Precision Motion Components Market Synopsis:

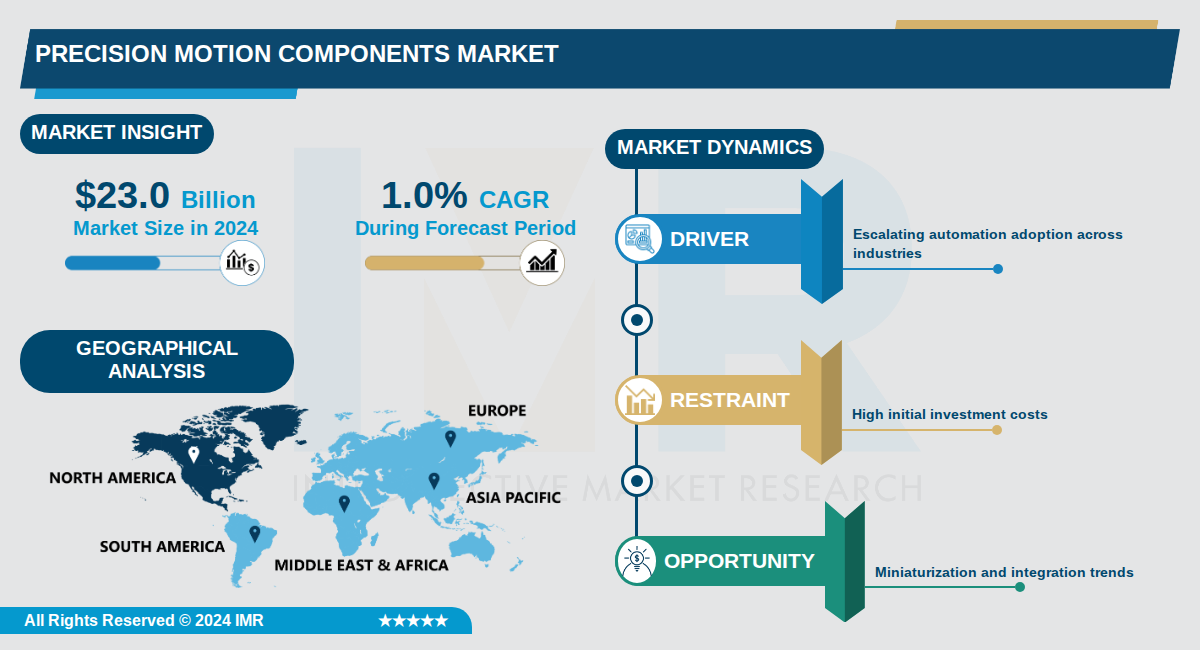

Precision Motion Components Market Size Was Valued at USD 23.0 Billion in 2024, and is Projected to Reach USD 24.0 Billion by 2035, Growing at a CAGR of 1.0% From 2024-2035.

The Precision Motion Components Market reached $23.0 billion in 2024 and is projected to grow to $24.0 billion by 2035, reflecting a compound annual growth rate (CAGR) of 1.0%. This market encompasses high-precision components essential for accurate and repeatable movements in various applications, driven by ongoing industrialization and technological advancements.

Key sectors fueling demand include industrial machinery, robotics, automotive, aerospace, and healthcare, where precision is critical for operations like CNC machining, packaging, and material handling. The Asia Pacific region leads due to its robust manufacturing hubs in China, Japan, and South Korea, while North America benefits from advanced technological infrastructure and innovation.

Major players such as Bosch Rexroth AG, THK Co., Ltd., NSK Ltd., Parker Hannifin Corporation, and Schneider Electric SE dominate the landscape, focusing on innovation in motion control solutions. Despite varying growth projections across reports, the market's steady expansion underscores its importance in enhancing manufacturing efficiency and automation.

Precision Motion Components Market Trend Analysis:

Miniaturization of Motion Components

- Manufacturers are developing increasingly compact and lightweight precision motion components to meet demands in portable medical devices and micro-robotics. For instance, Physik Instrumente (PI) has introduced piezoelectric actuators under 1mm in size that achieve sub-micron resolution, enabling precise positioning in space-constrained endoscopy tools. This trend reduces system weight by up to 40% compared to traditional servo motors, as seen in Novanta's integrated modules for handheld surgical robots.

- In semiconductor applications, miniaturized linear actuators from Parker Hannifin support wafer handling with 0.1 micron accuracy in equipment half the size of previous generations. Moog's aerospace components for satellites weigh 30% less while maintaining radiation-hardened performance, driving a market segment projected at $3 billion. These advancements lower assembly costs by integrating sensors directly into actuators, simplifying designs for high-volume production.

Integration of Smart Sensors and AI

- Precision motion components are increasingly combining motors, sensors, and AI-driven controllers into single intelligent modules for real-time feedback and predictive maintenance. AEROTECH's systems use embedded AI to adjust torque dynamically, reducing downtime by 25% in semiconductor fabs like those operated by TSMC. This integration supports closed-loop control growing at 6.6% CAGR, essential for robotics and high-speed manufacturing.

- Fanuc Corporation's cobots incorporate smart gear racks with sensor fusion for 99.9% repeatability in assembly lines, while Yaskawa Electric's linear motors leverage machine learning to optimize motion paths, boosting throughput by 15%. In medical devices, PI's piezo stages with AI calibration achieve nanometer precision for microscopy, addressing demands in biotech firms like Illumina. This trend is fueled by Industry 4.0, with servo-based systems holding the largest market share due to superior dynamic response.

Shift to Energy-Efficient Linear Motors

- Linear motor systems are gaining traction with a projected 7.9% CAGR, offering direct drive motion that eliminates mechanical wear and cuts energy use by 20-30% over traditional ball screws. Bosch Rexroth's ironless linear motors power high-speed pick-and-place machines in electronics assembly, delivering 5g acceleration with 50% less power than stepper systems. This shift supports sustainability goals in regions like Europe, where regulations mandate eco-friendly materials.

- THK's advanced linear guides in CNC machines from SCHNEEBERGER reduce friction losses, extending lifespan to over 100,000 km while complying with energy efficiency standards. In North America's reshoring initiatives, these motors equip warehouse automation at Amazon facilities, enhancing productivity with lower operational costs. The trend aligns with the global motion control market's growth from $17.31 billion in 2026 to $27.85 billion by 2034.

Precision Motion Components Market Segment Analysis:

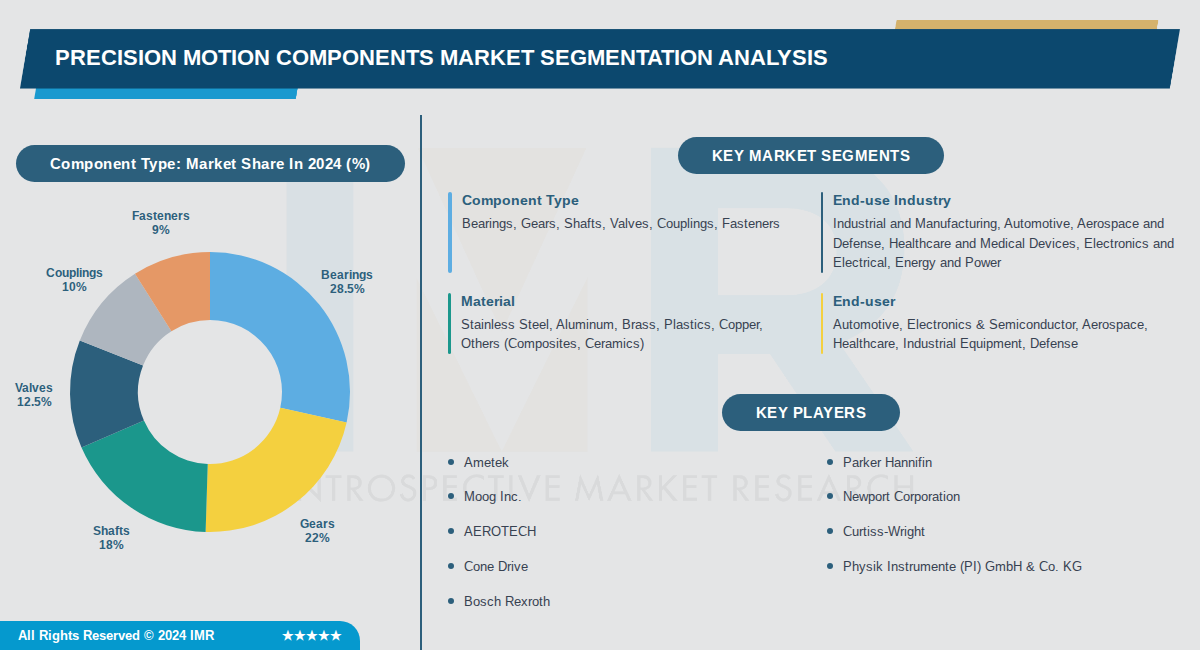

Precision Motion Components Market is Segmented on the basis of By Component Type, By End-use Industry, By Material

By Component Type, Bearings segment is expected to dominate the market during the forecast period

- Bearings dominate due to their critical role in reducing friction and enabling smooth, high-precision movement in machinery across automotive, aerospace, and industrial applications.

- The rise of automation and robotics has increased demand for advanced bearings with tight tolerances, accounting for over 70% of precision motion failures linked to bearing wear.

By End-use Industry, Industrial and Manufacturing segment is expected to dominate the market during the forecast period

- Industrial and Manufacturing leads due to ongoing modernization of factories and heavy reliance on precision components for CNC machines, robotics, and automated assembly lines.

- Automation trends under Industry 4.0 have driven over 40% market share as manufacturers prioritize components meeting micron-level tolerances for efficiency and quality.

By Material, Stainless Steel segment is expected to dominate the market during the forecast period

- Stainless steel dominates owing to its exceptional corrosion resistance, strength, and machinability essential for durable precision motion parts in harsh environments.

- It captures over 35% share in automotive and aerospace where high-load, fatigue-resistant properties ensure long-term reliability in motion systems.

By End-user, Automotive segment is expected to dominate the market during the forecast period

- Automotive leads driven by surging EV production requiring thousands of precision parts per vehicle for electric motors, transmissions, and lightweight structures.

- Over 50% of precision motion components in vehicles are for powertrain and chassis systems, boosted by fuel efficiency mandates and EV transition.

Precision Motion Components Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast Period

- North America dominates the Precision Motion Components market due to its leadership in innovation and adoption, particularly driven by powerhouse industries like aerospace, defense, and semiconductors. Key countries such as the United States lead with significant research and development investments and a robust industrial base. This positions the region ahead of others in market concentration and advanced technology deployment.

- The region's strong infrastructure supports high-tech manufacturing, with favorable regulations and government investments in defense and semiconductor sectors accelerating demand. A mature ecosystem for automation and precision engineering ensures quick adoption of miniaturized, high-accuracy components. Economic stability and skilled workforce further enhance market maturity compared to faster-growing but less concentrated regions like Asia-Pacific.

- Major players including Parker Hannifin and Moog maintain a significant presence, driving innovation in motors, actuators, and controllers. Recent developments focus on higher accuracy, speed, and payload capacity for aerospace and medical applications. These companies leverage North America's R&D hubs to stay ahead in a moderately concentrated market.

Active Key Players in the Precision Motion Components Market:

- Ametek (USA)

- Parker Hannifin (USA)

- Moog Inc. (USA)

- Newport Corporation (USA)

- AEROTECH (USA)

- Curtiss-Wright (USA)

- Cone Drive (USA)

- Physik Instrumente (PI) GmbH & Co. KG (Germany)

- Bosch Rexroth (Germany)

- Schunk GmbH & Co. KG (Germany)

- Igus GmbH (Germany)

- Siemens AG (Germany)

- Novanta (USA)

- Altra (USA)

- Honeywell International (USA)

- ABB Group (Switzerland)

- THK (Japan)

- Ewellix (Sweden)

- Hiwin (Taiwan)

- SMC Corporation (Japan)

- Other Active Players

|

Precision Motion Components Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 23.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

1.0 % |

Market Size in 2035: |

USD 24.0 Billion |

|

Segments Covered: |

By Component Type |

|

|

|

By End-use Industry |

|

||

|

By Material |

|

||

|

By End-user |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Precision Motion Components Market by Component Type (2017-2035)

4.1 Precision Motion Components Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Bearings

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Gears

4.5 Shafts

4.6 Valves

4.7 Couplings

4.8 Fasteners

Chapter 5: Precision Motion Components Market by End-use Industry (2017-2035)

5.1 Precision Motion Components Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Industrial and Manufacturing

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Automotive

5.5 Aerospace and Defense

5.6 Healthcare and Medical Devices

5.7 Electronics and Electrical

5.8 Energy and Power

Chapter 6: Precision Motion Components Market by Material (2017-2035)

6.1 Precision Motion Components Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Stainless Steel

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Aluminum

6.5 Brass

6.6 Plastics

6.7 Copper

6.8 Others (Composites

6.9 Ceramics)

Chapter 7: Precision Motion Components Market by End-user (2017-2035)

7.1 Precision Motion Components Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Automotive

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Electronics & Semiconductor

7.5 Aerospace

7.6 Healthcare

7.7 Industrial Equipment

7.8 Defense

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Precision Motion Components Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 AMETEK

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 PARKER HANNIFIN

8.4 MOOG INC.

8.5 NEWPORT CORPORATION

8.6 AEROTECH

8.7 CURTISS-WRIGHT

8.8 CONE DRIVE

8.9 PHYSIK INSTRUMENTE (PI) GMBH & CO. KG

8.10 BOSCH REXROTH

8.11 SCHUNK GMBH & CO. KG

8.12 IGUS GMBH

8.13 SIEMENS AG

8.14 NOVANTA

8.15 ALTRA

8.16 HONEYWELL INTERNATIONAL

8.17 ABB GROUP

8.18 THK

8.19 EWELLIX

8.20 HIWIN

8.21 SMC CORPORATION

Chapter 9: Global Precision Motion Components Market By Region

9.1 Overview

9.2. North America Precision Motion Components Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Precision Motion Components Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Precision Motion Components Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Precision Motion Components Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Precision Motion Components Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Precision Motion Components Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Precision Motion Components Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 23.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

1.0 % |

Market Size in 2035: |

USD 24.0 Billion |

|

Segments Covered: |

By Component Type |

|

|

|

By End-use Industry |

|

||

|

By Material |

|

||

|

By End-user |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||