Key Market Highlights

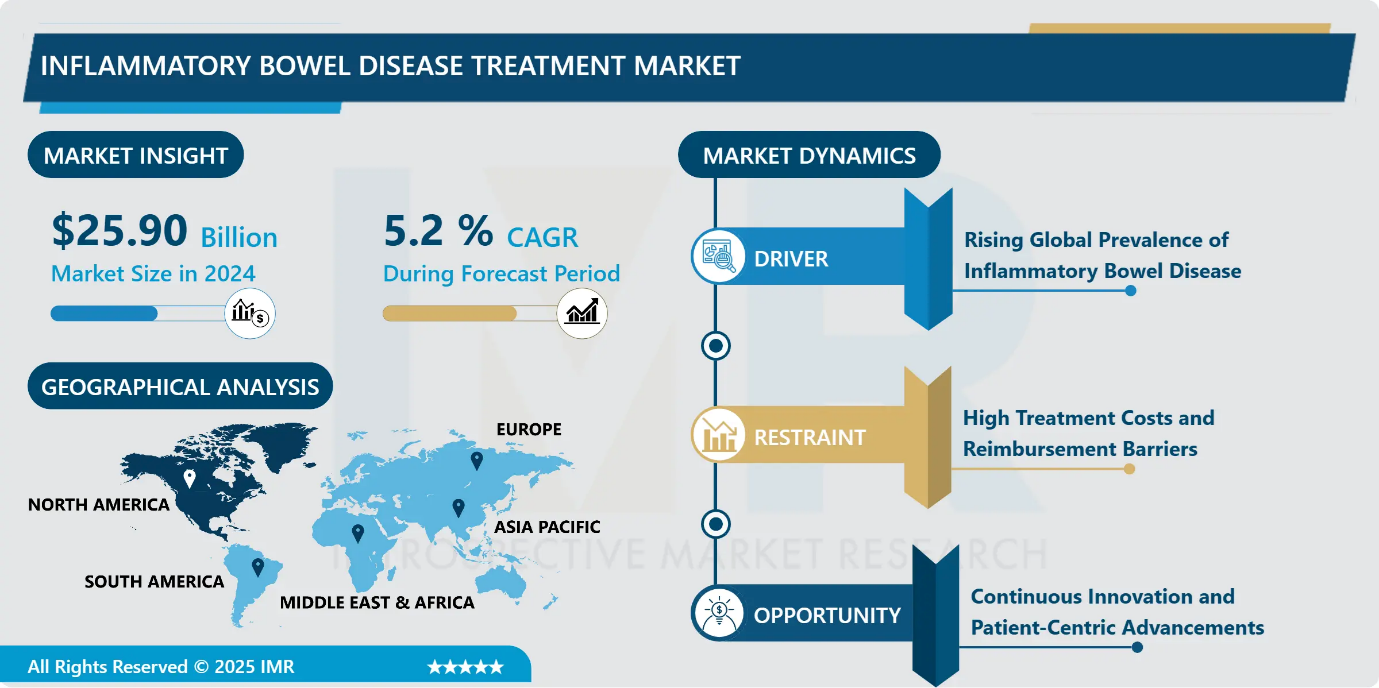

Inflammatory Bowel Disease Treatment Market Size Was Valued at USD 25.90 Billion in 2024, and is Projected to Reach USD 45.23 Billion by 2035, Growing at a CAGR of 5.2 % from 2025-2035.

- Market Size in 2024: USD 25.90 Billion

- Projected Market Size by 2035: USD 45.23 Billion

- CAGR (2025–2035): 5.2 %

- Leading Market in 2024: North America

- Fastest-Growing Market: Asia Pacific

- By Drug Class: The TNF Inhibitors segment is anticipated to lead the market by accounting for 25.3% of the market share throughout the forecast period.

- By Route of Administration: The Injectable segment is expected to capture 27.4% of the market share, thereby maintaining its dominance over the forecast period.

- By Region: North America region is projected to hold 34.2% of the market share during the forecast period.

- Active Players: AbbVie Inc. (U.S.), Abbott Laboratories (U.S.), Alvotech (Iceland), Amgen Inc. (U.S.), Biogen Inc. (U.S.), and Other Active Players.

Inflammatory Bowel Disease Treatment Market Synopsis:

The Inflammatory Bowel Disease (IBD) Treatment Market refers to the global pharmaceutical industry focused on developing and commercializing therapies for chronic inflammatory conditions of the gastrointestinal tract, primarily Crohn’s disease and ulcerative colitis. According to the European Federation of Crohn's & Ulcerative Colitis Associations (EFCCA), nearly 10 million people worldwide live with IBD, highlighting a significant unmet clinical need. Rising prevalence, increasing diagnosis rates, and growing awareness are driving demand for effective long-term therapies. The market encompasses aminosalicylates, corticosteroids, biologics such as TNF and interleukin inhibitors, and oral small molecules including JAK inhibitors. Strong product pipelines, biosimilar adoption, AI-driven drug discovery, and supportive government healthcare initiatives are further accelerating market growth globally.

Inflammatory Bowel Disease Treatment Market Dynamics and Trend Analysis:

Inflammatory Bowel Disease Treatment Market Growth Driver

Rising Global Prevalence of Inflammatory Bowel Disease

- The increasing global incidence of inflammatory bowel disease (IBD), including Crohn’s disease and ulcerative colitis, is a major factor propelling market growth. Shifts toward Westernized diets, sedentary lifestyles, urbanization, and greater exposure to environmental triggers have contributed to a steady rise in diagnoses worldwide. Improved awareness and advancements in diagnostic capabilities have also led to earlier and more accurate detection. As the patient pool expands across both developed and emerging regions, demand for advanced, long-term therapeutic options continues to grow, driving sustained investment, innovation, and commercialization within the IBD treatment market.

Inflammatory Bowel Disease Treatment Market Limiting Factor

High Treatment Costs and Reimbursement Barriers

- The inflammatory bowel disease drugs market faces significant constraints due to the high cost of biologics and advanced targeted therapies, which limit affordability and restrict access, particularly in cost-sensitive and emerging markets. Premium pricing places substantial pressure on healthcare systems and patients, reducing widespread adoption despite strong clinical demand. Additionally, restrictive reimbursement frameworks, step-therapy requirements, prior authorization processes, and high out-of-pocket expenses delay treatment initiation and limit timely access to innovative therapies. These financial and administrative barriers hinder optimal patient uptake, slow market penetration of advanced drugs, and pose ongoing challenges to sustained market expansion.

Inflammatory Bowel Disease Treatment Market Expansion Opportunity

Continuous Innovation and Patient-Centric Advancements

- The inflammatory bowel disease drugs market presents strong growth opportunities driven by continuous therapeutic innovation and an expanding clinical pipeline. Ongoing research is introducing novel biologics, targeted small molecules, and next-generation mechanisms designed to improve efficacy and safety outcomes. Advancements in diagnostic technologies and growing disease awareness are enabling earlier detection and timely treatment initiation, expanding the treated patient population. Additionally, the shift toward targeted, patient-friendly therapies including convenient oral formulations and treatments with improved tolerabilitysupports better adherence and long-term disease management. These developments create significant commercial potential for companies investing in differentiated, precision-based IBD treatment solutions.

Inflammatory Bowel Disease Treatment Market Challenge and Risk

Safety, Regulatory, and Treatment Complexity Challenges

- The inflammatory bowel disease treatment market faces challenges related to safety concerns, stringent regulatory requirements, and complex disease management. Advanced immunomodulatory therapies may increase the risk of infections and other adverse events, prompting cautious prescribing and ongoing patient monitoring. Regulatory agencies impose rigorous clinical trial standards and post-marketing safety requirements, extending development timelines and increasing research costs. Additionally, IBD requires long-term, multifaceted treatment strategies involving biologics, oral therapies, and continuous monitoring, which can affect patient adherence and strain healthcare resources. These factors collectively create operational, clinical, and commercial hurdles for market participants.

Inflammatory Bowel Disease Treatment Market Trend

Accelerating Innovation and Expanding Access to Advanced Therapies

- The inflammatory bowel disease treatment market is witnessing a strong shift toward advanced biologics and targeted small molecules, including TNF inhibitors, interleukin inhibitors, anti-integrins, and JAK inhibitors. These therapies offer improved clinical remission rates, targeted mechanisms of action, and enhanced safety profiles compared to conventional treatments, significantly improving patient outcomes. Simultaneously, expanding healthcare infrastructure, broader insurance coverage, and supportive reimbursement frameworks are improving patient access to high-cost innovative therapies. As affordability and availability increase across developed and emerging markets, the adoption of premium, next-generation treatments continues to rise, shaping the competitive landscape and driving sustained market expansion.

Inflammatory Bowel Disease Treatment Market Segment Analysis:

Inflammatory Bowel Disease Treatment Market is segmented based on Disease, Drug Class, Molecule Type, Drug Type, Route of Administration, Distribution Channel, End-User, and Region.

By Drug Class, TNF inhibitors segment is expected to dominate the market with around 25.3% share during the forecast period.

- TNF inhibitors continue to dominate the inflammatory bowel disease therapeutics market due to their established clinical efficacy, long-term safety data, and strong physician familiarity. Their widespread reimbursement coverage and extensive real-world evidence have positioned them as standard first-line biologic therapies, reinforcing sustained demand despite biosimilar competition. However, JAK inhibitors are rapidly gaining traction owing to their oral administration, fast onset of action, and expanding safety validation. Interleukin inhibitors, particularly IL-23–targeted agents, are also witnessing growing adoption as reimbursement expands globally. The emergence of novel mechanisms, including TL1A and gut-restricted small molecules, reflects increasing therapeutic diversification within the market.

By Route of Administration, Injectable is expected to dominate with close to 27.4% market share during the forecast period.

- Injectable currently dominate the market, primarily because most biologics are administered through subcutaneous or intravenous routes and remain the backbone of moderate-to-severe IBD treatment. Their dominance is supported by strong clinical outcomes and physician confidence in biologic regimens. However, oral therapies are emerging as the fastest-growing segment due to greater convenience, improved patient adherence, and preference for non-invasive administration. Demand is particularly strong among younger and working populations seeking flexible treatment options. As safety profiles strengthen and regulatory clarity improves, oral small molecules are increasingly influencing first-line treatment strategies and long-term disease management approaches.

Inflammatory Bowel Disease Treatment Market Regional Insights:

North America region is estimated to lead the market with around 34.2% share during the forecast period.

- North America dominates the inflammatory bowel disease (IBD) treatment market due to its advanced healthcare infrastructure, strong reimbursement frameworks, and rapid regulatory approvals through the U.S. FDA. The region benefits from early adoption of innovative biologics and oral small molecules, supported by robust real-world evidence and continuous product launches. A strong presence of leading pharmaceutical companies such as AbbVie Inc. and Johnson & Johnson further strengthens market growth. Additionally, high disease awareness, active clinical research, patient advocacy programs, and supportive government policies enhance treatment accessibility, making North America the leading regional market for IBD therapies.

Inflammatory Bowel Disease Treatment Market Active Players:

- AbbVie Inc. (U.S.)

- Abbott Laboratories (U.S.)

- Alvotech (Iceland)

- Amgen Inc. (U.S.)

- Biogen Inc. (U.S.)

- Boehringer Ingelheim (Germany)

- Celltrion Inc. (South Korea)

- Eli Lilly and Company (U.S.)

- Ferring Pharmaceuticals (Switzerland)

- Johnson & Johnson (U.S.)

- Merck & Co., Inc. (U.S.)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- UCB S.A. (Belgium)

- Other Active Players

Key Industry Developments in the Inflammatory Bowel Disease Treatment Market:

- In January 2025, Eli Lilly and Company received FDA approval for Omvoh to treat adults with moderately to severely active Crohn’s disease.This approval expanded Omvoh’s indications within inflammatory bowel disease.The drug had previously been approved in 2023 for the treatment of ulcerative colitis, marking Lilly’s growing presence in the IBD market.

- In May 2024, Johnson & Johnson announced Phase 3 results from its Crohn’s disease program evaluating Tremfya.The late-stage clinical data showed superior efficacy compared to Stelara in achieving key endoscopic endpoints.These findings strengthened Tremfya’s position as a promising therapy for patients with moderate to severe Crohn’s disease.

Technical Overview of the Inflammatory Bowel Disease (IBD) Treatment Market

- The Inflammatory Bowel Disease (IBD) Treatment Market is technically characterized by a diversified therapeutic landscape targeting chronic immune-mediated inflammation of the gastrointestinal tract, primarily Crohn’s disease and ulcerative colitis. Treatment modalities focus on modulating key inflammatory pathways, including tumor necrosis factor (TNF), interleukin (IL)-12/23, IL-23, integrins, and Janus kinase (JAK) signaling.

- Biologics such as monoclonal antibodies are engineered to selectively inhibit cytokines or adhesion molecules, while small molecules offer intracellular pathway modulation through oral administration. The market also includes corticosteroids and aminosalicylates for mild-to-moderate disease management. Advances in precision medicine, biomarker-driven therapy selection, and therapeutic drug monitoring are optimizing patient outcomes. Biosimilars are increasing cost competitiveness, particularly in TNF inhibitor segments. Additionally, innovations in drug delivery systems, subcutaneous self-injection devices, and gut-selective molecules are enhancing safety, adherence, and long-term disease control across diverse patient populations.

|

Inflammatory Bowel Disease Treatment Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2024 |

Market Size in 2024: |

USD 25.90 Bn. |

|

Forecast Period 2025-32 CAGR: |

5.2 % |

Market Size in 2035: |

USD 45.23 Bn. |

|

Segments Covered: |

By Disease |

|

|

|

By Drug Class |

|

||

|

By Molecule Type |

|

||

|

By Drug Type |

|

||

|

By Route of Administration |

|

||

|

By Distribution Channel |

|

||

|

By End-User |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Inflammatory Bowel Disease Market by Disease (2018-2035)

4.1 Inflammatory Bowel Disease Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Crohn’s Disease and Ulcerative Colitis

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

Chapter 5: Inflammatory Bowel Disease Market by Drug Class (2018-2035)

5.1 Inflammatory Bowel Disease Market Snapshot and Growth Engine

5.2 Market Overview

5.3 TNF Inhibitors

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 JAK Inhibitors

5.5 Integrin Antagonists

5.6 Interleukin Inhibitors

5.7 Corticosteroids

5.8 Aminosalicylates

5.9 and Others

Chapter 6: Inflammatory Bowel Disease Market by Molecule Type (2018-2035)

6.1 Inflammatory Bowel Disease Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Biologics

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Biosimilars

6.5 and Small Molecules

Chapter 7: Inflammatory Bowel Disease Market by Drug Type (2018-2035)

7.1 Inflammatory Bowel Disease Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Biologics

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Small Molecules

7.5 Corticosteroids

7.6 and Others

Chapter 8: Inflammatory Bowel Disease Market by Route of Administration (2018-2035)

8.1 Inflammatory Bowel Disease Market Snapshot and Growth Engine

8.2 Market Overview

8.3 Oral

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

8.3.3 Key Market Trends, Growth Factors, and Opportunities

8.3.4 Geographic Segmentation Analysis

8.4 Injectable

8.5 Intravenous

8.6 Rectal

8.7 and Parenteral

Chapter 9: Inflammatory Bowel Disease Market by Distribution Channel (2018-2035)

9.1 Inflammatory Bowel Disease Market Snapshot and Growth Engine

9.2 Market Overview

9.3 Hospital Pharmacies

9.3.1 Introduction and Market Overview

9.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

9.3.3 Key Market Trends, Growth Factors, and Opportunities

9.3.4 Geographic Segmentation Analysis

9.4 Retail Pharmacies

9.5 Online Pharmacies

9.6 and Others

Chapter 10: Inflammatory Bowel Disease Market by End-User (2018-2035)

10.1 Inflammatory Bowel Disease Market Snapshot and Growth Engine

10.2 Market Overview

10.3 Hospitals

10.3.1 Introduction and Market Overview

10.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

10.3.3 Key Market Trends, Growth Factors, and Opportunities

10.3.4 Geographic Segmentation Analysis

10.4 Specialty Clinics

10.5 Home Care Settings

10.6 Pharmacies

10.7 and Others

Chapter 11: Company Profiles and Competitive Analysis

11.1 Competitive Landscape

11.1.1 Competitive Benchmarking

11.1.2 Inflammatory Bowel Disease Market Share by Manufacturer/Service Provider(2024)

11.1.3 Industry BCG Matrix

11.1.4 PArtnerships, Mergers & Acquisitions

11.2 ABBVIE INC. (U.S.)

11.2.1 Company Overview

11.2.2 Key Executives

11.2.3 Company Snapshot

11.2.4 Role of the Company in the Market

11.2.5 Sustainability and Social Responsibility

11.2.6 Operating Business Segments

11.2.7 Product Portfolio

11.2.8 Business Performance

11.2.9 Recent News & Developments

11.2.10 SWOT Analysis

11.3 ABBOTT LABORATORIES (U.S.)

11.4 ALVOTECH (ICELAND)

11.5 AMGEN INC. (U.S.)

11.6 BIOGEN INC. (U.S.)

11.7 BOEHRINGER INGELHEIM (GERMANY)

11.8 CELLTRION INC. (SOUTH KOREA)

11.9 ELI LILLY AND COMPANY (U.S.)

11.10 FERRING PHARMACEUTICALS (SWITZERLAND)

11.11 JOHNSON & JOHNSON (U.S.)

11.12 MERCK & CO.

11.13 INC. (U.S.)

11.14 NOVARTIS AG (SWITZERLAND)

11.15 PFIZER INC. (U.S.)

11.16 TAKEDA PHARMACEUTICAL COMPANY LIMITED (JAPAN)

11.17 UCB S.A. (BELGIUM).

11.18 AND OTHER ACTIVE PLAYERS.

Chapter 12: Global Inflammatory Bowel Disease Market By Region

12.1 Overview

12.2. North America Inflammatory Bowel Disease Market

12.2.1 Key Market Trends, Growth Factors and Opportunities

12.2.2 Top Key Companies

12.2.3 Historic and Forecasted Market Size by Segments

12.2.4 Historic and Forecast Market Size by Country

12.2.4.1 US

12.2.4.2 Canada

12.2.4.3 Mexico

12.3. Eastern Europe Inflammatory Bowel Disease Market

12.3.1 Key Market Trends, Growth Factors and Opportunities

12.3.2 Top Key Companies

12.3.3 Historic and Forecasted Market Size by Segments

12.3.4 Historic and Forecast Market Size by Country

12.3.4.1 Russia

12.3.4.2 Bulgaria

12.3.4.3 The Czech Republic

12.3.4.4 Hungary

12.3.4.5 Poland

12.3.4.6 Romania

12.3.4.7 Rest of Eastern Europe

12.4. Western Europe Inflammatory Bowel Disease Market

12.4.1 Key Market Trends, Growth Factors and Opportunities

12.4.2 Top Key Companies

12.4.3 Historic and Forecasted Market Size by Segments

12.4.4 Historic and Forecast Market Size by Country

12.4.4.1 Germany

12.4.4.2 UK

12.4.4.3 France

12.4.4.4 The Netherlands

12.4.4.5 Italy

12.4.4.6 Spain

12.4.4.7 Rest of Western Europe

12.5. Asia Pacific Inflammatory Bowel Disease Market

12.5.1 Key Market Trends, Growth Factors and Opportunities

12.5.2 Top Key Companies

12.5.3 Historic and Forecasted Market Size by Segments

12.5.4 Historic and Forecast Market Size by Country

12.5.4.1 China

12.5.4.2 India

12.5.4.3 Japan

12.5.4.4 South Korea

12.5.4.5 Malaysia

12.5.4.6 Thailand

12.5.4.7 Vietnam

12.5.4.8 The Philippines

12.5.4.9 Australia

12.5.4.10 New Zealand

12.5.4.11 Rest of APAC

12.6. Middle East & Africa Inflammatory Bowel Disease Market

12.6.1 Key Market Trends, Growth Factors and Opportunities

12.6.2 Top Key Companies

12.6.3 Historic and Forecasted Market Size by Segments

12.6.4 Historic and Forecast Market Size by Country

12.6.4.1 Turkiye

12.6.4.2 Bahrain

12.6.4.3 Kuwait

12.6.4.4 Saudi Arabia

12.6.4.5 Qatar

12.6.4.6 UAE

12.6.4.7 Israel

12.6.4.8 South Africa

12.7. South America Inflammatory Bowel Disease Market

12.7.1 Key Market Trends, Growth Factors and Opportunities

12.7.2 Top Key Companies

12.7.3 Historic and Forecasted Market Size by Segments

12.7.4 Historic and Forecast Market Size by Country

12.7.4.1 Brazil

12.7.4.2 Argentina

12.7.4.3 Rest of SA

Chapter 13 Analyst Viewpoint and Conclusion

Chapter 14 Our Thematic Research Methodology

13.1 Research Process

13.2 Primary Research

13.3 Secondary Research

Chapter 15 Case Study

Chapter 16 Appendix

14.1 Sources

14.2 List of Tables and figures

14.3 Short Forms and Citations

14.4 Assumption and Conversion

14.5 Disclaimer

|

Inflammatory Bowel Disease Treatment Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2024 |

Market Size in 2024: |

USD 25.90 Bn. |

|

Forecast Period 2025-32 CAGR: |

5.2 % |

Market Size in 2035: |

USD 45.23 Bn. |

|

Segments Covered: |

By Disease |

|

|

|

By Drug Class |

|

||

|

By Molecule Type |

|

||

|

By Drug Type |

|

||

|

By Route of Administration |

|

||

|

By Distribution Channel |

|

||

|

By End-User |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||