Superalloys Market Synopsis:

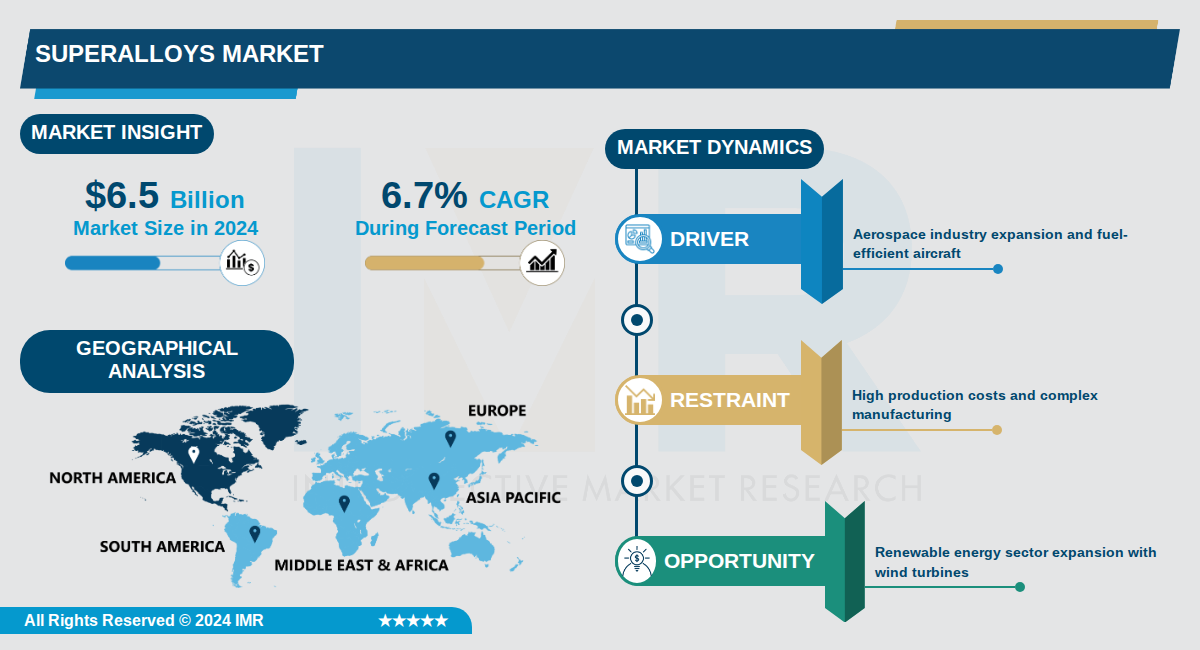

Superalloys Market Size Was Valued at USD 6.5 Billion in 2024, and is Projected to Reach USD 12.3 Billion by 2035, Growing at a CAGR of 6.7% From 2024-2035.

The global superalloys market, valued at $6.5 billion in 2024, is projected to reach $12.3 billion by 2035, growing at a compound annual growth rate (CAGR) of 6.7%. Superalloys, primarily nickel-based, cobalt-based, and iron-based, are high-performance materials renowned for their exceptional strength, corrosion resistance, and ability to withstand extreme temperatures above 800°C, making them essential in demanding applications.

Aerospace dominates the market, accounting for over 65% of demand in recent years, driven by the need for turbine engines, aircraft structural parts, and components in jet engines that require superior high-temperature performance and lightweight properties. North America leads with approximately 35% market share, bolstered by major players like Boeing, Lockheed Martin, and GE Aviation, while Europe and East Asia follow with strong aerospace and industrial bases.

Beyond aerospace, superalloys find growing use in power generation for advanced gas turbines, automotive for high-performance engines and turbochargers, oil & gas for drilling tools, and medical devices due to biocompatibility and corrosion resistance. Nickel-based variants hold the largest share owing to their oxidation and creep resistance in extreme conditions.

Superalloys Market Trend Analysis:

Adoption of Additive Manufacturing in Superalloys

- Additive manufacturing is revolutionizing superalloys production by enabling the creation of complex turbine blades and aerospace components with reduced weight and material waste. Companies like GE Aviation are leveraging 3D printing for nickel-based superalloys in jet engine parts, achieving up to 20% weight reduction compared to traditional casting methods. This shift supports next-generation aircraft engines from Boeing, improving fuel efficiency and performance under extreme temperatures exceeding 800°C.

- North America leads this trend with a 35% market share in 2025, driven by strong adoption from Lockheed Martin and defense contractors integrating 3D-printed cobalt-based superalloys for durable, lightweight systems. The technology cuts production times by optimizing microstructures through precise layer-by-layer deposition, minimizing defects in high-stress applications like combustors.

- In Asia-Pacific, rapid infrastructure growth fuels additive manufacturing expansion, with investments in local startups producing Ni-based superalloys for electric vehicle components and renewable energy turbines.

AI-Driven Alloy Design and Optimization

- Artificial intelligence and machine learning are transforming superalloys development by accelerating alloy composition optimization and predictive maintenance. Computational tools from companies like Mishra Dhatu Nigam Limited shorten R&D cycles from years to months, tailoring nickel-based superalloys for specific high-temperature needs in GE Aviation's turbine blades. AI analyzes microstructure properties to enhance creep resistance and oxidation stability, boosting performance by up to 15% in gas turbines.

- In the power generation sector, AI enables real-time monitoring and defect detection in industrial gas turbines, reducing downtime for operators modernizing plants with superalloys from Doncasters Group. This integration supports efficient energy systems, with predictive models optimizing heat treatment schedules for cobalt-based alloys used in nuclear reactors.

- Europe's strict emissions standards drive AI adoption in automotive applications, where firms like Sunflag Iron & Steel Co. Ltd use machine learning to develop iron-based superalloys for turbochargers in hybrid vehicles.

Expansion into Medical and Automotive Applications

- Cobalt-based superalloys are surging in medical implants due to biocompatibility and corrosion resistance, with global aging populations driving demand for hip and knee replacements from Cannon Muskegon. This segment grows significantly as orthopedic devices require thermal stability, expanding the market beyond aerospace to over 10% of total superalloys usage by 2033.

- In automotive, superalloys support high-performance engines and turbochargers in electric and hybrid vehicles from major manufacturers, enduring elevated temperatures and mechanical stress. Iron-based variants are key in exhaust systems, fueled by Asia-Pacific's EV boom and infrastructure investments.

- This diversification reduces aerospace dependency, with nickel-based superalloys entering petrochemical plants and renewable energy systems, projecting the overall market to USD 11.4 billion by 2033.

Superalloys Market Segment Analysis:

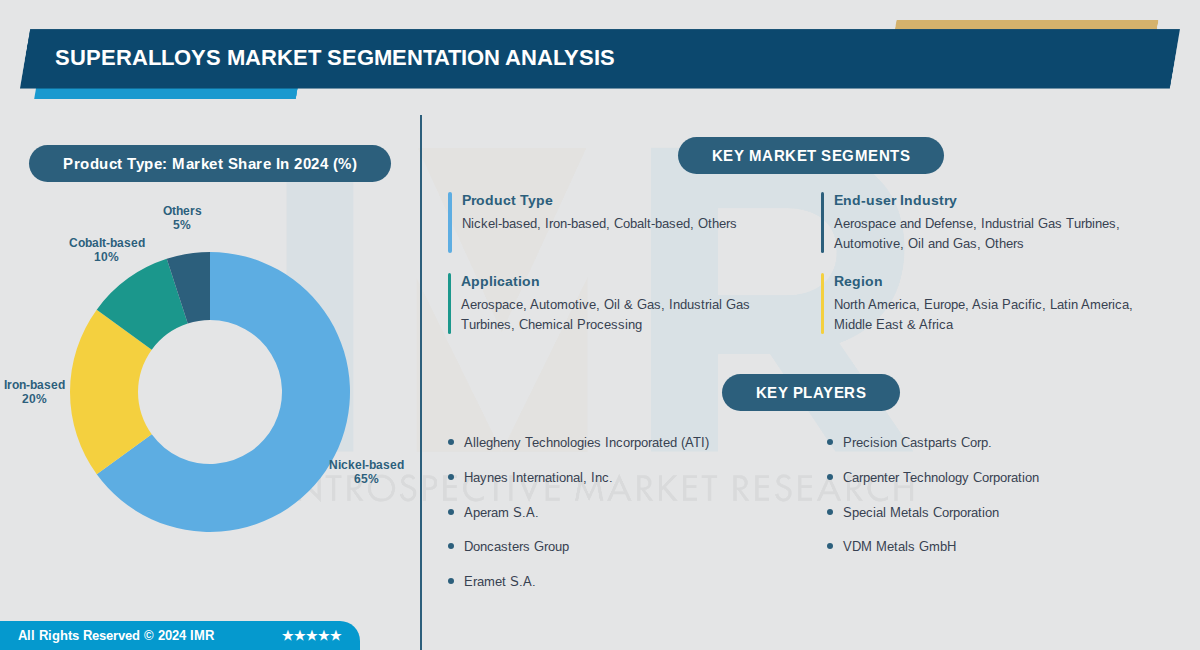

Superalloys Market is Segmented on the basis of By Product Type, By End-user Industry, By Application

By Product Type, Nickel-based segment is expected to dominate the market during the forecast period

- Nickel-based superalloys dominate due to their superior high-temperature strength, oxidation resistance, and corrosion resistance, making them ideal for turbine blades, combustors, and aerospace engine components.

- They account for over 66% market share in recent analyses, driven by extensive use in aerospace and industrial gas turbines where extreme conditions demand unmatched performance.

By End-user Industry, Aerospace and Defense segment is expected to dominate the market during the forecast period

- Aerospace and defense leads due to surging demand for lightweight, heat-resistant materials in aircraft engines, turbine blades, and structural components amid rising global defense budgets and fuel-efficient aircraft development.

- This segment holds nearly 39% revenue share, supported by major manufacturers like Boeing and GE Aviation relying on superalloys for high-performance applications in extreme environments.

By Application, Aerospace segment is expected to dominate the market during the forecast period

- Aerospace dominates as superalloys provide essential properties like high mechanical strength and heat resistance critical for jet engines and turbines operating under extreme temperatures.

- The segment's 45% share is propelled by innovations in additive manufacturing and increasing aircraft production, particularly in North America where it drives regional market leadership.

By Region, North America segment is expected to dominate the market during the forecast period

- North America leads with around 40-50% share due to its robust aerospace, defense, and power generation sectors, bolstered by key players like Boeing, Lockheed Martin, and GE Aviation.

- Advanced manufacturing capabilities, significant R&D investments, and high adoption in clean energy and additive manufacturing further cement its dominant position.

Superalloys Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast Period

- North America dominates the superalloys market with a 35% share in 2025, primarily driven by the United States, which accounted for a leading market value of USD 2.45 billion in 2024. The U.S. benefits from its advanced aerospace and defense industries, while Canada and Mexico contribute through manufacturing and supply chains. This regional leadership is reinforced across multiple market analyses for both general superalloys and nickel-based variants.

- The region's dominance stems from a strong industrial base in aerospace, defense, automotive, and power generation, supported by robust infrastructure and significant R&D investments. Favorable policies and high demand for high-temperature materials in jet engines and turbines further bolster the market. North America's established supply chain ensures reliable production and innovation in superalloy applications.

- Major players headquartered in the U.S., such as Precision Castparts Corporation, Allegheny Technologies Limited, Carpenter Technology Corporation, Boeing, Lockheed Martin, and General Electric Aviation, drive the market through technological advancements and strategic expansions. Recent U.S. investments in aerospace, including space programs with budgets exceeding USD 22 billion, continue to fuel demand. These developments solidify North America's competitive edge.

Active Key Players in the Superalloys Market:

- Allegheny Technologies Incorporated (ATI) (USA)

- Precision Castparts Corp. (USA)

- Haynes International, Inc. (USA)

- Carpenter Technology Corporation (USA)

- Aperam S.A. (Luxembourg)

- Special Metals Corporation (USA)

- Doncasters Group (UK)

- VDM Metals GmbH (Germany)

- Eramet S.A. (France)

- Nippon Yakin Kogyo Co., Ltd. (Japan)

- Hitachi Metals, Ltd. (Japan)

- VSMPO-AVISMA Corporation (Russia)

- ThyssenKrupp AG (Germany)

- BaoSteel (China)

- Mishra Dhatu Nigam Limited (India)

- Fushun Special Steel Co., Ltd. (China)

- Outokumpu Oyj (Finland)

- Cannon Muskegon (USA)

- Sunflag Iron & Steel Co. Ltd (India)

- Western Superconducting Technologies Co., Ltd. (China)

- Other Active Players

|

Superalloys Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 6.5 Billion |

|

Forecast Period 2024-2035 CAGR: |

6.7 % |

Market Size in 2035: |

USD 12.3 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By End-user Industry |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Superalloys Market by Product Type (2017-2035)

4.1 Superalloys Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Nickel-based

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Iron-based

4.5 Cobalt-based

4.6 Others

Chapter 5: Superalloys Market by End-user Industry (2017-2035)

5.1 Superalloys Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Aerospace and Defense

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Industrial Gas Turbines

5.5 Automotive

5.6 Oil and Gas

5.7 Others

Chapter 6: Superalloys Market by Application (2017-2035)

6.1 Superalloys Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Aerospace

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Automotive

6.5 Oil & Gas

6.6 Industrial Gas Turbines

6.7 Chemical Processing

Chapter 7: Superalloys Market by Region (2017-2035)

7.1 Superalloys Market Snapshot and Growth Engine

7.2 Market Overview

7.3 North America

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Europe

7.5 Asia Pacific

7.6 Latin America

7.7 Middle East & Africa

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Superalloys Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 ALLEGHENY TECHNOLOGIES INCORPORATED (ATI)

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 PRECISION CASTPARTS CORP.

8.4 HAYNES INTERNATIONAL

8.5 INC.

8.6 CARPENTER TECHNOLOGY CORPORATION

8.7 APERAM S.A.

8.8 SPECIAL METALS CORPORATION

8.9 DONCASTERS GROUP

8.10 VDM METALS GMBH

8.11 ERAMET S.A.

8.12 NIPPON YAKIN KOGYO CO.

8.13 LTD.

8.14 HITACHI METALS

8.15 LTD.

8.16 VSMPO-AVISMA CORPORATION

8.17 THYSSENKRUPP AG

8.18 BAOSTEEL

8.19 MISHRA DHATU NIGAM LIMITED

8.20 FUSHUN SPECIAL STEEL CO.

8.21 LTD.

8.22 OUTOKUMPU OYJ

8.23 CANNON MUSKEGON

8.24 SUNFLAG IRON & STEEL CO. LTD

8.25 WESTERN SUPERCONDUCTING TECHNOLOGIES CO.

8.26 LTD.

Chapter 9: Global Superalloys Market By Region

9.1 Overview

9.2. North America Superalloys Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Superalloys Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Superalloys Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Superalloys Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Superalloys Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Superalloys Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Superalloys Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 6.5 Billion |

|

Forecast Period 2024-2035 CAGR: |

6.7 % |

Market Size in 2035: |

USD 12.3 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By End-user Industry |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||