North America Alloy Market Overview:

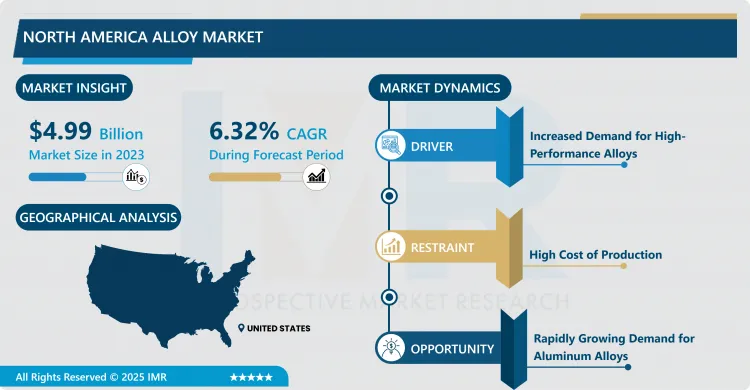

North America Alloy Market size was valued at USD 4.99 billion in 2023 and is projected to reach USD 8.66 billion by 2032, growing at a CAGR of 6.32% from 2024 to 2032.

The North America alloy market is a dynamic and critical segment of the metals industry, playing a role in various sectors such as aerospace, automotive, construction, and manufacturing. Alloys are materials composed of two or more metallic elements or a combination of metals and non-metals, engineered to possess specific properties and characteristics that are superior to individual metals. The market is characterized by its substantial growth and diversification over the years, driven by technological advancements and the increasing demand for high-performance materials.

The North America alloy market's growth is its extensive use in the automotive and aerospace industries. Alloys like aluminum alloys, stainless steel, and titanium alloys are essential components in the production of lightweight and durable automotive and aircraft parts, contributing to fuel efficiency and improved performance. The rising need for energy-efficient and eco-friendly transportation options has further spurred the demand for innovative alloy materials in this sector.

Alloys are also indispensable in the construction and infrastructure sectors. High-strength alloys are employed in structural components, ensuring the stability and safety of buildings, bridges, and other infrastructure projects. The market for corrosion-resistant alloys has also witnessed significant growth due to the need for long-lasting and low-maintenance structures in various environments.

North America Alloy Market Trend Analysis:

Increased Demand for High-Performance Alloys

- The increased demand for high-performance alloys in the Alloy Market can be attributed to several key factors driving growth and transformation in various industries. Firstly, advancements in technology have spurred the demand for materials that can withstand extreme conditions and deliver superior performance. High-performance alloys, known for their exceptional mechanical properties and resistance to corrosion and heat, have become crucial in applications ranging from aerospace and automotive to energy production and medical devices.

- The growing emphasis on sustainability and environmental concerns has prompted industries to seek more durable and longer-lasting materials. High-performance alloys not only extend the lifespan of components but also reduce the need for frequent replacements and repairs, ultimately minimizing waste and resource consumption. This eco-friendly aspect of high-performance alloys aligns with the push toward sustainable practices and circular economies.

- Aerospace and automotive sectors have witnessed a surge in demand for lightweight materials that can enhance fuel efficiency and reduce emissions. High-performance alloys offer a compelling solution, as they provide the desired strength-to-weight ratio, enabling manufacturers to create lighter yet robust components. As the world moves towards stricter emission regulations and greater energy efficiency, high-performance alloys are likely to play a pivotal role in achieving these goals.

Rapidly Growing Demand for Aluminum Alloys

- The automotive industry has been a major driver of increased demand for aluminum alloys. Aluminum is lightweight, corrosion-resistant, and offers an excellent strength-to-weight ratio, making it an ideal choice for manufacturers aiming to reduce the overall weight of vehicles. As automotive manufacturers prioritize fuel efficiency and emissions reduction, aluminum alloys have become a preferred material for components like body panels, engine blocks, and suspension parts. The shift towards electric vehicles (EVs) further amplifies this demand, as aluminum's lightweight properties contribute to extending the range of EVs.

- Aerospace industry has also witnessed a surge in the use of aluminum alloys. With air travel on the rise, aircraft manufacturers are constantly seeking materials that provide durability while minimizing weight. Aluminum alloys meet these criteria, making them integral in the construction of various aircraft components, such as fuselages, wings, and landing gear. Moreover, the aerospace industry's drive towards fuel efficiency has led to the development of more advanced aluminum alloys that offer enhanced performance characteristics, further boosting their demand.

- The construction and building sectors have contributed significantly to the increased demand for aluminum alloys. Aluminium’s corrosion resistance and strength make it an attractive choice for building facades, structural elements, and interior design applications. The construction industry's emphasis on sustainability has also driven the use of aluminum alloys, as they are highly recyclable, promoting environmentally friendly practices.

Segmentation Analysis of The North America Alloy Market:

Alloy Market is segmented into type of alloy, material type, vehicle type, and end-user industry.

By Material Type, the Aluminium Alloy segment is Anticipated to Dominate the Market Over the Forecast period.

- Aluminum Alloys are highly regarded for their lightweight yet durable characteristics. This unique blend of strength and low density makes them ideal for applications where weight reduction is critical, such as in the automotive and aerospace industries. The lightweight nature of aluminum alloys can lead to improved fuel efficiency in vehicles and increased payload capacity in aircraft, which are essential considerations in today's environmentally conscious and cost-sensitive markets.

- The recycling process requires significantly less energy compared to primary production, contributing to reduced greenhouse gas emissions. This sustainability aspect is becoming increasingly important as environmental concerns grow, and industries strive to meet stricter regulations and consumer demands for greener products. The recyclability of aluminum alloys further solidifies their dominance in the market as a sustainable choice.

- Aluminum alloys possess excellent thermal and electrical conductivity properties. These qualities make them valuable in various applications, such as electrical wiring, heat exchangers, and electronic components. The versatility of aluminum alloys across multiple industries, from automotive to electronics, ensures a steady demand, further strengthening their position as a dominant material type in the market.

By End-Use Industry, the Automotive segment held the largest share in 2023

- The automotive segment holds the largest share in the alloy market due to a confluence of factors primarily driven by the need for enhanced vehicle performance, fuel efficiency, and safety. Modern vehicles increasingly rely on alloys, especially aluminum alloys, to replace heavier traditional materials like steel. This shift is largely attributed to the demand for lightweighting, which improves fuel economy and reduces emissions, aligning with stricter environmental regulations and consumer preferences for greener vehicles.

- Alloys offer superior strength-to-weight ratios, enabling the production of more robust and durable vehicle components without adding excessive weight. This is crucial for structural components like chassis, body panels, and suspension systems, which directly impact vehicle safety and handling. The growing demand for high-performance vehicles and electric vehicles (EVs) further fuels the use of alloys, as these materials play a vital role in optimizing power-to-weight ratios and extending driving range.

- The alloys contribute to improved vehicle aesthetics, with alloy wheels being a popular choice among consumers for their visual appeal. The continuous advancements in alloy technology, coupled with the automotive industry's focus on innovation, ensure that alloys remain integral to vehicle manufacturing, solidifying the automotive segment's dominance in the alloy market.

Active Players in the North America Alloy Market:

- Timkensteel Corporation (United States)

- Haynes International (United States)

- Nucor Corporation (United States)

- Ulbrich Stainless Steels & Special Metals (United States)

- Special Metals Corporation (United States)

- AMETEK Specialty Metal Products (United States)

- Precision Castparts Corp (PCC) (United States)

- Allegheny Ludlum (United States)

- Tata Steel (India)

- AK Steel Holding Corporation (United States)

- Allegheny Technologies, Incorporated (ATI) (United States)

- Carpenter Technology Corporation (United States)

- JFE Steel Corporation (Japan)

- Sandvik AB (Sweden), and Other Active Players.

Key Industry Developments in the North America Alloy Market:

- In April 2024, the acquisition of United States Steel by Nippon Steel was approved by U.S. Steel’s stockholders at a special meeting of stockholders held on April 12, 2024 (local time). Nippon Steel expressed confidence that the acquisition would protect and grow U.S. Steel and bring significant benefits to its stakeholders, including customers, employees, union workers, suppliers, communities, and stockholders – as well as to the American steel industry and the United States as a whole. The vote yesterday represented a major step toward achieving this goal.

|

North America Alloy Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 4.99 Bn. |

|

Forecast Period 2024-32 CAGR: |

6.32% |

Market Size in 2032: |

USD 8.66 Bn. |

|

Segments Covered: |

By Type of Alloy |

|

|

|

By Material Type |

|

||

|

By Vehicle Type |

|

||

|

By End-Use Industry |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the Report: |

|

||

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: North America Alloy Market by Type of Alloy (2018-2032)

4.1 North America Alloy Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Ferrous Alloys

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Non-Ferrous Alloys

4.5 Superalloys

4.6 Noble Alloys

Chapter 5: North America Alloy Market by Material Type (2018-2032)

5.1 North America Alloy Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Aluminum Alloy

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Titanium Alloy

5.5 Magnesium Alloy

Chapter 6: North America Alloy Market by Vehicle Type (2018-2032)

6.1 North America Alloy Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Passenger Vehicles

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Commercial Vehicles

Chapter 7: North America Alloy Market by End-Use Industry (2018-2032)

7.1 North America Alloy Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Automotive

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Aerospace and Défense

7.5 Construction

7.6 Electronics

7.7 Oil and Gas

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 North America Alloy Market Share by Manufacturer (2024)

8.1.3 Industry BCG Matrix

8.1.4 Heat Map Analysis

8.1.5 Mergers and Acquisitions

8.2 TIMKENSTEEL CORPORATION (UNITED STATES)

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Operating Business Segments

8.2.5 Product Portfolio

8.2.6 Business Performance

8.2.7 Recent News & Development

8.2.8 SWOT Analysis

8.3 HAYNES INTERNATIONAL (UNITED STATES)

8.4 NUCOR CORPORATION (UNITED STATES)

8.5 ULBRICH STAINLESS STEELS & SPECIAL METALS (UNITED STATES)

8.6 SPECIAL METALS CORPORATION (UNITED STATES)

8.7 AMETEK SPECIALTY METAL PRODUCTS (UNITED STATES)

8.8 PRECISION CASTPARTS CORP (PCC) (UNITED STATES)

8.9 ALLEGHENY LUDLUM (UNITED STATES)

8.10 TATA STEEL (INDIA)

8.11 AK STEEL HOLDING CORPORATION (UNITED STATES)

8.12 ALLEGHENY TECHNOLOGIES

8.13 INCORPORATED (ATI) (UNITED STATES)

8.14 CARPENTER TECHNOLOGY CORPORATION (UNITED STATES)

8.15 JFE STEEL CORPORATION (JAPAN)

8.16 SANDVIK AB (SWEDEN)

8.17 AND

Chapter 9:North America Alloy Market Analysis, Insights and Forecast, 2016-2028

9.1 Market Overview

9.2 Key Market Trends, Growth Factors and Opportunities

9.3 Key Players

9.4 Historic and Forecasted Market Size by Type of Alloy

9.4.1 Ferrous Alloys

9.4.2 Non-Ferrous Alloys

9.4.3 Superalloys

9.4.4 Noble Alloys

9.5 Historic and Forecasted Market Size by Material Type

9.5.1 Aluminum Alloy

9.5.2 Titanium Alloy

9.5.3 Magnesium Alloy

9.6 Historic and Forecasted Market Size by Vehicle Type

9.6.1 Passenger Vehicles

9.6.2 Commercial Vehicles

9.7 Historic and Forecasted Market Size by End-Use Industry

9.7.1 Automotive

9.7.2 Aerospace and Défense

9.7.3 Construction

9.7.4 Electronics

9.7.5 Oil and Gas

9.8 Historic and Forecast Market Size by Country

9.8.1 U.S.

9.8.2 Canada

9.8.3 Mexico

Chapter 10 Analyst Viewpoint and Conclusion

10.1 Recommendations and Conclusion

Chapter 11 Our Thematic Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

|

North America Alloy Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 4.99 Bn. |

|

Forecast Period 2024-32 CAGR: |

6.32% |

Market Size in 2032: |

USD 8.66 Bn. |

|

Segments Covered: |

By Type of Alloy |

|

|

|

By Material Type |

|

||

|

By Vehicle Type |

|

||

|

By End-Use Industry |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the Report: |

|

||

Frequently Asked Questions :

The forecast period in the Alloy Market research report is 2024-2032.

Timkensteel Corporation (United States), Haynes International (United States), Nucor Corporation (United States), Ulbrich Stainless Steels & Special Metals (United States), Special Metals Corporation (United States), AMETEK Specialty Metal Products (United States), Precision Castparts Corp (PCC) (United States), Allegheny Ludlum (United States), Tata Steel (India), AK Steel Holding Corporation (United States), Allegheny Technologies, Incorporated (ATI) (United States), Carpenter Technology Corporation (United States), JFE Steel Corporation (Japan), Sandvik AB (Sweden), and Other Active Players

The Alloy Market is segmented into Type of Alloy, Material Type, Vehicle Type, End-Use Industry, and region. By Type of Alloy, the market is categorized into Ferrous Alloys, Non-Ferrous Alloys, Superalloys, and Noble Alloys. Material Type, the market is categorized into Aluminium Alloy, Titanium Alloy, and Magnesium Alloy. By Vehicle Type, the market is categorized into Passenger Vehicles and Commercial Vehicles. By End-Use Industry, the market is categorized into Automotive, Aerospace and Defense, Construction, Electronics, Oil and Gas. By region, it is analyzed across North America (U.S.; Canada; Mexico)

The North America alloy market is a dynamic and critical segment of the metals industry, playing a role in various sectors such as aerospace, automotive, construction, and manufacturing. Alloys are materials composed of two or more metallic elements or a combination of metals and non-metals, engineered to possess specific properties and characteristics that are superior to individual metals. This market is characterized by its substantial growth and diversification over the years, driven by technological advancements and the increasing demand for high-performance materials.

North America Alloy Market size was valued at USD 20.08 billion in 2023 and is projected to reach USD 36.3 billion by 2032, growing at a CAGR of 6.8% from 2024 to 2032.