Pharmaceutical Manufacturing Equipment Market Synopsis:

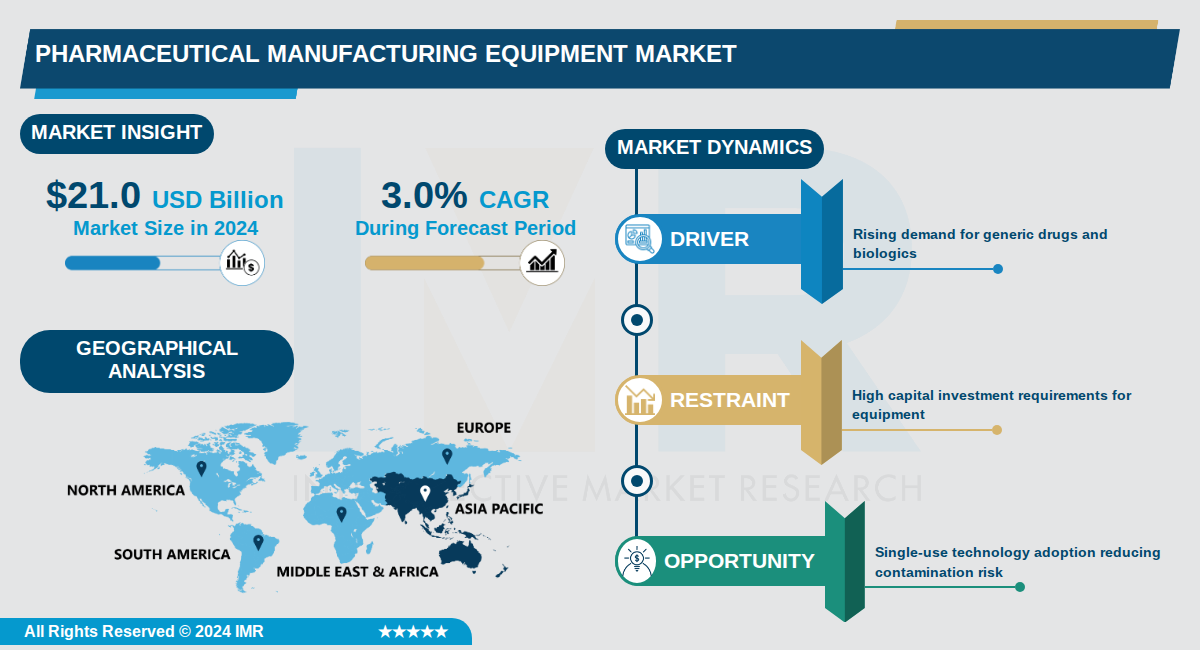

Pharmaceutical Manufacturing Equipment Market Size Was Valued at USD 21.0 Billion in 2024, and is Projected to Reach USD 30.0 Billion by 2035, Growing at a CAGR of 3.0% From 2024-2035.

The pharmaceutical manufacturing equipment market is valued at $21.0 billion in 2024 and is projected to reach $30.0 billion by 2035, growing at a CAGR of 3.0%.[user data]

This market encompasses processing, filling, packaging, and inspection equipment essential for drug formulation, biologics production, and sterile operations, with processing equipment holding the dominant share due to its role in mixing, granulation, and drying.

Key trends include a shift toward automation, continuous manufacturing, single-use systems, and AI integration, driven by demands for efficiency, regulatory compliance, and scalability in producing generics, biologics, vaccines, and complex formulations across global facilities.

Pharmaceutical Manufacturing Equipment Market Trend Analysis:

Rapid Adoption of Single-Use Technologies and Modular Manufacturing

- Single-use technologies (SUT) are reshaping pharmaceutical manufacturing by reducing contamination risk, lowering operational costs, and dramatically cutting validation timelines. Demand for biologics, which now account for 62% of pre-clinical and clinical manufacturing runs, is driving suppliers to replace traditional monolithic stainless-steel installations with modular, single-use assemblies that reduce validation timelines from 18 months to under 6 months.

- Flexible manufacturing systems are projected to reach USD 2.3 billion in market size by 2026, driven by plug-and-produce platforms, microfactories, and modular facilities. These systems enable smaller batch sizes, distributed production, and faster adaptation to new therapies, allowing pharmaceutical companies to respond more quickly to market demands for critical therapeutics and vaccines.

- The continuous manufacturing segment is experiencing the highest growth with a projected CAGR of 8.27% through 2032. This rapid adoption has been accelerated by post-pandemic digital transformation and the easy integration of continuous manufacturing technology into existing automated systems, supported by heavy investment in biopharmaceutical manufacturing facilities.

Integration of Automation, AI, and Industry 4.0 Technologies

- Automation and IoT integration are fundamentally transforming manufacturing processes by enabling real-time monitoring, predictive analytics, and enhanced quality control. COVID-19 accelerated digital transformation and increased demand for high-speed manufacturing equipment, with IoT enabling real-time monitoring that improves operational efficiency while automation reduces labor costs and enhances flexible manufacturing capabilities.

- Generative AI adoption in pharmaceutical manufacturing is expected to rise at a 43.12% CAGR, building on machine learning's current 38.78% market share. GSK invested USD 800 million to expand its Marietta, Pennsylvania facility with digital twins, robotics, predictive maintenance, and smart process optimization, demonstrating major pharma commitment to AI-enabled manufacturing.

- Industry 4.0 practices are becoming standard across regions, particularly in Europe where manufacturers prioritize digital integration into production environments. Future advances include quantum-AI hybrid models for improved in-silico predictions and digital twins evolving into 4-P models covering processes, facilities, products, and patient replicas, creating more sophisticated manufacturing ecosystems.

Stringent Regulatory Compliance Driving Equipment Modernization and Upgrades

- FDA and EMA regulatory guidelines require the use of state-of-the-art machinery for precision and validation, making regulatory compliance a primary driver of equipment investment. Stringent GMP-driven equipment upgrades are expected to contribute +0.7% to market growth in the short term, with a notable EU retrofit spike as manufacturers modernize production lines to meet evolving compliance standards.

- Rising demand for sterile injectables, vaccines, and high-potency medicines is increasing regulatory pressure on manufacturers to upgrade and retrofit existing equipment. Approximately 49% of pharmaceutical manufacturers are upgrading or retrofitting equipment according to PMMI 2026 data, with anti-counterfeiting technologies such as advanced sterilization and track-and-trace solutions gaining prominence to ensure regulatory adherence.

- CDMOs and contract manufacturers are expanding capacity and upgrading facilities to meet global standards, driven partly by outsourcing trends in low-cost regions. The mixing and blending equipment segment holds 22.79% market share in 2026 due to regulatory requirements for specialized, high-capacity equipment needed for miniaturized yet effective medicines for global exports.

Pharmaceutical Manufacturing Equipment Market Segment Analysis:

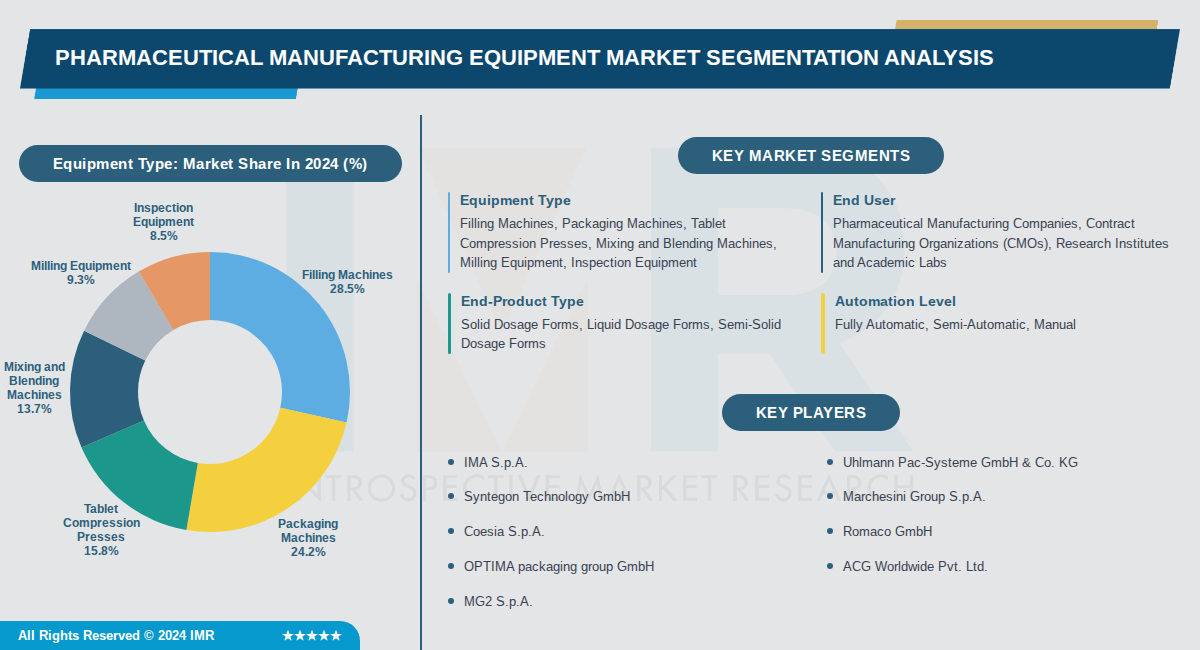

Pharmaceutical Manufacturing Equipment Market is Segmented on the basis of By Equipment Type, By End User, By End-Product Type

By Equipment Type, Filling Machines segment is expected to dominate the market during the forecast period

- Filling Machines dominate due to their critical role in precise drug delivery for both solid and liquid dosage forms, essential for high-volume production lines.

- Rising demand for biologics and injectables requires advanced aseptic filling systems, driving over 70% of new equipment investments in this category.

By End User, Pharmaceutical Manufacturing Companies segment is expected to dominate the market during the forecast period

- Pharmaceutical Manufacturing Companies lead as primary users investing heavily in scalable equipment for in-house production of generics and biologics.

- They account for the majority of equipment spending due to regulatory compliance needs and expansion of global manufacturing facilities.

By End-Product Type, Solid Dosage Forms segment is expected to dominate the market during the forecast period

- Solid Dosage Forms dominate because tablets and capsules represent the largest share of global pharmaceutical output, favored for stability and ease of distribution.

- Equipment for compression, coating, and encapsulation sees highest adoption as solid forms comprise over 60% of prescribed medications worldwide.

By Automation Level, Fully Automatic segment is expected to dominate the market during the forecast period

- Fully Automatic systems lead due to minimal human intervention, advanced robotics, and sensors ensuring compliance with stringent FDA and EMA regulations.

- Automation reduces contamination risks and boosts throughput by 40-50%, driving adoption in high-volume biologic and sterile manufacturing.

Pharmaceutical Manufacturing Equipment Market Regional Insights:

Asia Pacific is Expected to Dominate the Pharmaceutical Manufacturing Equipment Market

- Asia Pacific dominates the global market with a 42.1% market share in 2025 and is projected to grow at a CAGR of 6.9%, driven by expanding pharmaceutical production capacities in China, India, and Japan. China alone is estimated to capture USD 4.36 billion in market value in 2026, supported by increasing investments in modern science, pharmaceutical research, and the region's cost-effective manufacturing advantages.

- The region's dominance is strengthened by abundant resources, technological advancements, and the presence of large integrated equipment providers alongside emerging local manufacturers. Countries such as India, Japan, and South Korea are growing rapidly due to continuous disease mutation, the need for reliable pharmaceutical capacities, and government emphasis on minimizing dependencies on other countries for generic medicines.

- Asia Pacific's market value reached USD 9.97 billion in 2025 and is expected to reach USD 10.71 billion in 2026, significantly outpacing North America (USD 7.78 billion in 2026) and Europe (USD 4.15 billion in 2026). The region benefits from high demand for cost-effective packaging solutions, solid dosage equipment, and the adoption of advanced manufacturing systems across pharmaceutical production sites.

Active Key Players in the Pharmaceutical Manufacturing Equipment Market:

- IMA S.p.A. (Italy)

- Uhlmann Pac-Systeme GmbH & Co. KG (Germany)

- Syntegon Technology GmbH (Germany)

- Marchesini Group S.p.A. (Italy)

- Coesia S.p.A. (Italy)

- Romaco GmbH (Germany)

- OPTIMA packaging group GmbH (Germany)

- ACG Worldwide Pvt. Ltd. (India)

- MG2 S.p.A. (Italy)

- GEA Group Aktiengesellschaft (Germany)

- KORSCH AG (Germany)

- KIKUSUI SEISAKUSHO LTD (Japan)

- B&P Littleford (USA)

- Lee Industries (USA)

- IDEX Corporation (USA)

- Freund Corporation (Japan)

- M.A.R. S.p.A. (Italy)

- Danaher Corporation (USA)

- Sartorius Stedim Biotech S.A. (Germany)

- Other Active Players

|

Pharmaceutical Manufacturing Equipment Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 21.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

3.0 % |

Market Size in 2035: |

USD 30.0 Billion |

|

Segments Covered: |

By Equipment Type |

|

|

|

By End User |

|

||

|

By End-Product Type |

|

||

|

By Automation Level |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Pharmaceutical Manufacturing Equipment Market by Equipment Type (2017-2035)

4.1 Pharmaceutical Manufacturing Equipment Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Filling Machines

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Packaging Machines

4.5 Tablet Compression Presses

4.6 Mixing and Blending Machines

4.7 Milling Equipment

4.8 Inspection Equipment

Chapter 5: Pharmaceutical Manufacturing Equipment Market by End User (2017-2035)

5.1 Pharmaceutical Manufacturing Equipment Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Pharmaceutical Manufacturing Companies

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Contract Manufacturing Organizations (CMOs)

5.5 Research Institutes and Academic Labs

Chapter 6: Pharmaceutical Manufacturing Equipment Market by End-Product Type (2017-2035)

6.1 Pharmaceutical Manufacturing Equipment Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Solid Dosage Forms

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Liquid Dosage Forms

6.5 Semi-Solid Dosage Forms

Chapter 7: Pharmaceutical Manufacturing Equipment Market by Automation Level (2017-2035)

7.1 Pharmaceutical Manufacturing Equipment Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Fully Automatic

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Semi-Automatic

7.5 Manual

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Pharmaceutical Manufacturing Equipment Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 IMA S.P.A.

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 UHLMANN PAC-SYSTEME GMBH & CO. KG

8.4 SYNTEGON TECHNOLOGY GMBH

8.5 MARCHESINI GROUP S.P.A.

8.6 COESIA S.P.A.

8.7 ROMACO GMBH

8.8 OPTIMA PACKAGING GROUP GMBH

8.9 ACG WORLDWIDE PVT. LTD.

8.10 MG2 S.P.A.

8.11 GEA GROUP AKTIENGESELLSCHAFT

8.12 KORSCH AG

8.13 KIKUSUI SEISAKUSHO LTD

8.14 B&P LITTLEFORD

8.15 LEE INDUSTRIES

8.16 IDEX CORPORATION

8.17 FREUND CORPORATION

8.18 M.A.R. S.P.A.

8.19 DANAHER CORPORATION

8.20 SARTORIUS STEDIM BIOTECH S.A.

Chapter 9: Global Pharmaceutical Manufacturing Equipment Market By Region

9.1 Overview

9.2. North America Pharmaceutical Manufacturing Equipment Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Pharmaceutical Manufacturing Equipment Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Pharmaceutical Manufacturing Equipment Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Pharmaceutical Manufacturing Equipment Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Pharmaceutical Manufacturing Equipment Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Pharmaceutical Manufacturing Equipment Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Pharmaceutical Manufacturing Equipment Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 21.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

3.0 % |

Market Size in 2035: |

USD 30.0 Billion |

|

Segments Covered: |

By Equipment Type |

|

|

|

By End User |

|

||

|

By End-Product Type |

|

||

|

By Automation Level |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||