Rapid Diagnostics Market Synopsis:

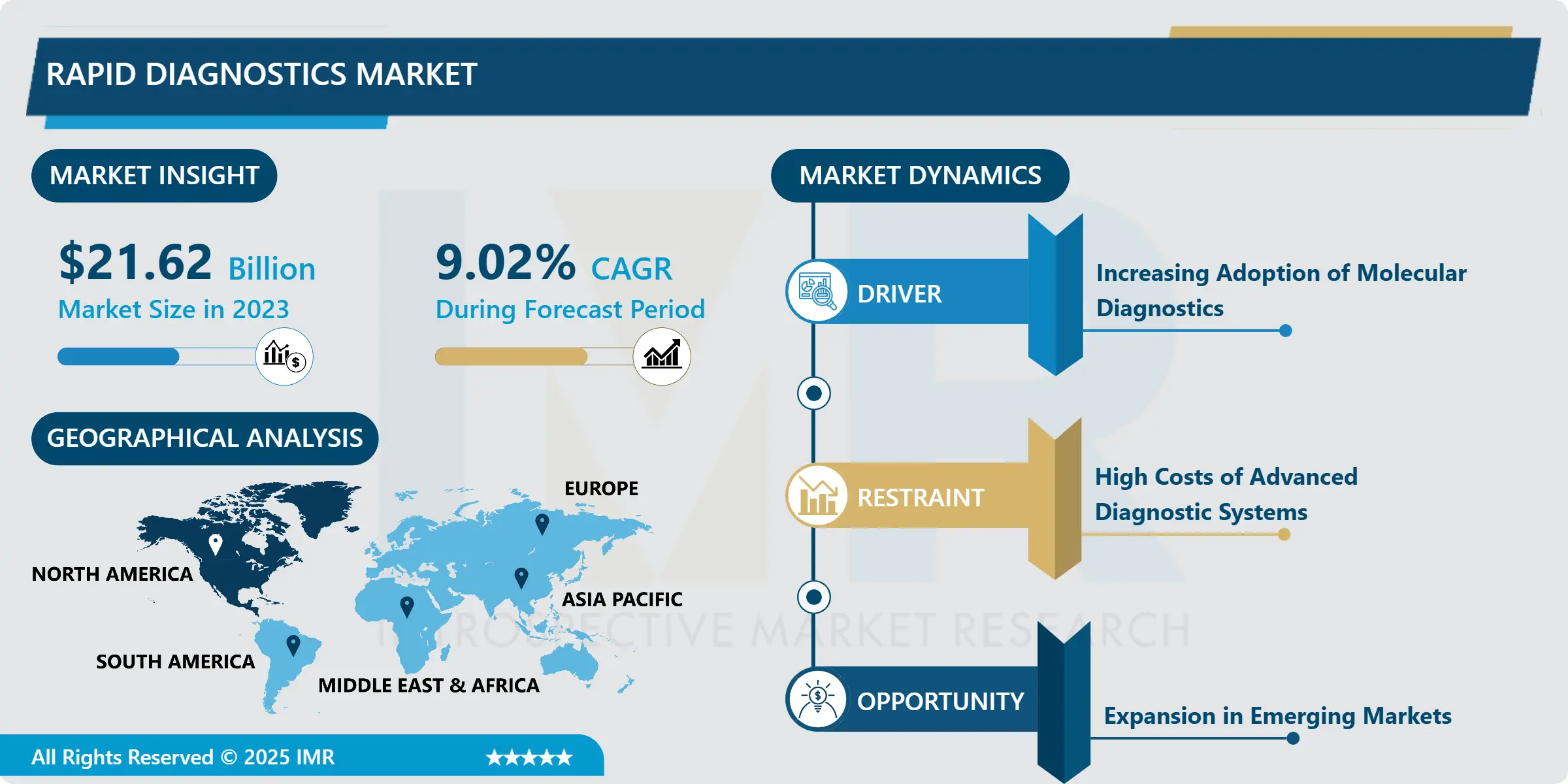

Rapid Diagnostics Market Size Was Valued at USD 21.62 Billion in 2023, and is Projected to Reach USD 47.03 Billion by 2032, Growing at a CAGR of 9.02% From 2024-2032.

The rapid diagnostics market is defined as diagnostic devices or assays that could be used in a healthcare facility or at the same time on the patient to provide diagnosis of a specific disease, condition or an infection in the shortest time possible. A most important feature when it comes to these tests is that they produce results within a shorter time span, within minutes to a few hours, making significant positive impacts on patient’s health and decreasing the time taken for results thus increasing clinical action. These rapid diagnostic tools include lateral flow and immunoassay, molecular, and other point-of-care diagnostic systems; used at hospitals, clinics, labs, and at home.

Rapid diagnostics industry has exhibited constant growth trajectory across the recent years due to the increasing demand for effective and efficient diagnostic solutions in all the fields of medicine and technologies. These tools are essential for prompt identification of infection, chronic diseases and other healthcare concerns; thus, cost effective and easy to use for healthcare practitioners and consumers. The market is emerging with development in molecular diagnostic technologies for which have high accuracy and sensitivity than the current techniques such as PCR.

Cue to the persisting threats of infectious diseases in the world which call for enhanced detection and monitoring techniques, rapid diagnostics got further more popular with the recent COVID-19 pandemic. This has occasioned a call for development of new and more transportable diagnostic systems especially for rural or hard-to-reach locales. The use of point-of-care diagnostic tests has been on the rise in the emerging economies to deal with the burgeoning health care needs and government drive to improve health care facilities in the region. Also, the development of home test kits and self-monitoring equipment will boost the market as more people want reliable and easy to obtain diagnostic opportunities.

Rapid Diagnostics Market Trend Analysis:

Increasing Adoption of Molecular Diagnostics

- It is noteworthy that molecular diagnosis constitutes one of the leading trends in the market for rapid diagnostics. These diagnostic tools, PCR testing and next-generation sequencing, provide more accurate, specific and quicker results in comparison to conventional testing systems. Molecular diagnostic is increasingly being used especially in infections like the COVID-19, HIV and tuberculosis, because they identify pathogens at the molecular level. These tests are most particularly useful in conditions where other approaches to diagnostics can come across limits concerning of rapidity, specificity, or sensitivity. Three significant trends characterize the future of molecular diagnostics: the focus of new developments on easy-to-use point-of-care devices, and therefore the growing role of diagnostics in primary care; the increasing complexity of diagnostics, which will make them comparable to modern molecular diagnostic lab platforms; and advances in molecular diagnostics technology that already point to their use outside specialized laboratories.

Expansion in Emerging Markets

- According to the market, there are ample growth prospects within the rapid diagnostics market in the emerging zones. In tropical and sub-tropical countries of Asia Pacific, Latin America and Africa, healthcare needs have emerged due to chronic diseases, infectious diseases and increasing population of the aging people. There is therefore strong and urgent demands for cheap, available and faster diagnostic techniques especially in these regions given the weak health systems and the growing disease prevalence. Isolation of government attempts in the enhancement of health care accessibility and increment in health care inclination is putting forward a friendly climate for the use of rapid diagnosing technologies. These are; The growth of point of care devices and the emergence of multiplex simple and affordable diagnostic kits for use in rural regions. Moreover, more e-Health and telemedicine markets in these locations contribute to the increased market growth since patients now prefer to get diagnostics tests from the comfort of their homes.

Rapid Diagnostics Market Segment Analysis:

Rapid Diagnostics Market is Segmented on the basis of Product, Technology, Application, End User, and Region.

By Product, the Over The Counter (OTC) Kits segment is expected to dominate the market during the forecast period

- From the product standpoint, over the counter (OTC) contributions to the market value of rapid medical diagnostic kits were significantly.This is the case because these tests can be performed in the “near-patient” and are cheaper than other laboratory testing procedures. These tests are applied mostly in home care since they are cheaper than laboratory tests. In patient testing, the popular samples used include saliva, urine and blood for diagnosing diseases, according to RDTs.

- Clinical cost savings that were highlighted by the Consumer Healthcare Products Association estimate that due to the low price of OTC diagnostic products. They also help identify different infectious and chronic diseases that may not necessarily have symptom and therefore, get treatment at an early stage to avoid the other associated complications with the disease. Although these tests are widely applied in home care, other end-use applications may include hospitals, clinics, and diagnostic laboratories.

By Technology, Lateral Flow segment expected to held the largest share

- The lateral flow technology segment has the highest share of the revenue. These tests are incorporated in many qualitative and quantitative identification of specific antigens, Gene amplification products, and antibodies in hospitals, clinics, and diagnostic laboratories, further enhancing segment growth.

- Lateral flow assays are affordable, fast and convenient to perform and are also highly accurate giving results in 10-15 minutes at best. These tests identify Ig G and Ig M antibodies against COVID-19 virus which is responsible for infecting human and causing diseases like COVID 19. In March 2020, Ozo Life gifted the world with OZO COVID-19 Rapid Test Kits, a latex enhanced, high sensitivity lateral flow immunoassay that can detect COVID-19 in the early stages. Thus, the lateral flow assays market growth is expected to be driven by the rise in strategic initiatives by market players during the lateral flow assays market forecast period.

Rapid Diagnostics Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

- North America continues to be in the apex of the rapid diagnostics market while the US continues to maintain its position in the market share. The higher emphasis on the healthcare industry, greater healthcare expenditure and market players all play a part in giving the region a higher market share. North America is projected to garner a most prominent market share due to a rise in the demand of rapid diagnostic solutions in hospitals, clinics and home care settings. In addition, research and development activities of the region have been high, with technological enhancement in diagnosis enhancing the leadership status. Higher demand in molecular diagnostics and increased number of approvals by governments for rapid testing devices shall enable the growth of this region. The COVID-19 also influenced the increased in demand of rapid diagnostic in North America particularly of infectious diseases test.

Active Key Players in the Rapid Diagnostics Market:

- Abbott Laboratories (USA)

- BD (Becton Dickinson) (USA)

- BioMérieux (France)

- Cepheid (USA)

- Danaher Corporation (USA)

- Grifols (Spain)

- Hologic, Inc. (USA)

- Mylan N.V. (USA)

- Oxford Nanopore Technologies (UK)

- PerkinElmer (USA)

- Qiagen N.V. (Germany)

- Roche Diagnostics (Switzerland)

- Siemens Healthineers (Germany)

- Sysmex Corporation (Japan)

- Thermo Fisher Scientific (USA), and Other Active Players

|

Rapid Diagnostics Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 21.62 Billion |

|

Forecast Period 2024-32 CAGR: |

9.02% |

Market Size in 2032: |

USD 47.03 Billion |

|

Segments Covered: |

By Product |

|

|

|

By Technology |

|

||

|

By Application |

|

||

|

End user |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Rapid Diagnostics Market by Product

4.1 Rapid Diagnostics Market Snapshot and Growth Engine

4.2 Rapid Diagnostics Market Overview

4.3 Over The Counter (OTC) Kits

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.3.3 Key Market Trends, Growth Factors and Opportunities

4.3.4 Over The Counter (OTC) Kits : Geographic Segmentation Analysis

4.4 Professional Kits

4.4.1 Introduction and Market Overview

4.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.4.3 Key Market Trends, Growth Factors and Opportunities

4.4.4 Professional Kits: Geographic Segmentation Analysis

Chapter 5: Rapid Diagnostics Market by Technology

5.1 Rapid Diagnostics Market Snapshot and Growth Engine

5.2 Rapid Diagnostics Market Overview

5.3 Lateral Flow

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.3.3 Key Market Trends, Growth Factors and Opportunities

5.3.4 Lateral Flow : Geographic Segmentation Analysis

5.4 Agglutination

5.4.1 Introduction and Market Overview

5.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.4.3 Key Market Trends, Growth Factors and Opportunities

5.4.4 Agglutination : Geographic Segmentation Analysis

5.5 Solid Phase

5.5.1 Introduction and Market Overview

5.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.5.3 Key Market Trends, Growth Factors and Opportunities

5.5.4 Solid Phase : Geographic Segmentation Analysis

5.6 Other Technologies.

5.6.1 Introduction and Market Overview

5.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.6.3 Key Market Trends, Growth Factors and Opportunities

5.6.4 Other Technologies.: Geographic Segmentation Analysis

Chapter 6: Rapid Diagnostics Market by Application

6.1 Rapid Diagnostics Market Snapshot and Growth Engine

6.2 Rapid Diagnostics Market Overview

6.3 Blood Glucose Testing

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.3.3 Key Market Trends, Growth Factors and Opportunities

6.3.4 Blood Glucose Testing : Geographic Segmentation Analysis

6.4 Infectious Disease Testing

6.4.1 Introduction and Market Overview

6.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.4.3 Key Market Trends, Growth Factors and Opportunities

6.4.4 Infectious Disease Testing: Geographic Segmentation Analysis

6.5 (COVID-19

6.5.1 Introduction and Market Overview

6.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.5.3 Key Market Trends, Growth Factors and Opportunities

6.5.4 (COVID-19 : Geographic Segmentation Analysis

6.6 Hepatitis

6.6.1 Introduction and Market Overview

6.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.6.3 Key Market Trends, Growth Factors and Opportunities

6.6.4 Hepatitis : Geographic Segmentation Analysis

6.7 HIV

6.7.1 Introduction and Market Overview

6.7.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.7.3 Key Market Trends, Growth Factors and Opportunities

6.7.4 HIV : Geographic Segmentation Analysis

6.8 Influenza

6.8.1 Introduction and Market Overview

6.8.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.8.3 Key Market Trends, Growth Factors and Opportunities

6.8.4 Influenza : Geographic Segmentation Analysis

6.9 Others)Cardiometabolic Testing

6.9.1 Introduction and Market Overview

6.9.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.9.3 Key Market Trends, Growth Factors and Opportunities

6.9.4 Others)Cardiometabolic Testing : Geographic Segmentation Analysis

6.10 Pregnancy and Fertility Testing

6.10.1 Introduction and Market Overview

6.10.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.10.3 Key Market Trends, Growth Factors and Opportunities

6.10.4 Pregnancy and Fertility Testing : Geographic Segmentation Analysis

6.11 Fecal Occult Blood Testing

6.11.1 Introduction and Market Overview

6.11.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.11.3 Key Market Trends, Growth Factors and Opportunities

6.11.4 Fecal Occult Blood Testing : Geographic Segmentation Analysis

6.12 Coagulation Testing

6.12.1 Introduction and Market Overview

6.12.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.12.3 Key Market Trends, Growth Factors and Opportunities

6.12.4 Coagulation Testing : Geographic Segmentation Analysis

6.13 Toxicology Testing

6.13.1 Introduction and Market Overview

6.13.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.13.3 Key Market Trends, Growth Factors and Opportunities

6.13.4 Toxicology Testing : Geographic Segmentation Analysis

6.14 Lipid Profile Testing

6.14.1 Introduction and Market Overview

6.14.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.14.3 Key Market Trends, Growth Factors and Opportunities

6.14.4 Lipid Profile Testing : Geographic Segmentation Analysis

6.15 Other Applications

6.15.1 Introduction and Market Overview

6.15.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.15.3 Key Market Trends, Growth Factors and Opportunities

6.15.4 Other Applications: Geographic Segmentation Analysis

Chapter 7: Rapid Diagnostics Market by End User

7.1 Rapid Diagnostics Market Snapshot and Growth Engine

7.2 Rapid Diagnostics Market Overview

7.3 Hospitals & Clinics

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

7.3.3 Key Market Trends, Growth Factors and Opportunities

7.3.4 Hospitals & Clinics : Geographic Segmentation Analysis

7.4 Home Care

7.4.1 Introduction and Market Overview

7.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

7.4.3 Key Market Trends, Growth Factors and Opportunities

7.4.4 Home Care : Geographic Segmentation Analysis

7.5 Diagnostic Laboratories

7.5.1 Introduction and Market Overview

7.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

7.5.3 Key Market Trends, Growth Factors and Opportunities

7.5.4 Diagnostic Laboratories: Geographic Segmentation Analysis

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Rapid Diagnostics Market Share by Manufacturer (2023)

8.1.3 Industry BCG Matrix

8.1.4 Heat Map Analysis

8.1.5 Mergers and Acquisitions

8.2 ABBOTT LABORATORIES (USA)

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Key Strategic Moves and Recent Developments

8.2.10 SWOT Analysis

8.3 BD (BECTON DICKINSON) (USA)

8.4 BIOMÉRIEUX (FRANCE)

8.5 CEPHEID (USA)

8.6 DANAHER CORPORATION (USA)

8.7 GRIFOLS (SPAIN)

8.8 HOLOGIC INC. (USA)

8.9 MYLAN N.V. (USA)

8.10 OXFORD NANOPORE TECHNOLOGIES (UK)

8.11 PERKINELMER (USA)

8.12 QIAGEN N.V. (GERMANY)

8.13 ROCHE DIAGNOSTICS (SWITZERLAND)

8.14 SIEMENS HEALTHINEERS (GERMANY)

8.15 SYSMEX CORPORATION (JAPAN)

8.16 THERMO FISHER SCIENTIFIC (USA)

8.17 OTHER ACTIVE PLAYERS

Chapter 9: Global Rapid Diagnostics Market By Region

9.1 Overview

9.2. North America Rapid Diagnostics Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecasted Market Size By Product

9.2.4.1 Over The Counter (OTC) Kits

9.2.4.2 Professional Kits

9.2.5 Historic and Forecasted Market Size By Technology

9.2.5.1 Lateral Flow

9.2.5.2 Agglutination

9.2.5.3 Solid Phase

9.2.5.4 Other Technologies.

9.2.6 Historic and Forecasted Market Size By Application

9.2.6.1 Blood Glucose Testing

9.2.6.2 Infectious Disease Testing

9.2.6.3 (COVID-19

9.2.6.4 Hepatitis

9.2.6.5 HIV

9.2.6.6 Influenza

9.2.6.7 Others)Cardiometabolic Testing

9.2.6.8 Pregnancy and Fertility Testing

9.2.6.9 Fecal Occult Blood Testing

9.2.6.10 Coagulation Testing

9.2.6.11 Toxicology Testing

9.2.6.12 Lipid Profile Testing

9.2.6.13 Other Applications

9.2.7 Historic and Forecasted Market Size By End User

9.2.7.1 Hospitals & Clinics

9.2.7.2 Home Care

9.2.7.3 Diagnostic Laboratories

9.2.8 Historic and Forecast Market Size by Country

9.2.8.1 US

9.2.8.2 Canada

9.2.8.3 Mexico

9.3. Eastern Europe Rapid Diagnostics Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecasted Market Size By Product

9.3.4.1 Over The Counter (OTC) Kits

9.3.4.2 Professional Kits

9.3.5 Historic and Forecasted Market Size By Technology

9.3.5.1 Lateral Flow

9.3.5.2 Agglutination

9.3.5.3 Solid Phase

9.3.5.4 Other Technologies.

9.3.6 Historic and Forecasted Market Size By Application

9.3.6.1 Blood Glucose Testing

9.3.6.2 Infectious Disease Testing

9.3.6.3 (COVID-19

9.3.6.4 Hepatitis

9.3.6.5 HIV

9.3.6.6 Influenza

9.3.6.7 Others)Cardiometabolic Testing

9.3.6.8 Pregnancy and Fertility Testing

9.3.6.9 Fecal Occult Blood Testing

9.3.6.10 Coagulation Testing

9.3.6.11 Toxicology Testing

9.3.6.12 Lipid Profile Testing

9.3.6.13 Other Applications

9.3.7 Historic and Forecasted Market Size By End User

9.3.7.1 Hospitals & Clinics

9.3.7.2 Home Care

9.3.7.3 Diagnostic Laboratories

9.3.8 Historic and Forecast Market Size by Country

9.3.8.1 Russia

9.3.8.2 Bulgaria

9.3.8.3 The Czech Republic

9.3.8.4 Hungary

9.3.8.5 Poland

9.3.8.6 Romania

9.3.8.7 Rest of Eastern Europe

9.4. Western Europe Rapid Diagnostics Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecasted Market Size By Product

9.4.4.1 Over The Counter (OTC) Kits

9.4.4.2 Professional Kits

9.4.5 Historic and Forecasted Market Size By Technology

9.4.5.1 Lateral Flow

9.4.5.2 Agglutination

9.4.5.3 Solid Phase

9.4.5.4 Other Technologies.

9.4.6 Historic and Forecasted Market Size By Application

9.4.6.1 Blood Glucose Testing

9.4.6.2 Infectious Disease Testing

9.4.6.3 (COVID-19

9.4.6.4 Hepatitis

9.4.6.5 HIV

9.4.6.6 Influenza

9.4.6.7 Others)Cardiometabolic Testing

9.4.6.8 Pregnancy and Fertility Testing

9.4.6.9 Fecal Occult Blood Testing

9.4.6.10 Coagulation Testing

9.4.6.11 Toxicology Testing

9.4.6.12 Lipid Profile Testing

9.4.6.13 Other Applications

9.4.7 Historic and Forecasted Market Size By End User

9.4.7.1 Hospitals & Clinics

9.4.7.2 Home Care

9.4.7.3 Diagnostic Laboratories

9.4.8 Historic and Forecast Market Size by Country

9.4.8.1 Germany

9.4.8.2 UK

9.4.8.3 France

9.4.8.4 The Netherlands

9.4.8.5 Italy

9.4.8.6 Spain

9.4.8.7 Rest of Western Europe

9.5. Asia Pacific Rapid Diagnostics Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecasted Market Size By Product

9.5.4.1 Over The Counter (OTC) Kits

9.5.4.2 Professional Kits

9.5.5 Historic and Forecasted Market Size By Technology

9.5.5.1 Lateral Flow

9.5.5.2 Agglutination

9.5.5.3 Solid Phase

9.5.5.4 Other Technologies.

9.5.6 Historic and Forecasted Market Size By Application

9.5.6.1 Blood Glucose Testing

9.5.6.2 Infectious Disease Testing

9.5.6.3 (COVID-19

9.5.6.4 Hepatitis

9.5.6.5 HIV

9.5.6.6 Influenza

9.5.6.7 Others)Cardiometabolic Testing

9.5.6.8 Pregnancy and Fertility Testing

9.5.6.9 Fecal Occult Blood Testing

9.5.6.10 Coagulation Testing

9.5.6.11 Toxicology Testing

9.5.6.12 Lipid Profile Testing

9.5.6.13 Other Applications

9.5.7 Historic and Forecasted Market Size By End User

9.5.7.1 Hospitals & Clinics

9.5.7.2 Home Care

9.5.7.3 Diagnostic Laboratories

9.5.8 Historic and Forecast Market Size by Country

9.5.8.1 China

9.5.8.2 India

9.5.8.3 Japan

9.5.8.4 South Korea

9.5.8.5 Malaysia

9.5.8.6 Thailand

9.5.8.7 Vietnam

9.5.8.8 The Philippines

9.5.8.9 Australia

9.5.8.10 New Zealand

9.5.8.11 Rest of APAC

9.6. Middle East & Africa Rapid Diagnostics Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecasted Market Size By Product

9.6.4.1 Over The Counter (OTC) Kits

9.6.4.2 Professional Kits

9.6.5 Historic and Forecasted Market Size By Technology

9.6.5.1 Lateral Flow

9.6.5.2 Agglutination

9.6.5.3 Solid Phase

9.6.5.4 Other Technologies.

9.6.6 Historic and Forecasted Market Size By Application

9.6.6.1 Blood Glucose Testing

9.6.6.2 Infectious Disease Testing

9.6.6.3 (COVID-19

9.6.6.4 Hepatitis

9.6.6.5 HIV

9.6.6.6 Influenza

9.6.6.7 Others)Cardiometabolic Testing

9.6.6.8 Pregnancy and Fertility Testing

9.6.6.9 Fecal Occult Blood Testing

9.6.6.10 Coagulation Testing

9.6.6.11 Toxicology Testing

9.6.6.12 Lipid Profile Testing

9.6.6.13 Other Applications

9.6.7 Historic and Forecasted Market Size By End User

9.6.7.1 Hospitals & Clinics

9.6.7.2 Home Care

9.6.7.3 Diagnostic Laboratories

9.6.8 Historic and Forecast Market Size by Country

9.6.8.1 Turkiye

9.6.8.2 Bahrain

9.6.8.3 Kuwait

9.6.8.4 Saudi Arabia

9.6.8.5 Qatar

9.6.8.6 UAE

9.6.8.7 Israel

9.6.8.8 South Africa

9.7. South America Rapid Diagnostics Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecasted Market Size By Product

9.7.4.1 Over The Counter (OTC) Kits

9.7.4.2 Professional Kits

9.7.5 Historic and Forecasted Market Size By Technology

9.7.5.1 Lateral Flow

9.7.5.2 Agglutination

9.7.5.3 Solid Phase

9.7.5.4 Other Technologies.

9.7.6 Historic and Forecasted Market Size By Application

9.7.6.1 Blood Glucose Testing

9.7.6.2 Infectious Disease Testing

9.7.6.3 (COVID-19

9.7.6.4 Hepatitis

9.7.6.5 HIV

9.7.6.6 Influenza

9.7.6.7 Others)Cardiometabolic Testing

9.7.6.8 Pregnancy and Fertility Testing

9.7.6.9 Fecal Occult Blood Testing

9.7.6.10 Coagulation Testing

9.7.6.11 Toxicology Testing

9.7.6.12 Lipid Profile Testing

9.7.6.13 Other Applications

9.7.7 Historic and Forecasted Market Size By End User

9.7.7.1 Hospitals & Clinics

9.7.7.2 Home Care

9.7.7.3 Diagnostic Laboratories

9.7.8 Historic and Forecast Market Size by Country

9.7.8.1 Brazil

9.7.8.2 Argentina

9.7.8.3 Rest of SA

Chapter 10 Analyst Viewpoint and Conclusion

10.1 Recommendations and Concluding Analysis

10.2 Potential Market Strategies

Chapter 11 Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

|

Rapid Diagnostics Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 21.62 Billion |

|

Forecast Period 2024-32 CAGR: |

9.02% |

Market Size in 2032: |

USD 47.03 Billion |

|

Segments Covered: |

By Product |

|

|

|

By Technology |

|

||

|

By Application |

|

||

|

End user |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||