Precision Medical Devices Market Synopsis:

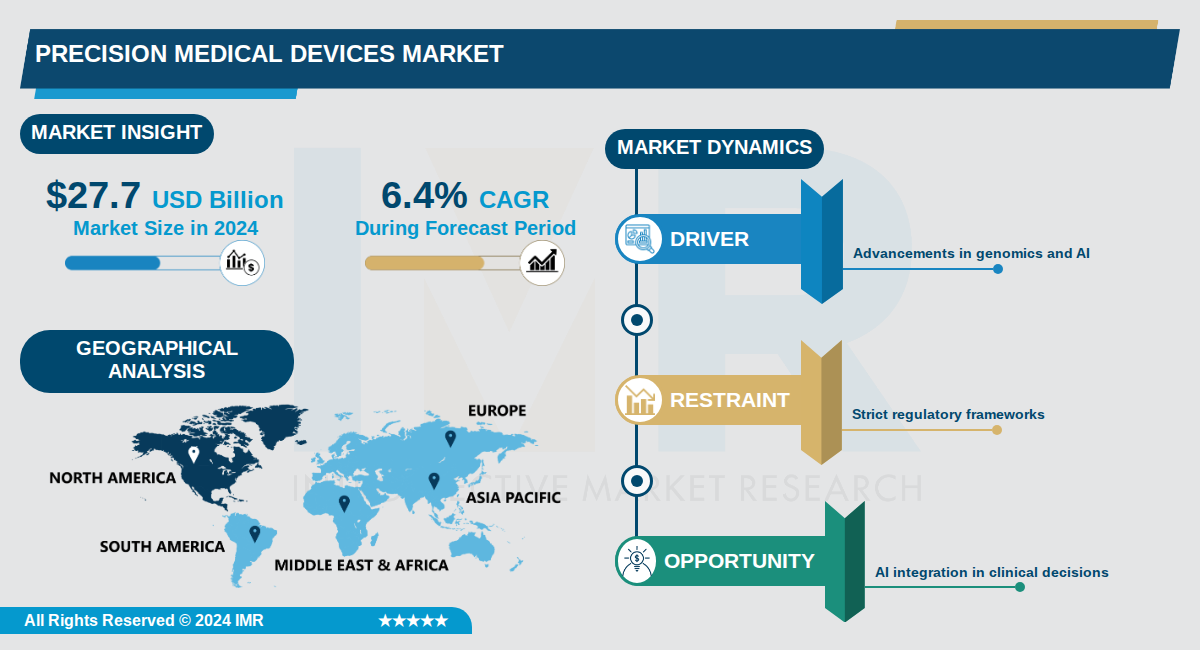

Precision Medical Devices Market Size Was Valued at USD 27.7 Billion in 2024, and is Projected to Reach USD 55.0 Billion by 2035, Growing at a CAGR of 6.4% From 2024-2035.

The Precision Medical Devices Market, a critical subset of precision medicine, was valued at $27.7 billion in 2024 and is projected to reach $55.0 billion by 2035, growing at a compound annual growth rate (CAGR) of 6.4%. This expansion reflects the increasing integration of advanced diagnostics and therapeutics tailored to individual patient profiles, driven by innovations in genomics and AI.

Key segments within the market include oncology diagnostics and devices, which dominate due to early adoption of genetic profiling and companion diagnostics, alongside rapid growth in rare genetic disease applications. Major players such as Roche Diagnostics, Illumina, Thermo Fisher Scientific, and Medtronic are leading advancements in next-generation sequencing, liquid biopsies, and automated insulin delivery systems.

North America holds the largest market share, supported by robust biotech ecosystems and regulatory frameworks, while Asia-Pacific is poised for the fastest growth due to investments in healthcare infrastructure and rising chronic disease prevalence. Hospitals and clinics remain the primary end-users, leveraging integrated precision tools for enhanced patient outcomes.

Precision Medical Devices Market Trend Analysis:

Expansion of Companion Diagnostics in Oncology

- More than 15 FDA clearances since 2024 have linked targeted drugs to specific biomarker tests, expanding the patient pool for precision oncology treatments. Illumina's TruSight Oncology Comprehensive became the first FDA-cleared pan-cancer in-vitro diagnostic profiling over 500 biomarkers in one run, enabling comprehensive genomic analysis. FoundationOne CDx now detects NTRK fusions across solid tumors, matching patients to larotrectinib therapy and driving a virtuous cycle of co-developed assays and drugs.

- The therascreen KRAS RGQ PCR Kit guides sotorasib plus panitumumab for KRAS G12C-mutated colorectal cancer, demonstrating how companion diagnostics refine treatment selection. Guardant Health's Shield blood test offers non-invasive colorectal cancer detection with 83% sensitivity in average-risk adults. Next-generation sequencing holds 33.78% market share in 2025, establishing it as the gold standard for pharmacogenomic workflows.

- These diagnostics incentivize drug developers to co-develop assays aligned with clinical trials, accelerating biomarker-guided therapies. Oncology remains the dominant application segment, fueled by molecularly targeted cancer drugs and affordable NGS tumor analysis.

Integration of AI and Machine Learning in Precision Diagnostics

- AI and machine learning represent the fastest-growing segment at a 17.62% CAGR, scaling variant annotation and detecting mutational signatures for tumor aggressiveness. Tools optimize algorithmic trial enrollment and translate complex data into actionable insights. Proteomics firm SomaLogic measures 10,000 proteins from a microliter sample, with AI models generating early disease risk scores.

- Software like Qlucore Omics Explorer and digital pathology AI support high-throughput technologies such as NGS, PCR, IHC, and mass spectrometry for biomarker discovery. In precision oncology, AI enhances clinical decision-making by processing genomic data for personalized therapies.

- Diagnostic labs and genomic providers like those using Illumina platforms adopt AI to interpret genetic data, improving patient stratification. Asia-Pacific's growth, with China's AI-centered precision health roadmap, amplifies AI adoption through national genome initiatives.

Rise of Multi-Omic Technologies and Biomarker Discovery

- Maturation of multi-omic technologies drives biomarker-driven development, combining genomics, proteomics, and other data layers for precise interventions. Companion diagnostics and biomarker tools grow at the fastest CAGR, employing NGS and software for data processing and patient classification. Oncology and rare genetic disorders lead due to strong genotype-phenotype links.

- Rare and genetic disorders segment expands rapidly, as 80% of rare diseases are genetic, with precision tools improving outcomes via timely genomic data. Applications in neurology and cardiology use molecular markers for risk stratification, supported by large datasets.

- Asia-Pacific leads regional growth at 14.12% CAGR, with China's Human Genome Project 2 and India's Genome India Project funding multi-omic research for region-specific targets. North America dominates via advanced genome sequencing post-Human Genome Project.

Precision Medical Devices Market Segment Analysis:

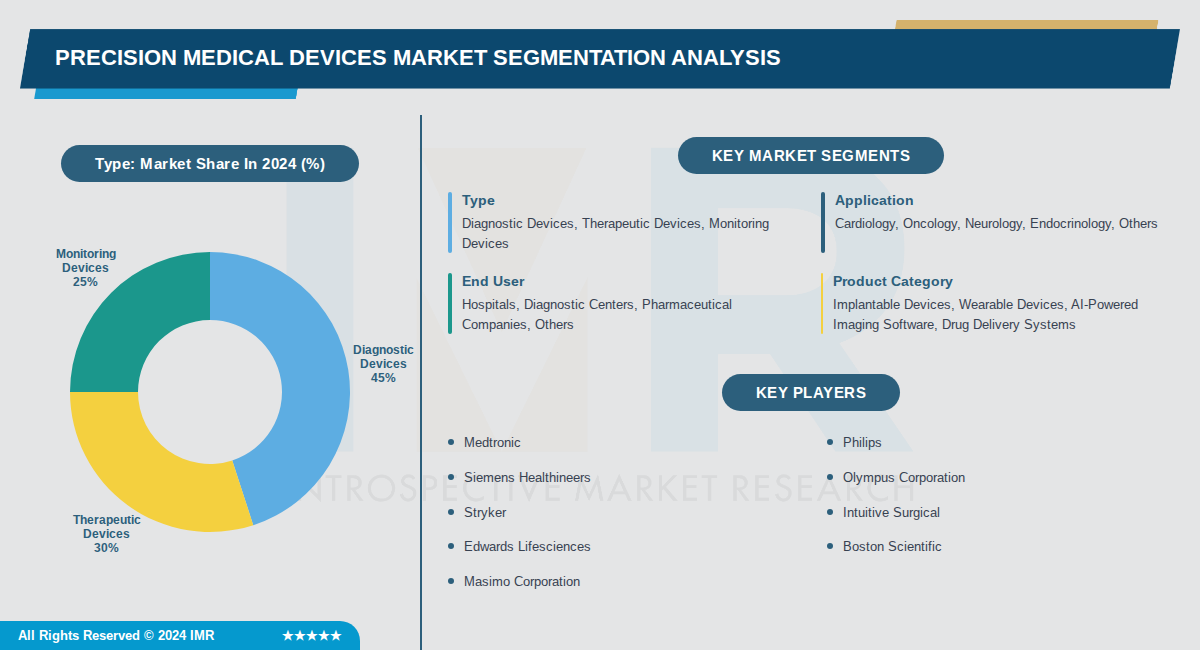

Precision Medical Devices Market is Segmented on the basis of By Type, By Application, By End User

By Type, Diagnostic Devices segment is expected to dominate the market during the forecast period

- Diagnostic devices dominate due to rising demand for early detection and personalized diagnostics in precision medicine, including AI-powered imaging and genetic testing tools.

- Advancements like non-invasive glucose monitors and companion diagnostics drive over 45% market share amid increasing chronic disease prevalence.

By Application, Cardiology segment is expected to dominate the market during the forecast period

- Cardiology leads with devices like pacemakers, defibrillators, and stents, fueled by high cardiovascular disease rates and minimally invasive innovations.

- North America and Europe's advanced healthcare systems prioritize cardiovascular precision devices, capturing dominant global share.

By End User, Hospitals segment is expected to dominate the market during the forecast period

- Hospitals dominate through integrated ecosystems for diagnostics, therapeutics, and monitoring with interdisciplinary teams for personalized care.

- High adoption of cutting-edge precision devices in hospitals for chronic conditions like cancer and heart disease secures over 50% revenue share.

By Product Category, Implantable Devices segment is expected to dominate the market during the forecast period

- Implantable devices such as drug delivery systems and pacemakers lead due to their role in long-term precision treatment and monitoring.

- Technological advancements and regulatory approvals in well-developed markets boost implantable devices to the largest segment.

Precision Medical Devices Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast Period

- North America dominates the precision medical devices market, primarily led by the United States, followed by Canada and Mexico. The region is projected to hold the largest revenue share, around 45-54% through 2035. This leadership stems from advanced adoption of personalized medicine technologies and a robust healthcare ecosystem.

- The region benefits from well-established infrastructure including hospitals, research institutes, and diagnostic labs, alongside favorable regulatory frameworks from bodies like the U.S. FDA and Health Canada. These factors streamline approvals and market entry for precision devices. Government initiatives and plummeting costs of next-generation sequencing further accelerate growth.

- Major players such as Illumina, Thermo Fisher, Roche, Pfizer, and Novartis are heavily concentrated here, driving innovations in sequencing and companion diagnostics. Recent developments include Regeneron's acquisition of 23andMe's genetic database and Bayer's expansions in Mexico. Strong venture funding and clinical adoption solidify North America's position.

Active Key Players in the Precision Medical Devices Market:

- Medtronic (USA)

- Philips (Netherlands)

- Siemens Healthineers (Germany)

- Olympus Corporation (Japan)

- Stryker (USA)

- Intuitive Surgical (USA)

- Edwards Lifesciences (USA)

- Boston Scientific (USA)

- Masimo Corporation (USA)

- Abiomed (USA)

- Shockwave Medical (USA)

- CMR Surgical (UK)

- HemoSonics (USA)

- Synchron (USA)

- Boston Micro Fabrication (USA)

- ABLE Human Motion (Netherlands)

- Garwood Medical Devices (USA)

- Other Active Players

|

Precision Medical Devices Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 27.7 Billion |

|

Forecast Period 2024-2035 CAGR: |

6.4 % |

Market Size in 2035: |

USD 55.0 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By End User |

|

||

|

By Product Category |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Precision Medical Devices Market by Type (2017-2035)

4.1 Precision Medical Devices Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Diagnostic Devices

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Therapeutic Devices

4.5 Monitoring Devices

Chapter 5: Precision Medical Devices Market by Application (2017-2035)

5.1 Precision Medical Devices Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Cardiology

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Oncology

5.5 Neurology

5.6 Endocrinology

5.7 Others

Chapter 6: Precision Medical Devices Market by End User (2017-2035)

6.1 Precision Medical Devices Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Hospitals

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Diagnostic Centers

6.5 Pharmaceutical Companies

6.6 Others

Chapter 7: Precision Medical Devices Market by Product Category (2017-2035)

7.1 Precision Medical Devices Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Implantable Devices

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Wearable Devices

7.5 AI-Powered Imaging Software

7.6 Drug Delivery Systems

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Precision Medical Devices Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 MEDTRONIC

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 PHILIPS

8.4 SIEMENS HEALTHINEERS

8.5 OLYMPUS CORPORATION

8.6 STRYKER

8.7 INTUITIVE SURGICAL

8.8 EDWARDS LIFESCIENCES

8.9 BOSTON SCIENTIFIC

8.10 MASIMO CORPORATION

8.11 ABIOMED

8.12 SHOCKWAVE MEDICAL

8.13 CMR SURGICAL

8.14 HEMOSONICS

8.15 SYNCHRON

8.16 BOSTON MICRO FABRICATION

8.17 ABLE HUMAN MOTION

8.18 GARWOOD MEDICAL DEVICES

Chapter 9: Global Precision Medical Devices Market By Region

9.1 Overview

9.2. North America Precision Medical Devices Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Precision Medical Devices Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Precision Medical Devices Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Precision Medical Devices Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Precision Medical Devices Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Precision Medical Devices Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Precision Medical Devices Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 27.7 Billion |

|

Forecast Period 2024-2035 CAGR: |

6.4 % |

Market Size in 2035: |

USD 55.0 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By End User |

|

||

|

By Product Category |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||