Metal Forging Market Synopsis:

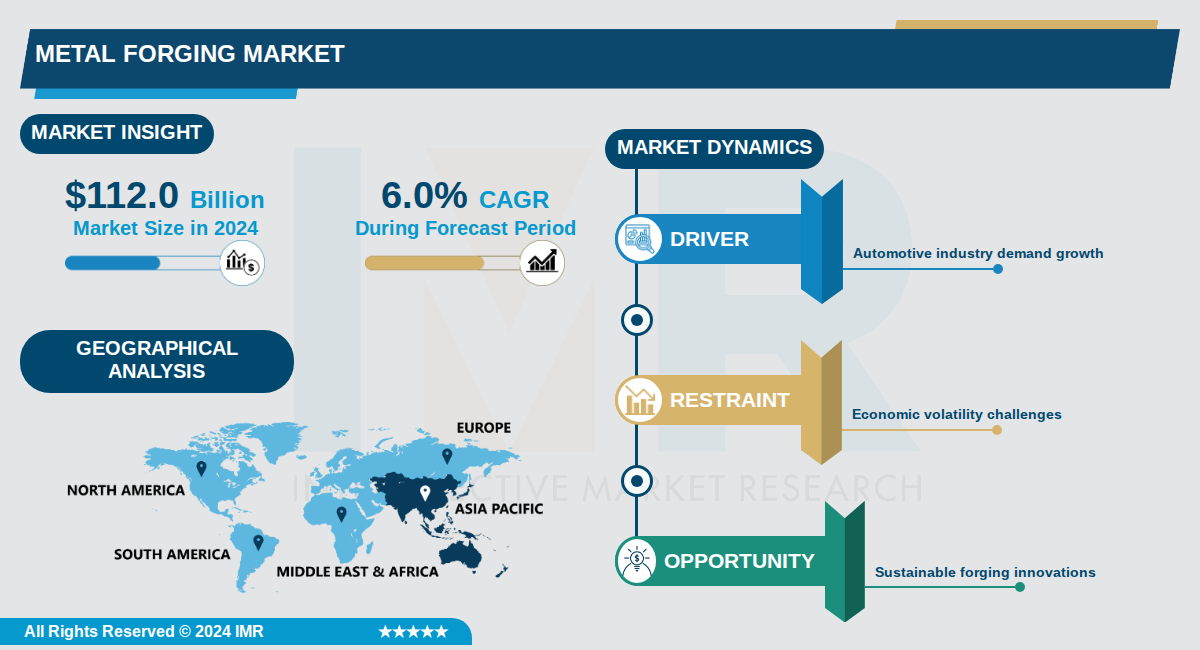

Metal Forging Market Size Was Valued at USD 112.0 Billion in 2024, and is Projected to Reach USD 203.0 Billion by 2035, Growing at a CAGR of 6.0% From 2024-2035.

The metal forging market, valued at $112.0 billion in 2024, is projected to reach $203.0 billion by 2035, growing at a compound annual growth rate (CAGR) of 6.0%. This expansion reflects strong demand across key industries, with variations in forecasts from sources estimating sizes between $94-102 billion in 2024 and growth rates of 7-9% through 2030-2035.

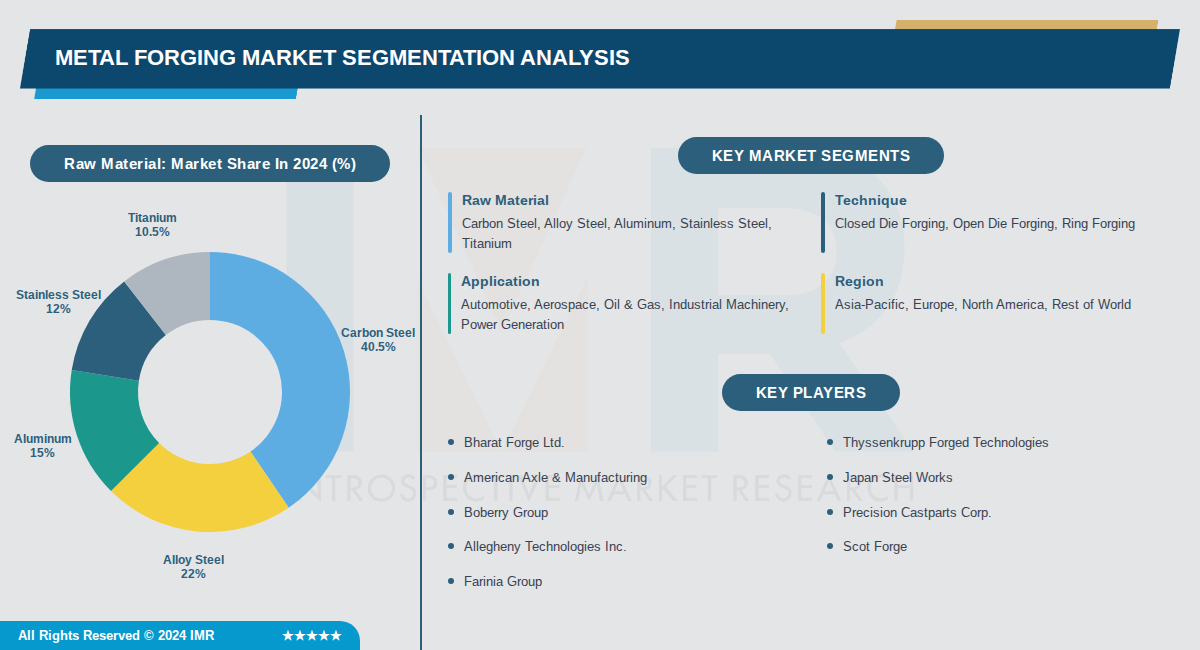

Dominant applications include automotive, aerospace & defense, and industrial machinery, where forged components such as crankshafts, landing gear, and engine parts provide superior strength, durability, and resistance to stress. Carbon steel leads in current revenue share, while stainless steel and aluminum are poised for significant growth due to lightweighting needs in electric vehicles and aircraft.

Asia-Pacific holds the largest market share, driven by infrastructure investments and automotive demand in countries like China and India, followed by growth in Europe and North America from advanced manufacturing and regulatory support for sustainability. Techniques like open die, closed die, and ring forging cater to diverse needs from large structural parts to precision components.

Metal Forging Market Trend Analysis:

Adoption of Automation and Industry 4.0 Technologies

- Manufacturers like voestalpine Group and CFS Forge are implementing advanced process controls and automation in hot forging services, achieving tolerances within ±0.2mm using computer-controlled hydraulic presses and intelligent heating systems. This has reduced energy consumption by 18-22% and increased production yields by 30% compared to traditional methods. Real-time monitoring systems track temperature, pressure, and quality parameters, with major players reporting 20-25% reductions in material waste after AI-driven optimization.

- In the U.S. aluminum forging market, robotic billet handling, automated press loading, and sensor-enabled furnaces with closed-loop feedback systems are addressing labor shortages and ensuring precise tolerance control for aerospace and EV components. Digital simulation software tests die geometries and temperature profiles pre-production, shortening development cycles and enabling near-net-shape parts with minimal machining. These technologies support AS9100 and NADCAP certifications critical for defense applications.

- Precision die forging and isothermal forging are being adopted by regional players for complex geometries in defense and energy sectors, improving material properties and efficiency throughout the forging cycle.

Development of Lightweight and High-Performance Alloys

- The stainless steel segment in metal forging is projected to grow at a CAGR of 9.2% from 2025 to 2034, driven by its superior corrosion resistance and use in demanding applications. Automotive manufacturers prefer lightweight aluminum forgings for EV battery housings and suspension systems, while aerospace specifies titanium forgings for jet engine components. Demand for superalloy forgings has grown 15% annually since 2021 for energy drilling equipment.

- High-performance alloys enable components to withstand extreme environments, with developments in high-strength steels and corrosion-resistant materials expanding applications across sectors. POSCO's new plant for specialized steel forgings and collaborations like Nippon Steel and JFE Steel focus on next-generation alloys for marine and industrial uses. These materials offer better strength-to-weight ratios compared to traditional carbon steel, which still dominates with over 40% market share due to cost-effectiveness.

- Carbon steel's durability supports its leadership in automotive, construction, and machinery, but advanced alloys are gaining traction for EVs and renewables where lightweighting reduces overall vehicle weight by up to 15%.

Growing Demand from Renewable Energy and EV Sectors

- Increasing adoption of renewable energy technologies drives demand for steel forgings in wind turbines and solar installations, requiring high-performance steel for extreme conditions. The shift toward electric vehicles creates opportunities for forged components in battery housings, suspension arms, and steering knuckles, with the automotive sector accounting for over 40% of hot forging demand. Rapid industrialization in Asia-Pacific, including plants by Bharat Forge and Frigate Engineering, supports this expansion.

- China Baowu has commissioned the world's largest forging press for marine components tied to offshore wind projects, while precision forging advancements produce complex parts with reduced waste for energy infrastructure. EV production growth is boosting aluminum closed-die forging, projected to grow the U.S. market from $1.41 billion in 2025 to $1.72 billion by 2032 at a 2.8% CAGR.

Metal Forging Market Segment Analysis:

Metal Forging Market is Segmented on the basis of By Raw Material, By Technique, By Application

By Raw Material, Carbon Steel segment is expected to dominate the market during the forecast period

- Carbon steel dominates due to its high strength-to-cost ratio, widespread availability, and suitability for broad forging applications in automotive and oil & gas industries.

- Lower material cost compared to stainless steel or titanium makes carbon steel preferred for high-volume production in tractors, aircraft, drilling equipment, and ships.

By Technique, Closed Die Forging segment is expected to dominate the market during the forecast period

- Closed die forging leads as it produces precise, high-strength components with superior metallurgical properties essential for automotive parts like crankshafts and gears.

- Its ability to handle complex shapes and tight tolerances drives adoption in high-demand sectors such as aerospace and defense where reliability is critical.

By Application, Automotive segment is expected to dominate the market during the forecast period

- Automotive dominates due to continuous demand for durable, high-strength components like axles, suspension parts, and engine elements amid rising vehicle production.

- Growth in electric vehicles and urbanization increases need for forged parts that withstand high torque, pressure, and temperature in harsh conditions.

By Region, Asia-Pacific segment is expected to dominate the market during the forecast period

- Asia-Pacific leads driven by rapid industrialization, cost-effective manufacturing, and strong automotive/aerospace hubs with skilled labor and government support.

- High exports of forged components and investments in advanced technologies accelerate consumption across infrastructure, energy, and transportation sectors.

Metal Forging Market Regional Insights:

Asia-Pacific Dominates the Global Metal Forging Market with 52% Market Share

- Asia-Pacific dominated the metal forging market with the largest market share of 52% in 2025 and is projected to lead through the forecast period to 2035. China and India are primary growth drivers, with China's market alone projected to reach USD 19.38 billion by 2026 and India's market reaching USD 4.06 billion by 2026. The region's dominance is underpinned by expansive steel industries, rapid industrialization, and massive manufacturing hubs.

- The region experiences rapid urbanization and infrastructure development including bridges, buildings, and transportation networks that require durable forged steel components. Asia-Pacific benefits from competitive manufacturing ecosystems, low labor costs, and special economic zones that attract forging investments. Japan and South Korea focus on advanced, high-precision forging for aerospace and automotive applications, while Southeast Asian nations like Thailand and Indonesia are emerging as key manufacturing hubs.

- China's emphasis on self-reliance in manufacturing has propelled advancements in forging technologies, while the automotive industry is a significant consumer generating 59% of market applications in 2025. Growing demand from the energy sector and infrastructure projects continues to propel market growth throughout the region. The region's competitive position is further strengthened by rising exports and ongoing digital transformation trends enhancing operational efficiencies.

Active Key Players in the Metal Forging Market:

- Bharat Forge Ltd. (India)

- Thyssenkrupp Forged Technologies (Germany)

- American Axle & Manufacturing (USA)

- Japan Steel Works (Japan)

- Boberry Group (China)

- Precision Castparts Corp. (USA)

- Allegheny Technologies Inc. (USA)

- Scot Forge (USA)

- Farinia Group (France)

- Schuler Group (Germany)

- Balu Forge Industries (India)

- Hilton Metal Forging (India)

- Siddhi Forge (India)

- Sun Forge (India)

- China First Heavy Industries (China)

- ELLWOOD Group, Inc. (USA)

- Bruck GmbH (Germany)

- Larsen & Toubro Limited (India)

- Other Active Players

|

Metal Forging Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 112.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

6.0 % |

Market Size in 2035: |

USD 203.0 Billion |

|

Segments Covered: |

By Raw Material |

|

|

|

By Technique |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Metal Forging Market by Raw Material (2017-2035)

4.1 Metal Forging Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Carbon Steel

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Alloy Steel

4.5 Aluminum

4.6 Stainless Steel

4.7 Titanium

Chapter 5: Metal Forging Market by Technique (2017-2035)

5.1 Metal Forging Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Closed Die Forging

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Open Die Forging

5.5 Ring Forging

Chapter 6: Metal Forging Market by Application (2017-2035)

6.1 Metal Forging Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Automotive

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Aerospace

6.5 Oil & Gas

6.6 Industrial Machinery

6.7 Power Generation

Chapter 7: Metal Forging Market by Region (2017-2035)

7.1 Metal Forging Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Asia-Pacific

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Europe

7.5 North America

7.6 Rest of World

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Metal Forging Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 BHARAT FORGE LTD.

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 THYSSENKRUPP FORGED TECHNOLOGIES

8.4 AMERICAN AXLE & MANUFACTURING

8.5 JAPAN STEEL WORKS

8.6 BOBERRY GROUP

8.7 PRECISION CASTPARTS CORP.

8.8 ALLEGHENY TECHNOLOGIES INC.

8.9 SCOT FORGE

8.10 FARINIA GROUP

8.11 SCHULER GROUP

8.12 BALU FORGE INDUSTRIES

8.13 HILTON METAL FORGING

8.14 SIDDHI FORGE

8.15 SUN FORGE

8.16 CHINA FIRST HEAVY INDUSTRIES

8.17 ELLWOOD GROUP

8.18 INC.

8.19 BRUCK GMBH

8.20 LARSEN & TOUBRO LIMITED

Chapter 9: Global Metal Forging Market By Region

9.1 Overview

9.2. North America Metal Forging Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Metal Forging Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Metal Forging Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Metal Forging Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Metal Forging Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Metal Forging Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Metal Forging Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 112.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

6.0 % |

Market Size in 2035: |

USD 203.0 Billion |

|

Segments Covered: |

By Raw Material |

|

|

|

By Technique |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||