Global Light Beer Market Overview

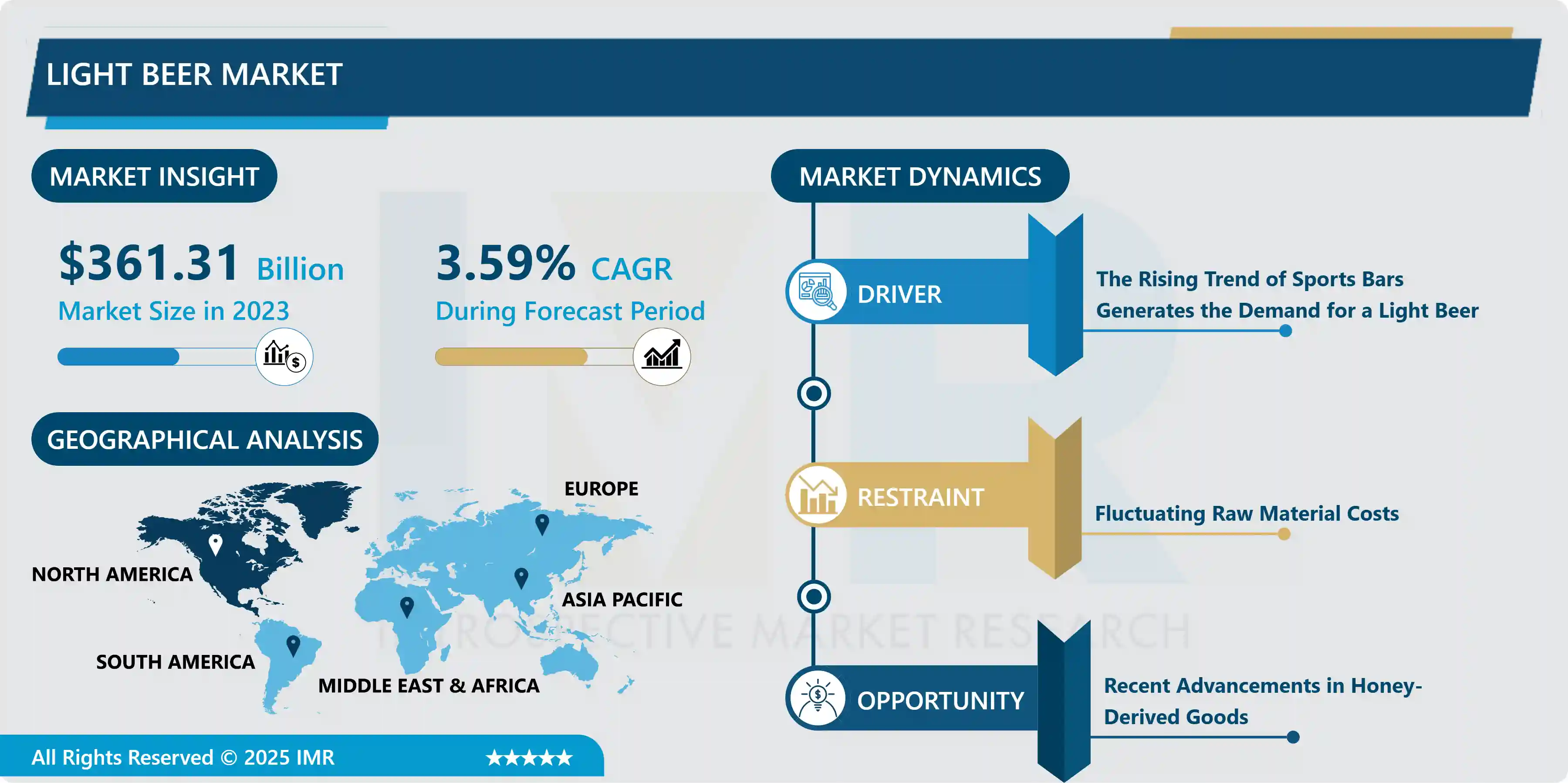

Global Light Beer Market was valued at USD 361.31 billion in 2023 and is expected to reach USD 496.29 billion by the year 2032, at a CAGR of 3.59%.

Light beer is a popular alcoholic beverage around the world containing alcohol content between 2-5%. It is a largely popular and most widely consumed alcoholic beverage with around the total volume of beer sold in 2020 was 170.4bn Litres. Among other types of beer, the general preference is light beer. Light beers can have the same flavor, crispness, creaminess, and body as a normal beer. The term 'light' in these brands merely refers to how few calories are included in a bottle or can of beer. A beer is only considered light if it has fewer calories than its normal counterpart. A 12-ounce bottle of Genesee Cream Ale, for example, may contain 150 calories whereas the light version contains 110 calories. Another distinction between light and normal beer is the amount of alcohol in each (ABV). A reduction in calories usually entails a fall in alcohol content. Many light beers, although not all, have a low alcohol level, with some reaching as low as 2.3 percent ABV. When you compare this to most conventional beers, which have an ABV of 4.1 percent to 5%, you can realize how much of a difference there is between regular beers and their lighter versions. Therefore, as a light alcoholic drink Light Beer Market is booming constantly throughout the years.

Market Dynamics and Factors For Light Beer

Drivers

The rising trend of sports bars generates the demand for a light beer.

- Sports crowd and people are spending a good length of time in the sports bar during live matches or general evening gatherings to discuss sports. Many of the specialty sports bars host special sports events which attract a mass crowd. Due to longer sports events, customers prefer light drinks such as light beer which is easy going with snacks for a longer duration. Sports-themed bars are popular alternatives for entrepreneurs looking to start a bar/restaurant company because they have a ready-made client base; sports enthusiasts enjoy congregating in drinking establishments with friends and watching their favorite teams on TV. Seasons of major sports leagues overlap and extend throughout the year, allowing a bar to remain popular throughout the year.

- Sharp rise in light alcoholic drinks among the young crowd.

- Beer use among those aged 18 to 25 years has increased significantly. The number of middle-aged and elderly males has stayed relatively unchanged, whilst the number of women has increased. According to the United Nations, the global young population is predicted to increase by 7% to 1.3 million by 2030, propelling the light beer industry forward. Due to increased social and professional meetings and financial freedom, the drinking trend among women is gaining favor across the world. This is a primary driver of the light beer industry.

Restraints

- Volatile costs influence the raw materials needed in beer production, limiting the expansion of the light beer industry. These drinks are made from crops that aren't being grown as efficiently as they should be owing to drought and other environmental difficulties, resulting in a supply-demand imbalance in the sector. This element reduces their output and raises product prices, impeding market expansion.

Opportunities

- Recent advancements in honey-derived goods look to be a feasible alternative for creating creative alcoholic drinks for customers, which will fuel the industry's future growth. Many inventive beverages, such as sherry-style wine, fruit-honey wine, and many varieties of meads, may be made from honey beer fermentation. These products come in a variety of tastes, depending on the honey's floral source, the yeast employed in the fermentation, and the additions utilized. Anheuser-Busch, for example, launched Natural Light Naturdays Strawberry Lemonade Beer in the United States to expand its market share. This strategy results in the creation of new unique items that meet client preferences and are offered as premium products. Beer has a big possibility to succeed in the light beer industry since it can be created using such techniques and because it is regarded as one of the finest qualities, sophisticated, and premium alcoholic beverages.

Challenges

- The rising popularity of Seltzers in alcoholic beverages presents a threat to the light beer market. Seltzer is essentially carbonated water or plain water with additional carbon dioxide bubbles. It varies from other carbonated beverages such as club soda and tonic water in that it lacks the odd-tasting minerals found in club soda and potassium sulfate in tonic water, as well as the high fructose corn syrup and quinine found in tonic water. Seltzer comes in various verity such as light, hard and flavored. The global seltzer market size is 8.95 billion USD in 2021. Therefore, tackling the growing popularity of seltzer and alternative to light beer is a major challenge to the light beer market.

Market Segmentation

- By Production, the Craft brewery segment is dominating the light beer market. Brewers are experimenting with new kinds like light lager and pale to capture customers' attention away from mainstream brands, and the craft lager category is seeing tremendous growth in the market. Craft lagers are becoming increasingly popular among consumers owing to their light and malty flavor. Brewers are moving their focus to products with longer shelf lives and lower-cost ingredients, which has resulted in a rise in craft larger output. Lagers made up 1764 entries in roughly 18 distinct varieties at the Great American Beer Festival (GABF), according to the Brewers Association, accounting for 15.8% of the alcoholic beverage. Therefore, the rising demand for light craft beer reflects on the growth of the light beer market globally.

- By Distribution Channel, Supermarket and hypermarket segment is dominating in the light beer market. Due to the convenience of having a wide selection of consumer items under one roof, abundant parking, and convenient operating hours. Furthermore, the popularity of hypermarkets in both established and emerging nations is boosted by urbanization, an increase in the working-class population, and competitive pricing.

- By Package, Glass Bottle is dominating the distribution channel segment in the beer market. Because of its low manufacturing cost, the glass bottle is the most widely used packaging material on the planet. The producers also feel that drinking beer from a glass bottle has a higher premium appeal than drinking beer from a metal can. Glass is dependable, long-lasting, and completely recyclable and reused. The continuous need for glass bottles, as well as their increased appeal in particular businesses and places across the world, is due to their fundamental properties. Consumers in industrialized countries such as the United States, the United Kingdom, Canada, and others are gravitating toward canned beer. Due to its favorable preservation features, such as an effective and handy container for retaining and limiting its exposure to light, canned beer is seeing an increase in demand in these nations.

Regional Analysis of Light Beer Market

- North America is dominating the light beer market. The fast proliferation of breweries in the United States has aided the spread of the beer market throughout the area. According to the Brewers Association, there were about 7,450 breweries in the United States in 2019 with a growth rate of 12. The majority of brewers in the United States have developed their distinct brews. In 2020, the brewing business in the United States will have sold around USD 100 billion in malt and drinks to American consumers through retail beer stores. Due to shifting taste preferences and different beer drinking experiences, the growing popularity of beer in the region is directly related to the increasing demand from millennials and the young working population. Consumer preferences are changing, and there is a rising desire for low-ABV beer which makes a driving factor for the light beer market in the North American region.

- Europe region is the second-highest market for a light beer. Beer is an essential component of culture, tradition, and nutrition in all European countries. The European Union is one of the world's most important beer-producing areas. According to The Brewers of Europe, 368,682 hectolitres of beer were consumed in 2019, made by 11,048 brewers across Europe. The European beer business is a relatively diversified sector in terms of structure. It consists mostly of small and medium-sized businesses, such as microbreweries and breweries that operate on a local, regional, or national scale, as well as significant European brewers that are global leaders in their professions The proliferation of new micro and small breweries in recent years is an indication of the industry's inventive potential. As some customers appear to convert to low-alcohol goods such as beer and low-alcohol and non-alcoholic versions in this category, the total alcohol content and hazardous use of alcohol in Europe has decreased. As a result, these consumer choices are expected to boost the European market's growth.

Key Major Player

- Anheuser-Busch InBev (Belgium)

- Heineken N.V. (Netherlands)

- Molson Coors Beverage Company (United States)

- Carlsberg Group (Denmark)

- Diageo plc (United Kingdom)

- Constellation Brands (United States)

- Asahi Group Holdings (Japan)

- SABMiller (South Africa)

- Grupo Modelo (Mexico)

- Kirin Holdings Company (Japan)

- Tsingtao Brewery Co., Ltd. (China)

- Ambev S.A. (Brazil)

- Boston Beer Company (United States)

- New Belgium Brewing Company (United States)

- Pabst Brewing Company (United States)

- Dogfish Head Brewery (United States)

- Stone Brewing (United States)

- Sierra Nevada Brewing Co. (United States)

- Deschutes Brewery (United States)

- Lagunitas Brewing Company (United States)

- BrewDog (United Kingdom)

- Harpoon Brewery (United States)

- Brooklyn Brewery (United States)

- Oskar Blues Brewery (United States )

- Victory Brewing Company (United States) and other major players.

Key Developments of Light Beer Market

- In February 2024, Flying Monkey, a crafted beer brand, was launched in Hyderabad. The brand promises the users a great experience and taste. It was launched in a grand event, and the event also had a tasting session. Many bloggers, vloggers, and popular social media influencers were invited to the event.

- In February 2024, Budweiser Brewing Group (BBG) introduced Corona Ligera, a lower-ABV version of the beloved Mexican lager. This new offering is exclusively accessible to the Tesco Group for six months, including availability for convenience through Booker starting on March 4th. With an ABV of 3.2%, it is crafted to be lighter-bodied, tailored to appeal to consumers such as the 18-34 age demographic, who have indicated a preference for premium, lower-alcohol beverages and moderation.

|

Global Light Beer Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 361.31 Bn. |

|

Forecast Period 2024-32 CAGR: |

3.59% |

Market Size in 2032: |

USD 496.29 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Distribution Channels |

|

||

|

By Package |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Light Beer Market by Type (2018-2032)

4.1 Light Beer Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Macro-Brewery

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Micro-Brewery

4.5 Craft Brewery

4.6 Others

Chapter 5: Light Beer Market by Distribution Channels (2018-2032)

5.1 Light Beer Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Hypermarkets & Supermarket

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 On-Trade

5.5 Specialty Stores

5.6 Convenience Store

5.7 Others

Chapter 6: Light Beer Market by Package (2018-2032)

6.1 Light Beer Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Keg

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Glass Bottle

6.5 Metal Can

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Light Beer Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 FARMVISIONAI (US)

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 AMHYDRO (US)

7.4 MIRAI CO. LTD (JAPAN)

7.5 OSRAM LICHT AG (GERMANY)

7.6 FREIGHT FARMS (US)

7.7 AEROFARMS LLC (US)

7.8 BRIGHT FARMS (US)

7.9 SKY GREENS (SINGAPORE)

7.10 SPREAD CO. LTD.; (JAPAN)

7.11 PLENTY UNLIMITED INC. (THE US)

7.12 FUTURE CROPS (NETHERLANDS)

7.13 VERTICAL FARM SYSTEMS (AUSTRALIA)

7.14 VALOYA (FINLAND)

7.15 EVERLIGHT ELECTRONICS CO. LTD. (TAIWAN)

7.16 HELIOSPECTRA AB (SWEDEN)

7.17 INTELLIGENT GROWTH SOLUTIONS (SCOTLAND)

7.18 GREEN SENSE FARMS (US)

7.19 AGRILUTION SYSTEMS GMBH (GERMANY)

7.20 VERTICAL FUTURE LTD (UK)

7.21 URBAN CROP SOLUTIONS (BELGIUM)

7.22 BOWERY FARMING (US)

7.23 AGRICOOL (FRANCE)

7.24 SWEGREEN (SWEDEN)

7.25 SANANBIO (US)

7.26 GROWPOD SOLUTIONS (US)

7.27 INFARM (GERMANY)

7.28 ALTIUS FARMS (US)

7.29 SIGNIFY HOLDING (NETHERLANDS)

7.30 4D BIOS INC (US)

7.31 GENERAL HYDROPONICS INC. (US)

Chapter 8: Global Light Beer Market By Region

8.1 Overview

8.2. North America Light Beer Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size by Type

8.2.4.1 Macro-Brewery

8.2.4.2 Micro-Brewery

8.2.4.3 Craft Brewery

8.2.4.4 Others

8.2.5 Historic and Forecasted Market Size by Distribution Channels

8.2.5.1 Hypermarkets & Supermarket

8.2.5.2 On-Trade

8.2.5.3 Specialty Stores

8.2.5.4 Convenience Store

8.2.5.5 Others

8.2.6 Historic and Forecasted Market Size by Package

8.2.6.1 Keg

8.2.6.2 Glass Bottle

8.2.6.3 Metal Can

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Light Beer Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size by Type

8.3.4.1 Macro-Brewery

8.3.4.2 Micro-Brewery

8.3.4.3 Craft Brewery

8.3.4.4 Others

8.3.5 Historic and Forecasted Market Size by Distribution Channels

8.3.5.1 Hypermarkets & Supermarket

8.3.5.2 On-Trade

8.3.5.3 Specialty Stores

8.3.5.4 Convenience Store

8.3.5.5 Others

8.3.6 Historic and Forecasted Market Size by Package

8.3.6.1 Keg

8.3.6.2 Glass Bottle

8.3.6.3 Metal Can

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Light Beer Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size by Type

8.4.4.1 Macro-Brewery

8.4.4.2 Micro-Brewery

8.4.4.3 Craft Brewery

8.4.4.4 Others

8.4.5 Historic and Forecasted Market Size by Distribution Channels

8.4.5.1 Hypermarkets & Supermarket

8.4.5.2 On-Trade

8.4.5.3 Specialty Stores

8.4.5.4 Convenience Store

8.4.5.5 Others

8.4.6 Historic and Forecasted Market Size by Package

8.4.6.1 Keg

8.4.6.2 Glass Bottle

8.4.6.3 Metal Can

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Light Beer Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size by Type

8.5.4.1 Macro-Brewery

8.5.4.2 Micro-Brewery

8.5.4.3 Craft Brewery

8.5.4.4 Others

8.5.5 Historic and Forecasted Market Size by Distribution Channels

8.5.5.1 Hypermarkets & Supermarket

8.5.5.2 On-Trade

8.5.5.3 Specialty Stores

8.5.5.4 Convenience Store

8.5.5.5 Others

8.5.6 Historic and Forecasted Market Size by Package

8.5.6.1 Keg

8.5.6.2 Glass Bottle

8.5.6.3 Metal Can

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Light Beer Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size by Type

8.6.4.1 Macro-Brewery

8.6.4.2 Micro-Brewery

8.6.4.3 Craft Brewery

8.6.4.4 Others

8.6.5 Historic and Forecasted Market Size by Distribution Channels

8.6.5.1 Hypermarkets & Supermarket

8.6.5.2 On-Trade

8.6.5.3 Specialty Stores

8.6.5.4 Convenience Store

8.6.5.5 Others

8.6.6 Historic and Forecasted Market Size by Package

8.6.6.1 Keg

8.6.6.2 Glass Bottle

8.6.6.3 Metal Can

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Light Beer Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size by Type

8.7.4.1 Macro-Brewery

8.7.4.2 Micro-Brewery

8.7.4.3 Craft Brewery

8.7.4.4 Others

8.7.5 Historic and Forecasted Market Size by Distribution Channels

8.7.5.1 Hypermarkets & Supermarket

8.7.5.2 On-Trade

8.7.5.3 Specialty Stores

8.7.5.4 Convenience Store

8.7.5.5 Others

8.7.6 Historic and Forecasted Market Size by Package

8.7.6.1 Keg

8.7.6.2 Glass Bottle

8.7.6.3 Metal Can

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Global Light Beer Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 361.31 Bn. |

|

Forecast Period 2024-32 CAGR: |

3.59% |

Market Size in 2032: |

USD 496.29 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Distribution Channels |

|

||

|

By Package |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||