Medical Grade Hypotube Market Synopsis:

Medical Grade Hypotube Market Size Was Valued at USD 3.0 Billion in 2024, and is Projected to Reach USD 5.0 Billion by 2035, Growing at a CAGR of 5.0% From 2024-2035.

The global Medical Grade Hypotube Market is valued at $3.0 billion in 2024 and is projected to reach $5.0 billion by 2035, reflecting a compound annual growth rate (CAGR) of 5.0%. Medical grade hypotubes are precision-engineered tubes essential for minimally invasive medical devices, particularly in cardiovascular, neurovascular, and urology applications. This growth aligns with broader trends in medical tubing markets, where demand for advanced, biocompatible components drives expansion.

North America currently dominates the market due to its advanced healthcare infrastructure, high adoption of minimally invasive surgeries, and robust research and development activities. Europe follows as the second-largest region, supported by high healthcare expenditures and innovation in medical technologies. The Asia Pacific region is poised for the fastest growth, fueled by improving healthcare systems, rising chronic disease prevalence, and increasing government investments.

Key end-users include hospitals, which lead due to high surgical volumes, and specialty clinics in cardiology, neurology, and urology. The market features a mix of established players like Freudenberg Medical and Heraeus, alongside smaller specialized manufacturers, with moderate mergers and acquisitions enhancing product portfolios and capabilities.

.png)

Medical Grade Hypotube Market Trend Analysis:

Rapid Expansion in Asia Pacific Markets

- The Asia Pacific region is projected to achieve the highest CAGR of around 8% for medical grade hypotubes through 2032, fueled by surging healthcare investments in countries like China, India, and Japan where government expenditures are modernizing hospital infrastructure. For instance, China's national healthcare spending reached over $1 trillion in 2024, enabling widespread adoption of advanced devices incorporating hypotubes from suppliers like Resonetics and Freudenberg Medical. This shift is creating new manufacturing hubs, with local firms partnering with global players such as Heraeus to meet rising demand for cardiovascular catheters.

- Hospitals in India, such as Apollo Hospitals and Fortis Healthcare, reported a 25% increase in minimally invasive procedures in 2025, directly boosting hypotube usage in guidewires and endoscopes supplied by Wytech and TE Connectivity. Japan's aging population, with over 36 million people aged 65+, has driven a 15% year-over-year growth in neurovascular device imports reliant on precision hypotubes. These developments are supported by policy reforms like India's Ayushman Bharat scheme, which reimburses advanced treatments and accelerates market penetration.

- Emerging partnerships, such as Cadence Inc.'s new facility in Vietnam announced in 2025, aim to cut production costs by 20% while complying with ISO standards, positioning Asia Pacific as a rival to North America's dominance.

Shift to Disposable Hypotube-Integrated Devices

- Healthcare providers are increasingly adopting disposable medical devices featuring medical grade hypotubes to slash hospital-acquired infection rates by up to 30%, with global usage rising 18% in 2024 per industry data. Companies like Amada Miyachi America and Advanced Medical Components (AMC) have launched single-use catheter kits with laser-cut hypotubes, reducing cross-contamination risks in high-volume settings like ambulatory surgical centers. This trend aligns with FDA guidelines emphasizing disposables in cardiovascular interventions, where hypotubes ensure flexibility and precision.

- In Europe, Germany's Fresenius Medical Care reported integrating disposable hypotube endoscopes in 40% of its procedures by mid-2025, cutting sterilization costs by 25% and improving turnaround times. U.S. hospitals following suit, with Mayo Clinic adopting Resonetics' disposable guidewires, have seen procedure volumes increase by 12% due to enhanced safety profiles. Market leaders like XL Precision Technologies project this segment to capture 35% of the $5.3 billion hypotube market by 2032.

Advancements in Precision Manufacturing Techniques

- Innovations like precision laser cutting and advanced metal alloy processing have enabled hypotube walls as thin as 0.001 inches with 50% greater strength, expanding applications in neurovascular stents from firms like Cambus Medical. Freudenberg Medical's 2025 rollout of electropolished Nitinol hypotubes improved corrosion resistance by 40%, meeting stringent biocompatibility standards for long-term implants. These techniques, adopted by Heraeus, have reduced production defects to under 0.5%, driving a 22% cost efficiency gain.

- TE Connectivity's investment in AI-optimized laser systems in 2024 produced hypotubes with variable stiffness profiles, ideal for Boston Scientific's next-gen guidewires used in 2 million annual procedures worldwide. Wytech's enhanced processing doubled fatigue life to over 1 million cycles, supporting minimally invasive robotics in surgeries performed at centers like Cleveland Clinic.

Medical Grade Hypotube Market Segment Analysis:

Medical Grade Hypotube Market is Segmented on the basis of By Type, By Application, By Material Grade

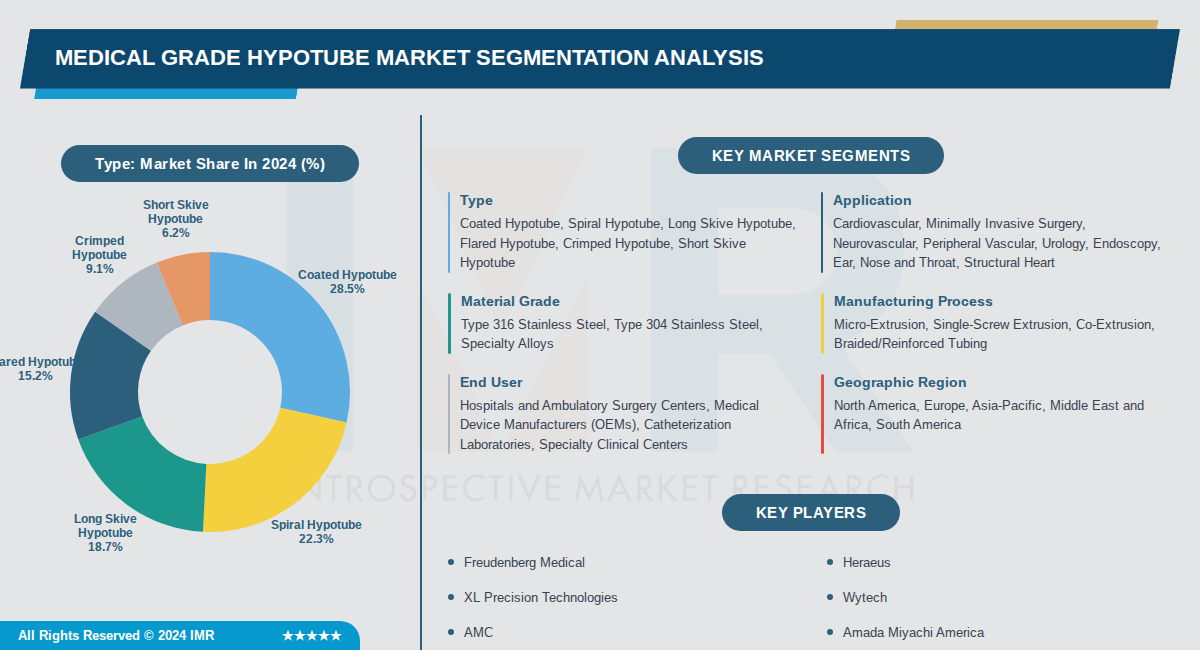

By Type, Coated Hypotube segment is expected to dominate the market during the forecast period

- Coated hypotubes dominate the market at 28.5% share because they provide enhanced lubricity, biocompatibility, and reduced friction during insertion, which are critical for minimally invasive cardiovascular procedures where smooth navigation through vessels is essential.

- Coated variants command premium pricing and are preferred by leading OEMs in interventional cardiology due to their proven clinical performance in reducing procedure time and improving patient outcomes in complex vascular interventions.

By Application, Cardiovascular segment is expected to dominate the market during the forecast period

- Cardiovascular applications dominate with 35.4% market share due to the exponential growth in percutaneous coronary interventions, angioplasty procedures, and catheter-based therapies globally, where hypotubes serve as critical structural components in guide wires and delivery systems.

- The cardiovascular segment benefits from aging demographics in developed markets, increasing prevalence of coronary artery disease, and continuous innovation in drug-eluting stent technology that requires precision hypotube designs for optimal device performance.

By Material Grade, Type 316 Stainless Steel segment is expected to dominate the market during the forecast period

- Type 316 stainless steel leads with 54.2% share because it offers superior corrosion resistance, higher molybdenum content, and enhanced biocompatibility, making it the preferred choice for long-term implantable devices and high-performance interventional tools that require exceptional durability.

- Medical-grade Type 316 hypotubes command premium pricing and are mandated for use in sensitive applications like neurovascular interventions where material purity, tensile strength, and compatibility with sterilization protocols directly impact clinical safety and device efficacy.

By Manufacturing Process, Micro-Extrusion segment is expected to dominate the market during the forecast period

- Micro-extrusion dominates with 42.7% share because it enables production of hypotubes with inner diameters below 0.1mm and exceptionally thin walls, which are essential for advanced neurovascular guidewires, pediatric interventions, and precision drug delivery systems that demand ultra-tight tolerances.

- Micro-extrusion technology commands the fastest growth rate at 11.02% CAGR through 2031 as medical device manufacturers increasingly prioritize minimally invasive solutions, and this process enables the creation of multilayer designs with lubricious inner cores and torque-stable outer structures.

By End User, Hospitals and Ambulatory Surgery Centers segment is expected to dominate the market during the forecast period

- Hospitals and ASCs dominate with 54.3% share because they conduct the majority of interventional procedures globally including coronary angiography, percutaneous interventions, and minimally invasive surgeries, creating sustained demand for high-quality hypotubes in their day-to-day operations.

- This segment's dominance is reinforced by the consolidation of medical procedures in hospital settings, regulatory requirements mandating quality components in clinical environments, and bulk procurement contracts with established hypotube suppliers that ensure supply continuity and clinical standards.

By Geographic Region, North America segment is expected to dominate the market during the forecast period

- North America leads with 41.0% market share due to its advanced healthcare infrastructure, high adoption rates of minimally invasive procedures, strong OEM partnerships, nearshoring manufacturing strategies, and robust reimbursement systems that support continued investment in precision medical devices.

- North America's dominance is sustained by leading U.S. and Canadian fabricators with established relationships with major interventional cardiology programs and medical device companies, combined with stringent regulatory compliance capabilities that meet FDA and ISO 13485 standards, creating barriers to entry for competitors.

Medical Grade Hypotube Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast Period

- North America dominates the medical grade hypotube market, primarily led by the United States, followed by Canada and Mexico. The region holds the largest market share due to high demand for advanced medical devices in minimally invasive procedures. This leadership is evident in current market analyses showing North America ahead of Europe and other regions.

- The region benefits from robust healthcare infrastructure, extensive research and development activities, and high healthcare expenditure. Stringent regulatory frameworks ensure quality and innovation in hypotube manufacturing. These factors create a favorable environment for adoption of medical grade hypotubes in surgical applications.

- A significant concentration of medical device manufacturers and key players operate in North America, driving production and innovation. Recent developments include ongoing investments in advanced materials for better biocompatibility and durability. This supports sustained market dominance through the forecast period.

Active Key Players in the Medical Grade Hypotube Market:

- Freudenberg Medical (USA)

- Heraeus (Germany)

- XL Precision Technologies (USA)

- Wytech (USA)

- AMC (USA)

- Amada Miyachi America (USA)

- Cambus Medical (Ireland)

- Cadence (USA)

- Resonetics (USA)

- Tegra Medical (USA)

- Creganna Medical Devices (Ireland)

- Duke Extrusion (USA)

- Colorado HypoTube (USA)

- Swastik Enterprise (India)

- Accu-Tube Corporation (USA)

- Advanced Medical Components (USA)

- Asahi Intecc Co., Ltd. (Japan)

- Boston Scientific Corporation (USA)

- Other Active Players

|

Medical Grade Hypotube Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 3.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

5.0 % |

Market Size in 2035: |

USD 5.0 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By Material Grade |

|

||

|

By Manufacturing Process |

|

||

|

By End User |

|

||

|

By Geographic Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Medical Grade Hypotube Market by Type (2017-2035)

4.1 Medical Grade Hypotube Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Coated Hypotube

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Spiral Hypotube

4.5 Long Skive Hypotube

4.6 Flared Hypotube

4.7 Crimped Hypotube

4.8 Short Skive Hypotube

Chapter 5: Medical Grade Hypotube Market by Application (2017-2035)

5.1 Medical Grade Hypotube Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Cardiovascular

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Minimally Invasive Surgery

5.5 Neurovascular

5.6 Peripheral Vascular

5.7 Urology

5.8 Endoscopy

5.9 Ear

5.10 Nose and Throat

5.11 Structural Heart

Chapter 6: Medical Grade Hypotube Market by Material Grade (2017-2035)

6.1 Medical Grade Hypotube Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Type 316 Stainless Steel

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Type 304 Stainless Steel

6.5 Specialty Alloys

Chapter 7: Medical Grade Hypotube Market by Manufacturing Process (2017-2035)

7.1 Medical Grade Hypotube Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Micro-Extrusion

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Single-Screw Extrusion

7.5 Co-Extrusion

7.6 Braided/Reinforced Tubing

Chapter 8: Medical Grade Hypotube Market by End User (2017-2035)

8.1 Medical Grade Hypotube Market Snapshot and Growth Engine

8.2 Market Overview

8.3 Hospitals and Ambulatory Surgery Centers

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

8.3.3 Key Market Trends, Growth Factors, and Opportunities

8.3.4 Geographic Segmentation Analysis

8.4 Medical Device Manufacturers (OEMs)

8.5 Catheterization Laboratories

8.6 Specialty Clinical Centers

Chapter 9: Medical Grade Hypotube Market by Geographic Region (2017-2035)

9.1 Medical Grade Hypotube Market Snapshot and Growth Engine

9.2 Market Overview

9.3 North America

9.3.1 Introduction and Market Overview

9.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

9.3.3 Key Market Trends, Growth Factors, and Opportunities

9.3.4 Geographic Segmentation Analysis

9.4 Europe

9.5 Asia-Pacific

9.6 Middle East and Africa

9.7 South America

Chapter 10: Company Profiles and Competitive Analysis

10.1 Competitive Landscape

10.1.1 Competitive Benchmarking

10.1.2 Medical Grade Hypotube Market Share by Manufacturer/Service Provider (2024)

10.1.3 Industry BCG Matrix

10.1.4 Partnerships, Mergers & Acquisitions

10.2 FREUDENBERG MEDICAL

10.2.1 Company Overview

10.2.2 Key Executives

10.2.3 Company Snapshot

10.2.4 Role of the Company in the Market

10.2.5 Sustainability and Social Responsibility

10.2.6 Operating Business Segments

10.2.7 Product Portfolio

10.2.8 Business Performance

10.2.9 Recent News & Developments

10.2.10 SWOT Analysis

10.3 HERAEUS

10.4 XL PRECISION TECHNOLOGIES

10.5 WYTECH

10.6 AMC

10.7 AMADA MIYACHI AMERICA

10.8 CAMBUS MEDICAL

10.9 CADENCE

10.10 RESONETICS

10.11 TEGRA MEDICAL

10.12 CREGANNA MEDICAL DEVICES

10.13 DUKE EXTRUSION

10.14 COLORADO HYPOTUBE

10.15 SWASTIK ENTERPRISE

10.16 ACCU-TUBE CORPORATION

10.17 ADVANCED MEDICAL COMPONENTS

10.18 ASAHI INTECC CO.

10.19 LTD.

10.20 BOSTON SCIENTIFIC CORPORATION

Chapter 11: Global Medical Grade Hypotube Market By Region

11.1 Overview

11.2. North America Medical Grade Hypotube Market

11.2.1 Key Market Trends, Growth Factors and Opportunities

11.2.2 Top Key Companies

11.2.3 Historic and Forecasted Market Size by Segments

11.2.4 Historic and Forecast Market Size by Country

11.3. Eastern Europe Medical Grade Hypotube Market

11.3.1 Key Market Trends, Growth Factors and Opportunities

11.3.2 Top Key Companies

11.3.3 Historic and Forecasted Market Size by Segments

11.3.4 Historic and Forecast Market Size by Country

11.4. Western Europe Medical Grade Hypotube Market

11.4.1 Key Market Trends, Growth Factors and Opportunities

11.4.2 Top Key Companies

11.4.3 Historic and Forecasted Market Size by Segments

11.4.4 Historic and Forecast Market Size by Country

11.5. Asia Pacific Medical Grade Hypotube Market

11.5.1 Key Market Trends, Growth Factors and Opportunities

11.5.2 Top Key Companies

11.5.3 Historic and Forecasted Market Size by Segments

11.5.4 Historic and Forecast Market Size by Country

11.6. Middle East & Africa Medical Grade Hypotube Market

11.6.1 Key Market Trends, Growth Factors and Opportunities

11.6.2 Top Key Companies

11.6.3 Historic and Forecasted Market Size by Segments

11.6.4 Historic and Forecast Market Size by Country

11.7. South America Medical Grade Hypotube Market

11.7.1 Key Market Trends, Growth Factors and Opportunities

11.7.2 Top Key Companies

11.7.3 Historic and Forecasted Market Size by Segments

11.7.4 Historic and Forecast Market Size by Country

Chapter 12: Analyst Viewpoint and Conclusion

Chapter 13: Research Methodology

13.1 Research Process

13.2 Primary Research

13.3 Secondary Research

Chapter 14: Case Study

Chapter 15: Appendix

15.1 Sources

15.2 List of Tables and Figures

15.3 Short Forms and Citations

15.4 Assumption and Conversion

15.5 Disclaimer

|

Medical Grade Hypotube Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 3.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

5.0 % |

Market Size in 2035: |

USD 5.0 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By Material Grade |

|

||

|

By Manufacturing Process |

|

||

|

By End User |

|

||

|

By Geographic Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||