Biomass Pellets Market Synopsis:

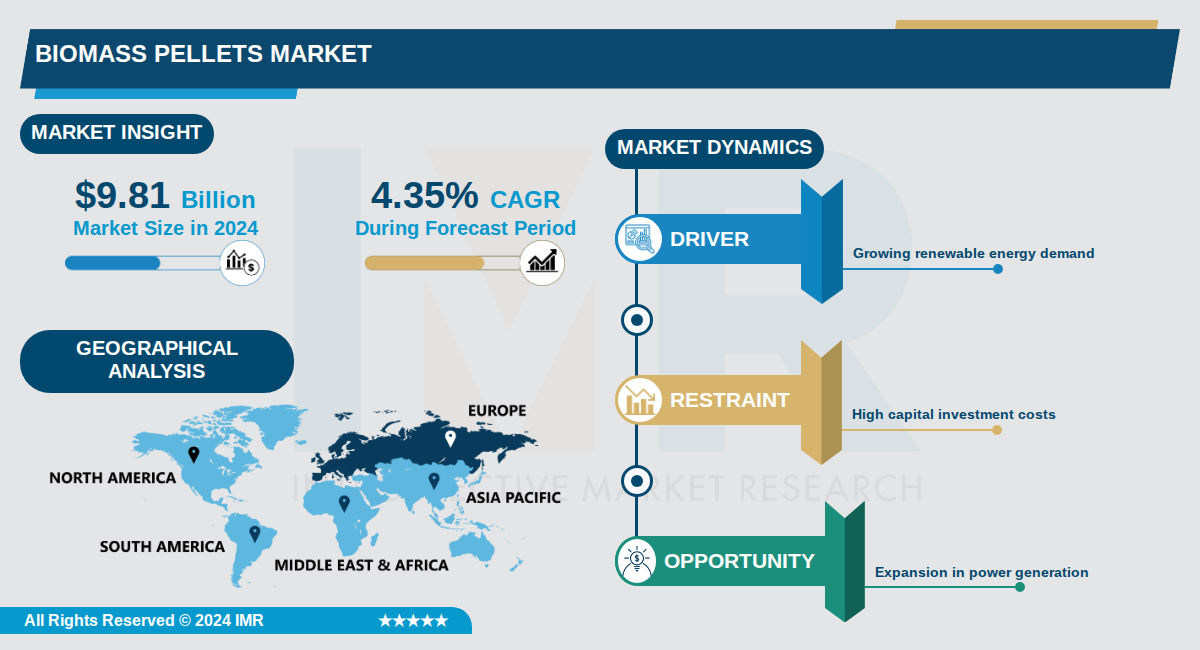

Biomass Pellets Market Size Was Valued at USD 9.81 Billion in 2024, and is Projected to Reach USD 14.78 Billion by 2035, Growing at a CAGR of 4.35% From 2024-2035.

The global biomass pellets market, valued at $9.81 billion in 2024, is projected to reach $14.78 billion by 2035, growing at a compound annual growth rate (CAGR) of 4.35%. This expansion reflects the increasing shift toward renewable energy sources amid rising demand for sustainable heating and power generation solutions. Biomass pellets, primarily derived from wood, agricultural residues, and energy crops, offer high energy density, efficient combustion, and lower emissions compared to traditional fossil fuels.

Regionally, Europe holds a dominant position with a significant market share, driven by stringent emission regulations and commitments to net-zero carbon goals, particularly in countries like Germany and the UK. North America remains a key market, supported by industrial applications and government subsidies such as the U.S. Rural Energy for America Program. Asia-Pacific is the fastest-growing region, fueled by abundant agricultural waste in nations like India and China, alongside rapid urbanization and supportive renewable energy policies.

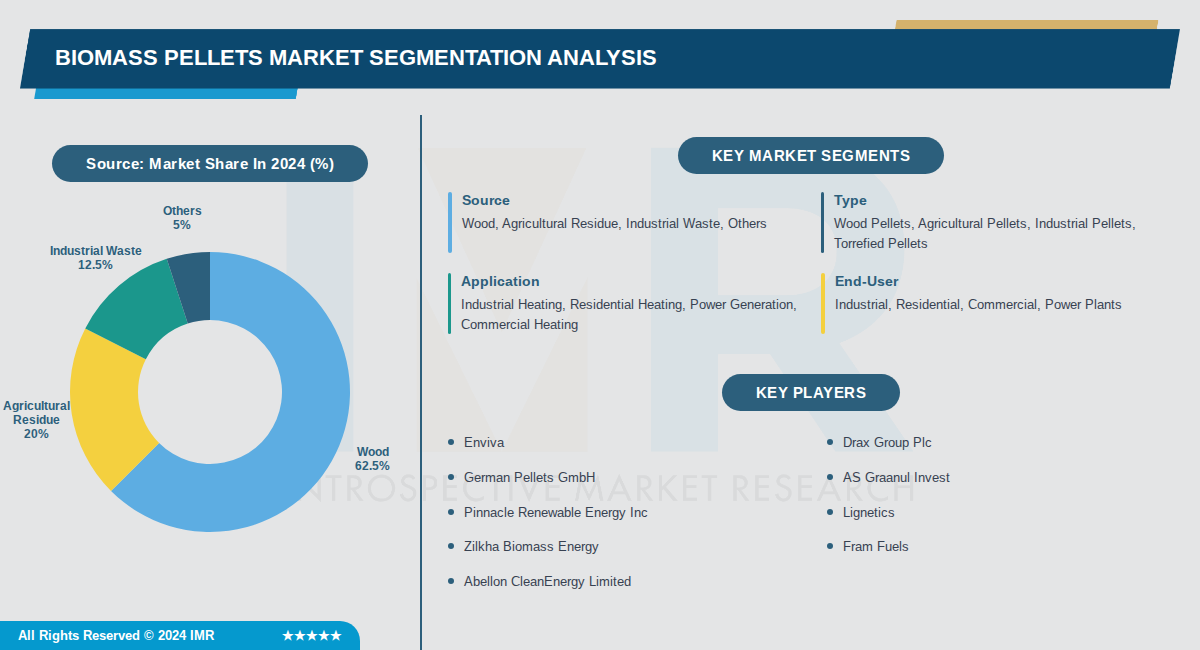

Market segmentation highlights wood pellets as the leading type, accounting for over 60% share due to their durability, ease of handling, and environmental benefits. The industrial sector, including power generation and heating, dominates applications, while emerging segments like energy crops and torrefied pellets are gaining traction for their enhanced properties and reduced emissions.

Biomass Pellets Market Trend Analysis:

Technological Advancement in Pellet Production and Mill Efficiency

- The biomass pellet industry is experiencing significant innovation in production technology, with a scale-up trend toward mega-plants exceeding 1 million tons annual capacity. These facilities require ultra-high-capacity mill lines and advanced process control systems, representing a major shift from smaller, traditional production models.

- Integration of AI and real-time optimization systems is becoming standard practice, with manufacturers implementing advanced process control and AI to optimize die pressure and temperature during production. This technological integration directly reduces operational costs, with mill energy efficiency measured in kWh/ton becoming a major competitive differentiator among producers.

- Development of specialized mills for torrefied biomass and blended feedstock pellets demonstrates the industry's commitment to processing diverse raw materials more efficiently. Companies are also investing in wear-resistant die and roller materials to handle contaminated post-consumer wood, extending equipment lifespan and reducing production downtime.

Sustainable Sourcing and Responsible Forest Management Practices

- The market is witnessing a fundamental shift toward sustainable sourcing practices with explicit focus on reducing deforestation and promoting responsible forest management. This commitment to environmental responsibility is gaining critical importance among consumers and directly influencing purchasing decisions, particularly in mature markets like Europe and North America.

- Emphasis on converting agricultural residues into standardized fuel pellets has expanded significantly, with technology enabling efficient processing of crop waste to meet stringent EU and North American sustainability standards. By 2030-31, biomass availability from agricultural residues is expected to increase to 283 million tonnes, with associated CO2 mitigation potential of 209 million tonnes from coal replacement.

- Regional initiatives in China and India are driving adoption of sustainable practices through government incentives for agro-waste utilization, with local manufacturers like Anyang GEMCO and FANWAY developing compact, mobile units for small-scale farms. This contrasts with mature markets focusing on premium automation upgrades while maintaining environmental accountability.

Expansion of Biomass Pellets into Industrial and Power Generation Applications

- Industrial applications now dominate the market, capturing 42.87% market share in 2026, with the industrial sector under increasing pressure to reduce carbon emissions and shift toward renewable energy sources. Industries such as cement, chemicals, food processing, pulp and paper, and metal processing are rapidly adopting wood pellets as a carbon-neutral alternative to oil and gas for heating and process applications.

- Power generation represents the dominant market force within the biomass pellet industry, driven by increasing demand for renewable energy to meet climate targets and continuous development of efficient biomass-fired power plants. Europe leads with 30% market share in 2025, with wood pellets used in combined heat and power (CHP) plants and dedicated power generation facilities generating electricity at scale.

- The building heating segment is experiencing significant growth at a CAGR of 9.2% from 2026 to 2032, with bio-pellets replacing coal or fossil fuels in co-firing industrial heating systems. Total pellet use for residential heating increased from 14.3 million in 2020 to 15.9 million in 2021, while commercial heating increased from 5.5 million to 6.1 million during the same period.

Biomass Pellets Market Segment Analysis:

Biomass Pellets Market is Segmented on the basis of By Source, By Type, By Application

By Source, Wood segment is expected to dominate the market during the forecast period

- Wood dominates due to its high energy density, low moisture content, and established supply chains from sawmills and forestry residues.

- Widely used in residential heating, power plants, and industrial furnaces across Europe and North America, supported by favorable policies and certifications.

By Type, Wood Pellets segment is expected to dominate the market during the forecast period

- Wood pellets lead with superior combustion efficiency, uniform quality, and compatibility with existing heating systems and boilers.

- They capture over 60% market share globally due to strong demand in residential and utility co-firing applications in key regions like Europe.

By Application, Industrial Heating segment is expected to dominate the market during the forecast period

- Industrial heating dominates as biomass pellets provide cost-effective, sustainable alternatives to fossil fuels in furnaces and boilers.

- High adoption in power plants for co-firing reduces carbon emissions and supports renewable energy transitions mandated by regulations.

By End-User, Industrial segment is expected to dominate the market during the forecast period

- Industrial end-users lead due to large-scale adoption for heating and power generation, replacing coal and oil amid emission regulations.

- Pellets offer reliable energy density and lower operational costs, driving over 40% market share in manufacturing and utility sectors.

Biomass Pellets Market Regional Insights:

Europe Dominates the Biomass Pellets Market with Over 52% Market Share

- Europe commands approximately 52.3% of the global wood pellets market share in 2025, making it the clear market leader. The region's dominance is driven by the United Kingdom and Germany, which are the biggest consuming nations. Germany alone is expected to maintain a 31.2% market share in Western Europe in 2025, supported by its extensive residential pellet heating infrastructure and widespread boiler installations.

- The region benefits from long-established renewable energy requirements, stringent carbon reduction targets, and well-developed biomass infrastructure that facilitates both production and consumption. Europe's regulatory environment has created sustained demand for biomass as countries transition away from fossil fuels, with co-firing in power plants and residential heating serving as primary consumption drivers.

- Western Europe's biomass pellets market is projected to grow from USD 4.1 billion in 2025 to USD 7.4 billion by 2035, registering a 6.0% CAGR. Italy and Spain also contribute significantly with 12.7% and 7.3% market shares respectively, while Nordic countries and nations like Austria and the Netherlands are expanding their biomass pellet adoption through emerging renewable heating programs.

Active Key Players in the Biomass Pellets Market:

- Enviva (USA)

- Drax Group Plc (UK)

- German Pellets GmbH (Germany)

- AS Graanul Invest (Estonia)

- Pinnacle Renewable Energy Inc (Canada)

- Lignetics (USA)

- Zilkha Biomass Energy (USA)

- Fram Fuels (USA)

- Abellon CleanEnergy Limited (India)

- Ecostan (India)

- JP Green Fuels (India)

- The Westervelt Company, Inc (USA)

- Forest Energy Corporation (USA)

- New England Wood Pellet (USA)

- Premium Pellet Ltd. (Ireland)

- BIOMAC Energy Ltd (Czech Republic)

- Pacific BioEnergy Corporation (Canada)

- Energex Corporation (USA)

- Other Active Players

|

Biomass Pellets Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 9.81 Billion |

|

Forecast Period 2024-2035 CAGR: |

4.35 % |

Market Size in 2035: |

USD 14.78 Billion |

|

Segments Covered: |

By Source |

|

|

|

By Type |

|

||

|

By Application |

|

||

|

By End-User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Biomass Pellets Market by Source (2017-2035)

4.1 Biomass Pellets Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Wood

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Agricultural Residue

4.5 Industrial Waste

4.6 Others

Chapter 5: Biomass Pellets Market by Type (2017-2035)

5.1 Biomass Pellets Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Wood Pellets

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Agricultural Pellets

5.5 Industrial Pellets

5.6 Torrefied Pellets

Chapter 6: Biomass Pellets Market by Application (2017-2035)

6.1 Biomass Pellets Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Industrial Heating

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Residential Heating

6.5 Power Generation

6.6 Commercial Heating

Chapter 7: Biomass Pellets Market by End-User (2017-2035)

7.1 Biomass Pellets Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Industrial

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Residential

7.5 Commercial

7.6 Power Plants

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Biomass Pellets Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 ENVIVA

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 DRAX GROUP PLC

8.4 GERMAN PELLETS GMBH

8.5 AS GRAANUL INVEST

8.6 PINNACLE RENEWABLE ENERGY INC

8.7 LIGNETICS

8.8 ZILKHA BIOMASS ENERGY

8.9 FRAM FUELS

8.10 ABELLON CLEANENERGY LIMITED

8.11 ECOSTAN

8.12 JP GREEN FUELS

8.13 THE WESTERVELT COMPANY

8.14 INC

8.15 FOREST ENERGY CORPORATION

8.16 NEW ENGLAND WOOD PELLET

8.17 PREMIUM PELLET LTD.

8.18 BIOMAC ENERGY LTD

8.19 PACIFIC BIOENERGY CORPORATION

8.20 ENERGEX CORPORATION

Chapter 9: Global Biomass Pellets Market By Region

9.1 Overview

9.2. North America Biomass Pellets Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Biomass Pellets Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Biomass Pellets Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Biomass Pellets Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Biomass Pellets Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Biomass Pellets Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Biomass Pellets Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 9.81 Billion |

|

Forecast Period 2024-2035 CAGR: |

4.35 % |

Market Size in 2035: |

USD 14.78 Billion |

|

Segments Covered: |

By Source |

|

|

|

By Type |

|

||

|

By Application |

|

||

|

By End-User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||