecasted Market Size by Type

7.5.4.1 Oil-based Wood Preservatives

7.5.4.2 Water-based Wood Preservatives

7.5.4.3 Solvent-based Wood Preservatives

7.5.5 Historic and Forecasted Market Size by Application

7.5.5.1 Residential

7.5.5.2 Commercial

7.5.5.3 Industrial

7.5.6 Historic and Forecast Market Size by Country

7.5.6.1 China

7.5.6.2 India

7.5.6.3 Japan

7.5.6.4 South Korea

7.5.6.5 Malaysia

7.5.6.6 Thailand

7.5.6.7 Vietnam

7.5.6.8 The Philippines

7.5.6.9 Australia

7.5.6.10 New Zealand

7.5.6.11 Rest of APAC

7.6. Middle East & Africa Wood Preservative Market

7.6.1 Key Market Trends, Growth Factors and Opportunities

7.6.2 Top Key Companies

7.6.3 Historic and Forecasted Market Size by Segments

7.6.4 Historic and Forecasted Market Size by Type

7.6.4.1 Oil-based Wood Preservatives

7.6.4.2 Water-based Wood Preservatives

7.6.4.3 Solvent-based Wood Preservatives

7.6.5 Historic and Forecasted Market Size by Application

7.6.5.1 Residential

7.6.5.2 Commercial

7.6.5.3 Industrial

7.6.6 Historic and Forecast Market Size by Country

7.6.6.1 Turkiye

7.6.6.2 Bahrain

7.6.6.3 Kuwait

7.6.6.4 Saudi Arabia

7.6.6.5 Qatar

7.6.6.6 UAE

7.6.6.7 Israel

7.6.6.8 South Africa

7.7. South America Wood Preservative Market

7.7.1 Key Market Trends, Growth Factors and Opportunities

7.7.2 Top Key Companies

7.7.3 Historic and Forecasted Market Size by Segments

7.7.4 Historic and Forecasted Market Size by Type

7.7.4.1 Oil-based Wood Preservatives

7.7.4.2 Water-based Wood Preservatives

7.7.4.3 Solvent-based Wood Preservatives

7.7.5 Historic and Forecasted Market Size by Application

7.7.5.1 Residential

7.7.5.2 Commercial

7.7.5.3 Industrial

7.7.6 Historic and Forecast Market Size by Country

7.7.6.1 Brazil

7.7.6.2 Argentina

7.7.6.3 Rest of SA

Chapter 8 Analyst Viewpoint and Conclusion

8.1 Recommendations and Concluding Analysis

8.2 Potential Market Strategies

Chapter 9 Research Methodology

9.1 Research Process

9.2 Primary Research

9.3 Secondary Research

|

Global Wood Preservative Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 1.59 Billion |

|

Forecast Period 2024-32 CAGR: |

5.6% |

Market Size in 2032: |

USD 2.60 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Frequently Asked Questions :

The forecast period in the Wood Preservative Market research report is 2024-2032.

BASF (Germany), Lonza Group (Switzerland), Koppers Holdings Inc. (USA), Rentokil Initial (UK), The Sherwin-Williams Company (USA), UPM-Kymmene Corporation (Finland), Arch Wood Protection (USA), McFarland Cascade (USA), NicoJack (Germany), Viance LLC (USA), Osmose, Inc. (USA), The Osmose Wood Preserving Company (USA), and Other Active Players.

The Wood Preservative Market is segmented into Type, Formulation, Application, End User and region. By Type, the market is categorized into Oil-based Wood Preservatives, Water-based Wood Preservatives, Solvent-based Wood Preservatives. By Application, the market is categorized into Residential, Commercial, Industrial, the market is categorized into By End-Use Industry, the market is categorized into Construction, Furniture, Packaging, Marine, Agriculture, Others. By Formulation, the market is categorized into Solvents, Emulsions, Powder. By region, it is analyzed across North America (U.S., Canada, Mexico), Eastern Europe (Russia, Bulgaria, The Czech Republic, Hungary, Poland, Romania, Rest of Eastern Europe), Western Europe (Germany, UK, France, The Netherlands, Italy, Spain, Rest of Western Europe), Asia Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Vietnam, The Philippines, Australia, New-Zealand, Rest of APAC), Middle East & Africa (Turkiye, Bahrain, Kuwait, Saudi Arabia, Qatar, UAE, Israel, South Africa),South America (Brazil, Argentina, Rest of SA).

Wood preservative industry entails the manufacture and sale of chemicals and other substances that prevent wooden products from degrading through natural forces, rotting, termite attacks and mould formation. These preservatives are used on wooden material for purposes of increasing the durability, anti-gravity effects from natural forces and to give them strength in their usage in construction of homes, offices, industries, and any other place they are required. The wood preservatives are generally known to be oil-borne and water-borne, as well as solvent-borne products, depending on the wood type and the proposed application.

Wood Preservative Market Size Was Valued at USD 1.59 Billion in 2023, and is Projected to Reach USD 2.60 Billion by 2032, Growing at a CAGR of 5.6% From 2024-2032.