Healthcare Cold Chain Monitoring Market Synopsis:

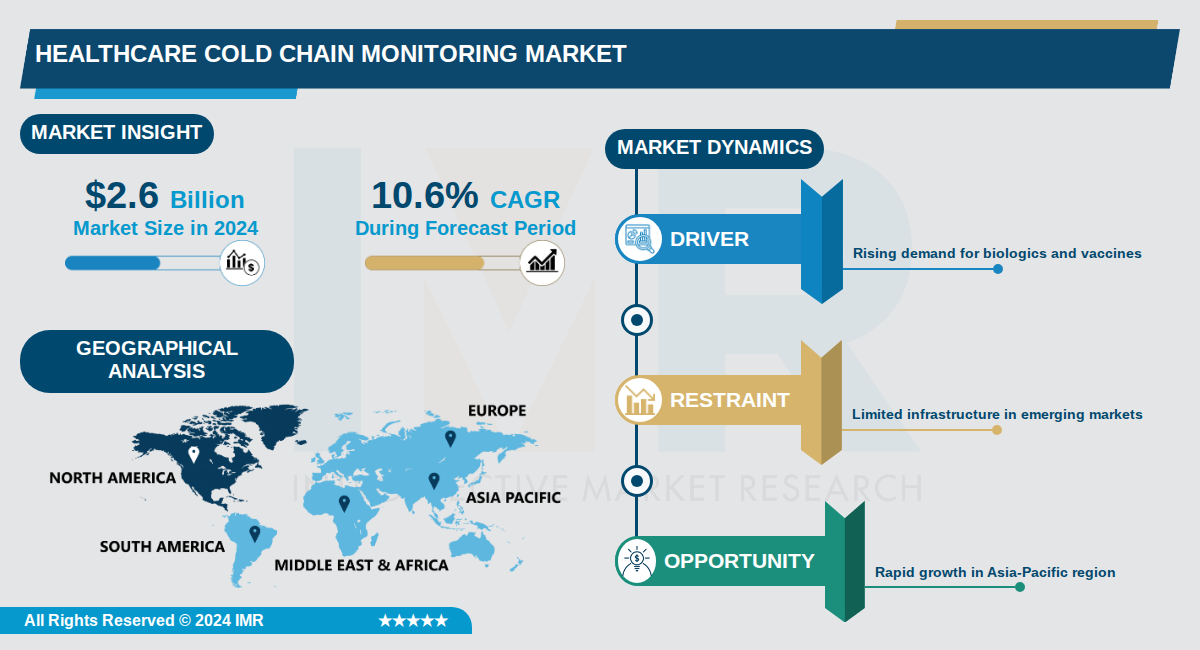

Healthcare Cold Chain Monitoring Market Size Was Valued at USD 2.6 Billion in 2024, and is Projected to Reach USD 8 Billion by 2035, Growing at a CAGR of 10.6% From 2024-2035.

The Healthcare Cold Chain Monitoring Market, valued at $2.6 billion in 2024, is projected to reach $8 billion by 2035, growing at a compound annual growth rate (CAGR) of 10.6%.

This market encompasses technologies and solutions for real-time temperature monitoring of temperature-sensitive healthcare products like vaccines, biologics, and pharmaceuticals throughout the supply chain. North America dominates as the largest region, while Asia-Pacific emerges as the fastest-growing due to expanding healthcare infrastructure and biopharmaceutical production.

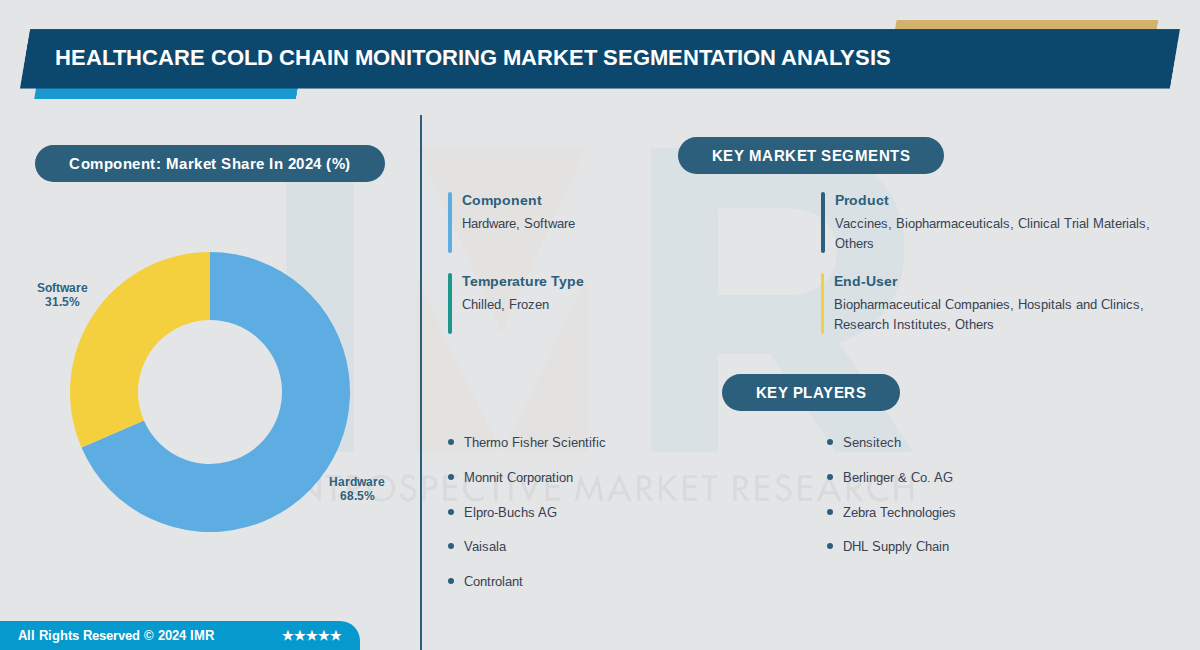

Key segments include hardware, which leads the market, and rapidly growing software driven by digitalization and IoT integration. Major players such as Thermo Fisher Scientific, Sensitech, and Berlinger & Co. AG are advancing IoT sensors, RFID, and cloud analytics for enhanced visibility and compliance.

Healthcare Cold Chain Monitoring Market Trend Analysis:

Shift Towards Cloud-Based Real-Time Monitoring Systems

- Cloud-based monitoring platforms with real-time alert capabilities now account for over 72% of new system implementations, displacing legacy data logger-based monitoring that requires manual download and retrospective analysis. This transition represents a fundamental shift in how organizations manage temperature-sensitive supply chains, enabling immediate notification of temperature excursions rather than discovering problems retroactively.

- IoT-enabled devices and real-time tracking systems are enhancing product safety and supply chain efficiency across the healthcare sector. These advanced technologies deliver end-to-end supply chain visibility with unprecedented data granularity, allowing pharmaceutical manufacturers, logistics service providers, and specialty pharmacies to maintain continuous oversight of temperature-controlled shipments throughout warehousing and transportation.

- The adoption of blockchain-secured audit trail platforms is providing regulators, food safety auditors, and pharmaceutical compliance officers with irrefutable chain-of-custody documentation. This technological convergence of cloud connectivity, IoT sensors, and blockchain creates transparent, tamper-proof records that satisfy stringent regulatory requirements from the FDA, EMA, and WHO.

Expansion of Biologics and Temperature-Sensitive Therapeutics Requiring Ultra-Cold Storage

- The explosion of biologic drugs, mRNA therapeutics, and cell and gene therapy products is expanding both technical requirements and per-shipment monitoring investment within the cold chain monitoring market. These high-value drug categories cannot tolerate any temperature excursion, making comprehensive monitoring a risk management imperative rather than a regulatory checkbox. IAG Cargo reported a 22% year-over-year increase in tonnage for its temperature-controlled Constant Climate product in 2024, emphasizing the growing volume of medical cargo requiring strict oversight.

- The healthcare cold chain monitoring market is driven by increasing demand for biologics and vaccines, as such products often require strict temperature control to ensure their effectiveness. The rising pivot toward high-value, biologically derived treatments such as insulin, gene therapies, and vaccines forces logistics providers to implement advanced data loggers and real-time tracking systems that surpass basic regulatory compliance to maintain total asset visibility.

- The chilled segment, which maintains vaccines, biologics, and pharmaceuticals at 2-8°C, dominates the market with the largest revenue share. This temperature range is essential for preserving the efficacy and safety of these sensitive healthcare products, and the high demand for chilled cold chain solutions across the industry highlights their critical importance for product integrity during storage and transport.

Intensification of Pharmaceutical Regulatory Compliance Mandates and GDP Requirements

- Pharmaceutical cold chain governance is tightening across all major markets, with the EMA's Guidelines on Good Distribution Practice for Medicinal Products for Human Use mandating validated continuous temperature monitoring with calibration-traceable sensor equipment, documented temperature excursion management procedures, and periodic mapping of storage facility thermal profiles. These requirements necessitate purpose-built monitoring technology infrastructure rather than manual periodic checks, creating non-negotiable, recurring investment demand from every pharmaceutical manufacturer and logistics provider.

- FDA 21 CFR Part 211 requirements and WHO prequalification standards enforce validated, continuous temperature monitoring throughout pharmaceutical warehousing and transportation. The post-pandemic pharmaceutical distribution lessons from the ultra-cold COVID-19 vaccine rollout permanently elevated institutional awareness of cold chain integrity as a patient safety and product liability imperative, accelerating the adoption of sophisticated monitoring solutions globally.

- The WHO's Model Guidance for the Storage and Transport of Time and Temperature-Sensitive Pharmaceutical Products is expanding the global regulatory footprint of GDP-aligned cold chain monitoring requirements across the developing world. This regulatory expansion, combined with North America's rigorous FDA pharmaceutical distribution compliance requirements and Europe's stringent EMA GDP guidelines, is driving consistent institutional monitoring platform demand worldwide.

Healthcare Cold Chain Monitoring Market Segment Analysis:

Healthcare Cold Chain Monitoring Market is Segmented on the basis of By Component, By Product, By Temperature Type

By Component, Hardware segment is expected to dominate the market during the forecast period

- Hardware dominates due to the essential role of devices like sensors, data loggers, RFID tools, and temperature detectors in real-time tracking of temperature-sensitive products such as vaccines and biopharmaceuticals.

- These physical components are critical for maintaining precise storage and transport conditions, as any deviation can compromise drug efficacy, driving widespread adoption across the supply chain.

By Product, Vaccines segment is expected to dominate the market during the forecast period

- Vaccines lead due to their pivotal role in public health initiatives, routine immunizations, and global distribution programs requiring stringent temperature control between 2-8°C.

- High-volume demand from vaccination campaigns and the need for reliable cold chain integrity during storage and transport solidify vaccines as the largest segment.

By Temperature Type, Chilled segment is expected to dominate the market during the forecast period

- Chilled dominates because most vaccines, biologics, and pharmaceuticals require maintenance at 2-8°C to preserve efficacy and safety, making it essential for the majority of healthcare products.

- The widespread use of chilled solutions across biopharma storage and logistics exceeds frozen needs, driven by the volume of temperature-sensitive items in routine distribution.

By End-User, Biopharmaceutical Companies segment is expected to dominate the market during the forecast period

- Biopharmaceutical companies lead due to the surging demand for complex biologics derived from living cells, necessitating advanced cold chain monitoring for quality and regulatory compliance.

- Stringent temperature control requirements for these high-value, sensitive products during production, storage, and transportation fuel their dominant position in the market.

Healthcare Cold Chain Monitoring Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast Period

- North America dominates the healthcare cold chain monitoring market, with the U.S. leading due to its developed economy and high demand from biopharmaceutical companies, hospitals, clinics, and research institutes. Canada also contributes significantly through large-scale vaccination programs and government investments in healthcare infrastructure. This regional leadership is evident as North America held the largest market share in 2024.

- The region benefits from advanced infrastructure and stringent regulations, including FDA guidelines and Health Canada's compliance standards for temperature-sensitive products. Widespread adoption of cold chain monitoring technology is recognized as a global technical standard, supported by adaptive business processes and specialized storage and transportation solutions. These factors ensure product efficacy and drive market growth.

- Key players such as Carrier Global Corporation, Testo SE & Co. KGaA, Monnit Corporation, Berlinger & Co. AG, and Emerson Electric Co. are prominent in the region. Recent developments include investments in validated monitoring systems and adherence to Good Distribution Practices (GDP) to maintain product quality. These efforts underscore North America's position in innovation and adoption of advanced cold chain solutions.

Active Key Players in the Healthcare Cold Chain Monitoring Market:

- Thermo Fisher Scientific (USA)

- Sensitech (USA)

- Monnit Corporation (USA)

- Berlinger & Co. AG (Switzerland)

- Elpro-Buchs AG (Switzerland)

- Zebra Technologies (USA)

- Vaisala (Finland)

- DHL Supply Chain (Germany)

- Controlant (Iceland)

- Emerson Electric (USA)

- Honeywell International (USA)

- Descartes Systems Group (Canada)

- Digi International (USA)

- Cold Chain Technologies (USA)

- Testo SE & Co. KGaA (Germany)

- ORBCOMM (USA)

- Carrier (USA)

- Cryoport Inc. (USA)

- Lineage Logistics (USA)

- Other Active Players

|

Healthcare Cold Chain Monitoring Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 2.6 Billion |

|

Forecast Period 2024-2035 CAGR: |

10.6 % |

Market Size in 2035: |

USD 8 Billion |

|

Segments Covered: |

By Component |

|

|

|

By Product |

|

||

|

By Temperature Type |

|

||

|

By End-User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Healthcare Cold Chain Monitoring Market by Component (2017-2035)

4.1 Healthcare Cold Chain Monitoring Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Hardware

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Software

Chapter 5: Healthcare Cold Chain Monitoring Market by Product (2017-2035)

5.1 Healthcare Cold Chain Monitoring Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Vaccines

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Biopharmaceuticals

5.5 Clinical Trial Materials

5.6 Others

Chapter 6: Healthcare Cold Chain Monitoring Market by Temperature Type (2017-2035)

6.1 Healthcare Cold Chain Monitoring Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Chilled

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Frozen

Chapter 7: Healthcare Cold Chain Monitoring Market by End-User (2017-2035)

7.1 Healthcare Cold Chain Monitoring Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Biopharmaceutical Companies

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Hospitals and Clinics

7.5 Research Institutes

7.6 Others

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Healthcare Cold Chain Monitoring Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 THERMO FISHER SCIENTIFIC

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 SENSITECH

8.4 MONNIT CORPORATION

8.5 BERLINGER & CO. AG

8.6 ELPRO-BUCHS AG

8.7 ZEBRA TECHNOLOGIES

8.8 VAISALA

8.9 DHL SUPPLY CHAIN

8.10 CONTROLANT

8.11 EMERSON ELECTRIC

8.12 HONEYWELL INTERNATIONAL

8.13 DESCARTES SYSTEMS GROUP

8.14 DIGI INTERNATIONAL

8.15 COLD CHAIN TECHNOLOGIES

8.16 TESTO SE & CO. KGAA

8.17 ORBCOMM

8.18 CARRIER

8.19 CRYOPORT INC.

8.20 LINEAGE LOGISTICS

Chapter 9: Global Healthcare Cold Chain Monitoring Market By Region

9.1 Overview

9.2. North America Healthcare Cold Chain Monitoring Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Healthcare Cold Chain Monitoring Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Healthcare Cold Chain Monitoring Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Healthcare Cold Chain Monitoring Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Healthcare Cold Chain Monitoring Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Healthcare Cold Chain Monitoring Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Healthcare Cold Chain Monitoring Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 2.6 Billion |

|

Forecast Period 2024-2035 CAGR: |

10.6 % |

Market Size in 2035: |

USD 8 Billion |

|

Segments Covered: |

By Component |

|

|

|

By Product |

|

||

|

By Temperature Type |

|

||

|

By End-User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||