Cellulose Fiber Market Synopsis:

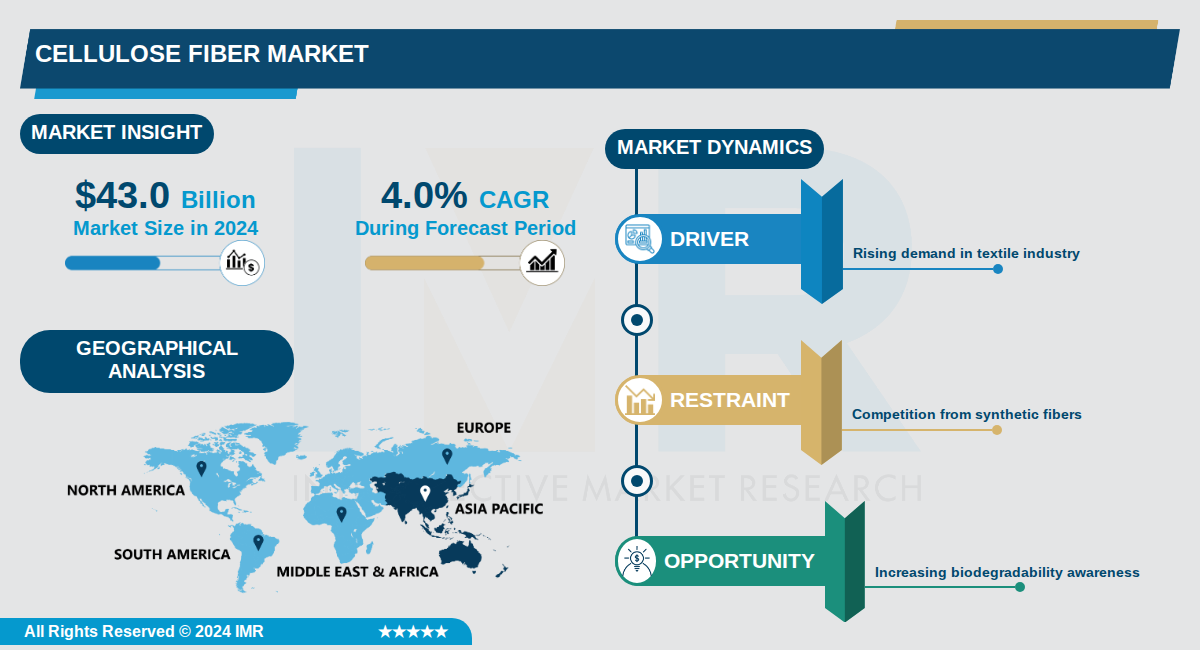

Cellulose Fiber Market Size Was Valued at USD 43.0 Billion in 2024, and is Projected to Reach USD 67.0 Billion by 2035, Growing at a CAGR of 4.0% From 2024-2035.

The global cellulose fiber market, valued at $43.0 billion in 2024, is projected to reach $67.0 billion by 2035, growing at a compound annual growth rate (CAGR) of 4.0%. This expansion reflects the increasing demand for sustainable, biodegradable materials derived from natural sources such as wood pulp, cotton, and other plant-based materials, which offer superior properties like high tensile strength, moisture absorption, and thermal regulation.

Cellulose fibers find extensive applications across industries including textiles (apparel and hygiene products), industrial uses (paper, composites, and filtration), and emerging sectors like construction and biomedical. Key segments include natural and synthetic types, with Asia Pacific dominating due to its significant market share, driven by robust manufacturing and consumer demand for eco-friendly alternatives to petrochemical fibers.

Major players such as Aditya Birla Management Corp., Celanese Corp., and Daicel Corp. are innovating in production processes like pulping and nanofiber development to enhance fiber quality and sustainability. The market's growth is supported by trends toward circular economy principles, with ongoing research into bacterial nanocellulose and lignin removal techniques expanding potential uses.

Cellulose Fiber Market Trend Analysis:

Rise of Sustainable Man-Made Cellulosic Fibers

- Major brands like Tencel are integrating lyocell and modal fibers into their clothing lines due to their breathability, softness, and moisture absorption properties, driving the textile segment to hold 47% market share in 2025. The fashion industry is shifting from synthetic polyester, which dominates 62.8% of the market, towards these biodegradable alternatives amid growing environmental scrutiny. Closed-loop viscose production systems are recovering 60-70% of chemicals and using one-third less water, making production more efficient and appealing to eco-conscious consumers.

- In Asia Pacific, which accounts for over 40% of global production, China's large-scale lyocell facilities and India's textile hubs in apparel and technical textiles are accelerating adoption. Companies are investing in certified wood sources for viscose and cellulose acetate, supporting premium home textiles and activewear. This shift positions cellulosic fibers to capture market share from petrochemical-based synthetics as regulations tighten.

- Natural cellulose fibers, comprising 70% of the market per some analyses, are growing due to their renewability and use in construction and fashion, with the natural segment expected to expand significantly through 2035 at a 4.76% CAGR.

Advancements in Nanocellulose Technologies

- Utilization of cellulose nanofibrils (CNFs) and cellulose nanocrystals (CNCs) is enhancing mechanical properties, biocompatibility, and biodegradability of fibers, boosting applications in industrial textiles like curtains and upholstery. These innovations are key to the industrial segment's notable growth, leveraging properties such as high absorbency and strength for filtration, paper production, and insulation. Vyansa Intelligence projects the market to reach USD 550 million by 2032 at 11.92% CAGR, partly fueled by these tech upgrades.

- In technical textiles and protective apparel, nanocellulose enables high-performance products meeting building codes for energy efficiency, with Asia Pacific governments sponsoring programs for specialty cellulose. North America sees rising demand in hygiene and biomedical sectors, where nano-enhanced fibers improve durability over traditional synthetics.

Expansion of Cellulose in Technical and Industrial Applications

- The industrial segment is surging due to cellulose fibers' unique properties in construction insulation, nonwoven fabrics, and sustainable packaging, with rapidly expanding paper and building sectors propelling demand. In Asia Pacific, India's integration of cellulosic fibers into technical textiles and Bangladesh's export-oriented manufacturing are key, supported by low-cost labor and biomass resources. This trend aligns with global pushes for versatile, cost-effective biodegradable materials replacing synthetics.

- Government policies in Asia Pacific promote plant-based sources over petrochemicals, enhancing applications in bio-based composites and high-value apparel. Europe's focus on green textiles and North America's hygiene industry further drive this shift, with market projections showing steady growth to USD 72.94 billion by 2035.

Cellulose Fiber Market Segment Analysis:

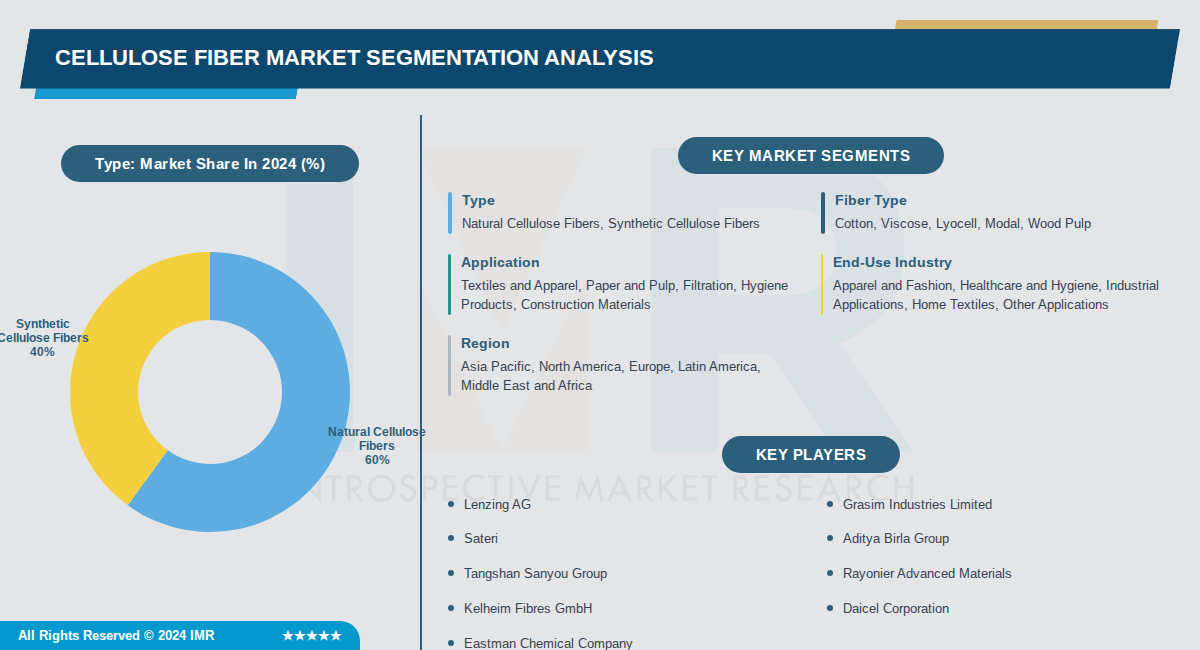

Cellulose Fiber Market is Segmented on the basis of By Type, By Fiber Type, By Application

By Type, Natural Cellulose Fibers segment is expected to dominate the market during the forecast period

- Natural cellulose fibers derived from cotton and wood pulp dominate with over 60% market share due to their biodegradability, environmental compliance, and established supply chains across textile and apparel industries.

- Rising environmental regulations and corporate sustainability commitments globally have accelerated preference for natural fibers, with major fashion brands increasingly adopting natural cellulose-based materials to meet consumer demand for eco-friendly products.

By Fiber Type, Cotton segment is expected to dominate the market during the forecast period

- Cotton leads the fiber type segmentation with 40% share due to its centuries-old cultivation infrastructure, widespread consumer familiarity, and versatility across apparel, home textiles, and industrial applications.

- Viscose maintains 25% share as a cost-effective regenerated cellulose fiber with superior drape properties, making it the preferred choice for mid-range fashion and textile manufacturers seeking balance between performance and affordability.

By Application, Textiles and Apparel segment is expected to dominate the market during the forecast period

- Textiles and apparel dominate with 47% market share driven by global fashion industry growth, increasing consumer preference for natural and sustainable clothing materials, and expanding middle-class populations in Asia Pacific demanding apparel products.

- Paper and pulp maintains 31.3% share as a mature, stable segment leveraging cellulose fibers for specialty papers, packaging materials, and tissue products with consistent industrial demand and established manufacturing relationships.

By End-Use Industry, Apparel and Fashion segment is expected to dominate the market during the forecast period

- Apparel and fashion command 45% of the market as primary drivers of cellulose fiber demand, with major brands integrating viscose, modal, and lyocell into collections to meet consumer sustainability expectations and regulatory requirements in EU and North America.

- Healthcare and hygiene applications account for 20% share through expanding demand for medical textiles, surgical materials, and absorbent hygiene products where cellulose fibers provide superior absorbency, breathability, and hypoallergenic properties.

By Region, Asia Pacific segment is expected to dominate the market during the forecast period

- Asia Pacific dominates with 42% regional share due to well-established textile sectors, abundant raw material resources for cellulose production, and major manufacturing hubs in China, India, and Bangladesh serving global fashion supply chains.

- North America and Europe combined account for 42% share through stringent environmental regulations driving sustainable fiber adoption, strong consumer willingness to pay premium prices for eco-friendly textiles, and significant investments in advanced cellulose production technologies.

Cellulose Fiber Market Regional Insights:

Asia Pacific Dominates the Global Cellulose Fiber Market with Over 40% Market Share

- Asia Pacific commands over 40% of global cellulose fiber production and consumption, making it the largest regional segment by a substantial margin. China leads the region as the largest producer and consumer of viscose fibers globally, with major companies like Sateri, Tangshan Sanyou, and Yibin Grace dominating global supply. India and Bangladesh have emerged as major textile hubs, benefiting from favorable labor structures and strong export-oriented ecosystems that drive cellulose fiber consumption across apparel categories.

- The region's dominance is anchored by well-established textile and apparel manufacturing sectors, abundant raw material resources, and advanced production technologies. Asia Pacific contains crucial feedstock availability and benefits from government-backed industrial upgrading programs that support sustainability initiatives. The rapid growth of textile supply chains, particularly in India, is focused on integrating cellulosic fibers into both high-value apparel and technical textile sectors, with rising urbanization and increasing disposable incomes driving consumption of apparel, hygiene products, and home textiles.

- Major developments include the commissioning of multiple large-scale lyocell facilities in China and the scaling of sustainable fiber production across Southeast Asian nations. Companies like Birla Cellulose in India and Sateri in China are serving global product demand. Asia Pacific is expected to remain the largest region through 2035, with the region's cluster effect intensifying competition while creating opportunities for strategic alliances and technology transfer among global players.

Active Key Players in the Cellulose Fiber Market:

- Lenzing AG (Austria)

- Grasim Industries Limited (India)

- Sateri (China)

- Aditya Birla Group (India)

- Tangshan Sanyou Group (China)

- Rayonier Advanced Materials (USA)

- Kelheim Fibres GmbH (Germany)

- Daicel Corporation (Japan)

- Eastman Chemical Company (USA)

- Sappi Limited (South Africa)

- Fulida Group Holding Co. Ltd (China)

- Celotech Chemical Co., Ltd. (China)

- Asahi Kasei Corporation (Japan)

- CFF GmbH & Co. KG (Germany)

- Borregaard AS (Norway)

- Spinnova Plc (Finland)

- China Bambro Textile Co. Ltd (China)

- Shandong Helon Textile Sci. & Tech. Co. Ltd (China)

- Indo Bharat Rayon Limited (India)

- Södra Cell AB (Sweden)

- Other Active Players

|

Cellulose Fiber Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 43.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

4.0 % |

Market Size in 2035: |

USD 67.0 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Fiber Type |

|

||

|

By Application |

|

||

|

By End-Use Industry |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Cellulose Fiber Market by Type (2017-2035)

4.1 Cellulose Fiber Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Natural Cellulose Fibers

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Synthetic Cellulose Fibers

Chapter 5: Cellulose Fiber Market by Fiber Type (2017-2035)

5.1 Cellulose Fiber Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Cotton

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Viscose

5.5 Lyocell

5.6 Modal

5.7 Wood Pulp

Chapter 6: Cellulose Fiber Market by Application (2017-2035)

6.1 Cellulose Fiber Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Textiles and Apparel

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Paper and Pulp

6.5 Filtration

6.6 Hygiene Products

6.7 Construction Materials

Chapter 7: Cellulose Fiber Market by End-Use Industry (2017-2035)

7.1 Cellulose Fiber Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Apparel and Fashion

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Healthcare and Hygiene

7.5 Industrial Applications

7.6 Home Textiles

7.7 Other Applications

Chapter 8: Cellulose Fiber Market by Region (2017-2035)

8.1 Cellulose Fiber Market Snapshot and Growth Engine

8.2 Market Overview

8.3 Asia Pacific

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

8.3.3 Key Market Trends, Growth Factors, and Opportunities

8.3.4 Geographic Segmentation Analysis

8.4 North America

8.5 Europe

8.6 Latin America

8.7 Middle East and Africa

Chapter 9: Company Profiles and Competitive Analysis

9.1 Competitive Landscape

9.1.1 Competitive Benchmarking

9.1.2 Cellulose Fiber Market Share by Manufacturer/Service Provider (2024)

9.1.3 Industry BCG Matrix

9.1.4 Partnerships, Mergers & Acquisitions

9.2 LENZING AG

9.2.1 Company Overview

9.2.2 Key Executives

9.2.3 Company Snapshot

9.2.4 Role of the Company in the Market

9.2.5 Sustainability and Social Responsibility

9.2.6 Operating Business Segments

9.2.7 Product Portfolio

9.2.8 Business Performance

9.2.9 Recent News & Developments

9.2.10 SWOT Analysis

9.3 GRASIM INDUSTRIES LIMITED

9.4 SATERI

9.5 ADITYA BIRLA GROUP

9.6 TANGSHAN SANYOU GROUP

9.7 RAYONIER ADVANCED MATERIALS

9.8 KELHEIM FIBRES GMBH

9.9 DAICEL CORPORATION

9.10 EASTMAN CHEMICAL COMPANY

9.11 SAPPI LIMITED

9.12 FULIDA GROUP HOLDING CO. LTD

9.13 CELOTECH CHEMICAL CO.

9.14 LTD.

9.15 ASAHI KASEI CORPORATION

9.16 CFF GMBH & CO. KG

9.17 BORREGAARD AS

9.18 SPINNOVA PLC

9.19 CHINA BAMBRO TEXTILE CO. LTD

9.20 SHANDONG HELON TEXTILE SCI. & TECH. CO. LTD

9.21 INDO BHARAT RAYON LIMITED

9.22 SÖDRA CELL AB

Chapter 10: Global Cellulose Fiber Market By Region

10.1 Overview

10.2. North America Cellulose Fiber Market

10.2.1 Key Market Trends, Growth Factors and Opportunities

10.2.2 Top Key Companies

10.2.3 Historic and Forecasted Market Size by Segments

10.2.4 Historic and Forecast Market Size by Country

10.3. Eastern Europe Cellulose Fiber Market

10.3.1 Key Market Trends, Growth Factors and Opportunities

10.3.2 Top Key Companies

10.3.3 Historic and Forecasted Market Size by Segments

10.3.4 Historic and Forecast Market Size by Country

10.4. Western Europe Cellulose Fiber Market

10.4.1 Key Market Trends, Growth Factors and Opportunities

10.4.2 Top Key Companies

10.4.3 Historic and Forecasted Market Size by Segments

10.4.4 Historic and Forecast Market Size by Country

10.5. Asia Pacific Cellulose Fiber Market

10.5.1 Key Market Trends, Growth Factors and Opportunities

10.5.2 Top Key Companies

10.5.3 Historic and Forecasted Market Size by Segments

10.5.4 Historic and Forecast Market Size by Country

10.6. Middle East & Africa Cellulose Fiber Market

10.6.1 Key Market Trends, Growth Factors and Opportunities

10.6.2 Top Key Companies

10.6.3 Historic and Forecasted Market Size by Segments

10.6.4 Historic and Forecast Market Size by Country

10.7. South America Cellulose Fiber Market

10.7.1 Key Market Trends, Growth Factors and Opportunities

10.7.2 Top Key Companies

10.7.3 Historic and Forecasted Market Size by Segments

10.7.4 Historic and Forecast Market Size by Country

Chapter 11: Analyst Viewpoint and Conclusion

Chapter 12: Research Methodology

12.1 Research Process

12.2 Primary Research

12.3 Secondary Research

Chapter 13: Case Study

Chapter 14: Appendix

14.1 Sources

14.2 List of Tables and Figures

14.3 Short Forms and Citations

14.4 Assumption and Conversion

14.5 Disclaimer

|

Cellulose Fiber Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 43.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

4.0 % |

Market Size in 2035: |

USD 67.0 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Fiber Type |

|

||

|

By Application |

|

||

|

By End-Use Industry |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||