Thermal Laminating Film Market Synopsis:

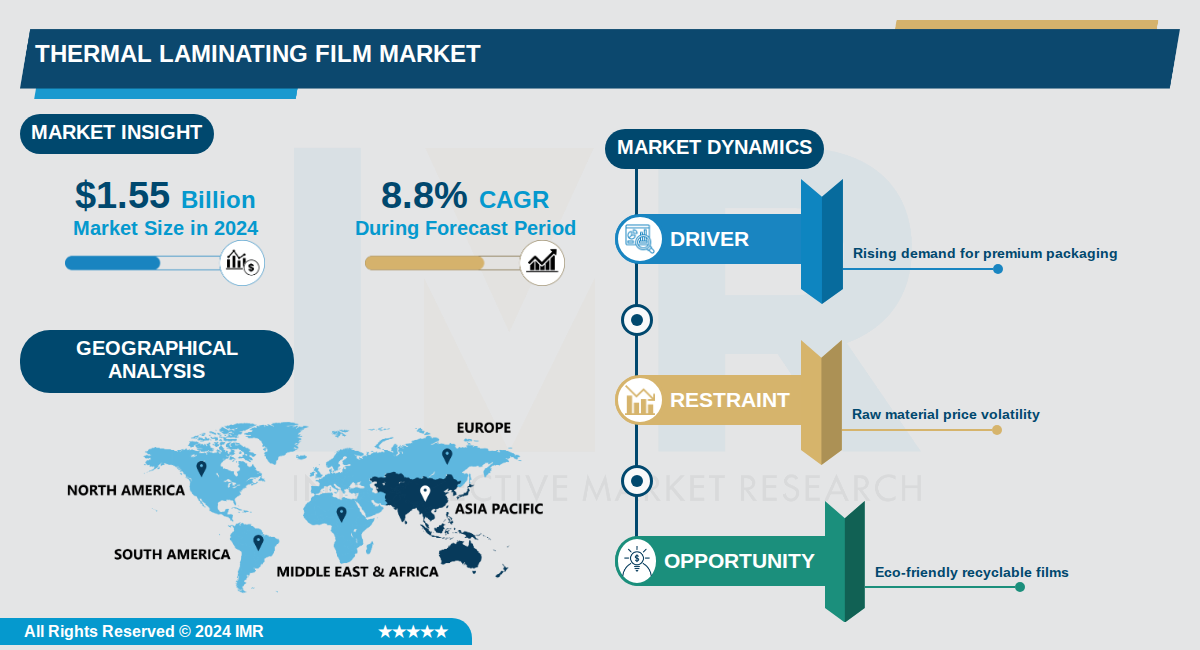

Thermal Laminating Film Market Size Was Valued at USD 1.55 Billion in 2024, and is Projected to Reach USD 3.6 Billion by 2035, Growing at a CAGR of 8.8% From 2024-2035.

The global Thermal Laminating Film Market, valued at $1.55 billion in 2024, is projected to reach $3.6 billion by 2035, growing at a compound annual growth rate (CAGR) of 8.8%.

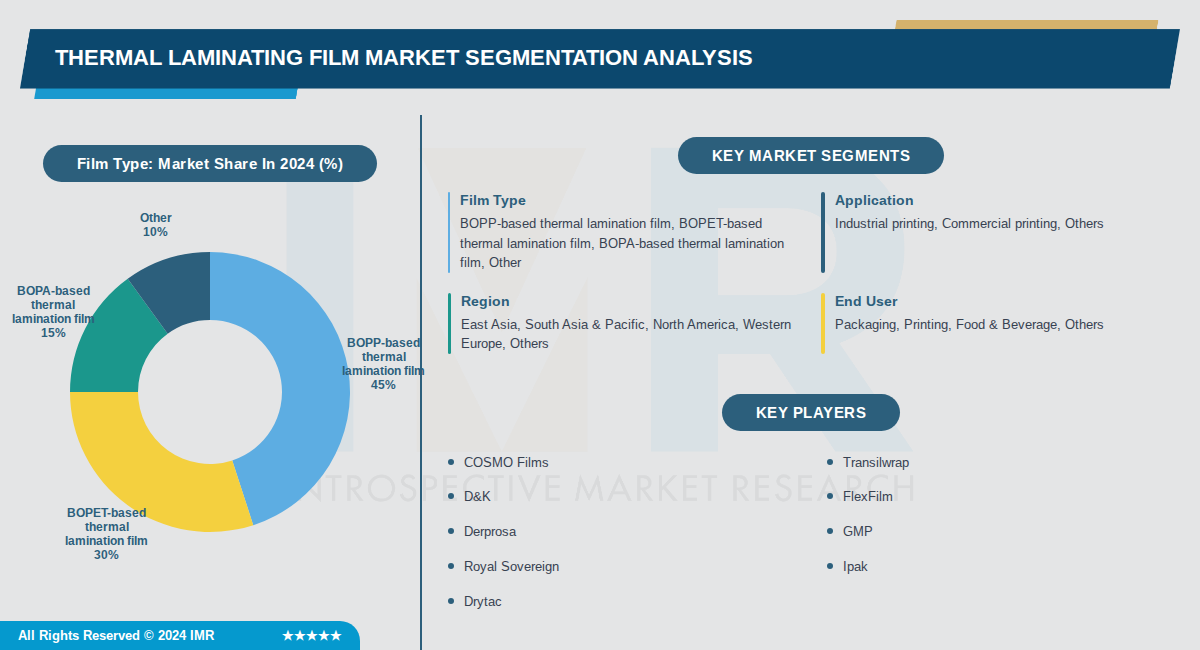

This market encompasses films primarily segmented by type, with BOPP-based films leading due to their versatility, and by application, where industrial printing holds the largest share, driven by demands in packaging and printing sectors.

Key regions including Asia Pacific, particularly China, dominate due to robust manufacturing, export-oriented supply, and expanding industries like food processing, e-commerce, and electronics, while North America and Europe contribute through premium packaging needs.

Thermal Laminating Film Market Trend Analysis:

Shift to Eco-Friendly and Biodegradable Films

- Stringent environmental regulations are accelerating the replacement of solvent-based thermal lamination with water-based and UV-curable alternatives, as seen in D&K's launch of a sustainable BOPA film derived from renewable resources that meets FDA food-grade standards. This shift addresses concerns over non-biodegradable plastics, with companies like COSMO Films investing in compostable options to comply with global sustainability mandates. Market data shows eco-friendly films gaining traction, reducing waste in packaging applications.

- Development of biodegradable films is surging due to government policies promoting green packaging, with Asia-Pacific leaders like Transilwrap expanding production in India to supply these materials for e-commerce needs. These films offer comparable clarity and durability to traditional BOPP and BOPET films but decompose naturally, appealing to brands in food and pharmaceutical sectors. Adoption is projected to drive a portion of the market's 2.3% CAGR through 2034.

- Challenges like higher initial costs are offset by long-term savings and consumer preference, with innovations in nanocoatings enhancing performance while maintaining eco-credentials.

Rise of Automated and AI-Integrated Laminating Systems

- Integration of artificial intelligence and IoT in laminating systems is transforming efficiency, enabling real-time monitoring and predictive maintenance in high-volume commercial printing operations dominated by BOPP-based films. Companies like Royal Sovereign and Drytac are deploying these systems to cut labor costs and errors, supporting the emergence of automated lines that handle customized laminates at scale. This trend aligns with the 3.4% CAGR growth from USD 3,062 million in 2019 to USD 3,753 million by 2026.

- Emergence of laser cutting and digital die cutting technologies allows precise lamination for niche applications in electronics and automotive industries, reducing material waste by up to 20% according to industry benchmarks. FlexFilm and Kangde Xin are leading with these innovations, integrating them into production for faster turnaround in packaging for e-commerce giants.

Expansion of Customized High-Performance Films in Asia-Pacific

- Asia-Pacific's dominance, holding over 50% of global revenue with China as the top market followed by India and Japan, fuels demand for tailored BOPET and BOPA films offering superior moisture resistance for food packaging. COSMO Films recently launched a high-performance BOPP variant for commercial printing, while Transilwrap's India capacity expansion targets rising e-commerce customization needs. This regional surge supports high-volume applications in advertising and publishing.

- Development of customized laminates with anti-scratch treatments and enhanced printability caters to industrial sectors like aerospace, where FlexFilm provides films with oxygen barrier properties. Driven by e-commerce growth, these solutions boost durability for labels and flexible packaging, contributing to the segment's leadership in commercial printing applications.

Thermal Laminating Film Market Segment Analysis:

Thermal Laminating Film Market is Segmented on the basis of By Film Type, By Application, By Region

By Film Type, BOPP-based thermal lamination film segment is expected to dominate the market during the forecast period

- BOPP-based films dominate due to their cost-effectiveness, excellent gloss and clarity, and widespread use in high-volume packaging applications like food and consumer goods.

- They account for the leading share as manufacturers prefer BOPP for its superior printability and barrier properties in premium and protective packaging demands.

By Application, Industrial printing segment is expected to dominate the market during the forecast period

- Industrial printing leads because of its bulk demand in protective packaging for sectors like electronics, automotive, and manufacturing where durability is critical.

- Rising e-commerce and brand protection needs drive higher volumes in industrial applications compared to shorter-run commercial print jobs.

By Region, East Asia segment is expected to dominate the market during the forecast period

- East Asia dominates with deep packaging ecosystems, rapid food processing growth, and export-oriented supply chains led by China, Japan, and South Korea.

- China's strong domestic manufacturing base and expanding e-commerce packaging underpin the highest regional volumes for BOPP-based laminates.

By End User, Packaging segment is expected to dominate the market during the forecast period

- Packaging end users lead due to surging demand for premium, protective solutions in food, cosmetics, and pharmaceuticals amid retail formalization.

- Eco-friendly BOPP and PET films tailored for flexible packaging drive the dominant share through technological advancements in solvent-free adhesives.

Thermal Laminating Film Market Regional Insights:

Asia-Pacific is Expected to Dominate the Thermal Laminating Film Market Over the Forecast Period

- Point 1: Asia-Pacific dominates production and consumption of thermal laminating films, with China and India experiencing the fastest expansion. The region accounts for close to 40% of the global market share, driven by a large and growing manufacturing base, expanding consumer markets, and relatively lower production costs compared to developed regions.

- Point 2: The region benefits from rapid industrialization and urbanization, particularly in China and India, which contributes to substantial demand for packaging and labeling solutions. Rising disposable incomes and the expansion of modern retail formats are spurring strong growth in packaged-goods demand across emerging markets in Asia-Pacific.

- Point 3: Major players including COSMO Films (GBC), Jindal Poly Films Limited (BC Jindal), and Mitsubishi Polyester Film, Inc. maintain significant market presence in the region. The Asia-Pacific region's cost-effectiveness in production and increasing adoption of thermal transfer printing across various applications further enhance its market dominance.

Active Key Players in the Thermal Laminating Film Market:

- COSMO Films (India)

- Transilwrap (USA)

- D&K (USA)

- FlexFilm (USA)

- Derprosa (Spain)

- GMP (USA)

- Royal Sovereign (USA)

- Ipak (USA)

- Drytac (Canada)

- PKC Co., Ltd (South Korea)

- J-Film Corporation (Japan)

- Shagun Films (India)

- Kangde Xin (China)

- New Era (China)

- Hongqing (China)

- KANGLONG (China)

- Dingxin (China)

- EKO Film (China)

- Eluson Film (China)

- Mitsubishi Polyester Film (Japan)

- Other Active Players

|

Thermal Laminating Film Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 1.55 Billion |

|

Forecast Period 2024-2035 CAGR: |

8.8 % |

Market Size in 2035: |

USD 3.6 Billion |

|

Segments Covered: |

By Film Type |

|

|

|

By Application |

|

||

|

By Region |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Thermal Laminating Film Market by Film Type (2017-2035)

4.1 Thermal Laminating Film Market Snapshot and Growth Engine

4.2 Market Overview

4.3 BOPP-based thermal lamination film

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 BOPET-based thermal lamination film

4.5 BOPA-based thermal lamination film

4.6 Other

Chapter 5: Thermal Laminating Film Market by Application (2017-2035)

5.1 Thermal Laminating Film Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Industrial printing

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Commercial printing

5.5 Others

Chapter 6: Thermal Laminating Film Market by Region (2017-2035)

6.1 Thermal Laminating Film Market Snapshot and Growth Engine

6.2 Market Overview

6.3 East Asia

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 South Asia & Pacific

6.5 North America

6.6 Western Europe

6.7 Others

Chapter 7: Thermal Laminating Film Market by End User (2017-2035)

7.1 Thermal Laminating Film Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Packaging

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Printing

7.5 Food & Beverage

7.6 Others

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Thermal Laminating Film Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 COSMO FILMS

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 TRANSILWRAP

8.4 D&K

8.5 FLEXFILM

8.6 DERPROSA

8.7 GMP

8.8 ROYAL SOVEREIGN

8.9 IPAK

8.10 DRYTAC

8.11 PKC CO.

8.12 LTD

8.13 J-FILM CORPORATION

8.14 SHAGUN FILMS

8.15 KANGDE XIN

8.16 NEW ERA

8.17 HONGQING

8.18 KANGLONG

8.19 DINGXIN

8.20 EKO FILM

8.21 ELUSON FILM

8.22 MITSUBISHI POLYESTER FILM

Chapter 9: Global Thermal Laminating Film Market By Region

9.1 Overview

9.2. North America Thermal Laminating Film Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Thermal Laminating Film Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Thermal Laminating Film Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Thermal Laminating Film Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Thermal Laminating Film Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Thermal Laminating Film Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Thermal Laminating Film Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 1.55 Billion |

|

Forecast Period 2024-2035 CAGR: |

8.8 % |

Market Size in 2035: |

USD 3.6 Billion |

|

Segments Covered: |

By Film Type |

|

|

|

By Application |

|

||

|

By Region |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||