Strapping Market Synopsis:

Strapping Market Size Was Valued at USD 7.2 Billion in 2024, and is Projected to Reach USD 11.5 Billion by 2035, Growing at a CAGR of 4.9% From 2024-2035.

The global strapping market, encompassing materials, machines, and tapes used for securing goods in packaging and logistics, was valued at $7.2 billion in 2024 and is projected to reach $11.5 billion by 2035, growing at a compound annual growth rate (CAGR) of 4.9%.

This market serves critical industries including food and beverages, consumer goods, e-commerce, automotive, and household appliances, where strapping ensures product safety, stability during transportation, and prevention of damage or spillage. Key materials like polypropylene (PP) and polyester (PET) dominate, with PP holding over 48% share in 2024, while automatic and semi-automatic machines gain traction for efficiency in high-volume production.

Regionally, Asia-Pacific leads with over 46% market share driven by industrialization in China, India, and Japan, robust exports, and e-commerce growth valued at $2.8 trillion in 2021. North America and Europe follow, fueled by manufacturing resurgence, sustainable packaging demands, and expanding online retail sectors.

Strapping Market Trend Analysis:

Shift Towards Sustainable and Eco-Friendly Strapping Materials

- Manufacturers are increasingly investing in recyclable and biodegradable strapping materials in response to environmental regulations and consumer awareness. Companies are developing eco-friendly coated steel strapping that reduces rust and environmental impact, while also exploring bio-based or compostable strapping options for organic produce and premium brands. This shift addresses growing scrutiny over plastic waste and positions companies for competitive advantage in sustainability-focused markets.

- The transition is particularly evident in the construction and food industries, where regulatory pressure on green building projects and food-contact regulations drive demand for recyclable and compostable solutions. Manufacturers producing strapping that meets both strength and durability requirements while minimizing environmental footprint are gaining market traction. However, the development of alternative materials may increase production costs and affect profit margins in the near term.

- Hybrid strapping systems combining steel and plastic properties are emerging as innovative solutions, such as Teufelberger's hybrid systems designed for applications requiring both high strength and flexibility. These products cater to industries seeking robust performance alongside reduced environmental footprint, particularly in construction and logistics sectors.

Integration of Digital Technologies and IoT-Enabled Strapping Systems

- IoT-enabled strapping machines offering real-time data monitoring and predictive maintenance are becoming increasingly common across manufacturing and logistics operations. Digital platforms for monitoring and managing strapping operations provide benefits such as inventory management, process optimization, and data analytics. This digitalization shift is expected to streamline operations, enhance supply chain transparency, and provide manufacturers with competitive advantages through improved operational efficiencies.

- Semi-automated strapping stations integrated with conveyor sortation systems for touchless pallet build-out represent a major operational trend addressing labor productivity and efficiency. The shift from manual to tool-applied strapping continues, with automated equipment boosting consumption of consistent, high-quality plastic strapping that feeds reliably into tensioners and sealers. These technologies reduce labor time per pallet and minimize packaging waste while supporting higher-throughput logistics facilities.

Material Transition from Steel to Plastic Strapping with Enhanced Specifications

- A measured but consistent transition from steel to plastic strapping, particularly polyester and PET, is occurring across core sectors including logistics, construction, and metals. Plastic strapping offers advantages including lower weight, resistance to corrosion, and superior compatibility with automated equipment. Ultra-high-tensile, low-elongation PET strapping is emerging as a steel alternative for coil banding applications, while polypropylene remains dominant due to cost-effectiveness.

- Specialized plastic strapping variants are gaining traction for specific applications, including anti-static and low-friction strapping for electronics and sensitive cargo, brightly colored or printed strapping for brand visibility and warehouse load identification, and weather-resistant materials like UV-stabilized polypropylene for outdoor storage. Composite and corded strapping are replacing steel in applications where weight, corrosion resistance, or worker safety concerns are paramount.

- The Asia-Pacific region is driving this trend through rapid industrialization and infrastructure development in countries like China and India, where the booming e-commerce sector demands reliable, efficient packaging solutions. Composite strapping for non-marring securement of finished metal surfaces and plastic-coated steel strapping for corrosion resistance represent hybrid approaches capturing diverse market segments.

Strapping Market Segment Analysis:

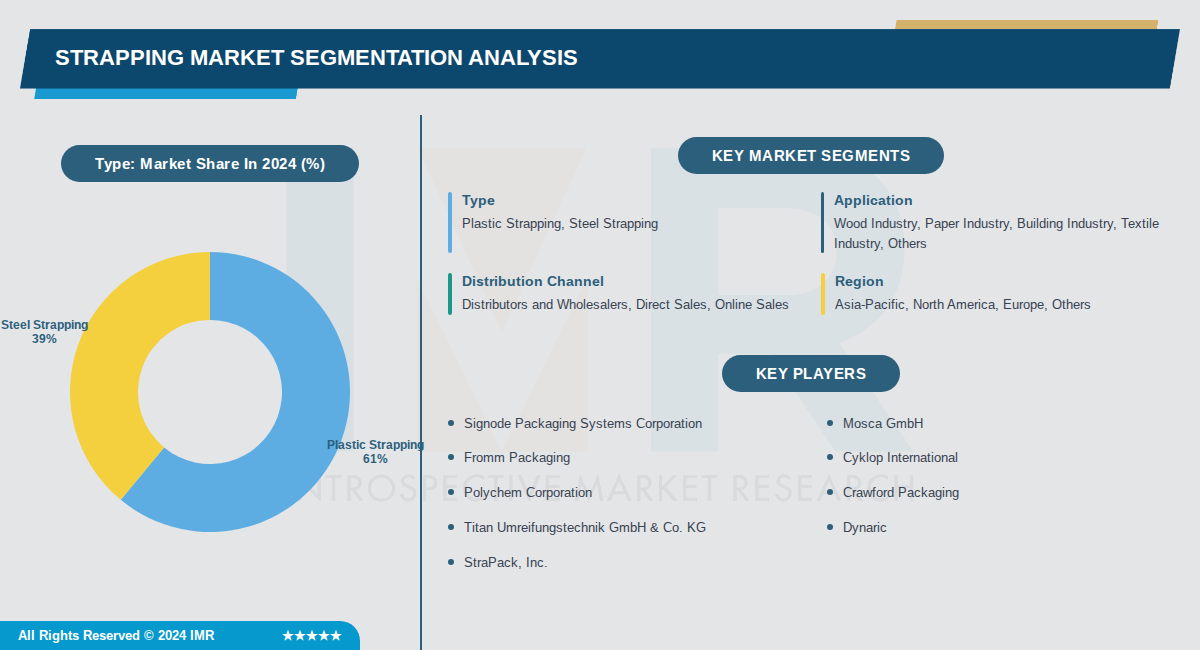

Strapping Market is Segmented on the basis of By Type, By Application, By Distribution Channel

By Type, Plastic Strapping segment is expected to dominate the market during the forecast period

- Plastic strapping dominates due to its lighter weight, lower cost, and greater flexibility compared to steel, making it ideal for a wider range of packaging applications.

- Increasing demand from e-commerce and logistics sectors favors plastic straps for their ease of use and reduced shipping costs, capturing over 60% market share.

By Application, Wood Industry segment is expected to dominate the market during the forecast period

- Wood industry leads due to high-volume bundling needs for lumber, pallets, and timber products during transportation and storage in construction and furniture sectors.

- Robust demand from expanding global construction and woodworking activities drives wood segment growth, supported by automated strapping in sawmills.

By Distribution Channel, Distributors and Wholesalers segment is expected to dominate the market during the forecast period

- Distributors and wholesalers dominate by providing wide accessibility to small and medium businesses across diverse industries requiring varied quantities.

- They bridge manufacturers and end-users efficiently, stocking multiple types like plastic and steel for quick fulfillment in fragmented markets.

By Region, Asia-Pacific segment is expected to dominate the market during the forecast period

- Asia-Pacific leads due to rapid industrialization, booming e-commerce, and manufacturing hubs in China and India driving massive packaging demand.

- High infrastructure development and export-oriented logistics amplify strapping use, with regional share bolstered by cost-effective local production.

Strapping Market Regional Insights:

Asia-Pacific Dominates the Strapping Market Due to Rapid Industrialization and Manufacturing Growth

- Asia-Pacific holds the largest market share in the strapping market, driven by rapid industrialization and infrastructure developments in key countries like China and India. China leads within the region due to its massive manufacturing scale and export-driven economy, while India contributes through accelerating SME upgrades and e-commerce growth. This dominance is evident across multiple reports, with the region commanding around 37.9% share in strapping devices.

- The region's expansive automotive, manufacturing, and e-commerce sectors fuel demand for robust packaging solutions. Infrastructure projects and booming consumer goods industries, particularly in China, India, Japan, and ASEAN nations, necessitate heavy-duty strapping for secure transportation. Favorable regulations supporting export-led growth and cost-competitive production further solidify Asia-Pacific's lead over more mature markets.

- Major players are investing heavily in Asia-Pacific, with local production facilities expanding to meet demand. Recent developments include adoption of automated and semi-automatic strapping systems in manufacturing hubs like China and Japan. Companies such as Signode Industrial Group and Mosca GmbH are focusing on this region for innovation in recyclable materials, aligning with rising sustainability needs in exports.

Active Key Players in the Strapping Market:

- Signode Packaging Systems Corporation (USA)

- Mosca GmbH (Germany)

- Fromm Packaging (Switzerland)

- Cyklop International (Germany)

- Polychem Corporation (USA)

- Crawford Packaging (Canada)

- Titan Umreifungstechnik GmbH & Co. KG (Germany)

- Dynaric (USA)

- StraPack, Inc. (USA)

- Milan Ligocki UNI PACK (Czech Republic)

- Linder GmbH (Germany)

- Teufelberger (Austria)

- Cordstrap (Netherlands)

- Samuel Packaging Systems (USA)

- 3M (USA)

- Avery Dennison (USA)

- Nitto Denko (Japan)

- ZHENDA (China)

- Other Active Players

|

Strapping Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 7.2 Billion |

|

Forecast Period 2024-2035 CAGR: |

4.9 % |

Market Size in 2035: |

USD 11.5 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By Distribution Channel |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Strapping Market by Type (2017-2035)

4.1 Strapping Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Plastic Strapping

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Steel Strapping

Chapter 5: Strapping Market by Application (2017-2035)

5.1 Strapping Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Wood Industry

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Paper Industry

5.5 Building Industry

5.6 Textile Industry

5.7 Others

Chapter 6: Strapping Market by Distribution Channel (2017-2035)

6.1 Strapping Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Distributors and Wholesalers

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Direct Sales

6.5 Online Sales

Chapter 7: Strapping Market by Region (2017-2035)

7.1 Strapping Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Asia-Pacific

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 North America

7.5 Europe

7.6 Others

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Strapping Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 SIGNODE PACKAGING SYSTEMS CORPORATION

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 MOSCA GMBH

8.4 FROMM PACKAGING

8.5 CYKLOP INTERNATIONAL

8.6 POLYCHEM CORPORATION

8.7 CRAWFORD PACKAGING

8.8 TITAN UMREIFUNGSTECHNIK GMBH & CO. KG

8.9 DYNARIC

8.10 STRAPACK

8.11 INC.

8.12 MILAN LIGOCKI UNI PACK

8.13 LINDER GMBH

8.14 TEUFELBERGER

8.15 CORDSTRAP

8.16 SAMUEL PACKAGING SYSTEMS

8.17 3M

8.18 AVERY DENNISON

8.19 NITTO DENKO

8.20 ZHENDA

Chapter 9: Global Strapping Market By Region

9.1 Overview

9.2. North America Strapping Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Strapping Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Strapping Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Strapping Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Strapping Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Strapping Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Strapping Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 7.2 Billion |

|

Forecast Period 2024-2035 CAGR: |

4.9 % |

Market Size in 2035: |

USD 11.5 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By Distribution Channel |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||