IVD Antibody Raw Materials Market Synopsis:

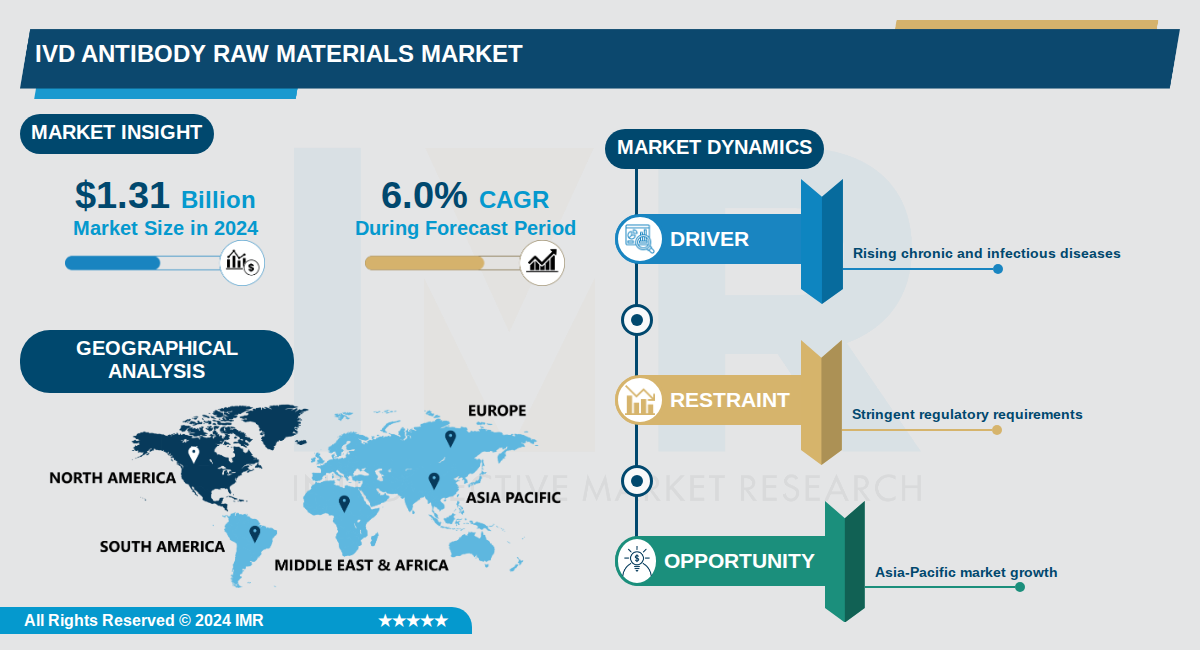

IVD Antibody Raw Materials Market Size Was Valued at USD 1.31 Billion in 2024, and is Projected to Reach USD 2.46 Billion by 2035, Growing at a CAGR of 6.0% From 2024-2035.

The IVD Antibody Raw Materials Market, a critical segment of the broader in vitro diagnostics (IVD) raw materials sector, was valued at $1.31 billion in 2024 and is projected to reach $2.46 billion by 2035, growing at a compound annual growth rate (CAGR) of 6.0%. This growth reflects the essential role of antibodies in manufacturing high-specificity diagnostic tests, including immunoassays and rapid tests for infectious diseases, cancer, and chronic conditions.

Antibodies dominate the IVD raw materials market due to their superior specificity and sensitivity, enabling detection of biomarkers at low concentrations (e.g., 5-10 pg/ml), which is vital for accurate early diagnosis. Key players such as Merck, Thermo Fisher Scientific, F. Hoffmann-La Roche, and Fapon Biotech are investing heavily in R&D and strategic acquisitions to innovate antibody production, particularly recombinant monoclonal antibodies.

The market benefits from broader IVD trends like the rise of point-of-care (POC) diagnostics, personalized medicine, and advancements in microfluidic technology, which demand high-quality antibody raw materials for efficient, miniaturized assays. Regional dynamics show Europe leading due to regulatory advancements like the IVDR and high demand for early diagnostics, while North America follows with advanced healthcare infrastructure.

IVD Antibody Raw Materials Market Trend Analysis:

Rise of Recombinant Antibodies and Novel Formats

- OEMs are heavily investing in recombinant protein engineering and monoclonal antibody production to boost specificity and stability in IVD kits, with companies like BD PharMingen and Abcam leading the charge by developing bispecific antibodies and antibody-drug conjugates that enhance diagnostic accuracy for cancer and infectious diseases.

- The IVD Antibody segment is projected to reach US$13.0 Billion by 2030 at a 3.8% CAGR, driven by these advanced formats which reduce batch-to-batch variability compared to polyclonal antibodies, enabling more reliable ELISA and lateral flow tests used in over 31.1% of the market's antibody applications.

- Abcam's recent launches of recombinant nanobodies have cut production costs by 20% while improving shelf-life to over 24 months, making them ideal for point-of-care diagnostics in remote settings.

Expansion of Multiplex and Point-of-Care Assays

- Rising adoption of multiplex assays for simultaneous detection of multiple analytes is fueling demand for custom coating and blocking reagents, with R&D Systems supplying materials for assays that detect up to 50 biomarkers in a single test for chronic disease panels.

- Point-of-care diagnostics growth, strengthened by home testing kits, requires high-quality antibodies and buffers; for instance, Cell Signaling Technology's reagents power rapid tests that deliver results in under 15 minutes, capturing 38.3% of demand from diagnostic laboratories.

- This trend supports a market expansion to over $9 billion by 2033 at 8% CAGR, as seen in North America's 34.8% share where POC testing for COVID-19 and flu has surged post-pandemic.

Integration of AI and Machine Learning in Antibody Diagnostics

- AI and ML integration is transforming IVD antibodies by optimizing assay design and predictive analytics, with companies like Biointron using deep learning on datasets from 14,500 COVID-19 patients to develop antibodies that predict disease outcomes with 95% accuracy.

- This enables personalized medicine applications, where highly specific antibodies paired with AI analyze genetic and protein data for tailored cancer diagnostics, addressing variability issues across suppliers noted in 25% of market challenges.

- Digital health platforms from Abcam integrate ML-driven antibody selection, reducing development time by 30% and supporting multiplex PCR assays that held the largest technology share in 2024.

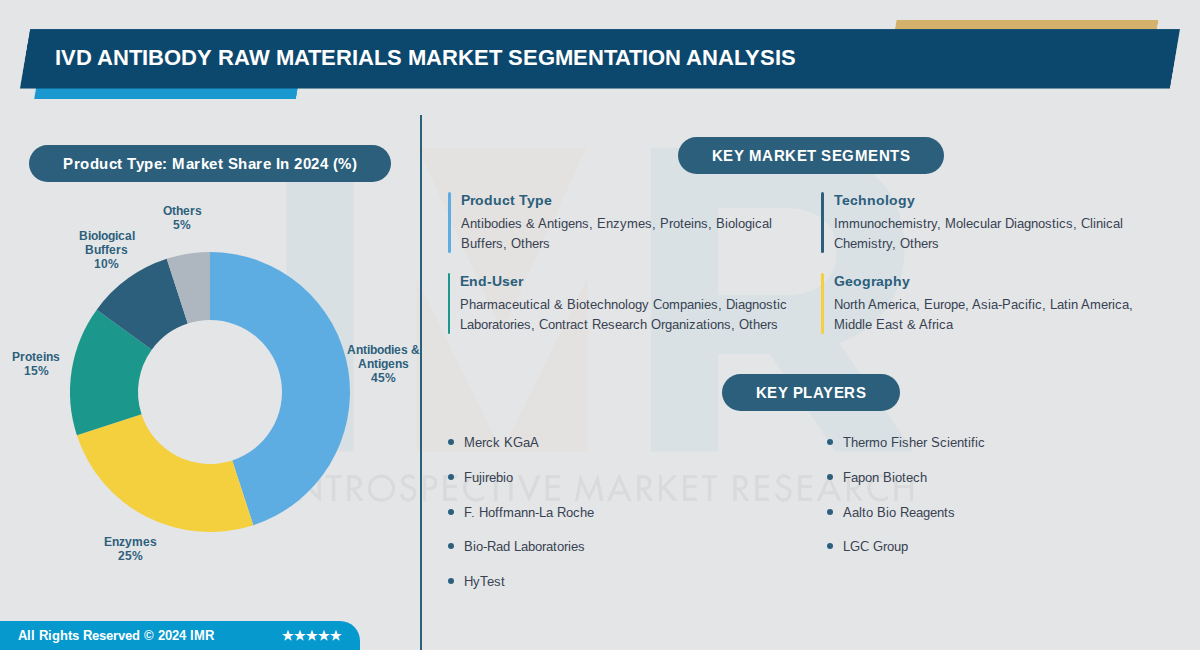

IVD Antibody Raw Materials Market Segment Analysis:

Ivd Antibody Raw Materials Market is Segmented on the basis of By Product Type, By Technology, By End-User

By Product Type, Antibodies & Antigens segment is expected to dominate the market during the forecast period

- Antibodies & antigens dominate due to their core role in immunochemistry and immunoassay-based IVD tests, which saw massive demand during COVID-19 for antigen and antibody detection.

- Rising prevalence of infectious and chronic diseases drives higher adoption of antibody-antigen tests, accounting for the majority of diagnostic reagent production.

By Technology, Immunochemistry segment is expected to dominate the market during the forecast period

- Immunochemistry leads as it relies heavily on high-specificity antibodies and antigens, essential for widespread immunoassay platforms in routine diagnostics.

- Advancements in antibody technologies and the expansion of point-of-care testing bolster immunochemistry's position over other technologies.

By End-User, Pharmaceutical & Biotechnology Companies segment is expected to dominate the market during the forecast period

- Pharma and biotech firms dominate through massive R&D investments in developing advanced IVD kits and reagents, requiring bulk high-quality antibody raw materials.

- Their focus on innovation in precision medicine and novel biomarkers sustains leadership in raw material consumption.

By Geography, North America segment is expected to dominate the market during the forecast period

- North America holds the lead with advanced healthcare infrastructure, high diagnostic testing volumes, and significant R&D funding in IVD technologies.

- Strong emphasis on genomics, molecular diagnostics, and early disease detection in the region amplifies demand for premium antibody raw materials.

IVD Antibody Raw Materials Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast Period

- North America dominates the IVD Antibody Raw Materials Market, holding a significant 35.14% market share, primarily driven by the United States, Canada, and Mexico. The region's leadership stems from its advanced healthcare systems and high demand for diagnostic testing, outpacing other areas like Europe and Asia-Pacific. This position is reinforced by detailed market analyses showing the highest sales values in the U.S. and Canada compared to Japan, China, and other regions.

- The dominance is supported by superior healthcare infrastructure, stringent regulatory environments, and substantial R&D investments in genomics, molecular diagnostics, and precision medicine. These factors enable early disease detection and personalized healthcare, boosting the need for high-quality antibodies and antigens. Additionally, strategic collaborations and regulatory approvals, such as CE-IVD endorsements, enhance market accessibility and growth in the U.S. and Canada.

- Major players like Thermo Fisher Scientific, Sysmex America, Merck KGaA, and Creative Diagnostics are headquartered or heavily active in North America, driving innovations such as recombinant proteins for COVID-19 tests that improve sensitivity by up to 15%. Recent developments include Sysmex America's July 2023 partnership with Sysmex Partec for antibody distribution in Canada. These activities solidify the region's market leadership through technological advancements and robust industry presence.

Active Key Players in the Ivd Antibody Raw Materials Market:

- Merck KGaA (Germany)

- Thermo Fisher Scientific (USA)

- Fujirebio (Japan)

- Fapon Biotech (China)

- F. Hoffmann-La Roche (Switzerland)

- Aalto Bio Reagents (Finland)

- Bio-Rad Laboratories (USA)

- LGC Group (UK)

- HyTest (Finland)

- Medix Biochemica (Finland)

- Meridian Bioscience (USA)

- MP Biomedicals (USA)

- Abcam (UK)

- Cell Signaling Technology (USA)

- BD Biosciences (USA)

- Sigma-Aldrich (USA)

- Creative Diagnostics (USA)

- Sino Biological (China)

- ACROBiosystems (China)

- Other Active Players

|

Ivd Antibody Raw Materials Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 1.31 Billion |

|

Forecast Period 2024-2035 CAGR: |

6.0 % |

Market Size in 2035: |

USD 2.46 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Technology |

|

||

|

By End-User |

|

||

|

By Geography |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Ivd Antibody Raw Materials Market by Product Type (2017-2035)

4.1 Ivd Antibody Raw Materials Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Antibodies & Antigens

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Enzymes

4.5 Proteins

4.6 Biological Buffers

4.7 Others

Chapter 5: Ivd Antibody Raw Materials Market by Technology (2017-2035)

5.1 Ivd Antibody Raw Materials Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Immunochemistry

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Molecular Diagnostics

5.5 Clinical Chemistry

5.6 Others

Chapter 6: Ivd Antibody Raw Materials Market by End-User (2017-2035)

6.1 Ivd Antibody Raw Materials Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Pharmaceutical & Biotechnology Companies

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Diagnostic Laboratories

6.5 Contract Research Organizations

6.6 Others

Chapter 7: Ivd Antibody Raw Materials Market by Geography (2017-2035)

7.1 Ivd Antibody Raw Materials Market Snapshot and Growth Engine

7.2 Market Overview

7.3 North America

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Europe

7.5 Asia-Pacific

7.6 Latin America

7.7 Middle East & Africa

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Ivd Antibody Raw Materials Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 MERCK KGAA

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 THERMO FISHER SCIENTIFIC

8.4 FUJIREBIO

8.5 FAPON BIOTECH

8.6 F. HOFFMANN-LA ROCHE

8.7 AALTO BIO REAGENTS

8.8 BIO-RAD LABORATORIES

8.9 LGC GROUP

8.10 HYTEST

8.11 MEDIX BIOCHEMICA

8.12 MERIDIAN BIOSCIENCE

8.13 MP BIOMEDICALS

8.14 ABCAM

8.15 CELL SIGNALING TECHNOLOGY

8.16 BD BIOSCIENCES

8.17 SIGMA-ALDRICH

8.18 CREATIVE DIAGNOSTICS

8.19 SINO BIOLOGICAL

8.20 ACROBIOSYSTEMS

Chapter 9: Global Ivd Antibody Raw Materials Market By Region

9.1 Overview

9.2. North America Ivd Antibody Raw Materials Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Ivd Antibody Raw Materials Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Ivd Antibody Raw Materials Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Ivd Antibody Raw Materials Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Ivd Antibody Raw Materials Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Ivd Antibody Raw Materials Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Ivd Antibody Raw Materials Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 1.31 Billion |

|

Forecast Period 2024-2035 CAGR: |

6.0 % |

Market Size in 2035: |

USD 2.46 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Technology |

|

||

|

By End-User |

|

||

|

By Geography |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||