Gene Electroporator Market Synopsis:

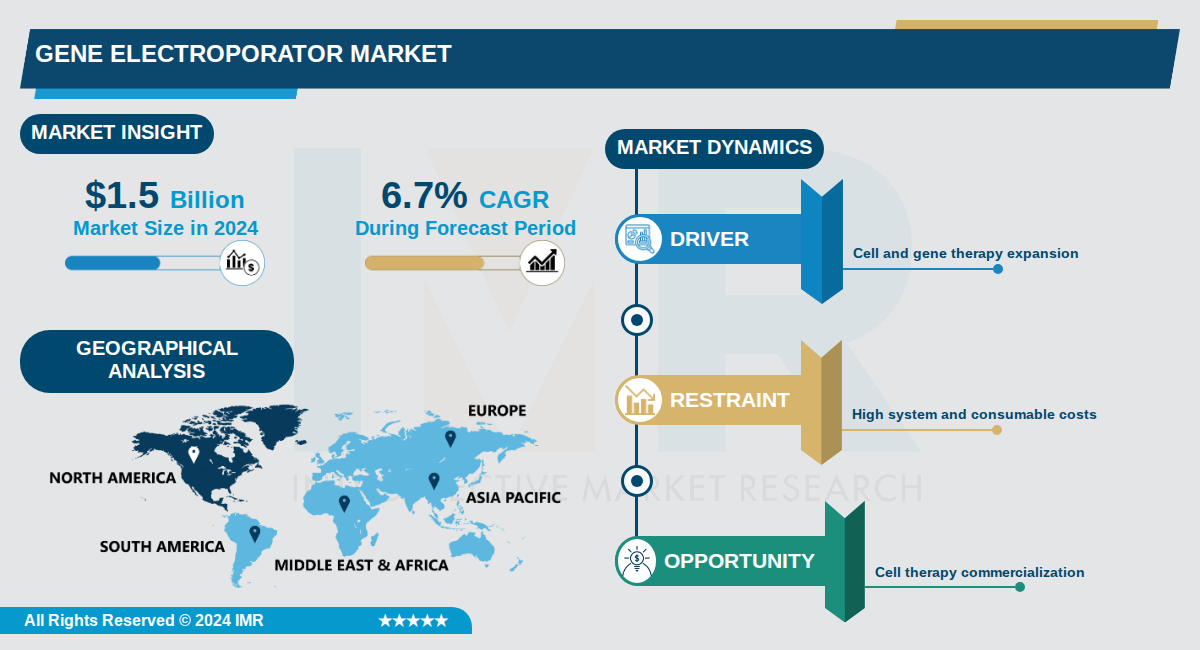

Gene Electroporator Market Size Was Valued at USD 1.5 Billion in 2024, and is Projected to Reach USD 3.0 Billion by 2035, Growing at a CAGR of 6.7% From 2024-2035.

The Gene Electroporator Market, valued at $1.5 billion in 2024, is projected to reach $3.0 billion by 2035, growing at a compound annual growth rate (CAGR) of 6.7%. This expansion reflects the increasing adoption of electroporation systems as a key non-viral gene delivery method in biotechnology and pharmaceutical applications.

Electroporation instruments, including electroporators, reagents, and electrodes, are essential for efficient transfection in gene therapy, cancer treatment, vaccine production, and protein production. The market is driven by demand for scalable, reproducible techniques that minimize cytotoxicity and support high-throughput workflows in clinical and research settings.

North America leads due to strong biotech presence and FDA support, while Asia-Pacific emerges as the fastest-growing region fueled by investments in China, South Korea, and India. Key end-users include biopharma companies, academic institutions, and CROs, with gene therapy applications showing the most rapid segment growth.

Gene Electroporator Market Trend Analysis:

Miniaturization and Automation of Electroporation Devices

- Companies like Bio-Rad have advanced this trend with the launch of the Gene Pulser Xcell Electroporation System in April 2022, featuring precise control over voltage and pulse duration for efficient transfection across diverse cell types including primary cells and stem cells. This system supports high-throughput screening in drug discovery, enabling researchers to process gene libraries and CRISPR-Cas9 constructs rapidly while minimizing manual intervention. Automation reduces procedure times and enhances reproducibility, addressing key limitations in traditional electroporation workflows.

- Thermo Fisher Scientific and Lonza are investing in miniaturized devices integrated with microfluidics, allowing portable use in point-of-care and in vivo applications outside standard labs. These innovations cut cell damage by optimizing pulse parameters, with reported transfection efficiencies exceeding 80% in hard-to-transfect cells like neurons. The shift supports scalability for immunotherapy production, where MaxCyte's flow electroporation systems process up to 25 billion cells per run for CAR-T therapies.

- Market projections reflect this trend's impact, with the global electroporator market growing from USD 0.43 billion in 2026 to USD 0.78 billion by 2035 at a 6.7% CAGR, driven by demand for automated high-throughput systems in pharmaceutical firms.

Rise of Specialized Systems for CRISPR and Immunotherapy

- Electroporation demand has surged with CRISPR-Cas9 adoption, where systems from Eppendorf and Nepa Gene Co. offer tailored pulse waveforms for gene editing in primary cells and stem cells, achieving over 90% knockout efficiency in T-cells. This specialization supports immunotherapy, with electroporation critical for CAR-T cell manufacturing used by companies like Novartis in Kymriah production. The trend aligns with gene therapy market expansion, projected to push electroporation revenues to $291.4 million by 2024 at 10.7% CAGR.

- Harvard Bioscience and BEX CO.LTD develop devices for specific applications like vaccine development, accelerated by COVID-19 needs where electroporation enabled rapid mRNA delivery testing. These systems minimize immunogenicity compared to viral vectors, facilitating scalable production for personalized medicine. North America's 45% market share, led by biotech hubs, underscores this trend with heavy R&D from firms like Merck.

- AngioDynamics and Mirus focus on in vivo electroporation for tumor treatments, combining electrodes with reagents to enhance DNA uptake by 5-fold, advancing electrochemotherapy clinical trials.

Expansion into High-Throughput and Portable Platforms

- Bio-Rad's automated electroporators enable high-throughput screening of thousands of CRISPR constructs daily, vital for functional genomics at pharmaceutical companies processing over 10,000 samples weekly. This trend boosts efficiency in drug discovery, with Lonza reporting 50% faster workflows using their Nucleofector platforms for biotech scale-up. Asia-Pacific's fastest growth at 20% market share reflects adoption by emerging players investing in these systems.

- Portable electroporators from Gel Company and Biotron Healthcare target field and clinical use, integrating nanoparticles for 70% improved transfection in vivo applications like wound healing therapies. Post-COVID innovations emphasize user-friendly designs, with North America dominating via startups innovating for remote lab access during pandemics.

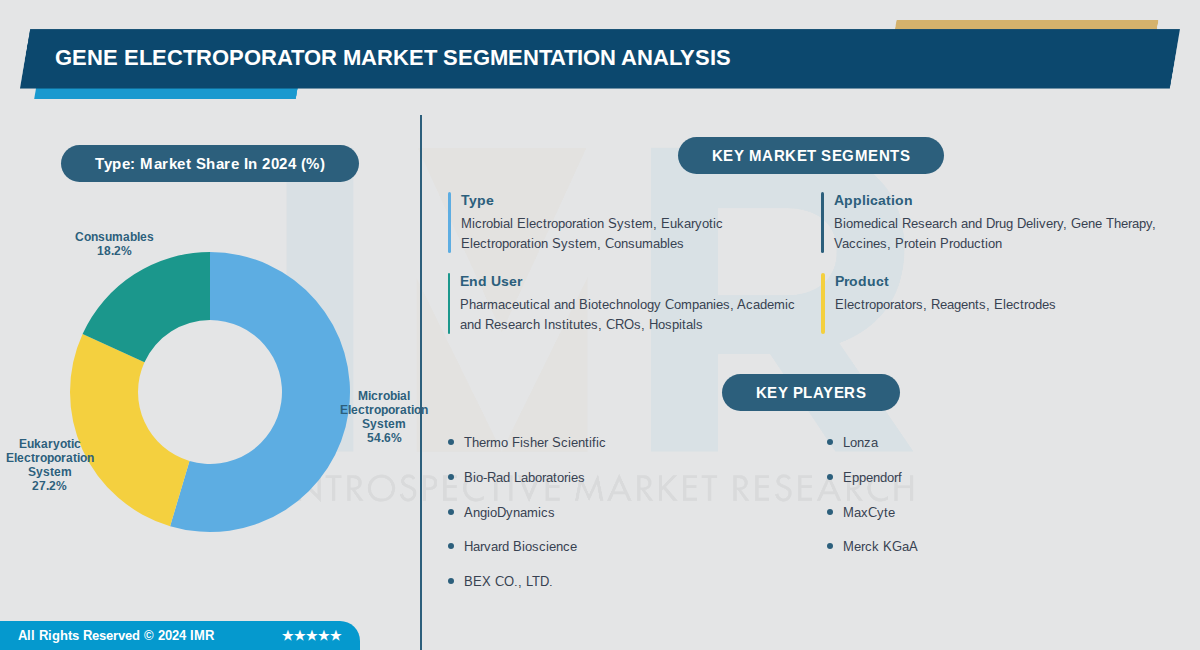

Gene Electroporator Market Segment Analysis:

Gene Electroporator Market is Segmented on the basis of By Type, By Application, By End User

By Type, Microbial Electroporation System segment is expected to dominate the market during the forecast period

- Microbial systems dominate due to high demand in genetic engineering for bacteria and yeast in vaccine development and protein production.

- Advancements in CRISPR and biopharmaceuticals drive over 50% market share as they require efficient microbial transfection.

By Application, Biomedical Research and Drug Delivery segment is expected to dominate the market during the forecast period

- Biomedical research leads from generating USD 65.6 million in 2023 revenue, fueled by R&D in life sciences and drug delivery systems.

- Regulatory approvals and clinical validations expand electroporation use across therapeutic areas, solidifying its top position.

By End User, Pharmaceutical and Biotechnology Companies segment is expected to dominate the market during the forecast period

- Pharma and biotech firms dominate due to heavy investments in gene therapy, CAR-T, and vaccine manufacturing pipelines.

- Presence of leaders like Thermo Fisher and Bio-Rad in these sectors drives adoption for scalable GMP-grade production.

By Product, Electroporators segment is expected to dominate the market during the forecast period

- Electroporators hold majority share as core instruments essential for all transfection protocols in research and clinical labs.

- Fastest growth in reagents complements devices, but hardware remains foundational for market expansion in biotech.

Gene Electroporator Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast Period

- North America dominates the gene electroporator market due to the presence of leading biotechnology and pharmaceutical companies, extensive academic and research institutions, and significant government funding for scientific research. Key countries like the U.S. and Canada drive this leadership through robust R&D ecosystems. This region holds the largest market share, approximately 45% in related electroporation technologies.

- The region benefits from well-established life sciences infrastructure, high R&D investments, and favorable regulations supporting biotechnology innovations. North America features advanced facilities for genetic engineering and high-throughput screening, boosting demand for electroporators. These factors create a mature market environment conducive to rapid adoption and growth.

- Major players such as Thermo Fisher Scientific, Bio-Rad, and AngioDynamics, all based in the U.S., lead the market with innovative products. Recent developments include Bio-Rad's Gene Pulser Xcell Electroporation System launched in April 2022, enhancing transfection efficiency for gene therapy and drug discovery. These advancements solidify North America's position through continuous industrial progress.

Active Key Players in the Gene Electroporator Market:

- Thermo Fisher Scientific (USA)

- Lonza (Switzerland)

- Bio-Rad Laboratories (USA)

- Eppendorf (Germany)

- AngioDynamics (USA)

- MaxCyte (USA)

- Harvard Bioscience (USA)

- Merck KGaA (Germany)

- BEX CO., LTD. (Japan)

- Nepa Gene Co., Ltd. (Japan)

- Mirus Bio LLC (USA)

- BTX (USA)

- Celetrix, LLC. (USA)

- Gamma Biosciences (USA)

- Altogen Biosystems (USA)

- Ala Scientific Instruments (USA)

- BioEra Life Sciences (India)

- Ichor Medical Systems (USA)

- Other Active Players

|

Gene Electroporator Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 1.5 Billion |

|

Forecast Period 2024-2035 CAGR: |

6.7 % |

Market Size in 2035: |

USD 3.0 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By End User |

|

||

|

By Product |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Gene Electroporator Market by Type (2017-2035)

4.1 Gene Electroporator Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Microbial Electroporation System

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Eukaryotic Electroporation System

4.5 Consumables

Chapter 5: Gene Electroporator Market by Application (2017-2035)

5.1 Gene Electroporator Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Biomedical Research and Drug Delivery

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Gene Therapy

5.5 Vaccines

5.6 Protein Production

Chapter 6: Gene Electroporator Market by End User (2017-2035)

6.1 Gene Electroporator Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Pharmaceutical and Biotechnology Companies

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Academic and Research Institutes

6.5 CROs

6.6 Hospitals

Chapter 7: Gene Electroporator Market by Product (2017-2035)

7.1 Gene Electroporator Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Electroporators

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Reagents

7.5 Electrodes

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Gene Electroporator Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 THERMO FISHER SCIENTIFIC

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 LONZA

8.4 BIO-RAD LABORATORIES

8.5 EPPENDORF

8.6 ANGIODYNAMICS

8.7 MAXCYTE

8.8 HARVARD BIOSCIENCE

8.9 MERCK KGAA

8.10 BEX CO.

8.11 LTD.

8.12 NEPA GENE CO.

8.13 LTD.

8.14 MIRUS BIO LLC

8.15 BTX

8.16 CELETRIX

8.17 LLC.

8.18 GAMMA BIOSCIENCES

8.19 ALTOGEN BIOSYSTEMS

8.20 ALA SCIENTIFIC INSTRUMENTS

8.21 BIOERA LIFE SCIENCES

8.22 ICHOR MEDICAL SYSTEMS

Chapter 9: Global Gene Electroporator Market By Region

9.1 Overview

9.2. North America Gene Electroporator Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Gene Electroporator Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Gene Electroporator Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Gene Electroporator Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Gene Electroporator Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Gene Electroporator Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Gene Electroporator Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 1.5 Billion |

|

Forecast Period 2024-2035 CAGR: |

6.7 % |

Market Size in 2035: |

USD 3.0 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By End User |

|

||

|

By Product |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||