Port Equipment Market Synopsis

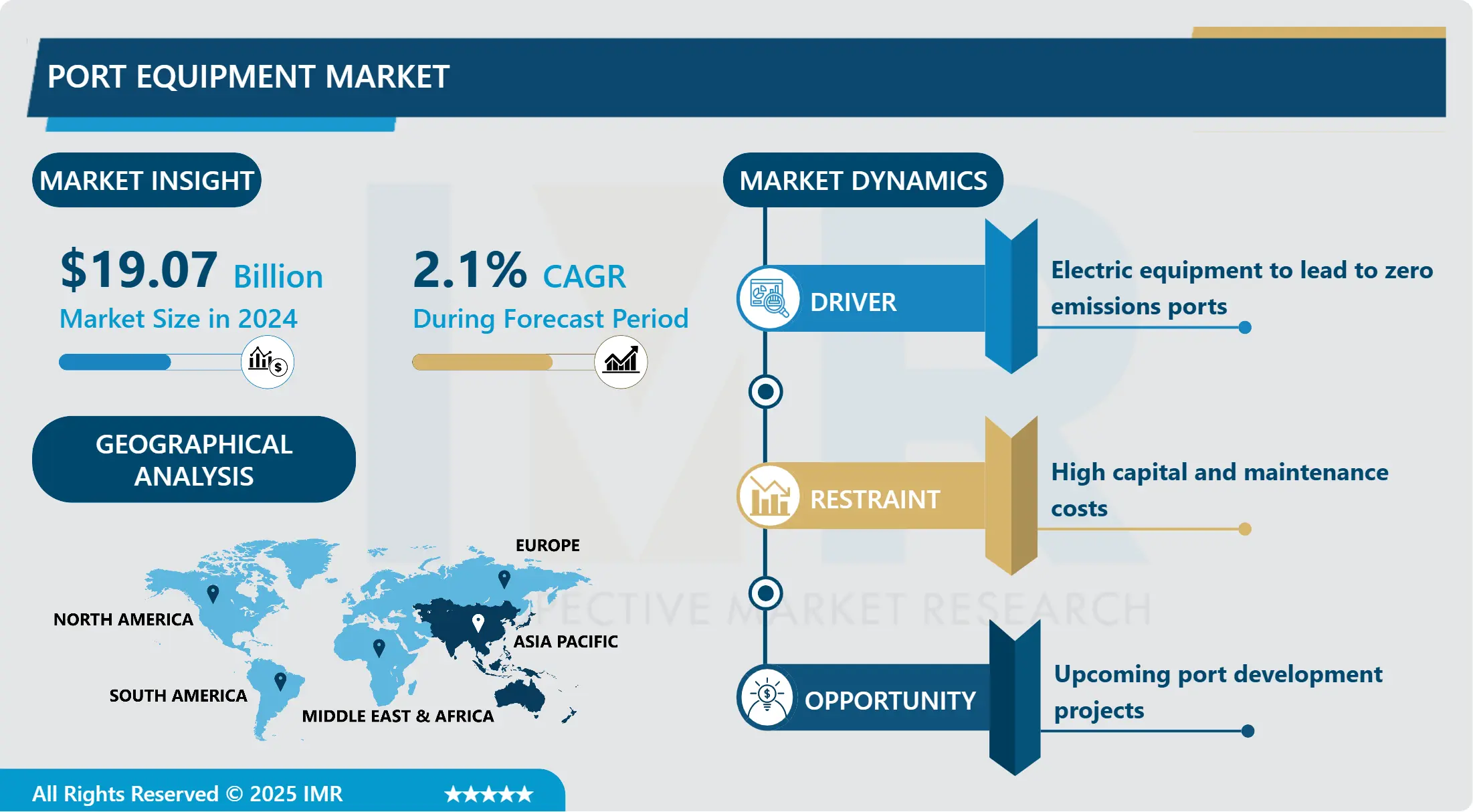

Port Equipment Market Size Was Valued at USD 19.07 Billion in 2024, and is Projected to Reach USD 22.52 Billion by 2032, Growing at a CAGR of 2.1% From 2025-2032.

The port equipment market encompasses a wide range of machinery and technologies utilized in port operations for handling cargo and facilitating maritime trade. This market includes various types of equipment such as cranes (container cranes, ship-to-shore cranes, gantry cranes), forklift trucks, straddle carriers, reach stackers, and terminal tractors, among others. These machines are essential for loading and unloading ships, transporting containers within terminals, and managing logistical operations efficiently. The port equipment market is influenced by factors such as global trade volumes, technological advancements in automation and efficiency, and infrastructure investments in port facilities worldwide, reflecting its crucial role in supporting international commerce and supply chains.

The demand for effective cargo handling operations and the increase in global trade are driving the market for port equipment. The need for sophisticated port machinery like automated guided vehicles (AGVs), straddle carriers, and container cranes is rising as ports around the world work to handle bigger ships and boost throughput. Leading companies in the industry are concentrating on innovation to create more dependable and ecologically friendly solutions, such as automation and electrification technologies.

To improve operational efficiency and safety, the market is also seeing a shift toward digitization and the integration of smart technology. Using IoT (Internet of Things) sensors and data analytics to improve equipment performance and expedite logistics is part of this. The implementation of remote monitoring and maintenance solutions has been expedited by the COVID-19 pandemic, hence propelling the growth of the market.

Market expansion is anticipated to be supported by government initiatives targeted at updating and developing port infrastructure, particularly in emerging economies. Upgrading machinery to handle more containers and expedite turnaround times is essential to staying competitive in the world of international trade.

In the future, market strategy and product development will probably be influenced by regulatory demands and sustainability concerns. Businesses that can provide solutions that lower energy usage, cut emissions, and boost operational effectiveness will be well-positioned to profit from the changing demands of the port equipment industry. With a focus on efficiency and sustainability, technological innovation, infrastructure investments, and an overall hopeful outlook, the port equipment market is expected to continue growing.

Port Equipment Market Trend Analysis

Port Equipment Market Growth Driver- Automation and Digitization Revolutionizing Port Operations

- In terms of efficiency and safety, the introduction of automation and digitalization in port operations is a revolutionary step. Traditional port logistics are being revolutionized by automated container handling equipment, such as robotic trucks and automated stacking cranes (ASCs). For example, ASCs can quickly and precisely load and remove containers from storage yards, greatly cutting down on turnaround times and maximizing space usage. In addition to increasing operational effectiveness, this automation reduces labor expenses and human error related to manual handling.

- Port automation also heavily relies on robotic vehicles, such as unmanned aerial vehicles (UAVs) and automated guided vehicles (AGVs). Containers are moved within terminals by AGVs, which expedites the movement of cargo and eases traffic. UAVs are used for aerial surveys and surveillance, giving data on port operations and infrastructure problems in real-time. Through optimal energy use and emissions reductions, these technologies allow ports to operate more flexibly and responsively to shifting needs, improving overall productivity while lowering the environmental effect.

- Additionally, the connectedness and intelligence of port operations are being improved by the incorporation of digital technologies. Large volumes of data are collected on container movements, equipment performance, and ambient variables by IoT sensors that are integrated into infrastructure and equipment. This data is analyzed by artificial intelligence (AI) and machine learning algorithms to enhance decision-making, forecast maintenance requirements, and optimize operations. Through improved resource management and lower carbon footprints, this data-driven strategy helps ports reach higher levels of efficiency, dependability, and safety while promoting sustainable practices.

- To put it simply, implementing automation and digitization in port operations is not only a necessary technological advancement but also a strategic necessity to effectively and sustainably satisfy the expanding demands of international trade. By adopting these innovations, ports can achieve competitive advantages in terms of cost-effectiveness, environmental stewardship, and operational agility. This will propel the port equipment market's evolution toward more intelligent, networked, and environmentally friendly solutions.

Port Equipment Market Expansion Opportunity- Sustainability Initiatives Reshaping Port Equipment Market

- Since ports all around the world are trying to lessen their environmental impact, sustainability has taken center stage in the port equipment market. Ports are forced to implement environmentally friendly solutions as a result of tightened environmental rules and increased scrutiny of carbon emissions. The move toward equipment powered by electricity or alternate fuels is one such development. Because they produce less pollutants and rely less on fossil fuels, electric-powered cranes and other machinery are becoming more and more common. In addition to improving the quality of the air in port regions, these developments also support the more general sustainability objectives set forth in international accords like the Paris Agreement and IMO (International Maritime Organization) regulations.

- Additionally, a deliberate effort is made to optimize energy use in port operations in addition to the introduction of electric power and other fuels. Producers are creating innovations that improve energy economy without sacrificing functionality. This covers advancements in energy storage technologies, crane regenerative braking, and smart grid integration for efficient power demand management. Ports can save a lot of money on operating expenses and show their support for sustainable practices by cutting back on energy use and emissions.

- Initiatives that allow ships to connect to the electrical grid while moored rather than operating their engines, such shore power facilities, are also gaining popularity. This lessens the pollutants that ships release into the air and helps port cities' local air quality. The port equipment market is undergoing a significant transformation, driven by sustainability-driven technologies that meet regulatory standards while also meeting the increasing aspirations of society and the environment for cleaner and greener operations in global trade logistics.

Port Equipment Market Segment Analysis:

Port Equipment Market Segmented based on Equipment, Type, Application, Demand, and Region.

By Equipment, Tug boats segment is expected to dominate the market during the forecast period

- A vital part of maritime operations, tug boats guarantee the secure and effective passage of ships through ports and harbors across the globe. Large container ships, tankers, and bulk carriers can all benefit from these sturdy boats' particular capabilities, which are built for docking, undocking, and confined space maneuvering. They can navigate and position vessels precisely thanks to their powerful engines and maneuverability, reducing the danger of marine accidents and guaranteeing smooth operations in crowded port situations.

- Tug boats are the industry leaders in ship handling because of their vital role in improving operational efficiency and port safety. Tug boats are a vital tool for ports and terminals to move a wide range of ships with different drafts and sizes, therefore each vessel's unique requirements must be catered to. Apart from their principal function in ship handling, tug boats also make a substantial contribution to emergency response capabilities. They offer crucial support in inclement weather, mechanical malfunctions, and other unanticipated difficulties at sea. As a result, MRO services—which are crucial for preserving these boats' operational readiness and safety compliance throughout their operating lifespan—maintain the need for tug boats.

- Furthermore, tug boats play an ever more important role as the volume of global trade increases and ports expand to accommodate larger vessels. As global sustainability objectives and regulatory requirements converge, modern tug boats are increasingly outfitted with cutting-edge technologies like dynamic positioning systems and environmentally friendly propulsion systems. This continuous development emphasizes how important tug boats are to the maritime sector, where they are still essential resources for guaranteeing safe and effective vessel operations in ports all over the world.

By By Application, Bulk Handling segment held the largest share in 2024

- Bulk handling systems are the largest application segment in the material handling equipment market, accounting for a significant share of the overall market. These systems are designed to efficiently move and transport large quantities of materials, such as grains, minerals, and other commodities, in a cost-effective and streamlined manner.

- The bulk handling segment encompasses a wide range of equipment, including conveyors, stackers, reclaimers, and ship loaders, among others. These systems are widely used in industries such as mining, agriculture, and logistics, where the efficient movement of large volumes of materials is crucial for operations. The growing demand for efficient and sustainable transportation of raw materials, coupled with the increasing need for automation and optimization in various industries, has been a key driver for the growth of the bulk handling segment.

Port Equipment Market Regional Insights:

Asia-Pacific is Expected to Dominate the Market Over the Forecast period

- Rapid urbanization and the ensuing spike in commercial activity are major factors driving the growth of the port equipment market in the Asia-Pacific region. Leading nations in the creation and growth of port infrastructure include China, India, and Singapore. Through the massive Belt and Road Initiative (BRI), China has played a key role in financing and building ports throughout Europe, Asia, and Africa, increasing trade and connectivity throughout the area. In contrast, India has been concentrating on modernizing its principal ports and creating new ones as part of the Sagarmala project in an effort to increase port capacity and efficiency for handling greater amounts of cargo.

- Furthermore, Singapore keeps up its status as a major marine hub by consistently investing in state-of-the-art port infrastructure. In these nations, implementing automated and smart port technologies is a crucial tactic for meeting the rising needs for container throughput. To increase productivity and streamline processes, automated container handling systems, blockchain-based logistics solutions, and AI-driven predictive analytics for cargo management are being used more and more. These developments lower overall logistics costs and boost competitiveness in international trade by improving port throughput capacities and ensuring faster vessel turnaround times.

- Moreover, the port equipment market is significantly shaped by the proactive government activities in the Asia-Pacific region. A favorable climate for innovation and investment is being created by policies that support sustainable practices, modernize port infrastructure, and enhance connectivity with inland logistics networks. Because of this, the area continues to draw large investments from both domestic and foreign companies, which speeds up the adoption of cutting-edge port machinery and technology. Because of this dynamic environment, Asia-Pacific is positioned to be a dominant force in the worldwide port equipment market and to maintain its leading position going forward.

Active Key Players in the Port Equipment Market

- Liebherr (Switzerland)

- TTS Group (Norway)

- Kalmar (Finland)

- Konecranes(Finland)

- Shanghai Zhenhua Heavy Industries (China)

- Lonking (China),

- Anhui Heli (China),

- CVS Ferrari (Italy),

- Hyster (the U.S.),

- Other Active Players

|

Global Port Equipment Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 19.07 Bn. |

|

Forecast Period 2025-32 CAGR: |

2.1 % |

Market Size in 2032: |

USD 22.52 Bn. |

|

Segments Covered: |

By Equipment |

|

|

|

By Type |

|

||

|

By Application |

|

||

|

By Demand |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Port Equipment Market by Equipment (2018-2032)

4.1 Port Equipment Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Tug boats

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Cranes

4.5 Mooring system

4.6 Ship loaders

4.7 Reach stackers

4.8 Automated guided vehicles

4.9 Forklift trucks

4.10 Container lift trucks

4.11 Terminal tractors

4.12 Straddle carriers

4.13 Others

Chapter 5: Port Equipment Market by Type (2018-2032)

5.1 Port Equipment Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Diesel

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Electric

5.5 Hybrid

Chapter 6: Port Equipment Market by Application (2018-2032)

6.1 Port Equipment Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Container Handling

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Bulk Handling

6.5 Ship Handling

6.6 Others

Chapter 7: Port Equipment Market by Demand (2018-2032)

7.1 Port Equipment Market Snapshot and Growth Engine

7.2 Market Overview

7.3 OEM

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 MRO

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Port Equipment Market Share by Manufacturer (2024)

8.1.3 Industry BCG Matrix

8.1.4 Heat Map Analysis

8.1.5 Mergers and Acquisitions

8.2 LIEBHERR (SWITZERLAND)

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Key Strategic Moves and Recent Developments

8.2.10 SWOT Analysis

8.3 TTS GROUP (NORWAY)

8.4 KALMAR (FINLAND)

8.5 KONECRANES(FINLAND)

8.6 SHANGHAI ZHENHUA HEAVY INDUSTRIES (CHINA)

8.7 LONKING (CHINA)

8.8 ANHUI HELI (CHINA) CVS FERRARI (ITALY) HYSTER (THE U.S.)

8.9 OTHER KEY PLAYERS

8.10

Chapter 9: Global Port Equipment Market By Region

9.1 Overview

9.2. North America Port Equipment Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecasted Market Size by Equipment

9.2.4.1 Tug boats

9.2.4.2 Cranes

9.2.4.3 Mooring system

9.2.4.4 Ship loaders

9.2.4.5 Reach stackers

9.2.4.6 Automated guided vehicles

9.2.4.7 Forklift trucks

9.2.4.8 Container lift trucks

9.2.4.9 Terminal tractors

9.2.4.10 Straddle carriers

9.2.4.11 Others

9.2.5 Historic and Forecasted Market Size by Type

9.2.5.1 Diesel

9.2.5.2 Electric

9.2.5.3 Hybrid

9.2.6 Historic and Forecasted Market Size by Application

9.2.6.1 Container Handling

9.2.6.2 Bulk Handling

9.2.6.3 Ship Handling

9.2.6.4 Others

9.2.7 Historic and Forecasted Market Size by Demand

9.2.7.1 OEM

9.2.7.2 MRO

9.2.8 Historic and Forecast Market Size by Country

9.2.8.1 US

9.2.8.2 Canada

9.2.8.3 Mexico

9.3. Eastern Europe Port Equipment Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecasted Market Size by Equipment

9.3.4.1 Tug boats

9.3.4.2 Cranes

9.3.4.3 Mooring system

9.3.4.4 Ship loaders

9.3.4.5 Reach stackers

9.3.4.6 Automated guided vehicles

9.3.4.7 Forklift trucks

9.3.4.8 Container lift trucks

9.3.4.9 Terminal tractors

9.3.4.10 Straddle carriers

9.3.4.11 Others

9.3.5 Historic and Forecasted Market Size by Type

9.3.5.1 Diesel

9.3.5.2 Electric

9.3.5.3 Hybrid

9.3.6 Historic and Forecasted Market Size by Application

9.3.6.1 Container Handling

9.3.6.2 Bulk Handling

9.3.6.3 Ship Handling

9.3.6.4 Others

9.3.7 Historic and Forecasted Market Size by Demand

9.3.7.1 OEM

9.3.7.2 MRO

9.3.8 Historic and Forecast Market Size by Country

9.3.8.1 Russia

9.3.8.2 Bulgaria

9.3.8.3 The Czech Republic

9.3.8.4 Hungary

9.3.8.5 Poland

9.3.8.6 Romania

9.3.8.7 Rest of Eastern Europe

9.4. Western Europe Port Equipment Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecasted Market Size by Equipment

9.4.4.1 Tug boats

9.4.4.2 Cranes

9.4.4.3 Mooring system

9.4.4.4 Ship loaders

9.4.4.5 Reach stackers

9.4.4.6 Automated guided vehicles

9.4.4.7 Forklift trucks

9.4.4.8 Container lift trucks

9.4.4.9 Terminal tractors

9.4.4.10 Straddle carriers

9.4.4.11 Others

9.4.5 Historic and Forecasted Market Size by Type

9.4.5.1 Diesel

9.4.5.2 Electric

9.4.5.3 Hybrid

9.4.6 Historic and Forecasted Market Size by Application

9.4.6.1 Container Handling

9.4.6.2 Bulk Handling

9.4.6.3 Ship Handling

9.4.6.4 Others

9.4.7 Historic and Forecasted Market Size by Demand

9.4.7.1 OEM

9.4.7.2 MRO

9.4.8 Historic and Forecast Market Size by Country

9.4.8.1 Germany

9.4.8.2 UK

9.4.8.3 France

9.4.8.4 The Netherlands

9.4.8.5 Italy

9.4.8.6 Spain

9.4.8.7 Rest of Western Europe

9.5. Asia Pacific Port Equipment Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecasted Market Size by Equipment

9.5.4.1 Tug boats

9.5.4.2 Cranes

9.5.4.3 Mooring system

9.5.4.4 Ship loaders

9.5.4.5 Reach stackers

9.5.4.6 Automated guided vehicles

9.5.4.7 Forklift trucks

9.5.4.8 Container lift trucks

9.5.4.9 Terminal tractors

9.5.4.10 Straddle carriers

9.5.4.11 Others

9.5.5 Historic and Forecasted Market Size by Type

9.5.5.1 Diesel

9.5.5.2 Electric

9.5.5.3 Hybrid

9.5.6 Historic and Forecasted Market Size by Application

9.5.6.1 Container Handling

9.5.6.2 Bulk Handling

9.5.6.3 Ship Handling

9.5.6.4 Others

9.5.7 Historic and Forecasted Market Size by Demand

9.5.7.1 OEM

9.5.7.2 MRO

9.5.8 Historic and Forecast Market Size by Country

9.5.8.1 China

9.5.8.2 India

9.5.8.3 Japan

9.5.8.4 South Korea

9.5.8.5 Malaysia

9.5.8.6 Thailand

9.5.8.7 Vietnam

9.5.8.8 The Philippines

9.5.8.9 Australia

9.5.8.10 New Zealand

9.5.8.11 Rest of APAC

9.6. Middle East & Africa Port Equipment Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecasted Market Size by Equipment

9.6.4.1 Tug boats

9.6.4.2 Cranes

9.6.4.3 Mooring system

9.6.4.4 Ship loaders

9.6.4.5 Reach stackers

9.6.4.6 Automated guided vehicles

9.6.4.7 Forklift trucks

9.6.4.8 Container lift trucks

9.6.4.9 Terminal tractors

9.6.4.10 Straddle carriers

9.6.4.11 Others

9.6.5 Historic and Forecasted Market Size by Type

9.6.5.1 Diesel

9.6.5.2 Electric

9.6.5.3 Hybrid

9.6.6 Historic and Forecasted Market Size by Application

9.6.6.1 Container Handling

9.6.6.2 Bulk Handling

9.6.6.3 Ship Handling

9.6.6.4 Others

9.6.7 Historic and Forecasted Market Size by Demand

9.6.7.1 OEM

9.6.7.2 MRO

9.6.8 Historic and Forecast Market Size by Country

9.6.8.1 Turkiye

9.6.8.2 Bahrain

9.6.8.3 Kuwait

9.6.8.4 Saudi Arabia

9.6.8.5 Qatar

9.6.8.6 UAE

9.6.8.7 Israel

9.6.8.8 South Africa

9.7. South America Port Equipment Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecasted Market Size by Equipment

9.7.4.1 Tug boats

9.7.4.2 Cranes

9.7.4.3 Mooring system

9.7.4.4 Ship loaders

9.7.4.5 Reach stackers

9.7.4.6 Automated guided vehicles

9.7.4.7 Forklift trucks

9.7.4.8 Container lift trucks

9.7.4.9 Terminal tractors

9.7.4.10 Straddle carriers

9.7.4.11 Others

9.7.5 Historic and Forecasted Market Size by Type

9.7.5.1 Diesel

9.7.5.2 Electric

9.7.5.3 Hybrid

9.7.6 Historic and Forecasted Market Size by Application

9.7.6.1 Container Handling

9.7.6.2 Bulk Handling

9.7.6.3 Ship Handling

9.7.6.4 Others

9.7.7 Historic and Forecasted Market Size by Demand

9.7.7.1 OEM

9.7.7.2 MRO

9.7.8 Historic and Forecast Market Size by Country

9.7.8.1 Brazil

9.7.8.2 Argentina

9.7.8.3 Rest of SA

Chapter 10 Analyst Viewpoint and Conclusion

10.1 Recommendations and Concluding Analysis

10.2 Potential Market Strategies

Chapter 11 Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

|

Global Port Equipment Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 19.07 Bn. |

|

Forecast Period 2025-32 CAGR: |

2.1 % |

Market Size in 2032: |

USD 22.52 Bn. |

|

Segments Covered: |

By Equipment |

|

|

|

By Type |

|

||

|

By Application |

|

||

|

By Demand |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||