Posterior Segment Eye Disorders Market Synopsis:

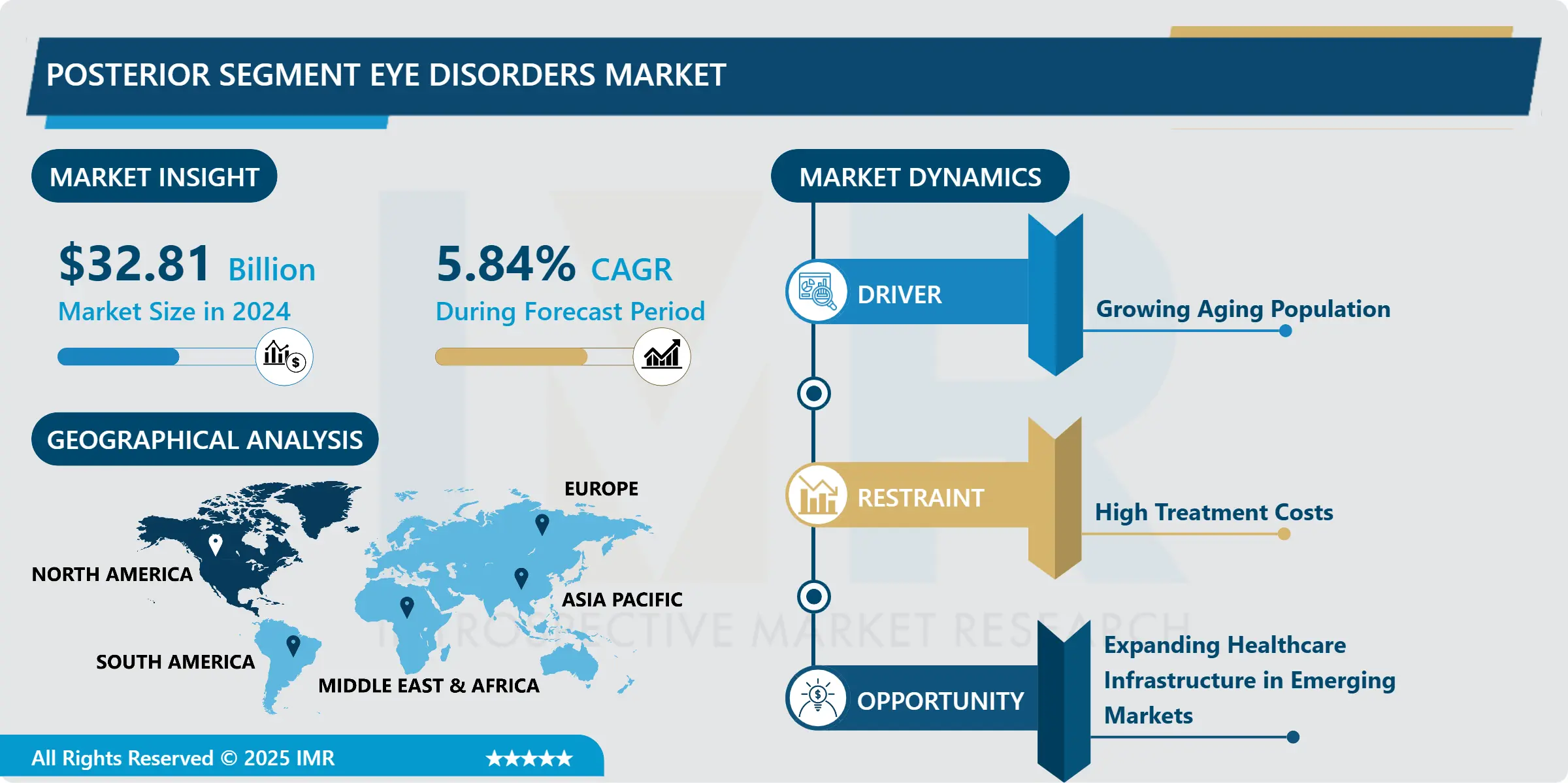

Posterior Segment Eye Disorders Market Size Was Valued at USD 32.81 Billion in 2024, and is Projected to Reach USD 61.26 Billion by 2035, Growing at a CAGR of 5.82% From 2025-2035.

The term Posterior Segment Eye Disorders Market is used to identify the healthcare business domain in the diagnosis, treatment, and control of diseases and diseases in the eye’s posterior segment, including the retina, macula, vitreous, and optic nerve. These disorders cause extensive vision loss and may result in blindness, so early and adequate treatment are critical. These are medical devices, pharmaceuticals, and surgical procedures used to treat retinal disorders including; diabetic retinopathy, macular degeneration, retinal vein occlusion, and other posterior segment diseases.

The market for the Posterior Segment Eye Disorders is rapidly growing in the global market mainly because of the many people who are suffering from age related diseases affecting the eye such as macular degeneration, diabetic retinopathy and retinal vein occlusion. Increased aging population worldwide coupled with increasing incidence of diabetes is have resulted in increasing number of patient developing retinal disorders hence the need for specialized treatments. It is propelled by growth in diagnostic tools, such as OCT, and fundus imaging for improved comprehension and management of posterior segment diseases.

There main drivers for the market growth is advanced treatments that are being developed to treat retinal diseases including the treatments like anti-VEGF therapies, corticosteroids and gene therapies. Also, the rising consciousness level of both healthcare professionals and patients about early detection and treatment is among key factors that continue to fuel growth in the particular market. Another positive aspect that may be expected from the increased number of clinical trials and investigations on new therapies is that the variety of treatment will also increase and guarantee more satisfactory results in the efforts to address patients’ needs.

Posterior Segment Eye Disorders Market Trend Analysis:

Adoption of Advanced Biologics and Minimally Invasive Therapies

- Advanced biologics and in particular anti-VEGF therapies are one of the most defined emerging trends of the Posterior Segment Eye Disorders Market. These therapies have changed the management of the age-related macular degeneration, diabetic macular edema and retinal vein occlusion. Avastin, Lucentis and Eylea are the only drugs belonging to the Anti-VEGF class that have proved to offer great results in managing of these diseases and in turn minimizing surgeries among patients.

- This tendency is rather obvious because a great number of less invasive methods of the treatment, such as intravitreal injections and laser therapies, appear and offer patients suitable options instead of surgical procedures. That move towards biologics as well as less invasive treatments is likely to increase in the coming years as more treatments are discovered, consequently fuelling the market for biologics.

Expansion of Market in Emerging Economies

- New economies are expected to offer major growth prospects in the Posterior Segment Eye Disorders Market. Diabetes and other risk factors related to posterior segment eye diseases have been on the rise especially in nations in the Asia Pacific, Central and Latin-American regions as well as the Middle-East region. But the problem that many of these regions encounter is that they have relatively restricted opportunities to obtain specific diagnostic and therapeutic technologies. Those organisations which are able to deliver effective solutions at lower costs and with higher access to these markets will be rewarded with significant numbers of customers that remain unplumbed at the moment.

- Moreover, it has strategic partnerships with healthcare providers and governments to build up the healthcare industry and education as some essential ways that will significantly influence market development. The above challenges can be addressed by new, low-cost tools for diagnosing and treating retinal conditions therefore reducing the barriers to market opportunities in growing markets.

Posterior Segment Eye Disorders Market Segment Analysis:

Posterior Segment Eye Disorders Market Segmented on the basis of type, treatment, end user and Region.

By Type, Diabetic Retinopathy segment is expected to dominate the market during the forecast period

- The market is primarily divided based on the nature of the disease to include Diabetic Retinopathy, Age-related Macular Degeneration (AMD), Retinal Vein Occlusion, Macular Edema and Retinal Detachment. Due to diabetic Retinopathy, blindness is a common occurrence in diabetic individuals and continues to fuel this market. Another remarkable disease is Age-related Macular Degeneration (AMD) that develops in the central part of the retina and is widespread among the elders, so there is an increased need for treatment for such pathology. The second most common type of occlusion is the Retinal Vein Occlusion which may lead to vision loss and the management of this disease also is rapidly developing.

- Other diseases, which comprise the market of AMD, include Macular Edema and Retinal Detachment retinal disease. Macular oedema is a complication that comes with difficulties such as diabetic retinopathy and causes swelling of the macula, distorting central vision. Retinal Detachment though it is rare in occurrence, is among the emergent diseases that if not effectively treated may lead to blindness at its worst stages. These types, amongst others, are a wide range of posterior segment eye disorders; all of which area are characterized by specialized management leading to more emphasis on diagnostic/research equipment, surgical interventions and therapeutic products in the market.

By Treatment, Medications segment expected to held the largest share

- The Posterior Segment Eye Disorders Market is primarily segmented by treatment modalities which belong to medications, surgical procedures, and diagnostic tools. These include; Anti-VEGF (vascular endothelial growth factor) treatments, steroids, and gene therapies which help solve problems such as Age-related Macular Degeneration (AMD), diabetic retinopathy, and macular edema. Lucentis, Eylea and Avastin, the Anti-VEGF treatments have fairly transformed the way retinal diseases are managed due to their action of preventing development of abnormal vessels besides controlling oedema. Steroids are administered to control inflammation and macular edema, while gene treatment is a relatively newer treatment technique that works on eliminating genes involving in retinal diseases.

- Besides medications, there are medical interventions like vitrectomy, retinal surgery required for treatment of such diseases as retinal detachment, macular hole and etc. Vitrectomy is an operation in which the vitreous gel is removed from the patient’s eye; it is used to treat a wide range of retinal diseases. Laser photocoagulation and cryotherapy are used in the treatment of the retinal tears, detachments and to prevent their progression. In addition, there’s a need for auxiliary diagnostic instruments in diagnosing posterior segment diseases, such as OCT and fundus cameras. OCT is used for high spatial resolution imaging of retina for early diagnosis of retinal conditions; while fundus cameras are used for fundus imaging for diagnosis and monitoring. These treatments and devices are for preserving the health of patients as well as being triggers for development of the market.

Posterior Segment Eye Disorders Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

- In 2023, the Posterior Segment Eye Disorders Market North America shall remain the key market captivating a striking market share in the worldwide market. At the same time, the U.S. takes one of the leading places, owing to the developed healthcare system, overall availability of new generation therapies, and a high incidence of age-related eye pathologies. Finally, projecting the market share in the year 2023 for North America the value is estimated to be of approximately 40-45.

- The factors such as rich pipeline of new treatment, high expenditure on healthcare, existence and presence of key market players also bolster the dominance of this region. Also, the growing prevalence of retinal diseases and the enhanced utilization of imaging and curative solutions make North America the dominant market worldwide.

Active Key Players in the Posterior Segment Eye Disorders Market:

- Alcon (Switzerland)

- Allergan (Ireland)

- Bausch + Lomb (USA)

- Bayer (Germany)

- Boehringer Ingelheim (Germany)

- Bristol-Myers Squibb (USA)

- Chengdu Kanghong Pharmaceutical Group (China)

- D.O.R.C. (Netherlands)

- Genentech (USA)

- Graybug Vision (USA)

- Kubota Vision (Japan)

- Novartis (Switzerland)

- Regeneron Pharmaceuticals (USA)

- Roche (Switzerland)

- Valeant Pharmaceuticals (USA), and Other Active Players.

|

Posterior Segment Eye Disorders Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 32.81 Billion |

|

Forecast Period 2025-35 CAGR: |

5.84% |

Market Size in 2035: |

USD 61.26 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Treatment |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Posterior Segment Eye Disorders Market by Type (2018-2035)

4.1 Posterior Segment Eye Disorders Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Diabetic Retinopathy

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Age-related Macular Degeneration (AMD)

4.5 Retinal Vein Occlusion

4.6 Macular Edema

4.7 Retinal Detachment

4.8 Others

Chapter 5: Posterior Segment Eye Disorders Market by Treatment (2018-2035)

5.1 Posterior Segment Eye Disorders Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Medications (Anti-VEGF

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Steroids

5.5 Gene Therapy)

5.6 Surgical Treatments (Vitrectomy

5.7 Retinal Surgery)

5.8 Diagnostic Devices (OCT

5.9 Fundus Cameras)

Chapter 6: Posterior Segment Eye Disorders Market by End User (2018-2035)

6.1 Posterior Segment Eye Disorders Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Hospitals

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Clinics

6.5 Ambulatory Surgical Centers

6.6 Diagnostic Centers

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Posterior Segment Eye Disorders Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 ALCON (SWITZERLAND)

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 ALLERGAN (IRELAND)

7.4 BAUSCH + LOMB (USA)

7.5 BAYER (GERMANY)

7.6 BOEHRINGER INGELHEIM (GERMANY)

7.7 BRISTOL-MYERS SQUIBB (USA)

7.8 CHENGDU KANGHONG PHARMACEUTICAL GROUP (CHINA)

7.9 D.O.R.C. (NETHERLANDS)

7.10 GENENTECH (USA)

7.11 GRAYBUG VISION (USA)

7.12 KUBOTA VISION (JAPAN)

7.13 NOVARTIS (SWITZERLAND)

7.14 REGENERON PHARMACEUTICALS (USA)

7.15 ROCHE (SWITZERLAND)

7.16 VALEANT PHARMACEUTICALS (USA)

7.17 OTHER ACTIVE PLAYERS

Chapter 8: Global Posterior Segment Eye Disorders Market By Region

8.1 Overview

8.2. North America Posterior Segment Eye Disorders Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size by Type

8.2.4.1 Diabetic Retinopathy

8.2.4.2 Age-related Macular Degeneration (AMD)

8.2.4.3 Retinal Vein Occlusion

8.2.4.4 Macular Edema

8.2.4.5 Retinal Detachment

8.2.4.6 Others

8.2.5 Historic and Forecasted Market Size by Treatment

8.2.5.1 Medications (Anti-VEGF

8.2.5.2 Steroids

8.2.5.3 Gene Therapy)

8.2.5.4 Surgical Treatments (Vitrectomy

8.2.5.5 Retinal Surgery)

8.2.5.6 Diagnostic Devices (OCT

8.2.5.7 Fundus Cameras)

8.2.6 Historic and Forecasted Market Size by End User

8.2.6.1 Hospitals

8.2.6.2 Clinics

8.2.6.3 Ambulatory Surgical Centers

8.2.6.4 Diagnostic Centers

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Posterior Segment Eye Disorders Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size by Type

8.3.4.1 Diabetic Retinopathy

8.3.4.2 Age-related Macular Degeneration (AMD)

8.3.4.3 Retinal Vein Occlusion

8.3.4.4 Macular Edema

8.3.4.5 Retinal Detachment

8.3.4.6 Others

8.3.5 Historic and Forecasted Market Size by Treatment

8.3.5.1 Medications (Anti-VEGF

8.3.5.2 Steroids

8.3.5.3 Gene Therapy)

8.3.5.4 Surgical Treatments (Vitrectomy

8.3.5.5 Retinal Surgery)

8.3.5.6 Diagnostic Devices (OCT

8.3.5.7 Fundus Cameras)

8.3.6 Historic and Forecasted Market Size by End User

8.3.6.1 Hospitals

8.3.6.2 Clinics

8.3.6.3 Ambulatory Surgical Centers

8.3.6.4 Diagnostic Centers

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Posterior Segment Eye Disorders Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size by Type

8.4.4.1 Diabetic Retinopathy

8.4.4.2 Age-related Macular Degeneration (AMD)

8.4.4.3 Retinal Vein Occlusion

8.4.4.4 Macular Edema

8.4.4.5 Retinal Detachment

8.4.4.6 Others

8.4.5 Historic and Forecasted Market Size by Treatment

8.4.5.1 Medications (Anti-VEGF

8.4.5.2 Steroids

8.4.5.3 Gene Therapy)

8.4.5.4 Surgical Treatments (Vitrectomy

8.4.5.5 Retinal Surgery)

8.4.5.6 Diagnostic Devices (OCT

8.4.5.7 Fundus Cameras)

8.4.6 Historic and Forecasted Market Size by End User

8.4.6.1 Hospitals

8.4.6.2 Clinics

8.4.6.3 Ambulatory Surgical Centers

8.4.6.4 Diagnostic Centers

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Posterior Segment Eye Disorders Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size by Type

8.5.4.1 Diabetic Retinopathy

8.5.4.2 Age-related Macular Degeneration (AMD)

8.5.4.3 Retinal Vein Occlusion

8.5.4.4 Macular Edema

8.5.4.5 Retinal Detachment

8.5.4.6 Others

8.5.5 Historic and Forecasted Market Size by Treatment

8.5.5.1 Medications (Anti-VEGF

8.5.5.2 Steroids

8.5.5.3 Gene Therapy)

8.5.5.4 Surgical Treatments (Vitrectomy

8.5.5.5 Retinal Surgery)

8.5.5.6 Diagnostic Devices (OCT

8.5.5.7 Fundus Cameras)

8.5.6 Historic and Forecasted Market Size by End User

8.5.6.1 Hospitals

8.5.6.2 Clinics

8.5.6.3 Ambulatory Surgical Centers

8.5.6.4 Diagnostic Centers

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Posterior Segment Eye Disorders Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size by Type

8.6.4.1 Diabetic Retinopathy

8.6.4.2 Age-related Macular Degeneration (AMD)

8.6.4.3 Retinal Vein Occlusion

8.6.4.4 Macular Edema

8.6.4.5 Retinal Detachment

8.6.4.6 Others

8.6.5 Historic and Forecasted Market Size by Treatment

8.6.5.1 Medications (Anti-VEGF

8.6.5.2 Steroids

8.6.5.3 Gene Therapy)

8.6.5.4 Surgical Treatments (Vitrectomy

8.6.5.5 Retinal Surgery)

8.6.5.6 Diagnostic Devices (OCT

8.6.5.7 Fundus Cameras)

8.6.6 Historic and Forecasted Market Size by End User

8.6.6.1 Hospitals

8.6.6.2 Clinics

8.6.6.3 Ambulatory Surgical Centers

8.6.6.4 Diagnostic Centers

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Posterior Segment Eye Disorders Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size by Type

8.7.4.1 Diabetic Retinopathy

8.7.4.2 Age-related Macular Degeneration (AMD)

8.7.4.3 Retinal Vein Occlusion

8.7.4.4 Macular Edema

8.7.4.5 Retinal Detachment

8.7.4.6 Others

8.7.5 Historic and Forecasted Market Size by Treatment

8.7.5.1 Medications (Anti-VEGF

8.7.5.2 Steroids

8.7.5.3 Gene Therapy)

8.7.5.4 Surgical Treatments (Vitrectomy

8.7.5.5 Retinal Surgery)

8.7.5.6 Diagnostic Devices (OCT

8.7.5.7 Fundus Cameras)

8.7.6 Historic and Forecasted Market Size by End User

8.7.6.1 Hospitals

8.7.6.2 Clinics

8.7.6.3 Ambulatory Surgical Centers

8.7.6.4 Diagnostic Centers

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Posterior Segment Eye Disorders Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 32.81 Billion |

|

Forecast Period 2025-35 CAGR: |

5.84% |

Market Size in 2035: |

USD 61.26 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Treatment |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||