Interventional Pulmonology Market Synopsis:

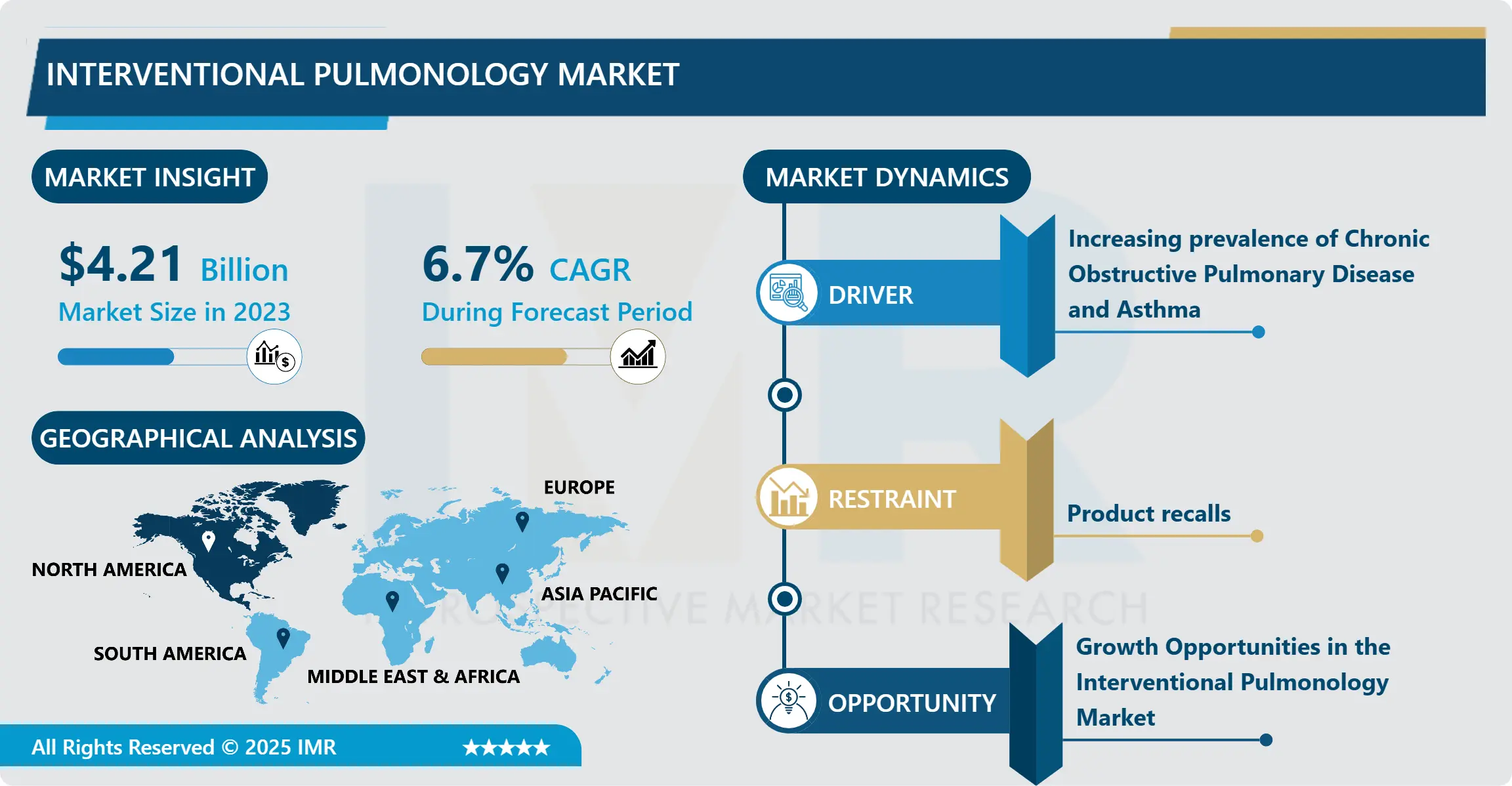

Interventional Pulmonology Market Size Was Valued at USD 4.21 Billion in 2023, and is Projected to Reach USD 7.55 Billion by 2032, Growing at a CAGR of 6.70% From 2024-2032.

The treatment of healthcare interventional pulmonology is a rather narrow segment of medical practice that involves the diagnosis and subsequent treatment of diseases that affect people’s lungs with the help of minimally invasive techniques. This market currently comprises of a variety of techniques and technologies including bronchoscopic techniques and technologies including bronchoscopy, endobronchial ultrasound (EBUS) and navigational bronchoscopy that enables delivery of various procedures to the lung and airways with relatively less discomfort to the patient and comparatively shorter recovery period than through surgical methods. Respiratory diseases including lung cancer, COPD, and interstitial lung disease are still on the rise worldwide, hence, interventional pulmonology services and products are expected to be on the rise due to increased technological developments, increasing global population and growing healthcare conglomerates’ emphasis on differentiation.

It is seize that this Interventional Pulmonology market is one of the fast-growing markets due to increased development of technologies as well as higher global cases of respiratory diseases. Interventional pulmonology refers to the use of minimally invasive diagnostic and therapeutic pediatric pulmonology, lung cancer diagnostic and management, interventional bronchoscopy, endobronchial ultrasound, and thoracoscopy. With increased global population, there is a higher tendency for most people to develop chronic obstructive pulmonary disease, lung cancer, chronic bronchitis and other respiratory diseases that require better diagnosis and efficient treatment. In addition, there is growing concern about diagnosing and treating lung diseases early thereby positively influencing the interventional pulmonology procedures.

Technological factors remain central in the market growth because innovations like navigation bronchoscopy and robot-assisted approaches guarantee accuracy as well as patient safety. They help pulmonologists conduct problematic interventions with less harm to the patient’s body, and with better results. And lastly, advancements such as new devices and instruments that are currently available for the medical fraternity such as new bronchoscopes and biopsy instruments are adding to the market growth. The situation regarding outpatient procedures is also developing well, as, as a rule, such interventions involve a shorter recovery period and the absence of a hospital stay, which affects the decision of patients and healthcare facilities.

Due to the present infrastructure, expenditure on healthcare, and regulatory permissions, the North America region has a large market share in the interventional pulmonology market. However, the fastest growth rate is expected in the Asia-Pacific region due to rising investments in the healthcare industry, improved awareness of pulmonary diseases, and the rising population of the region. Industry leaders are now aiming to form strategic alliances, acquisition and mergers to diversify their portfolios and to extend their market share. This is because as the interventional pulmonology market grows in the future, ongoing research will reveal fresh techniques and products to further drive the market and help patients get better.

Interventional Pulmonology Market Trend Analysis:

Key Trends in the Interventional Pulmonology Market

-

Another popular trend of the interventional pulmonology market is the use of imaging techniques including endobronchial ultrasound (EBUS) and fluoroscopy. Using these technologies, doctors achieve high accuracy in both diagnostic and therapeutic methods related to lung structures visibility. This helps in providing better biopsy and fewer complications hence improving on the patients’ health. EBUS assists clinicians to get detailed views of mediastinal lymph nodes & neighbouring tissues for diagnosis & staging of lung cancer & other respiratory diseases. This is because as more and more healthcare providers integrate these technologies into their practice they will act as a catalyst to the development of the interventional pulmonology segment.

- Not only have excellent imaging been developed in interventional pulmonology, but also, the use of robotic-assisted bronchoscopy is changing this field. Such novel application of the SPR system provides higher flexibility and accuracy even beyond the current bronchoscopy methods. Due to enhancing flexibility and control during operation, robotic systems reduce patient’s pain and enhance the sustainability of operations. Therefore, there is a sense of increased attention to the ability to invest across some of the leading firms operating in the sector in order to create new and exciting products and therapies that incorporate new technologies. The competition is being shifted, toward development of new invigorating procedures which are in sync with the augmenting insurgence of demand of interventions with minimal invasiveness to the human body that anthropologically cements the place of interventional pulmonology in the existing respiratory therapeutics.

Advancements in the Interventional Pulmonology Market Through Technological Innovations

-

Innovative technology in interventional pulmonology such as enhanced imaging and stiffer bronchoscopes supplies additional to useful accuracy with diagnostics and treatments. Techniques like radial EBUS, and navigational bronchoscopy helps in better identification of lesion and therefore enhances the chance of biopsies or other procedures being done. These advance also makes diagnosis possible while improving the treatment returns because it allows the clinicians to deliver procedures that are sensitive to the patients. Additionally, the visuals of the pulmonary anatomy is real helps to offer precise interferences with the anatomy and this can go along way in increasing the patient satisfaction and their confidence in these medical procedures.

- The fact that recovery time to normalcy is shortened due to these techniques is another factor which explains why interventional pulmonology has become the go to specialty for the management of various pulmonary diseases. In the context of setting up more healthcare facilities that have leer sophisticated equipment for diagnostics and treatment and training of specialists the use of such a technologies starts growing. The employment of new people in this field is in line with the progressive improvement of the efficiency of the pulmonary services because the new generation nurses, Respiratory therapists, etc, are more skilled as compared to their counterparts in the past. Increasing demand for enhanced patient value and the growing need for less invasive procedures is fuelling the growth of the market and makes interventional pulmonology a key focal point in healthcare sector.

Interventional Pulmonology Market Segment Analysis:

Interventional Pulmonology Market is Segmented on the basis of Type, Application, End User, and Region

By Type, Bronchoscopes segment is expected to dominate the market during the forecast period

-

Bronchoscopes are essential in current pulmonary practice as it offers doctors an opportunity to see the bronchial tree and perform numerous interventions. These devices come in two main types: flexible and rigid. Flexible bronchoscopes are particularly preferred in practice due to the options available and the amount of CO that patients experience during the procedure. This design enables the passage through the intricate structure of the lungs to reach difficult to access regions of the lungs. Bendability is vital when it concerns performing such operation like biopsies, foreign body removal, and airway interventions whereby precision and patient tolerance is very essential.

- Rigid bronchoscopes are employed in less frequent occasions; in surgeries for example or when larger instruments are required. They provide a wider aperture for the passage of endoscopes which may be of importance in particular circumstances. Nevertheless, considerable patient discomfort and the necessity of sedation are usually reported during examinations conducted with the help of rigid bronchoscopes. In general, how to choose between the two basically relies on specific clinical factors while at the same time, flexible bronchoscopes gradually become the first choice for various diagnostic and therapeutic procedures due to improved patient satisfaction in addition to better results.

By End User, Hospitals segment expected to held the largest share

-

Hospitals remain the most critical and significant client in bronchoscopes and endotherapy device market since it provides modern facilities that help healthcare personnel handle many complicated respiratory procedures. Of these institutions are to provide care to patients who develop complications that need intensive care especially if they have respiratory illnesses. Specialized teams of physicians including pulmonologists, anesthesiologists and nursing staff can devise respiratory treatments that will suit every patient’s needs in the hospitals. This approach is important since it favors proper evaluation of the patients and fit intervention that is important for management of severe asthma, COPD and lung cancer.

- Also, the treatment choice in hospitals is vast because of the modern technologies in bronchoscopy and respiratory therapy. For example, in the interventional airway procedure, they use a flexible bronchoscopy for the less invasive technique of visualizing and performing surgical interventions in the bronchial tree, but they use a rigid bronchoscopy in extensive surgery requiring the use of large instruments. Furthermore, hospitals enjoy most of the state of art imaging technologies, including computed tomography (CT) scans and fluoroscopy that can be deployed to support bronchoscopic interventions and improve the diagnostic yield. The wide range of capabilities is valuable not only in effective management of respiratory conditions but demonstrates the role of hospitals as a system to provide necessary volume of individual attention in the sphere of respiratory care.

Interventional Pulmonology Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

-

North America dominates the interventional pulmonology market due to well developed health infrastructure, presence of high number of cases of chronic obstructive pulmonary disease and lung cancer. The region has fairly well developed healthcare systems which are well equipped to support the use of minimally invasive interventional technology. This in combination with higher emphasis put on research and development promotes innovations in treatment techniques. Over time, healthcare providers are always in a constant search for the better results of their treatments; the use of new technologies & techniques results in increased quality of care for patients with respiratory diseases.

- Also, the demographic of knowledgeable people in a healthcare facility specializing in interventional pulmonology services is experienced across North America that in turn fuels the growth of the market. The availability and constant growth of qualified interventional pulmonologists backed by positive changes in reimbursement when it comes to these complex treatments, pressures the healthcare organizations and facilities into exploring these capabilities further. Availabilities of insurance policies for interventional pulmonology techniques increase market utilization, which improving the rate of utilization. IA running head: INTERVENTIONAL PULMONOLOGY IN NORTH AMERICA As the need for efficient interventions for chronic respiratory diseases continues to be revolutionarily felt, North America is thus projected to retain its market dominance hence helping to steer the interventional pulmonology market and, in effect, the quality of the outcomes achieved in the treatment of patients’ chronic respiratory diseases.

Active Key Players in the Interventional Pulmonology Market:

-

Boston Scientific Corporation,

- Olympus Corporation,

- FUJIFILM Corporation,

- Becton,

- Dickinson and Company,

- Smith’s Group plc.,

- Cook Medical,

- Vygon,

- PENTAX Medical,

- Clarus Medical LLC,

- HUGER Medical Instrument Co., Ltd.,

- Richard Wolf Corporation,

- Karl Storz,

- Taewoong Medical Co., Ltd.,

- ELLA – CS, s.r.o

- Other Active Players

|

Interventional Pulmonology Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 4.21 Billion |

|

Forecast Period 2024-32 CAGR: |

6.70% |

Market Size in 2032: |

USD 7.55 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Interventional Pulmonology Market by Product Type

4.1 Interventional Pulmonology Market Snapshot and Growth Engine

4.2 Interventional Pulmonology Market Overview

4.3 Bronchoscopes

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.3.3 Key Market Trends, Growth Factors and Opportunities

4.3.4 Bronchoscopes: Geographic Segmentation Analysis

4.4 Electromagnetic Navigation Bronchoscopy Systems

4.4.1 Introduction and Market Overview

4.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.4.3 Key Market Trends, Growth Factors and Opportunities

4.4.4 Electromagnetic Navigation Bronchoscopy Systems: Geographic Segmentation Analysis

4.5 Pleuroscopes

4.5.1 Introduction and Market Overview

4.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.5.3 Key Market Trends, Growth Factors and Opportunities

4.5.4 Pleuroscopes: Geographic Segmentation Analysis

4.6 Respiratory Endotherapy Devices

4.6.1 Introduction and Market Overview

4.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.6.3 Key Market Trends, Growth Factors and Opportunities

4.6.4 Respiratory Endotherapy Devices: Geographic Segmentation Analysis

4.7 Airway Stents

4.7.1 Introduction and Market Overview

4.7.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.7.3 Key Market Trends, Growth Factors and Opportunities

4.7.4 Airway Stents: Geographic Segmentation Analysis

4.8 Pleural Catheters

4.8.1 Introduction and Market Overview

4.8.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.8.3 Key Market Trends, Growth Factors and Opportunities

4.8.4 Pleural Catheters: Geographic Segmentation Analysis

4.9 Endobronchial Valves

4.9.1 Introduction and Market Overview

4.9.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.9.3 Key Market Trends, Growth Factors and Opportunities

4.9.4 Endobronchial Valves: Geographic Segmentation Analysis

4.10 Bronchial Thermoplasty Systems

4.10.1 Introduction and Market Overview

4.10.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.10.3 Key Market Trends, Growth Factors and Opportunities

4.10.4 Bronchial Thermoplasty Systems: Geographic Segmentation Analysis

Chapter 5: Interventional Pulmonology Market by Indication

5.1 Interventional Pulmonology Market Snapshot and Growth Engine

5.2 Interventional Pulmonology Market Overview

5.3 Asthma

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.3.3 Key Market Trends, Growth Factors and Opportunities

5.3.4 Asthma: Geographic Segmentation Analysis

5.4 Chronic Obstructive Pulmonary Disease

5.4.1 Introduction and Market Overview

5.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.4.3 Key Market Trends, Growth Factors and Opportunities

5.4.4 Chronic Obstructive Pulmonary Disease: Geographic Segmentation Analysis

5.5 Lung Cancer

5.5.1 Introduction and Market Overview

5.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.5.3 Key Market Trends, Growth Factors and Opportunities

5.5.4 Lung Cancer: Geographic Segmentation Analysis

5.6 Tracheal & Bronchial Stenosis

5.6.1 Introduction and Market Overview

5.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.6.3 Key Market Trends, Growth Factors and Opportunities

5.6.4 Tracheal & Bronchial Stenosis: Geographic Segmentation Analysis

5.7 Others

5.7.1 Introduction and Market Overview

5.7.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.7.3 Key Market Trends, Growth Factors and Opportunities

5.7.4 Others: Geographic Segmentation Analysis

Chapter 6: Interventional Pulmonology Market by End User

6.1 Interventional Pulmonology Market Snapshot and Growth Engine

6.2 Interventional Pulmonology Market Overview

6.3 Hospitals

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.3.3 Key Market Trends, Growth Factors and Opportunities

6.3.4 Hospitals: Geographic Segmentation Analysis

6.4 Ambulatory Surgical Centers

6.4.1 Introduction and Market Overview

6.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.4.3 Key Market Trends, Growth Factors and Opportunities

6.4.4 Ambulatory Surgical Centers: Geographic Segmentation Analysis

6.5 Diagnostic Centers

6.5.1 Introduction and Market Overview

6.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.5.3 Key Market Trends, Growth Factors and Opportunities

6.5.4 Diagnostic Centers: Geographic Segmentation Analysis

6.6 Specialty Clinics

6.6.1 Introduction and Market Overview

6.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.6.3 Key Market Trends, Growth Factors and Opportunities

6.6.4 Specialty Clinics : Geographic Segmentation Analysis

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Interventional Pulmonology Market Share by Manufacturer (2023)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 BOSTON SCIENTIFIC CORPORATION

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 OLYMPUS CORPORATION

7.4 FUJIFILM CORPORATION

7.5 BECTON

7.6 DICKINSON AND COMPANY

7.7 SMITHS GROUP PLC.

7.8 COOK MEDICAL

7.9 VYGON

7.10 PENTAX MEDICAL

7.11 CLARUS MEDICAL LLC

7.12 HUGER MEDICAL INSTRUMENT CO. LTD.

7.13 RICHARD WOLF CORPORATION

7.14 KARL STORZ

7.15 TAEWOONG MEDICAL CO. LTD.

7.16 AND ELLA – CS

7.17 S.R.O

7.18 OTHER ACTIVE PLAYERS

Chapter 8: Global Interventional Pulmonology Market By Region

8.1 Overview

8.2. North America Interventional Pulmonology Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size By Product Type

8.2.4.1 Bronchoscopes

8.2.4.2 Electromagnetic Navigation Bronchoscopy Systems

8.2.4.3 Pleuroscopes

8.2.4.4 Respiratory Endotherapy Devices

8.2.4.5 Airway Stents

8.2.4.6 Pleural Catheters

8.2.4.7 Endobronchial Valves

8.2.4.8 Bronchial Thermoplasty Systems

8.2.5 Historic and Forecasted Market Size By Indication

8.2.5.1 Asthma

8.2.5.2 Chronic Obstructive Pulmonary Disease

8.2.5.3 Lung Cancer

8.2.5.4 Tracheal & Bronchial Stenosis

8.2.5.5 Others

8.2.6 Historic and Forecasted Market Size By End User

8.2.6.1 Hospitals

8.2.6.2 Ambulatory Surgical Centers

8.2.6.3 Diagnostic Centers

8.2.6.4 Specialty Clinics

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Interventional Pulmonology Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size By Product Type

8.3.4.1 Bronchoscopes

8.3.4.2 Electromagnetic Navigation Bronchoscopy Systems

8.3.4.3 Pleuroscopes

8.3.4.4 Respiratory Endotherapy Devices

8.3.4.5 Airway Stents

8.3.4.6 Pleural Catheters

8.3.4.7 Endobronchial Valves

8.3.4.8 Bronchial Thermoplasty Systems

8.3.5 Historic and Forecasted Market Size By Indication

8.3.5.1 Asthma

8.3.5.2 Chronic Obstructive Pulmonary Disease

8.3.5.3 Lung Cancer

8.3.5.4 Tracheal & Bronchial Stenosis

8.3.5.5 Others

8.3.6 Historic and Forecasted Market Size By End User

8.3.6.1 Hospitals

8.3.6.2 Ambulatory Surgical Centers

8.3.6.3 Diagnostic Centers

8.3.6.4 Specialty Clinics

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Interventional Pulmonology Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size By Product Type

8.4.4.1 Bronchoscopes

8.4.4.2 Electromagnetic Navigation Bronchoscopy Systems

8.4.4.3 Pleuroscopes

8.4.4.4 Respiratory Endotherapy Devices

8.4.4.5 Airway Stents

8.4.4.6 Pleural Catheters

8.4.4.7 Endobronchial Valves

8.4.4.8 Bronchial Thermoplasty Systems

8.4.5 Historic and Forecasted Market Size By Indication

8.4.5.1 Asthma

8.4.5.2 Chronic Obstructive Pulmonary Disease

8.4.5.3 Lung Cancer

8.4.5.4 Tracheal & Bronchial Stenosis

8.4.5.5 Others

8.4.6 Historic and Forecasted Market Size By End User

8.4.6.1 Hospitals

8.4.6.2 Ambulatory Surgical Centers

8.4.6.3 Diagnostic Centers

8.4.6.4 Specialty Clinics

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Interventional Pulmonology Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size By Product Type

8.5.4.1 Bronchoscopes

8.5.4.2 Electromagnetic Navigation Bronchoscopy Systems

8.5.4.3 Pleuroscopes

8.5.4.4 Respiratory Endotherapy Devices

8.5.4.5 Airway Stents

8.5.4.6 Pleural Catheters

8.5.4.7 Endobronchial Valves

8.5.4.8 Bronchial Thermoplasty Systems

8.5.5 Historic and Forecasted Market Size By Indication

8.5.5.1 Asthma

8.5.5.2 Chronic Obstructive Pulmonary Disease

8.5.5.3 Lung Cancer

8.5.5.4 Tracheal & Bronchial Stenosis

8.5.5.5 Others

8.5.6 Historic and Forecasted Market Size By End User

8.5.6.1 Hospitals

8.5.6.2 Ambulatory Surgical Centers

8.5.6.3 Diagnostic Centers

8.5.6.4 Specialty Clinics

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Interventional Pulmonology Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size By Product Type

8.6.4.1 Bronchoscopes

8.6.4.2 Electromagnetic Navigation Bronchoscopy Systems

8.6.4.3 Pleuroscopes

8.6.4.4 Respiratory Endotherapy Devices

8.6.4.5 Airway Stents

8.6.4.6 Pleural Catheters

8.6.4.7 Endobronchial Valves

8.6.4.8 Bronchial Thermoplasty Systems

8.6.5 Historic and Forecasted Market Size By Indication

8.6.5.1 Asthma

8.6.5.2 Chronic Obstructive Pulmonary Disease

8.6.5.3 Lung Cancer

8.6.5.4 Tracheal & Bronchial Stenosis

8.6.5.5 Others

8.6.6 Historic and Forecasted Market Size By End User

8.6.6.1 Hospitals

8.6.6.2 Ambulatory Surgical Centers

8.6.6.3 Diagnostic Centers

8.6.6.4 Specialty Clinics

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Interventional Pulmonology Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size By Product Type

8.7.4.1 Bronchoscopes

8.7.4.2 Electromagnetic Navigation Bronchoscopy Systems

8.7.4.3 Pleuroscopes

8.7.4.4 Respiratory Endotherapy Devices

8.7.4.5 Airway Stents

8.7.4.6 Pleural Catheters

8.7.4.7 Endobronchial Valves

8.7.4.8 Bronchial Thermoplasty Systems

8.7.5 Historic and Forecasted Market Size By Indication

8.7.5.1 Asthma

8.7.5.2 Chronic Obstructive Pulmonary Disease

8.7.5.3 Lung Cancer

8.7.5.4 Tracheal & Bronchial Stenosis

8.7.5.5 Others

8.7.6 Historic and Forecasted Market Size By End User

8.7.6.1 Hospitals

8.7.6.2 Ambulatory Surgical Centers

8.7.6.3 Diagnostic Centers

8.7.6.4 Specialty Clinics

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Interventional Pulmonology Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 4.21 Billion |

|

Forecast Period 2024-32 CAGR: |

6.70% |

Market Size in 2032: |

USD 7.55 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||