Hereditary Cancer Testing Market Synopsis

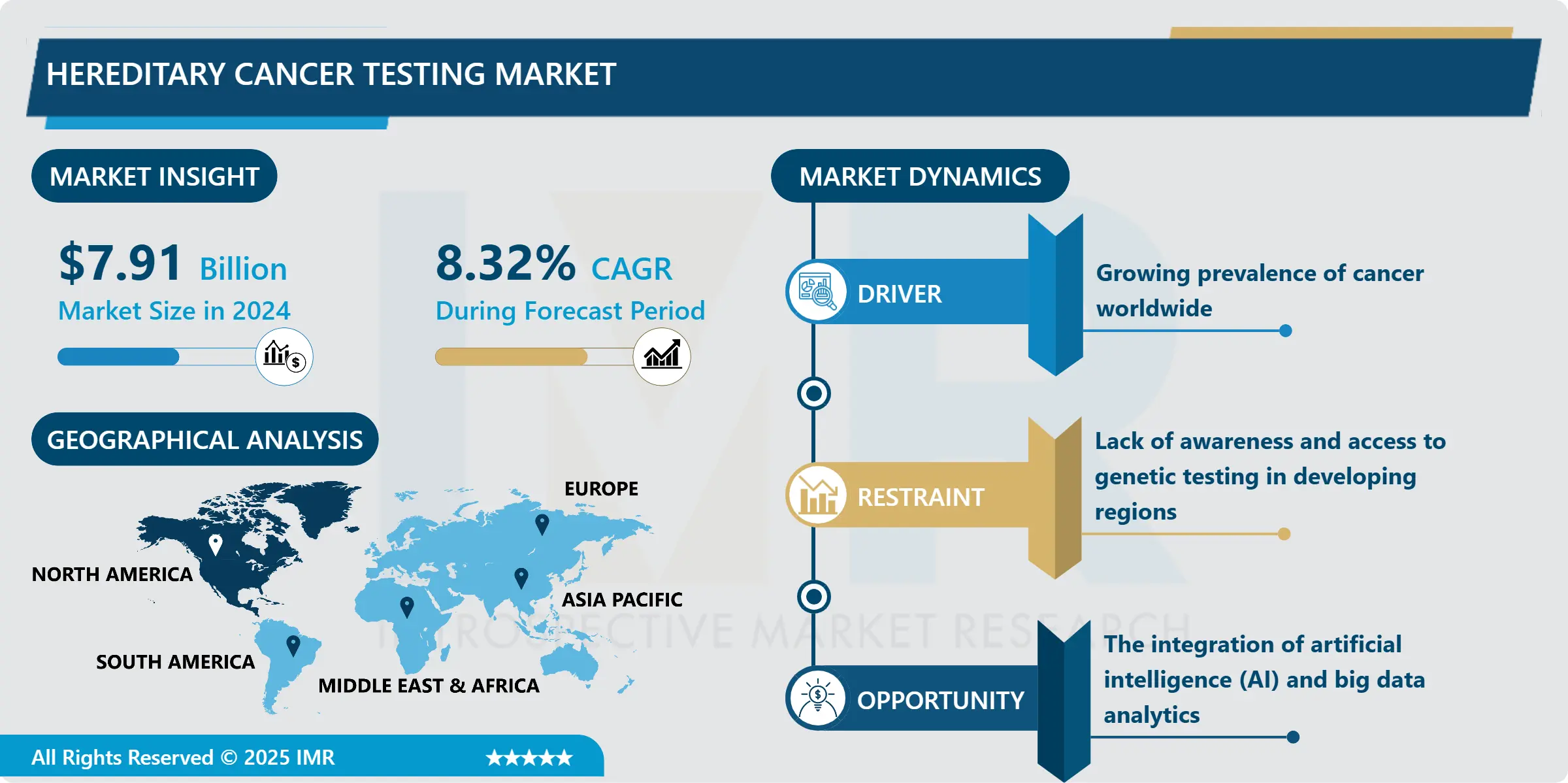

Hereditary Cancer Testing Market Size Was Valued at USD 7.91 Billion in 2024, and is Projected to Reach USD 19.05 Billion by 2035, Growing at a CAGR of 8.32% From 2025-2035.

Hereditary Cancer Testing Market can be defined as the healthcare industry’s niche involving the delivery of genetic tests that can help determine predisposition to certain types of cancer. These tests aid in establish genetic cancer susceptibility syndromes that run in families and increase the risk of getting cancers of Breast, Ovary, Colon, and Prostrate. Hereditary cancer testing is based on an inspection of a human organism’s DNA to identify certain inherited mutations of genes, chromosomes or proteins. The findings are useful to aid in early identification, delay or prevention, and target management plans.

The Hereditary Cancer Testing Market has grown rapidly in the last couple of years due to rising consciousness about genetic examination. Due to recent developments in molecular diagnostics, screening for one or more genes can be easily done through NGS which provides a wide variety of testing possibilities. The increase in new cases of cancer worldwide and particularly familial or hereditary cancer such as breast and ovarian cancer has seen health care consumers and practitioners looking for pathways to early detection and diagnosis resulting in the need for genetic testing. Also, increased demand for various cancer screenings due to government support and insurance reimbursement have also burgeoned this market. The use of hereditary cancer tests is gradually becoming common in clinical practice, providing people with a family history of cancer with more relevant information about their health and preferences for treatment.

The market is also benefited from prudent mergers and relations between firms dealing in diagnostic equipment and reagents, health care providers, and academic research institutions. These partnerships are to create new testing products, increase test availability in the emerging markets, and provide tailor-made treatment programs based on the genetic type. The ability of detecting several genes associated with cancer all at once through multi-gene panel testing is the best advancement experienced in the diagnosis of hereditary cancer syndromes to date. This has made it possible for the healthcare providers to provide better accuracy of the risk involved for the patient thus better quality better provision of care and cost savings. Further, more and more regulatory bodies are approving hereditary cancer tests so they become more available for use in the clinical practice.

Hereditary Cancer Testing Market Trend Analysis

Increasing Adoption of Multi-Gene Panel Testing

- An emerging trend that defines the todays Hereditary Cancer Testing Market is the growth of multipanel testing based on parallel gene testing. While single-gene tests detect only one gene in the body, multi-gene panel testing looks into more than one gene that leads to hereditary cancer risks. This has occurred with the understanding that there are multiple genes associated with cancer and thus dealing with several factors at the same time would provide a better indication of the risk of developing cancer. This is especially beneficial in patients who have immense family histories, in which many possibilities of gene mutations can be considered. The increasing use of this testing method is being occasioned by improved next generation sequencing technology that is cheaper, faster and accurate. With the increasing understanding of the genetics of cancer, the employment of multiple gene testing will soon replace this gene testing for hereditary cancer.

Expansion in Emerging Markets

- A major strong in the Hereditary Cancer Testing Market that could be used is the fact that the market is yet to fully penetrate the international market suggesting that there is always room for growth whereby the markets in Asia-Pacific and Latin America could be explored. These regions are seeing an increased incidence of cancer, primarily cross-linked to factors such as changes in the lifestyle, increased aging population, and urbanization. However, knowledge in genetic testing and the related advantages is still relatively small than those of the developed markets. The governments as well as the healthcare centres in these areas are gradually coming to acknowledge the need for screening and individualized treatments and care and this could boost the uptake of hereditary cancer testing.

- Further, some manufacturers of genetic testing products planning to expand in Asia Pacific area attracted by continuously growing population of middle-income people and constantly developing healthcare sectors. In this regard, genetic testing companies may devise affordable testing solutions and improve cooperation with other medical facilities to gain the largest possible market share. Creating higher coverage of educational materials, raising awareness about early diagnosis’ advantages, and securing testing opportunities through local collaborations will remain important in realising full potential of these markets.

Hereditary Cancer Testing Market Segment Analysis:

Hereditary Cancer Testing Market Segmented on the basis of Disease Type and Technology.

By Disease Type, Hereditary non-Cancer Testing segment is expected to dominate the market during the forecast period

- The hereditary non-cancer testing segment is expected to contribute to maximum market share in the hereditary cancer testing market throughout the forecast period due to rising hereditary cancer testing awareness and enhancing genetic testing techniques. The segment dominated the market revenues and SIEM market and facilitated over 81.2% of the augmented market growth in 2024. Hereditary non-cancer gene testing is aimed at identifying many more genetic diseases including cardiovascular diseases, neurological diseases, and inherited metabolic diseases.

- A growing need for the early diagnosis and prophylaxis of such non- neoplastic hereditary disorders is driving the growth of this segment. Also, non-cancer hereditary test is on steep rise due to the improved NGS technology and the availability of economical genetic test. The rising opportunity of personalized medicine as well as preventing health care also contributes to this market segment, as patients and doctors and other care takers enhance efforts in reducing risks of hereditary diseases. Despite slower growth during the forecast period, hereditary non-cancer testing segment holds substantial potential and demonstrates the highest CAGR growth compared to the other segments.

By Technology, molecular testing segment expected to held the largest share

- When segmented based on the molecular testing, the segment had the largest share in terms of revenue accounting for 54.4% in 2024. This dominance is due to the increasing throughput of molecular diagnostic technologies in genetic testing, the presence of high sensitivity and specificity, and increased identification of mutations associated with hereditary cancers. Molecular tests include the PCR and NGS techniques which can detect specific gene changes and mutations at the molecular level and are therefore the recommended tests by care providers and scientists.

- The need for genetic testing for customize medical treatment based on patients’ DNA has also led to the growth of molecular testing. Further, investments in these technologies are continuously progressing and incorporating high-tech features that have enabled quicker and less expensive deliveries, and increasing access to the populace – all of that points towards a very spectacular development of the segment in the course of the entire forecast period. For this reason, molecular testing remains highly likely to sustain its dominance while also enjoying the fastest growth in the near future.

Hereditary Cancer Testing Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

- North America held the largest share in the Global Hereditary Cancer Testing Market, in 2024 due to factors like enhanced healthcare systems, higher level of understanding in genetic tests and supportive government policies undertaken for cancer screening services. The area has established and rapidly growing biotechnology and diagnostic industries that have contributed to creation of efficient hereditary cancer detecting methods. In 2024, North America is expected to provide about 45-50% of market share.

- One has seen that America in particular has been a major driver of this dominance as it has progressively invest more in cancer research and genetic testing technologies. High participation of various players, testing services available nearly across the region, and substantial incorporation of genetic testing in healthcare practices have consolidated the leadership of North America in the market still further. Further, the increased incidence in cancer in combination with the increasing trend in use of biomarkers in cancer has upped the demand for hereditary cancer testing across the regions.

Active Key Players in the Hereditary Cancer Testing Market

- Ambry Genetics (USA)

- Baylor Genetics (USA)

- Bio-Rad Laboratories (USA)

- CENTOGENE AG (Germany)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Genomic Health (USA)

- Illumina, Inc. (USA)

- Invitae Corporation (USA)

- Laboratory Corporation of America (USA)

- Myriad Genetics (USA)

- Natera, Inc. (USA)

- NeoGenomics Laboratories (USA)

- Pathway Genomics (USA)

- Quest Diagnostics (USA)

- Thermo Fisher Scientific (USA) Other key Players

|

Global Hereditary Cancer Testing Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 7.91 Bn. |

|

Forecast Period 2025-35 CAGR: |

8.32% |

Market Size in 2035: |

USD 19.05 Bn. |

|

Segments Covered: |

By Disease Type |

|

|

|

By Technology |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Hereditary Cancer Testing Market by Disease Type (2018-2035)

4.1 Hereditary Cancer Testing Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Hereditary Cancer Testing

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Hereditary Non-cancer Testing

Chapter 5: Hereditary Cancer Testing Market by Technology (2018-2035)

5.1 Hereditary Cancer Testing Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Cytogenetic

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Biochemical

5.5 Molecular Testing

Chapter 6: Company Profiles and Competitive Analysis

6.1 Competitive Landscape

6.1.1 Competitive Benchmarking

6.1.2 Hereditary Cancer Testing Market Share by Manufacturer (2024)

6.1.3 Industry BCG Matrix

6.1.4 Heat Map Analysis

6.1.5 Mergers and Acquisitions

6.2 AMBRY GENETICS (USA)

6.2.1 Company Overview

6.2.2 Key Executives

6.2.3 Company Snapshot

6.2.4 Role of the Company in the Market

6.2.5 Sustainability and Social Responsibility

6.2.6 Operating Business Segments

6.2.7 Product Portfolio

6.2.8 Business Performance

6.2.9 Key Strategic Moves and Recent Developments

6.2.10 SWOT Analysis

6.3 BAYLOR GENETICS (USA)

6.4 BIO-RAD LABORATORIES (USA)

6.5 CENTOGENE AG (GERMANY)

6.6 F. HOFFMANN-LA ROCHE LTD. (SWITZERLAND)

6.7 GENOMIC HEALTH (USA)

6.8 ILLUMINA INC. (USA)

6.9 INVITAE CORPORATION (USA)

6.10 LABORATORY CORPORATION OF AMERICA (USA)

6.11 MYRIAD GENETICS (USA)

6.12 NATERA INC. (USA)

6.13 NEOGENOMICS LABORATORIES (USA)

6.14 PATHWAY GENOMICS (USA)

6.15 QUEST DIAGNOSTICS (USA)

6.16 THERMO FISHER SCIENTIFIC (USA)

6.17 OTHER KEY PLAYERS

6.18

Chapter 7: Global Hereditary Cancer Testing Market By Region

7.1 Overview

7.2. North America Hereditary Cancer Testing Market

7.2.1 Key Market Trends, Growth Factors and Opportunities

7.2.2 Top Key Companies

7.2.3 Historic and Forecasted Market Size by Segments

7.2.4 Historic and Forecasted Market Size by Disease Type

7.2.4.1 Hereditary Cancer Testing

7.2.4.2 Hereditary Non-cancer Testing

7.2.5 Historic and Forecasted Market Size by Technology

7.2.5.1 Cytogenetic

7.2.5.2 Biochemical

7.2.5.3 Molecular Testing

7.2.6 Historic and Forecast Market Size by Country

7.2.6.1 US

7.2.6.2 Canada

7.2.6.3 Mexico

7.3. Eastern Europe Hereditary Cancer Testing Market

7.3.1 Key Market Trends, Growth Factors and Opportunities

7.3.2 Top Key Companies

7.3.3 Historic and Forecasted Market Size by Segments

7.3.4 Historic and Forecasted Market Size by Disease Type

7.3.4.1 Hereditary Cancer Testing

7.3.4.2 Hereditary Non-cancer Testing

7.3.5 Historic and Forecasted Market Size by Technology

7.3.5.1 Cytogenetic

7.3.5.2 Biochemical

7.3.5.3 Molecular Testing

7.3.6 Historic and Forecast Market Size by Country

7.3.6.1 Russia

7.3.6.2 Bulgaria

7.3.6.3 The Czech Republic

7.3.6.4 Hungary

7.3.6.5 Poland

7.3.6.6 Romania

7.3.6.7 Rest of Eastern Europe

7.4. Western Europe Hereditary Cancer Testing Market

7.4.1 Key Market Trends, Growth Factors and Opportunities

7.4.2 Top Key Companies

7.4.3 Historic and Forecasted Market Size by Segments

7.4.4 Historic and Forecasted Market Size by Disease Type

7.4.4.1 Hereditary Cancer Testing

7.4.4.2 Hereditary Non-cancer Testing

7.4.5 Historic and Forecasted Market Size by Technology

7.4.5.1 Cytogenetic

7.4.5.2 Biochemical

7.4.5.3 Molecular Testing

7.4.6 Historic and Forecast Market Size by Country

7.4.6.1 Germany

7.4.6.2 UK

7.4.6.3 France

7.4.6.4 The Netherlands

7.4.6.5 Italy

7.4.6.6 Spain

7.4.6.7 Rest of Western Europe

7.5. Asia Pacific Hereditary Cancer Testing Market

7.5.1 Key Market Trends, Growth Factors and Opportunities

7.5.2 Top Key Companies

7.5.3 Historic and Forecasted Market Size by Segments

7.5.4 Historic and Forecasted Market Size by Disease Type

7.5.4.1 Hereditary Cancer Testing

7.5.4.2 Hereditary Non-cancer Testing

7.5.5 Historic and Forecasted Market Size by Technology

7.5.5.1 Cytogenetic

7.5.5.2 Biochemical

7.5.5.3 Molecular Testing

7.5.6 Historic and Forecast Market Size by Country

7.5.6.1 China

7.5.6.2 India

7.5.6.3 Japan

7.5.6.4 South Korea

7.5.6.5 Malaysia

7.5.6.6 Thailand

7.5.6.7 Vietnam

7.5.6.8 The Philippines

7.5.6.9 Australia

7.5.6.10 New Zealand

7.5.6.11 Rest of APAC

7.6. Middle East & Africa Hereditary Cancer Testing Market

7.6.1 Key Market Trends, Growth Factors and Opportunities

7.6.2 Top Key Companies

7.6.3 Historic and Forecasted Market Size by Segments

7.6.4 Historic and Forecasted Market Size by Disease Type

7.6.4.1 Hereditary Cancer Testing

7.6.4.2 Hereditary Non-cancer Testing

7.6.5 Historic and Forecasted Market Size by Technology

7.6.5.1 Cytogenetic

7.6.5.2 Biochemical

7.6.5.3 Molecular Testing

7.6.6 Historic and Forecast Market Size by Country

7.6.6.1 Turkiye

7.6.6.2 Bahrain

7.6.6.3 Kuwait

7.6.6.4 Saudi Arabia

7.6.6.5 Qatar

7.6.6.6 UAE

7.6.6.7 Israel

7.6.6.8 South Africa

7.7. South America Hereditary Cancer Testing Market

7.7.1 Key Market Trends, Growth Factors and Opportunities

7.7.2 Top Key Companies

7.7.3 Historic and Forecasted Market Size by Segments

7.7.4 Historic and Forecasted Market Size by Disease Type

7.7.4.1 Hereditary Cancer Testing

7.7.4.2 Hereditary Non-cancer Testing

7.7.5 Historic and Forecasted Market Size by Technology

7.7.5.1 Cytogenetic

7.7.5.2 Biochemical

7.7.5.3 Molecular Testing

7.7.6 Historic and Forecast Market Size by Country

7.7.6.1 Brazil

7.7.6.2 Argentina

7.7.6.3 Rest of SA

Chapter 8 Analyst Viewpoint and Conclusion

8.1 Recommendations and Concluding Analysis

8.2 Potential Market Strategies

Chapter 9 Research Methodology

9.1 Research Process

9.2 Primary Research

9.3 Secondary Research

|

Global Hereditary Cancer Testing Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 7.91 Bn. |

|

Forecast Period 2025-35 CAGR: |

8.32% |

Market Size in 2035: |

USD 19.05 Bn. |

|

Segments Covered: |

By Disease Type |

|

|

|

By Technology |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||