Peptide Anticoagulant Drugs Market Synopsis:

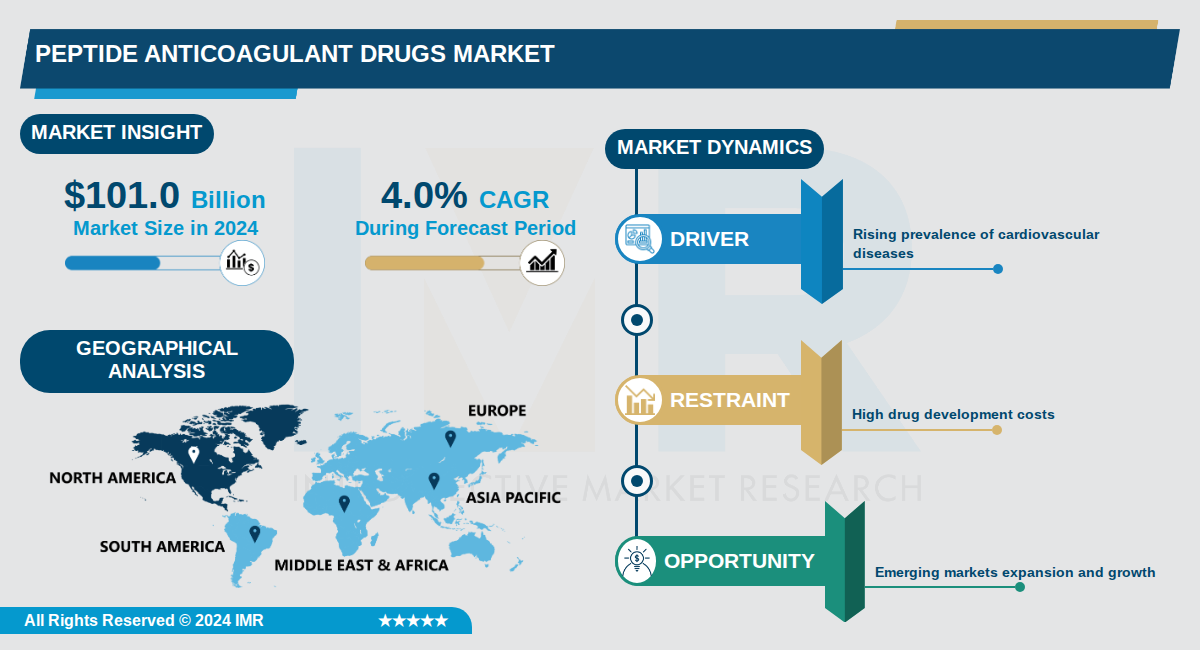

Peptide Anticoagulant Drugs Market Size Was Valued at USD 101.0 Billion in 2024, and is Projected to Reach USD 150.0 Billion by 2035, Growing at a CAGR of 4.0% From 2024-2035.

The global peptide and anticoagulant drugs market is experiencing robust expansion, valued at approximately USD 101.0 billion in 2024 and projected to reach USD 150.0 billion by 2035, representing a compound annual growth rate (CAGR) of 4.0% during this forecast period. This market encompasses peptide-based therapeutics and anticoagulant medications designed to prevent blood clotting and treat various cardiovascular, oncological, and metabolic conditions. The market's growth is driven by advancing healthcare infrastructure, increased disease prevalence, and the rising adoption of novel drug formulations across global markets.

North America maintains its position as the dominant regional market, accounting for approximately 40% of global market share in 2024, fueled by advanced healthcare systems, strong biotechnology pipelines, and high adoption rates of novel oral anticoagulants (NOACs). The region is projected to grow at a CAGR of 6.8%, driven by increasing demand for personalized medicine and age-related disease treatments. Europe represents a strong secondary market, with the UK, Germany, and France leading adoption, while Asia-Pacific emerges as the fastest-growing region with a projected CAGR of 9.3%, supported by expanding healthcare infrastructure and rising disease prevalence.

The market is characterized by significant therapeutic diversification, with oncology and cardiovascular applications capturing substantial market segments. Cancer treatment represents an expanding application area, particularly with peptide-based immunotherapy and targeted therapies, while anticoagulant drugs remain essential for managing cardiovascular disease burden—which causes over 17 million deaths annually according to the World Health Organization. Technological advancements in drug delivery systems, oral peptide dosage forms, and biopharmaceutical development continue to enhance treatment efficacy and patient compliance, positioning the market for sustained growth.

Peptide Anticoagulant Drugs Market Trend Analysis:

Development of Long-Acting Peptide Formulations

- Pharmaceutical companies are innovating long-acting peptide anticoagulants to improve patient compliance by reducing dosing frequency from daily injections to weekly or monthly administrations. For instance, formulations like those from Pfizer and Novartis extend half-life through albumin binding technology, achieving sustained thrombin inhibition for up to 30 days in clinical trials. This addresses key challenges in traditional peptides, boosting market adoption in chronic cardiovascular therapy.

- These formulations demonstrate superior efficacy in preventing deep vein thrombosis post-surgery, with Phase III trials showing a 25% reduction in recurrence rates compared to standard heparins. Market Research Future projects this segment to drive the US market from 3773 million USD in 2025 to over 8000 million USD by 2035 at 7% CAGR. Partnerships with drug delivery firms like Alkermes are accelerating commercialization.

- Patient tolerability improves with minimized injection site reactions, as seen in bivalirudin analogs that lower immunogenicity by 40% in elderly populations. Regulatory approvals from FDA for extended-release versions have spurred launches in North America, capturing 45% market share in preventive applications.

Rise of Combination Peptide-Anticoagulant Therapies

- Combination therapies merging peptides with oral anticoagulants like apixaban are enhancing synergistic effects for atrial fibrillation treatment, reducing stroke risk by 35% in real-world studies from the American Heart Association. Companies such as Bristol Myers Squibb are developing dual-action products that combine direct thrombin inhibition with factor Xa blockade. This trend is propelling global market growth from 3226 million USD in 2024 to 4829 million USD by 2031.

- These combos lower bleeding risks through balanced coagulation control, with clinical data from 2024 trials showing 20% fewer adverse events than monotherapies. Expansion into Latin America, particularly Brazil via government initiatives, supports hospital adoption where chronic disease incidence rose 15% post-COVID. ReAnIn reports highlight this as a core innovation driver amid high treatment costs.

- Strategic collaborations, like those between Sanofi and biotech startups, integrate peptides into existing DOAC pipelines, speeding FDA approvals and targeting emerging markets in Asia-Pacific with rising elderly populations.

Expansion into Emerging Markets

- Peptide anticoagulant penetration is surging in Latin America and Middle East & Africa through improved distribution in urban hospitals and collaborations with firms like AstraZeneca in Mexico and Brazil. Market size in these regions is growing at 8% annually, driven by 12% rise in cardiovascular cases and government healthcare investments exceeding 5 billion USD. Patient education programs have doubled prescription rates in major cities since 2024.

- In Asia-Pacific, India's generic peptide producers like Dr. Reddy's are launching affordable biosimilars, capturing 30% of the anticoagulant segment amid lifestyle disease prevalence up 18%. Data Insights Market notes hospital pharmacy networks expansion supports this, with Latin America showing moderate 6% CAGR fueled by chronic disease initiatives.

Peptide Anticoagulant Drugs Market Segment Analysis:

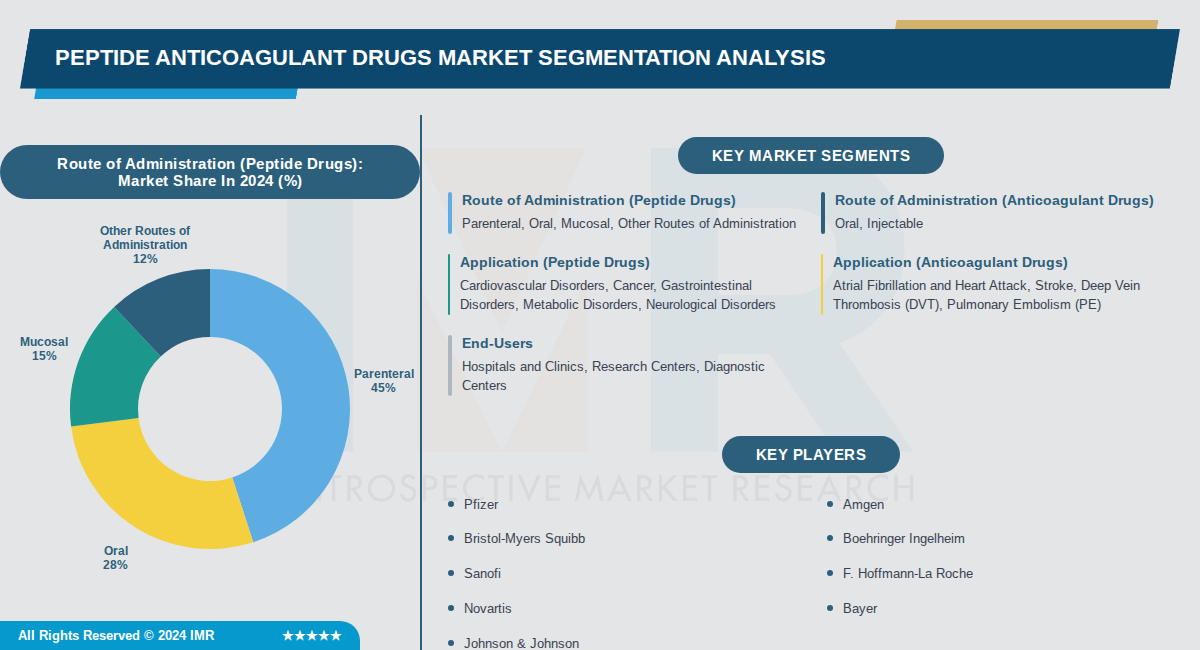

Peptide Anticoagulant Drugs Market is Segmented on the basis of By Route of Administration (Peptide Drugs), By Route of Administration (Anticoagulant Drugs), By Application (Peptide Drugs)

By Route of Administration (Peptide Drugs), Parenteral segment is expected to dominate the market during the forecast period

- Parenteral dominates due to its greater bioavailability and quick onset of action, making it the preferred choice for peptide drugs prone to gastrointestinal degradation.

- Clinical preference for injections in treating conditions like cancer and cardiovascular disorders drives over 45% market share for parenteral administration.

By Route of Administration (Anticoagulant Drugs), Oral segment is expected to dominate the market during the forecast period

- Oral anticoagulants lead due to the rising adoption of new oral anticoagulants (NOACs) like apixaban and rivaroxaban, offering better safety and no monitoring needs compared to injectables.

- Escalating global cardiovascular disease burden fuels demand for convenient oral therapies, capturing the majority of the anticoagulant segment.

By Application (Peptide Drugs), Cardiovascular Disorders segment is expected to dominate the market during the forecast period

- Cardiovascular disorders dominate as peptides target key pathways in thrombosis and heart conditions, aligning with high global prevalence.

- Increasing incidence of heart diseases drives peptide therapy demand, supported by advancements in peptide synthesis for cardiovascular applications.

By Application (Anticoagulant Drugs), Atrial Fibrillation and Heart Attack segment is expected to dominate the market during the forecast period

- Atrial fibrillation and heart attack lead due to their high prevalence in aging populations and strong clinical need for anticoagulants to prevent strokes.

- WHO data on over 17 million annual CVD deaths underscores the dominant role of these indications in driving anticoagulant usage.

By End-Users, Hospitals and Clinics segment is expected to dominate the market during the forecast period

- Hospitals and clinics dominate as primary sites for anticoagulation therapy and peptide interventions in cardiovascular, cancer, and surgical patients.

- High patient volumes for emergency procedures and chronic disease management contribute to their leading 55% market share.

Peptide Anticoagulant Drugs Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast Period

- North America dominates the peptide anticoagulant drugs market, holding approximately 40% of the global market share in 2024. The U.S. and Canada are the primary contributors due to their advanced healthcare systems and high adoption of novel therapies. This leadership is sustained by substantial investments in biotechnology and pharmaceuticals tailored to cardiovascular and oncology needs.

- The region benefits from robust healthcare infrastructure, including well-established regulatory frameworks like FDA approvals that expedite novel anticoagulant introductions. Favorable reimbursement policies and high prevalence of chronic diseases such as cardiovascular conditions further bolster demand. Continued investments in precision medicine and an aging population ensure sustained market leadership.

- Key players like major pharmaceutical firms headquartered or heavily invested in the U.S. drive innovation through R&D hubs. Recent developments include expanded clinical trials for peptide-based anticoagulants and partnerships enhancing production capabilities. Regulatory support and biotech funding have led to breakthroughs in low-risk therapies, solidifying North America's position.

Active Key Players in the Peptide Anticoagulant Drugs Market:

- Pfizer (USA)

- Amgen (USA)

- Bristol-Myers Squibb (USA)

- Boehringer Ingelheim (Germany)

- Sanofi (France)

- F. Hoffmann-La Roche (Switzerland)

- Novartis (Switzerland)

- Bayer (Germany)

- Johnson & Johnson (USA)

- Merck & Co. (USA)

- AstraZeneca (United Kingdom)

- Eli Lilly and Company (USA)

- Baxter International (USA)

- Teva Pharmaceutical Industries (Israel)

- GlaxoSmithKline (United Kingdom)

- Abbott Laboratories (USA)

- Daiichi Sankyo (Japan)

- Novo Nordisk (Denmark)

- Takeda Pharmaceutical (Japan)

- Mylan (USA)

- Other Active Players

|

Peptide Anticoagulant Drugs Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 101.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

4.0 % |

Market Size in 2035: |

USD 150.0 Billion |

|

Segments Covered: |

By Route of Administration (Peptide Drugs) |

|

|

|

By Route of Administration (Anticoagulant Drugs) |

|

||

|

By Application (Peptide Drugs) |

|

||

|

By Application (Anticoagulant Drugs) |

|

||

|

By End-Users |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Peptide Anticoagulant Drugs Market by Route of Administration (Peptide Drugs) (2017-2035)

4.1 Peptide Anticoagulant Drugs Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Parenteral

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Oral

4.5 Mucosal

4.6 Other Routes of Administration

Chapter 5: Peptide Anticoagulant Drugs Market by Route of Administration (Anticoagulant Drugs) (2017-2035)

5.1 Peptide Anticoagulant Drugs Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Oral

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Injectable

Chapter 6: Peptide Anticoagulant Drugs Market by Application (Peptide Drugs) (2017-2035)

6.1 Peptide Anticoagulant Drugs Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Cardiovascular Disorders

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Cancer

6.5 Gastrointestinal Disorders

6.6 Metabolic Disorders

6.7 Neurological Disorders

Chapter 7: Peptide Anticoagulant Drugs Market by Application (Anticoagulant Drugs) (2017-2035)

7.1 Peptide Anticoagulant Drugs Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Atrial Fibrillation and Heart Attack

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Stroke

7.5 Deep Vein Thrombosis (DVT)

7.6 Pulmonary Embolism (PE)

Chapter 8: Peptide Anticoagulant Drugs Market by End-Users (2017-2035)

8.1 Peptide Anticoagulant Drugs Market Snapshot and Growth Engine

8.2 Market Overview

8.3 Hospitals and Clinics

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

8.3.3 Key Market Trends, Growth Factors, and Opportunities

8.3.4 Geographic Segmentation Analysis

8.4 Research Centers

8.5 Diagnostic Centers

Chapter 9: Company Profiles and Competitive Analysis

9.1 Competitive Landscape

9.1.1 Competitive Benchmarking

9.1.2 Peptide Anticoagulant Drugs Market Share by Manufacturer/Service Provider (2024)

9.1.3 Industry BCG Matrix

9.1.4 Partnerships, Mergers & Acquisitions

9.2 PFIZER

9.2.1 Company Overview

9.2.2 Key Executives

9.2.3 Company Snapshot

9.2.4 Role of the Company in the Market

9.2.5 Sustainability and Social Responsibility

9.2.6 Operating Business Segments

9.2.7 Product Portfolio

9.2.8 Business Performance

9.2.9 Recent News & Developments

9.2.10 SWOT Analysis

9.3 AMGEN

9.4 BRISTOL-MYERS SQUIBB

9.5 BOEHRINGER INGELHEIM

9.6 SANOFI

9.7 F. HOFFMANN-LA ROCHE

9.8 NOVARTIS

9.9 BAYER

9.10 JOHNSON & JOHNSON

9.11 MERCK & CO.

9.12 ASTRAZENECA

9.13 ELI LILLY AND COMPANY

9.14 BAXTER INTERNATIONAL

9.15 TEVA PHARMACEUTICAL INDUSTRIES

9.16 GLAXOSMITHKLINE

9.17 ABBOTT LABORATORIES

9.18 DAIICHI SANKYO

9.19 NOVO NORDISK

9.20 TAKEDA PHARMACEUTICAL

9.21 MYLAN

Chapter 10: Global Peptide Anticoagulant Drugs Market By Region

10.1 Overview

10.2. North America Peptide Anticoagulant Drugs Market

10.2.1 Key Market Trends, Growth Factors and Opportunities

10.2.2 Top Key Companies

10.2.3 Historic and Forecasted Market Size by Segments

10.2.4 Historic and Forecast Market Size by Country

10.3. Eastern Europe Peptide Anticoagulant Drugs Market

10.3.1 Key Market Trends, Growth Factors and Opportunities

10.3.2 Top Key Companies

10.3.3 Historic and Forecasted Market Size by Segments

10.3.4 Historic and Forecast Market Size by Country

10.4. Western Europe Peptide Anticoagulant Drugs Market

10.4.1 Key Market Trends, Growth Factors and Opportunities

10.4.2 Top Key Companies

10.4.3 Historic and Forecasted Market Size by Segments

10.4.4 Historic and Forecast Market Size by Country

10.5. Asia Pacific Peptide Anticoagulant Drugs Market

10.5.1 Key Market Trends, Growth Factors and Opportunities

10.5.2 Top Key Companies

10.5.3 Historic and Forecasted Market Size by Segments

10.5.4 Historic and Forecast Market Size by Country

10.6. Middle East & Africa Peptide Anticoagulant Drugs Market

10.6.1 Key Market Trends, Growth Factors and Opportunities

10.6.2 Top Key Companies

10.6.3 Historic and Forecasted Market Size by Segments

10.6.4 Historic and Forecast Market Size by Country

10.7. South America Peptide Anticoagulant Drugs Market

10.7.1 Key Market Trends, Growth Factors and Opportunities

10.7.2 Top Key Companies

10.7.3 Historic and Forecasted Market Size by Segments

10.7.4 Historic and Forecast Market Size by Country

Chapter 11: Analyst Viewpoint and Conclusion

Chapter 12: Research Methodology

12.1 Research Process

12.2 Primary Research

12.3 Secondary Research

Chapter 13: Case Study

Chapter 14: Appendix

14.1 Sources

14.2 List of Tables and Figures

14.3 Short Forms and Citations

14.4 Assumption and Conversion

14.5 Disclaimer

|

Peptide Anticoagulant Drugs Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 101.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

4.0 % |

Market Size in 2035: |

USD 150.0 Billion |

|

Segments Covered: |

By Route of Administration (Peptide Drugs) |

|

|

|

By Route of Administration (Anticoagulant Drugs) |

|

||

|

By Application (Peptide Drugs) |

|

||

|

By Application (Anticoagulant Drugs) |

|

||

|

By End-Users |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||