Electroplating Market Synopsis:

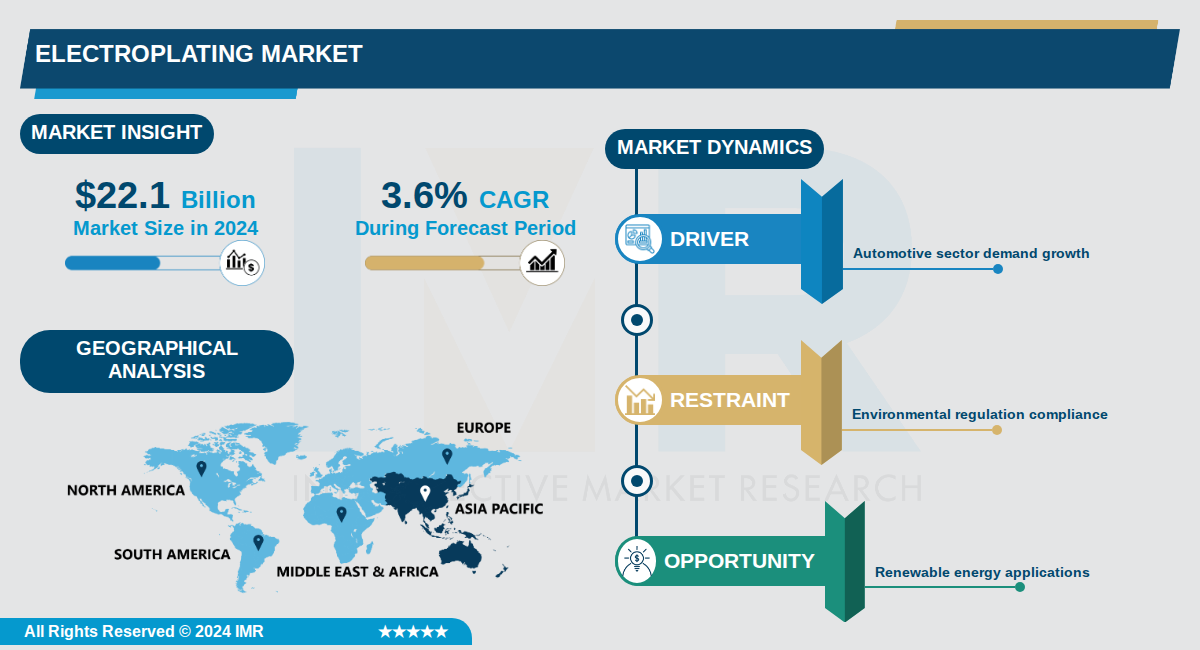

Electroplating Market Size Was Valued at USD 22.1 Billion in 2024, and is Projected to Reach USD 32.7 Billion by 2035, Growing at a CAGR of 3.6% From 2024-2035.

The global electroplating market, valued at $22.1 billion in 2024, is projected to reach $32.7 billion by 2035, growing at a compound annual growth rate (CAGR) of 3.6%. Electroplating, a process of depositing a metal coating on a surface to enhance properties like corrosion resistance, conductivity, and aesthetics, serves critical roles across multiple industries including automotive, electronics, aerospace, and consumer goods.

Key end-user sectors driving demand include automotive, where electroplating improves durability and visual appeal of components like bumpers and trims, and electronics, essential for printed circuit boards, semiconductors, and connectors to boost performance and longevity. Asia Pacific dominates the market due to robust manufacturing in electronics and automotive sectors in countries like China, India, Japan, and South Korea, while North America exhibits the fastest growth fueled by advancements in aerospace and high-performance applications.

Market trends highlight a shift toward green technologies, such as low-toxicity electrolytes, water-saving systems, and resource-efficient processes, alongside rising demand for customized coatings offering specialized properties like enhanced wear resistance. Innovations like pulse plating and nanotechnology further improve efficiency, supporting steady global expansion amid industrialization and regulatory pressures.

Electroplating Market Trend Analysis:

Shift to Trivalent Chromium Plating

- Major electroplating companies are rapidly replacing toxic hexavalent chromium with trivalent chromium alternatives due to global regulations like REACH in Europe, which banned hexavalent forms in 2023. This shift reduces environmental hazards while maintaining corrosion resistance for automotive and aerospace parts. For instance, Atotech, now part of MKS Instruments, invested heavily in trivalent chromium baths that achieve 95% of hexavalent performance at lower costs.

- Trivalent processes consume 30-40% less energy and produce non-hazardous waste, enabling firms like MacDermid Enthone to secure contracts with EV makers such as Tesla for battery connectors. Wastewater treatment integration cuts disposal costs by 50%, boosting adoption in high-volume electronics manufacturing. Market projections show trivalent chromium capturing 60% of decorative plating by 2026.

- Customization for specific alloys like zinc-nickel trivalent coatings enhances wear resistance by 25% for machinery parts, as seen in partnerships between DuPont and industrial equipment suppliers.

Adoption of Nanotechnology in Coatings

- Nanostructured electroplating coatings with particle sizes under 100nm deliver 2-3 times higher hardness and conductivity than traditional layers, transforming electronics components like PCB connectors. In 2022, advancements by companies such as Technic Inc. enabled nano-gold coatings for 5G antennas, improving signal integrity by 40% and reducing power loss. These coatings are critical for IoT devices, where over 75 billion units are expected by 2025.

- Automotive applications include nano-nickel composites on EV chassis parts from suppliers like Rio Grande Co., extending lifespan against corrosion by 50% in harsh conditions. The technology also cuts material usage by 20%, aligning with cost pressures in mass production. Electronics giants like Samsung integrate these for semiconductor packaging to meet miniaturization demands.

- Nano-coatings enable antimicrobial properties for medical devices, with firms like Umicore developing silver nanoparticle platings that kill 99.9% of bacteria on surgical tools.

Integration of Industry 4.0 and Smart Automation

- Electroplating lines now feature IoT sensors, AI algorithms, and robotics for real-time monitoring of bath chemistry and deposition rates, reducing defects by 35% as implemented by ProPlate in automotive plants. In 2021, General Motors adopted these systems for EV component plating, achieving 20% higher throughput and full traceability via blockchain-integrated data logs. Pulse plating technology within these setups uses AI to optimize current pulses, saving 25% energy.

- AI-driven predictive maintenance cuts downtime by 40% for rack plating systems, with companies like Covent Ya partnering with Siemens for fully automated lines handling 10,000 parts per hour. This supports the electronics boom, where 5G rollout demands uniform coatings on billions of connectors annually. Wastewater recycling rates exceed 90% through automated closed-loop controls.

- Smart plating adapts to complex geometries in additive-manufactured parts, as pioneered by 360iResearch-highlighted innovations for aerospace firms like Boeing.

Electroplating Market Segment Analysis:

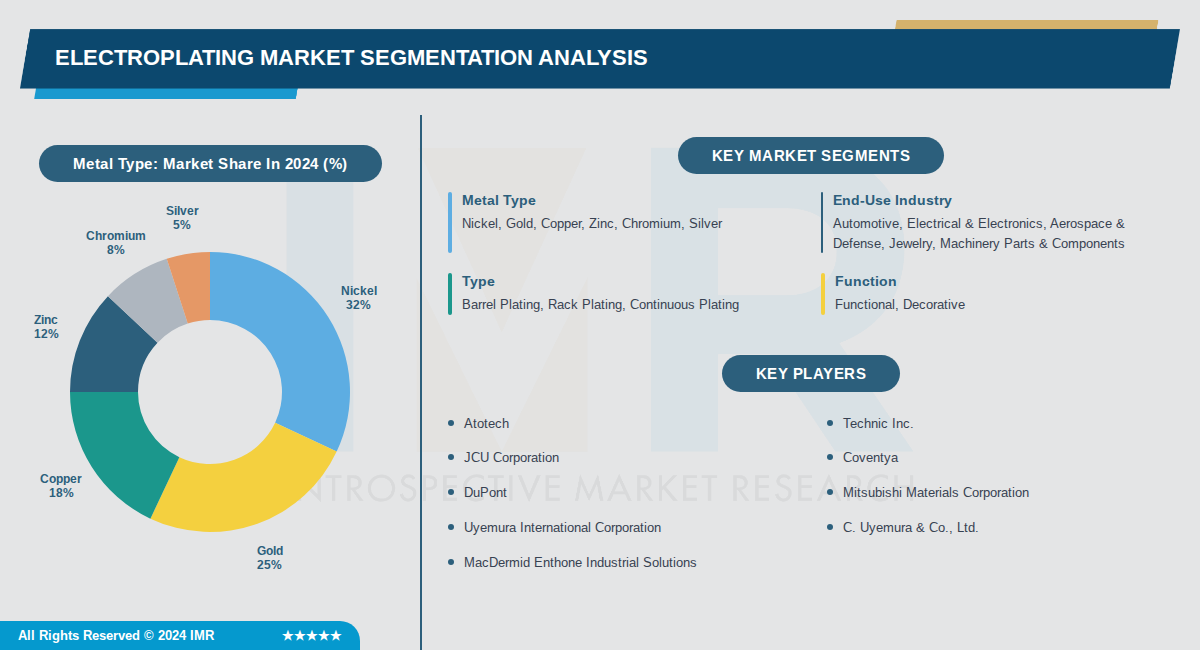

Electroplating Market is Segmented on the basis of By Metal Type, By End-Use Industry, By Type

By Metal Type, Nickel segment is expected to dominate the market during the forecast period

- Nickel plating dominates due to its exceptional corrosion resistance and versatility across automotive fasteners, aerospace landing gear, and electronic connectors.

- It provides superior wear protection in high-stress applications, driving its 32% market share amid rising EV and machinery demands.

By End-Use Industry, Automotive segment is expected to dominate the market during the forecast period

- Automotive leads due to extensive use in components for corrosion and wear protection, especially zinc-nickel plating in EVs and high-heat parts.

- Expanding global vehicle production, including EVs, fuels demand for durable electroplated finishes in chassis, engines, and trim.

By Type, Barrel Plating segment is expected to dominate the market during the forecast period

- Barrel plating holds the largest share for its cost-efficiency in high-volume processing of small parts like fasteners and electronics components.

- It enables uniform coating on bulk items, suiting the scale of automotive and machinery manufacturing demands.

By Function, Functional segment is expected to dominate the market during the forecast period

- Functional electroplating dominates for essential properties like corrosion resistance, wear protection, and conductivity in industrial applications.

- Rising needs in automotive, aerospace, and electronics for performance-enhancing coatings drive its overwhelming market leadership.

Electroplating Market Regional Insights:

Asia-Pacific Dominates the Electroplating Market

- Asia-Pacific leads the global electroplating market due to its massive manufacturing scale in key countries like China, India, Japan, and South Korea. These nations drive high demand from electronics, automotive, and consumer goods sectors, with China alone hosting extensive production hubs in regions like the Yangtze River Delta and Pearl River Delta. The region's share exceeded 47% in recent years, fueled by rapid industrialization and supply chain centrality.

- Robust infrastructure supports just-in-time delivery through concentrated production clusters in Guangdong and Jiangsu provinces, complemented by government initiatives, investments, and relatively favorable regulations. Emerging shifts to inland facilities prioritize cleaner energy and skilled labor amid sustainability pushes, while Southeast Asian countries like Vietnam, Thailand, and Malaysia emerge as cost-competitive hubs with tightening environmental standards. This infrastructure edge sustains Asia-Pacific's market leadership over the forecast period.

- Major players thrive in integrated supply chains linking raw materials to end-users, with heavy R&D investments in eco-friendly plating solutions like cyanide-free intermediates. Recent developments include China's expansion of specialist electroplating parks to 162 by 2023, supported by provincial grants for wastewater recycling, alongside relocating electronics manufacturing boosting demand in Southeast Asia. These innovations position regional leaders at the forefront of global advancements.

Active Key Players in the Electroplating Market:

- Atotech (Germany)

- Technic Inc. (USA)

- JCU Corporation (Japan)

- Coventya (France)

- DuPont (USA)

- Mitsubishi Materials Corporation (Japan)

- Uyemura International Corporation (Japan)

- C. Uyemura & Co., Ltd. (Japan)

- MacDermid Enthone Industrial Solutions (USA)

- BASF SE (Germany)

- Sharretts Plating Company (USA)

- Precision Plating Co. (USA)

- Pioneer Metal Finishing LLC (USA)

- Chemetall GmbH (Germany)

- Dr.-Ing. Max Schlötter GmbH & Co. KG (Germany)

- TOHO ZINC CO., LTD (Japan)

- Sheen Electroplaters Pvt Ltd (India)

- Summit Corporation of America (USA)

- Kuntz Electroplating Inc. (Canada)

- Other Active Players

|

Electroplating Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 22.1 Billion |

|

Forecast Period 2024-2035 CAGR: |

3.6 % |

Market Size in 2035: |

USD 32.7 Billion |

|

Segments Covered: |

By Metal Type |

|

|

|

By End-Use Industry |

|

||

|

By Type |

|

||

|

By Function |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Electroplating Market by Metal Type (2017-2035)

4.1 Electroplating Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Nickel

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Gold

4.5 Copper

4.6 Zinc

4.7 Chromium

4.8 Silver

Chapter 5: Electroplating Market by End-Use Industry (2017-2035)

5.1 Electroplating Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Automotive

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Electrical & Electronics

5.5 Aerospace & Defense

5.6 Jewelry

5.7 Machinery Parts & Components

Chapter 6: Electroplating Market by Type (2017-2035)

6.1 Electroplating Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Barrel Plating

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Rack Plating

6.5 Continuous Plating

Chapter 7: Electroplating Market by Function (2017-2035)

7.1 Electroplating Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Functional

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Decorative

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Electroplating Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 ATOTECH

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 TECHNIC INC.

8.4 JCU CORPORATION

8.5 COVENTYA

8.6 DUPONT

8.7 MITSUBISHI MATERIALS CORPORATION

8.8 UYEMURA INTERNATIONAL CORPORATION

8.9 C. UYEMURA & CO.

8.10 LTD.

8.11 MACDERMID ENTHONE INDUSTRIAL SOLUTIONS

8.12 BASF SE

8.13 SHARRETTS PLATING COMPANY

8.14 PRECISION PLATING CO.

8.15 PIONEER METAL FINISHING LLC

8.16 CHEMETALL GMBH

8.17 DR.-ING. MAX SCHLÖTTER GMBH & CO. KG

8.18 TOHO ZINC CO.

8.19 LTD

8.20 SHEEN ELECTROPLATERS PVT LTD

8.21 SUMMIT CORPORATION OF AMERICA

8.22 KUNTZ ELECTROPLATING INC.

Chapter 9: Global Electroplating Market By Region

9.1 Overview

9.2. North America Electroplating Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Electroplating Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Electroplating Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Electroplating Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Electroplating Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Electroplating Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Electroplating Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 22.1 Billion |

|

Forecast Period 2024-2035 CAGR: |

3.6 % |

Market Size in 2035: |

USD 32.7 Billion |

|

Segments Covered: |

By Metal Type |

|

|

|

By End-Use Industry |

|

||

|

By Type |

|

||

|

By Function |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||