Focal Segmental Glomerulosclerosis Market Synopsis

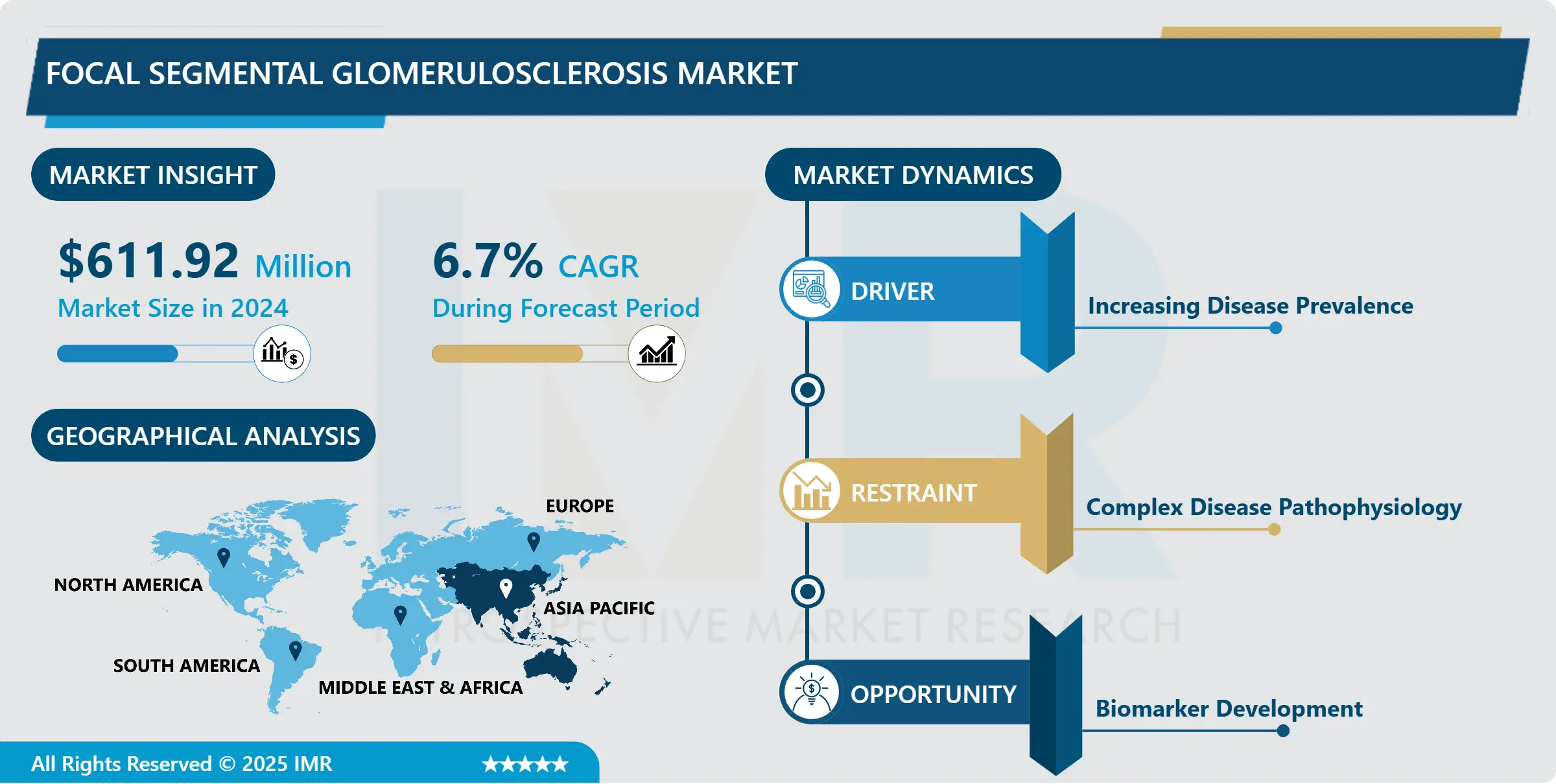

Focal Segmental Glomerulosclerosis Market Size Was Valued at USD 611.92 Million in 2024, and is Projected to Reach USD 1248.83 Million by 2035, Growing at a CAGR of 6.7% From 2025-2035.

Focal Segmental Glomerulosclerosis (FSGS) is a rare and serious kidney disorder characterized by scarring (sclerosis) in the kidney's glomeruli, the tiny structures responsible for filtering waste from the blood. This condition can lead to nephrotic syndrome, manifesting in proteinuria (excess protein in the urine), hypoalbuminemia (low levels of albumin in the blood), and edema (swelling). The FSGS market encompasses the pharmaceutical and biotechnological efforts to diagnose, treat, and manage the disease, focusing on developing novel therapies, improving existing treatments, and enhancing diagnostic techniques. This market includes a range of stakeholders such as drug manufacturers, healthcare providers, researchers, and patients, all aiming to mitigate the impact of FSGS on affected individuals.

The market for focal segmental glomerulosclerosis (FSGS) is expanding significantly because to a rise in the prevalence of the condition, improvements in diagnostic methods, and the creation of novel treatment alternatives. A portion of the glomeruli, which are microscopic structures inside the kidneys that filter waste and excess chemicals from the blood, have scarring (sclerosis) in FSGS, a rare kidney disease. If left untreated, this illness can result in significant kidney damage and, eventually, end-stage renal disease (ESRD).Globally, the incidence of FSGS is increasing, according to recent epidemiological studies, which is fueling the need for more efficient treatment alternatives. Better illness management has resulted from early diagnosis and intervention due to growing awareness of the disease among patients and healthcare providers. The accuracy of the FSGS diagnosis has increased due to advancements in diagnostic techniques, such as the use of genetic testing and biopsy techniques, opening the door to more individualized treatment plans.

Extensive research and development (R&D) efforts to decipher the intricate pathophysiology of FSGS and pinpoint viable treatment targets are driving the market. Research institutes and pharmaceutical corporations are making significant investments in the creation of innovative medications and biologics intended to stop or reverse the course of the illness. New medicines are predicted to greatly improve the therapeutic landscape. One such treatment is targeted therapy, which targets the underlying causes of FSGS. These medications are demonstrating promise in clinical trials.

To expedite the research and marketing of novel treatments, major companies in the FSGS market are concentrating on strategic alliances and collaborations. These partnerships frequently entail the pooling of knowledge, assets, and technological know-how, which can spur quicker innovation and wider market penetration. Furthermore, regulatory agencies are realizing how urgently effective FSGS medicines are needed, which is accelerating review procedures and perhaps approving products for the market.

Even with the bright future, the FSGS market still has a number of obstacles to overcome. Patients and healthcare systems are severely impacted by the high expense of therapy, especially new medicines. Comprehensive clinical trials are also required to guarantee safety and efficacy due to the strict regulatory environment for new drug approvals, which can be expensive and time-consuming. However, the market's potential is still considerable due to ongoing clinical trials and the potential for ground-breaking treatments that could change the way FSGS sufferers are treated.In conclusion, rising illness prevalence, improvements in diagnosis and treatment, and substantial R&D spending are all contributing to the FSGS market's anticipated rapid expansion. The market's future is bright due to the potential introduction of novel medicines that could significantly enhance patient outcomes and quality of life, even in the face of persistent constraints including high treatment costs and regulatory barriers.

Focal Segmental Glomerulosclerosis Market Trend Analysis

Innovative Therapies and Drug Development in the FSGS Market

- Novel treatments targeted at meeting patients' unmet medical requirements are proliferating in the FSGS market. To develop new treatments, pharmaceutical companies are making significant investments in research and development (R&D). At the forefront of this study are biologic agents, such monoclonal antibodies, and small molecule inhibitors. Drugs that address the underlying pathophysiology of FSGS are notable developments since they attempt to provide disease-modifying effects instead of only symptomatic alleviation.

- A potentially effective class of biologic medicines being investigated for the treatment of FSGS is monoclonal antibodies (mAbs). These antibodies are made to specifically target proteins that are implicated in the pathogenesis of the disease. Targeting suPAR (soluble urokinase-type plasminogen activator receptor), a molecule linked to the pathophysiology of FSGS, for example, has demonstrated promise in lowering proteinuria and delaying the course of the illness. Similarly, mAbs that target CD20, a protein on the surface of B-cells, are being investigated for their potential to modify the immune response associated with FSGS patients' glomerular damage.

- An essential area of research for FSGS medication development is small molecule inhibitors. These substances have the ability to specifically target important disease-related signaling pathways. For instance, researchers are looking into inhibitors of the APOL1 gene variants, which are highly linked to FSGS in people of African heritage. These medications try to avoid kidney injury by selectively blocking the harmful variations of this gene. To further safeguard these vital kidney filtering unit cells, inhibitors of the TRPC5 ion channel, which is implicated in podocyte survival and function, are being developed.

- The emphasis on treatments that alter disease signifies a substantial departure from conventional methods that mainly treat symptoms. By addressing the underlying causes of FSGS, these innovative treatments hope to slow or even reverse the course of the illness. Drugs that target fibrotic pathways, for instance, aim to lessen or stop glomerular scarring, which is a defining feature of FSGS. By lowering the need for procedures like kidney transplantation or dialysis, this strategy not only promises to improve kidney function but also improve patients' quality of life. The creation of these treatments demonstrates the pharmaceutical industry's dedication to advancing care alternatives that provide FSGS patients with long-term advantages.

Increased Focus on Precision Medicine in the FSGS Market

- The FSGS industry is seeing a notable upsurge in precision medicine, mainly because of the expanding knowledge that multiple genetic and molecular processes can give rise to FSGS. This method customizes medical care to each patient's unique needs, taking into account their lifestyle, genetic composition, and environmental influences. This entails identifying certain genetic alterations and molecular mechanisms that underlie FSGS in order to facilitate more focused and efficient therapies. The management of FSGS may change as a result of precision medicine, which could pave the door for more individualized and possibly curative treatments.

- Precision medicine in FSGS is primarily based on genomics advancements and biomarker identification. The NPHS2, WT1, and APOL1 gene mutations, among other genetic variants linked to FSGS, can now be identified thanks to genome sequencing methods. These findings allow the genetic profiles of FSGS to be classified into discrete categories. Furthermore, biomarkers reflecting disease activity or progression are being developed to facilitate early diagnosis and track response to treatment. With the help of this accurate classification, physicians may customize treatment plans to the unique FSGS subtype, enhancing therapeutic results and reducing unneeded side effects.

- It is anticipated that the move to more individualized treatment plans will greatly increase the effectiveness of FSGS medicines and boost patient outcomes. Precision medicine aims to address the underlying genetic and molecular causes of the disease in order to provide more effective interventions that may have fewer side effects. For example, treatments that precisely block the pathogenic consequences of APOL1 gene variations may be beneficial for patients with APOL1-related FSGS. In a similar vein, individuals with immune-mediated FSGS might benefit more from therapies that alter particular immune pathways. By providing patients with more precise prognoses and personalized care plans, this customized approach not only increases the likelihood that their treatments will be successful but also improves their quality of life and long-term health outcomes.

Focal Segmental Glomerulosclerosis Market Segment Analysis:

Focal Segmental Glomerulosclerosis Market Segmented based on By Diseases Type and By Disease Management.

By Diseases Type, Primary focal segmental Glomerulosclerosis segment is expected to dominate the market during the forecast period

- Of all the glomerular disorders, primary focal segmental glomerulosclerosis (FSGS) is unique in that it is a complex and mysterious condition. Since primary FSGS frequently manifests without a known cause, it is classified as idiopathic, in contrast to several other renal disorders with well-established etiologies. This intricacy highlights the difficulty of accurately diagnosing and treating the illness. The damage done to the kidneys' fragile glomeruli—the filtering units—is the distinguishing feature of primary FSGS. These units develop sclerosis, or scar tissue, as a result of the damage, which makes it more difficult for them to remove waste from the blood. Proteinuria, or the leaking of protein into the urine, consequently develops and further complicates the progression of the illness. Primary FSGS necessitates a thorough and specialized approach to management due to its complex pathology, comprising a multidisciplinary team of nephrologists, pathologists, and other healthcare specialists.

- Furthermore, the unrelenting advancement of main FSGS highlights its noteworthy influence on individual patients as well as the larger healthcare system. Primary FSGS often progresses to end-stage renal disease (ESRD), a critical stage where kidney function is significantly reduced and requires life-sustaining therapies like dialysis or kidney transplantation, if timely and targeted care is not provided. This course of events not only presents significant obstacles to the well-being of patients but also places a significant burden on healthcare resources. The complex interaction of immunological dysregulation, environmental variables, and genetic predisposition adds layers of complexity to the disease's pathophysiology, which motivates ongoing research efforts to solve its mysteries. Consequently, primary FSGS plays a pivotal role in medical research and clinical practice by propelling innovation in therapeutic approaches, patient care regimens, and diagnostic methods. The significant clinical significance of this phenomenon highlights the pressing necessity for ongoing study and collaboration in order to enhance the outcomes for impacted individuals and mitigate the strain on global healthcare systems.

By Disease Management, Diagnosis (Creatinine Test ) segment held the largest share in 2023

- A key component of kidney function assessment, the creatinine test is essential for both initial screenings and continuous renal health monitoring. Its non-invasiveness and capacity to provide insightful information on the glomerular filtration rate (GFR), a crucial measure of kidney function, account for its widespread use. The waste product creatinine is produced during muscle metabolism and is eliminated from the blood by the kidneys at a steady pace into the urine. Raised blood creatinine levels are a sign of impaired kidney function because the impaired kidneys have a harder time eliminating this waste product from the body. As a result, the creatinine test is a crucial diagnostic tool for kidney dysfunction since it may be used to quickly detect the early indicators of the condition and take action to prevent further decline.

- Moreover, the function of the creatinine test goes beyond simple detection to include clinical decision support and the incitement of additional diagnostic testing. When renal function is compromised due to elevated creatinine levels, medical professionals may choose to do further tests, such as kidney biopsies, in order to determine the underlying reason of renal dysfunction. For the purpose of correctly detecting diseases such as primary focal segmental glomerulosclerosis (FSGS) and starting treatment plans that are customized for each patient, this diagnostic cascade is essential. Because of its accessibility and dependability, the creatinine test therefore plays a significant role in the diagnostic process. It also acts as a starting point for more thorough assessments, which makes it easier to implement prompt therapies meant to maintain kidney function and improve patient outcomes.

Focal Segmental Glomerulosclerosis Market Regional Insights:

Asia-Pacific is Expected to Dominate the Market Over the Forecast period

- The Asia-Pacific region is emerging as a dominant force in the Focal Segmental Glomerulosclerosis (FSGS) market, propelled by several critical factors. One of the primary drivers is the significant increase in healthcare expenditure across the region. Governments in countries like China, India, and Japan are heavily investing in healthcare infrastructure, aiming to provide better access to medical services and improve the overall quality of care. These investments are not only enhancing existing facilities but also facilitating the establishment of advanced diagnostic and treatment centers. This expansion in healthcare infrastructure is crucial for addressing the rising prevalence of chronic kidney diseases, including FSGS, as it enables earlier diagnosis and more effective treatment options.

- China, India, and Japan stand at the forefront of this market growth, largely due to their substantial populations and the corresponding high incidence rates of diabetes and hypertension, which are significant risk factors for FSGS. In China, the rapid urbanization and lifestyle changes have led to an increase in non-communicable diseases, including those affecting the kidneys. Similarly, India faces a growing burden of diabetes and hypertension, contributing to a higher incidence of kidney diseases. Japan, with its aging population, is also seeing a rise in chronic kidney conditions. These countries are making concerted efforts to address these health challenges through public health initiatives and healthcare reforms. Government initiatives aimed at improving healthcare access and quality are crucial in driving the FSGS market. For instance, national health policies focusing on the prevention and management of chronic diseases play a pivotal role in creating awareness and facilitating early intervention.

- Furthermore, the Asia-Pacific region is benefiting from rising investments in biotechnology and medical research. Both private and public sectors are channeling significant funds into research and development, fostering innovation in diagnostic technologies and treatment methodologies. This is leading to the development of more effective and precise diagnostic tools, which are essential for early detection and management of FSGS. The large patient pool in the region provides a substantial market for these innovations. Additionally, increased awareness about kidney health through educational campaigns and public health programs is encouraging people to seek medical advice earlier, thereby improving outcomes for FSGS patients. The convergence of these factors—improved healthcare infrastructure, a large patient population, and advancements in medical technology—positions the Asia-Pacific region as a dominant player in the global FSGS market, with robust growth prospects in the coming years.

Active Key Players in the Focal Segmental Glomerulosclerosis Market

- Variant Pharmaceuticals, Inc.

- ChemoCentryx, Inc.

- Travere Therapeutics

- AbbVie, Inc.

- Novartis AG

- Pfizer, Inc.

- AstraZeneca plc.

- Sanofi S.A.

- GlaxoSmithKline plc.

- Teva Pharmaceutical Industries Ltd.

- Other Key Players

Key Industry Developments in the Focal Segmental Glomerulosclerosis Market:

- In May 2022, Travere Therapeutics announced that the U.S. Food and Drug Administration (FDA) had granted accelerated approval to FILSPARI (sparsentan) to reduce proteinuria in adults with primary IgAN at risk of rapid disease progression

|

Focal Segmental Glomerulosclerosis Market |

|||

|

Base Year: |

2025 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 611.92 Mn. |

|

Forecast Period 2025-35 CAGR: |

6.7% |

Market Size in 2035: |

USD 1248.83 Mn. |

|

Segments Covered: |

By Diseases Type |

|

|

|

By Disease Management |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Focal Segmental Glomerulosclerosis Market by Diseases Type (2018-2035)

4.1 Focal Segmental Glomerulosclerosis Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Primary focal segmental Glomerulosclerosis

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Secondary focal segmental Glomerulosclerosis

Chapter 5: Focal Segmental Glomerulosclerosis Market by Disease Management (2018-2035)

5.1 Focal Segmental Glomerulosclerosis Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Diagnosis

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Kidney Biopsy

5.5 Creatinine Test

5.6 Others

5.7 Treatment

5.8 Drug Therapy

5.9 Dialysis

5.10 Kidney Transplant

Chapter 6: Company Profiles and Competitive Analysis

6.1 Competitive Landscape

6.1.1 Competitive Benchmarking

6.1.2 Focal Segmental Glomerulosclerosis Market Share by Manufacturer (2024)

6.1.3 Industry BCG Matrix

6.1.4 Heat Map Analysis

6.1.5 Mergers and Acquisitions

6.2 VARIANT PHARMACEUTICALS INCCHEMOCENTRYX INCTRAVERE THERAPEUTICS

6.2.1 Company Overview

6.2.2 Key Executives

6.2.3 Company Snapshot

6.2.4 Role of the Company in the Market

6.2.5 Sustainability and Social Responsibility

6.2.6 Operating Business Segments

6.2.7 Product Portfolio

6.2.8 Business Performance

6.2.9 Key Strategic Moves and Recent Developments

6.2.10 SWOT Analysis

6.3 ABBVIE INCNOVARTIS AG

6.4 PFIZER INCASTRAZENECA PLCSANOFI S.AGLAXOSMITHKLINE PLCTEVA PHARMACEUTICAL INDUSTRIES LTDOTHER KEY PLAYERS

Chapter 7: Global Focal Segmental Glomerulosclerosis Market By Region

7.1 Overview

7.2. North America Focal Segmental Glomerulosclerosis Market

7.2.1 Key Market Trends, Growth Factors and Opportunities

7.2.2 Top Key Companies

7.2.3 Historic and Forecasted Market Size by Segments

7.2.4 Historic and Forecasted Market Size by Diseases Type

7.2.4.1 Primary focal segmental Glomerulosclerosis

7.2.4.2 Secondary focal segmental Glomerulosclerosis

7.2.5 Historic and Forecasted Market Size by Disease Management

7.2.5.1 Diagnosis

7.2.5.2 Kidney Biopsy

7.2.5.3 Creatinine Test

7.2.5.4 Others

7.2.5.5 Treatment

7.2.5.6 Drug Therapy

7.2.5.7 Dialysis

7.2.5.8 Kidney Transplant

7.2.6 Historic and Forecast Market Size by Country

7.2.6.1 US

7.2.6.2 Canada

7.2.6.3 Mexico

7.3. Eastern Europe Focal Segmental Glomerulosclerosis Market

7.3.1 Key Market Trends, Growth Factors and Opportunities

7.3.2 Top Key Companies

7.3.3 Historic and Forecasted Market Size by Segments

7.3.4 Historic and Forecasted Market Size by Diseases Type

7.3.4.1 Primary focal segmental Glomerulosclerosis

7.3.4.2 Secondary focal segmental Glomerulosclerosis

7.3.5 Historic and Forecasted Market Size by Disease Management

7.3.5.1 Diagnosis

7.3.5.2 Kidney Biopsy

7.3.5.3 Creatinine Test

7.3.5.4 Others

7.3.5.5 Treatment

7.3.5.6 Drug Therapy

7.3.5.7 Dialysis

7.3.5.8 Kidney Transplant

7.3.6 Historic and Forecast Market Size by Country

7.3.6.1 Russia

7.3.6.2 Bulgaria

7.3.6.3 The Czech Republic

7.3.6.4 Hungary

7.3.6.5 Poland

7.3.6.6 Romania

7.3.6.7 Rest of Eastern Europe

7.4. Western Europe Focal Segmental Glomerulosclerosis Market

7.4.1 Key Market Trends, Growth Factors and Opportunities

7.4.2 Top Key Companies

7.4.3 Historic and Forecasted Market Size by Segments

7.4.4 Historic and Forecasted Market Size by Diseases Type

7.4.4.1 Primary focal segmental Glomerulosclerosis

7.4.4.2 Secondary focal segmental Glomerulosclerosis

7.4.5 Historic and Forecasted Market Size by Disease Management

7.4.5.1 Diagnosis

7.4.5.2 Kidney Biopsy

7.4.5.3 Creatinine Test

7.4.5.4 Others

7.4.5.5 Treatment

7.4.5.6 Drug Therapy

7.4.5.7 Dialysis

7.4.5.8 Kidney Transplant

7.4.6 Historic and Forecast Market Size by Country

7.4.6.1 Germany

7.4.6.2 UK

7.4.6.3 France

7.4.6.4 The Netherlands

7.4.6.5 Italy

7.4.6.6 Spain

7.4.6.7 Rest of Western Europe

7.5. Asia Pacific Focal Segmental Glomerulosclerosis Market

7.5.1 Key Market Trends, Growth Factors and Opportunities

7.5.2 Top Key Companies

7.5.3 Historic and Forecasted Market Size by Segments

7.5.4 Historic and Forecasted Market Size by Diseases Type

7.5.4.1 Primary focal segmental Glomerulosclerosis

7.5.4.2 Secondary focal segmental Glomerulosclerosis

7.5.5 Historic and Forecasted Market Size by Disease Management

7.5.5.1 Diagnosis

7.5.5.2 Kidney Biopsy

7.5.5.3 Creatinine Test

7.5.5.4 Others

7.5.5.5 Treatment

7.5.5.6 Drug Therapy

7.5.5.7 Dialysis

7.5.5.8 Kidney Transplant

7.5.6 Historic and Forecast Market Size by Country

7.5.6.1 China

7.5.6.2 India

7.5.6.3 Japan

7.5.6.4 South Korea

7.5.6.5 Malaysia

7.5.6.6 Thailand

7.5.6.7 Vietnam

7.5.6.8 The Philippines

7.5.6.9 Australia

7.5.6.10 New Zealand

7.5.6.11 Rest of APAC

7.6. Middle East & Africa Focal Segmental Glomerulosclerosis Market

7.6.1 Key Market Trends, Growth Factors and Opportunities

7.6.2 Top Key Companies

7.6.3 Historic and Forecasted Market Size by Segments

7.6.4 Historic and Forecasted Market Size by Diseases Type

7.6.4.1 Primary focal segmental Glomerulosclerosis

7.6.4.2 Secondary focal segmental Glomerulosclerosis

7.6.5 Historic and Forecasted Market Size by Disease Management

7.6.5.1 Diagnosis

7.6.5.2 Kidney Biopsy

7.6.5.3 Creatinine Test

7.6.5.4 Others

7.6.5.5 Treatment

7.6.5.6 Drug Therapy

7.6.5.7 Dialysis

7.6.5.8 Kidney Transplant

7.6.6 Historic and Forecast Market Size by Country

7.6.6.1 Turkiye

7.6.6.2 Bahrain

7.6.6.3 Kuwait

7.6.6.4 Saudi Arabia

7.6.6.5 Qatar

7.6.6.6 UAE

7.6.6.7 Israel

7.6.6.8 South Africa

7.7. South America Focal Segmental Glomerulosclerosis Market

7.7.1 Key Market Trends, Growth Factors and Opportunities

7.7.2 Top Key Companies

7.7.3 Historic and Forecasted Market Size by Segments

7.7.4 Historic and Forecasted Market Size by Diseases Type

7.7.4.1 Primary focal segmental Glomerulosclerosis

7.7.4.2 Secondary focal segmental Glomerulosclerosis

7.7.5 Historic and Forecasted Market Size by Disease Management

7.7.5.1 Diagnosis

7.7.5.2 Kidney Biopsy

7.7.5.3 Creatinine Test

7.7.5.4 Others

7.7.5.5 Treatment

7.7.5.6 Drug Therapy

7.7.5.7 Dialysis

7.7.5.8 Kidney Transplant

7.7.6 Historic and Forecast Market Size by Country

7.7.6.1 Brazil

7.7.6.2 Argentina

7.7.6.3 Rest of SA

Chapter 8 Analyst Viewpoint and Conclusion

8.1 Recommendations and Concluding Analysis

8.2 Potential Market Strategies

Chapter 9 Research Methodology

9.1 Research Process

9.2 Primary Research

9.3 Secondary Research

|

Focal Segmental Glomerulosclerosis Market |

|||

|

Base Year: |

2025 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 611.92 Mn. |

|

Forecast Period 2025-35 CAGR: |

6.7% |

Market Size in 2035: |

USD 1248.83 Mn. |

|

Segments Covered: |

By Diseases Type |

|

|

|

By Disease Management |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||