Structural Heart Devices Market Synopsis:

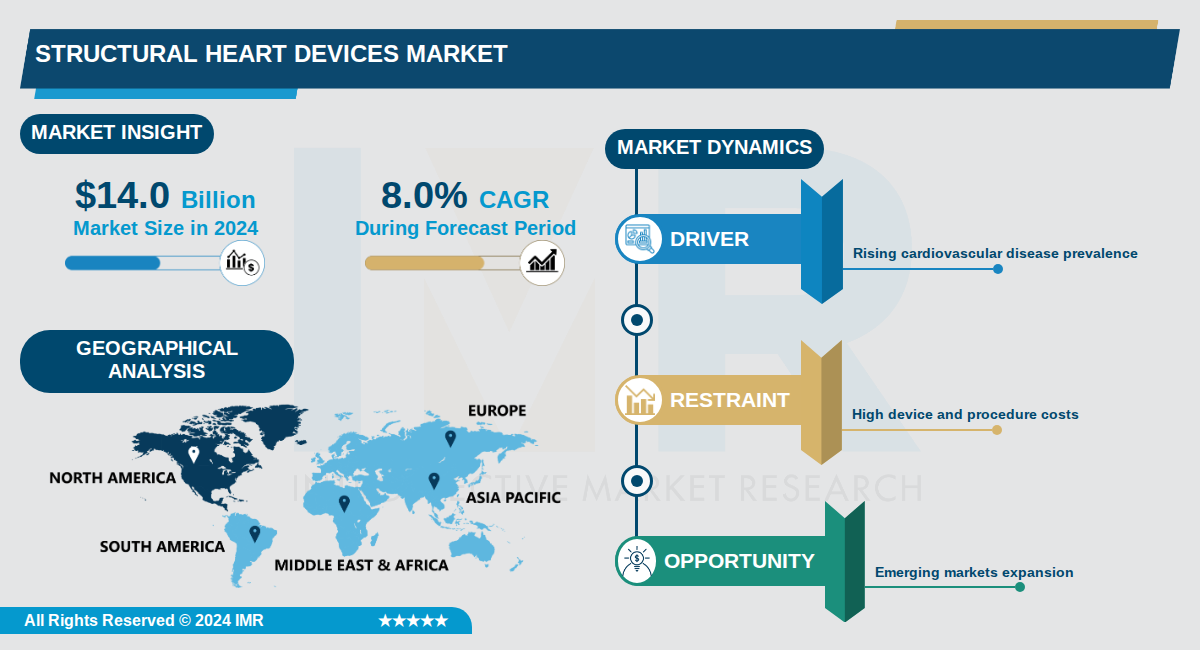

Structural Heart Devices Market Size Was Valued at USD 14.0 Billion in 2024, and is Projected to Reach USD 31.0 Billion by 2035, Growing at a CAGR of 8.0% From 2024-2035.

The global structural heart devices market is experiencing robust growth, valued at approximately USD 14.0 billion in 2024 and projected to reach USD 31.0 billion by 2035, representing a compound annual growth rate (CAGR) of 8.0%. Structural heart devices are medical devices designed for the diagnosis and treatment of structural abnormalities within the heart, including conditions such as valvular heart disease, atrial septal defects, and ventricular septal defects. This market encompasses a diverse range of products and procedures that address critical cardiovascular health challenges affecting millions globally.

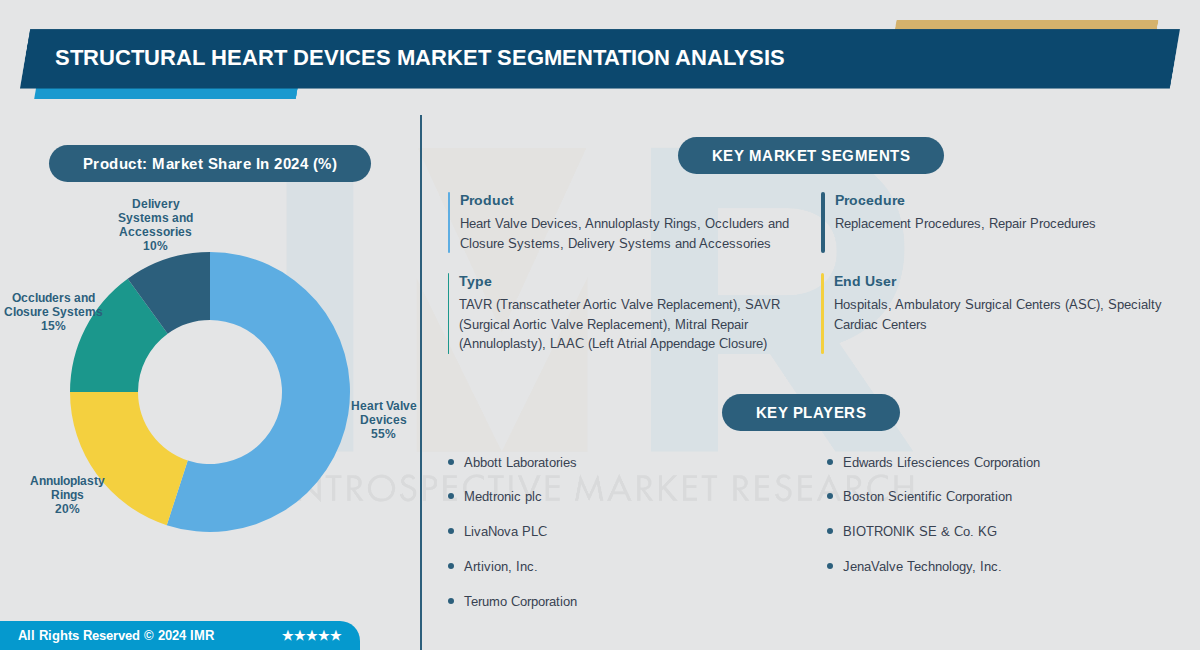

The market is segmented by product type, procedure, end-user, and region, with heart valve devices representing the largest product segment due to increasing cases of calcific aortic valve disease and rheumatic heart diseases. Replacement procedures dominate the procedural segment, driven by rising demand for advanced minimally invasive techniques and improved prosthetic valve designs. North America leads the market geographically with a 52.5% revenue share in 2024, supported by aging populations, increased healthcare spending, and strong regulatory frameworks.

Key market drivers include the rising prevalence of cardiovascular diseases, expanding insurance coverage, growing adoption of minimally invasive procedures, and technological advancements in device design. Asia Pacific is emerging as the fastest-growing region, driven by a large patient pool, growing geriatric population, improving healthcare infrastructure, and increasing medical tourism. The market is characterized by the presence of major players including Edwards Lifesciences Corporation, Boston Scientific Corporation, Abbott, and Medtronic, who continue to invest in research and development to drive innovation.

Structural Heart Devices Market Trend Analysis:

Expansion of Transcatheter Aortic Valve Replacement to Low-Risk Patients

- Transcatheter Aortic Valve Replacement (TAVR) procedures, led by companies like Medtronic and Edwards Lifesciences, are expanding beyond high-risk patients into intermediate- and low-risk cohorts, driving market growth to USD 34.1 billion by 2030 at a 9.8% CAGR. This shift is supported by improved procedural safety profiles and enhanced valve durability data from long-term studies. In 2024, Medtronic received CE certification for its Evolut FX+ TAVR system, featuring four times wider coronary access windows than prior models to enable easier future interventions.

- Sustained adoption of TAVR as the primary revenue contributor is evident, with valve replacement procedures holding the largest market share in 2025 and expected to dominate through 2026. Regulatory approvals for expanded indications have broadened patient eligibility, particularly for younger demographics. For example, MicroPort CardioFlow's second-generation VitaFlow Liberty TAVR system gained South Korea’s MFDS approval in December 2024, facilitating entry into Asian markets.

- Procedural volumes are rising due to advanced cardiac programs in developed healthcare systems, with North America commanding 52.5% market share in 2024 from high demand for minimally invasive options. This expansion is projected to push segment revenue beyond USD 54.5 billion by 2035 as clinical validation continues.

Rise of Mitral Valve Repair Technologies

- The mitral repair segment is advancing rapidly with transcatheter edge-to-edge repair (TEER) platforms and minimally invasive annuloplasty solutions, positioning it as the second-largest contributor after TAVR. In January 2024, CardioMech AS raised USD 13 million to advance its MVRS platform using transcatheter chordal replacement technology, mimicking surgical outcomes for younger and higher-risk patients. This addresses mitral regurgitation, a key valvular disease tied to aging populations.

- Companies like Abbott and Boston Scientific are driving growth through TEER systems, fueled by increasing procedural volumes and favorable reimbursements in key markets. The segment benefits from regulatory approvals expanding indications for transcatheter heart valves. Market projections show strong CAGR for repair procedures amid rising heart valve disease prevalence, accounting for over 75% of indications in 2025.

- Technological innovations such as retrievable transcatheter valves and patient-specific 3D modeling are improving outcomes in mitral interventions, boosting adoption in Europe and China where CVD cases are surging.

Adoption of Repositionable and Next-Generation Transcatheter Valves

- Next-generation structural heart devices feature retrievable and repositionable transcatheter valves with customized biomaterials for better biocompatibility, expanding eligibility to lower-risk patients. Edwards Lifesciences and Abbott lead with design improvements like precise 3D modeling for patient-specific valve sizing, enhancing procedural success rates. These advancements are key to the market's growth from USD 14.65 billion in 2025 to USD 27.16 billion by 2034 at 7.2% CAGR.

- Medtronic's Evolut FX+ system exemplifies this trend with larger coronary access windows, certified in Europe in October 2024, improving long-term care strategies. LivaNova and JenaValve Technology are also innovating in occlusion and closure devices, supporting higher-risk procedures with reduced recovery times. Investor interest, including venture funding for early-stage firms, is accelerating these developments.

- This trend is evident in accessories segment growth, driven by rising procedural volumes for valve replacement and repair, with instruments dominating due to global increases in structural defect treatments.

Structural Heart Devices Market Segment Analysis:

Structural Heart Devices Market is Segmented on the basis of By Product, By Procedure, By Type

By Product, Heart Valve Devices segment is expected to dominate the market during the forecast period

- Heart valve devices dominate due to the high prevalence of valvular heart diseases and the rapid adoption of transcatheter technologies like TAVR, which offer superior outcomes over traditional surgery.

- TAVR procedures alone account for the majority of structural heart interventions globally, driven by expanding indications to lower-risk patients and proven long-term durability data.

By Procedure, Replacement Procedures segment is expected to dominate the market during the forecast period

- Replacement procedures lead the market because of the surging demand for TAVR and other transcatheter valve replacements, which provide less invasive alternatives with shorter recovery times.

- Replacement segment valued over USD 7.3 billion in 2024, reflecting higher procedural volumes and reimbursements compared to repair techniques amid rising aortic stenosis cases.

By Type, TAVR (Transcatheter Aortic Valve Replacement) segment is expected to dominate the market during the forecast period

- TAVR holds the largest share due to its minimally invasive nature, expanding clinical guidelines to younger and lower-risk patients, and strong evidence from landmark trials showing mortality benefits.

- TAVR captured the dominant revenue share in 2024, fueled by technological advancements in valve durability and procedural efficiency across major markets like North America.

By End User, Hospitals segment is expected to dominate the market during the forecast period

- Hospitals dominate as they house advanced structural heart programs, specialized cath labs, and multidisciplinary teams essential for complex TAVR and LAAC procedures.

- Hospital systems lead due to high procedural volumes, integration of innovative cardiac programs, and ability to attract patients seeking comprehensive care for structural heart conditions.

Structural Heart Devices Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast Period

- North America dominates the structural heart devices market, holding the largest share such as 36.52% in 2025 and up to 52.5% in 2024. The U.S. leads within the region with a market value of USD 4.98 billion in 2025, supported by high procedural volumes for heart valve operations. Canada and Mexico also contribute, with Canada anticipated for fast growth.

- The region's dominance stems from advanced healthcare infrastructure, high healthcare spending, and favorable reimbursement policies for minimally invasive procedures like transcatheter aortic valve replacement. A growing geriatric population and rising prevalence of cardiovascular diseases further boost demand. Government initiatives, including CDC grants for heart valve disease awareness, enhance market growth.

- Major players like Medtronic, Edwards Lifesciences, Boston Scientific, and Abbott have a strong presence, driving innovation in devices such as prosthetic heart valves. Recent developments include increased adoption of endovascular procedures and research investments. These companies leverage the region's high procedural volumes to maintain leadership.

Active Key Players in the Structural Heart Devices Market:

- Abbott Laboratories (USA)

- Edwards Lifesciences Corporation (USA)

- Medtronic plc (Ireland)

- Boston Scientific Corporation (USA)

- LivaNova PLC (UK)

- BIOTRONIK SE & Co. KG (Germany)

- Artivion, Inc. (USA)

- JenaValve Technology, Inc. (Germany)

- Terumo Corporation (Japan)

- Lepu Medical Technology Co., Ltd. (China)

- MicroPort Scientific Corporation (China)

- Meril Life Sciences Pvt. Ltd. (India)

- Micro Interventional Devices, Inc. (USA)

- Relisys Medical Devices Limited (India)

- Venus Medtech, Inc. (China)

- AtriCure, Inc. (USA)

- W. L. Gore & Associates, Inc. (USA)

- HighLife Medical (France)

- Other Active Players

|

Structural Heart Devices Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 14.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

8.0 % |

Market Size in 2035: |

USD 31.0 Billion |

|

Segments Covered: |

By Product |

|

|

|

By Procedure |

|

||

|

By Type |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Structural Heart Devices Market by Product (2017-2035)

4.1 Structural Heart Devices Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Heart Valve Devices

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Annuloplasty Rings

4.5 Occluders and Closure Systems

4.6 Delivery Systems and Accessories

Chapter 5: Structural Heart Devices Market by Procedure (2017-2035)

5.1 Structural Heart Devices Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Replacement Procedures

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Repair Procedures

Chapter 6: Structural Heart Devices Market by Type (2017-2035)

6.1 Structural Heart Devices Market Snapshot and Growth Engine

6.2 Market Overview

6.3 TAVR (Transcatheter Aortic Valve Replacement)

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 SAVR (Surgical Aortic Valve Replacement)

6.5 Mitral Repair (Annuloplasty)

6.6 LAAC (Left Atrial Appendage Closure)

Chapter 7: Structural Heart Devices Market by End User (2017-2035)

7.1 Structural Heart Devices Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Hospitals

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Ambulatory Surgical Centers (ASC)

7.5 Specialty Cardiac Centers

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Structural Heart Devices Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 ABBOTT LABORATORIES

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 EDWARDS LIFESCIENCES CORPORATION

8.4 MEDTRONIC PLC

8.5 BOSTON SCIENTIFIC CORPORATION

8.6 LIVANOVA PLC

8.7 BIOTRONIK SE & CO. KG

8.8 ARTIVION

8.9 INC.

8.10 JENAVALVE TECHNOLOGY

8.11 INC.

8.12 TERUMO CORPORATION

8.13 LEPU MEDICAL TECHNOLOGY CO.

8.14 LTD.

8.15 MICROPORT SCIENTIFIC CORPORATION

8.16 MERIL LIFE SCIENCES PVT. LTD.

8.17 MICRO INTERVENTIONAL DEVICES

8.18 INC.

8.19 RELISYS MEDICAL DEVICES LIMITED

8.20 VENUS MEDTECH

8.21 INC.

8.22 ATRICURE

8.23 INC.

8.24 W. L. GORE & ASSOCIATES

8.25 INC.

8.26 HIGHLIFE MEDICAL

Chapter 9: Global Structural Heart Devices Market By Region

9.1 Overview

9.2. North America Structural Heart Devices Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Structural Heart Devices Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Structural Heart Devices Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Structural Heart Devices Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Structural Heart Devices Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Structural Heart Devices Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Structural Heart Devices Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 14.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

8.0 % |

Market Size in 2035: |

USD 31.0 Billion |

|

Segments Covered: |

By Product |

|

|

|

By Procedure |

|

||

|

By Type |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||