Electronic Adhesives Market Synopsis:

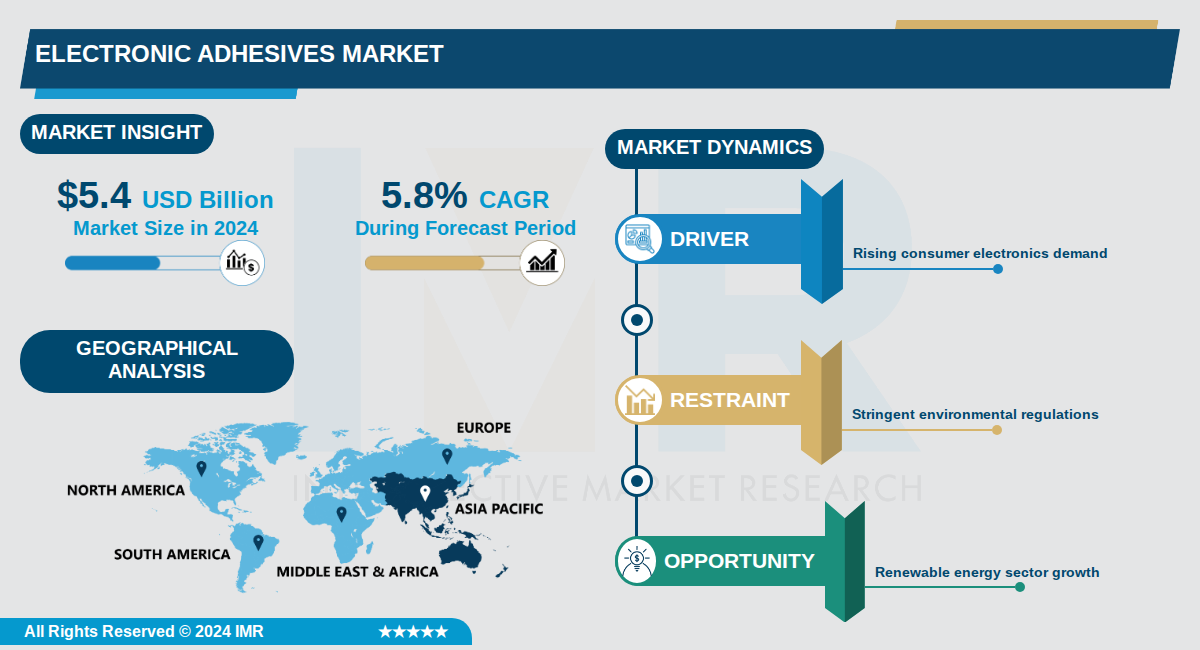

Electronic Adhesives Market Size Was Valued at USD 5.4 Billion in 2024, and is Projected to Reach USD 9.5 Billion by 2035, Growing at a CAGR of 5.8% From 2024-2035.

The global electronic adhesives market was valued at approximately $5.4-5.68 billion in 2024 and is projected to reach $9.5-13.69 billion by 2034-2035, representing compound annual growth rates (CAGR) between 5.8% and 9.2%. Electronic adhesives are essential materials used for bonding electronic components to printed circuit boards (PCBs), encapsulating semiconductors, and securing sensitive electronic assemblies across diverse industries including consumer electronics, automotive, medical, aerospace, and industrial applications. These adhesives enable surface mounting of components and provide critical functionality in miniaturized and high-performance electronic devices.

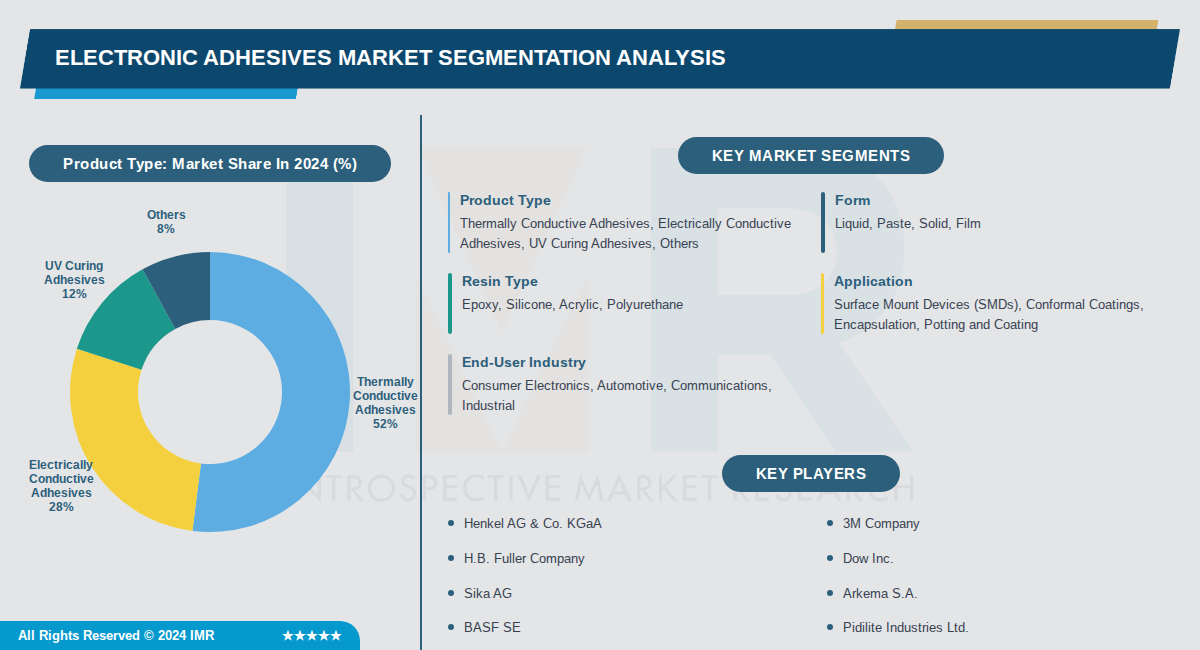

The market encompasses various resin types, with epoxy resins commanding approximately 37% market share in 2024, followed by silicone, acrylic, and polyurethane resins. Electronic adhesives are valued for their thermal conductivity, electrical conductivity, durability, optical clarity, and rapid curing properties, making them indispensable for applications ranging from touch screens and displays to optomechanical assemblies and fiber-optic connectivity. The consumer electronics segment leads end-user demand, driven by increased adoption of smartphones, wearables, and smart devices, while the surface mounting segment represents the dominant application category.

Asia Pacific is the largest regional market, accounting for approximately 32% revenue share in 2024, while North America is experiencing the fastest growth trajectory. Key market drivers include technological advancements in 5G infrastructure, rapid expansion of electric vehicles, miniaturization and automation trends in electronics manufacturing, and new product launches by major players such as Master Bond Inc. and DELO. The market continues to benefit from growing industrialization, demand for high-performance materials in emerging economies, and increased electronic content per vehicle in automotive applications.

Electronic Adhesives Market Trend Analysis:

Shift Towards Environmentally Friendly and Sustainable Adhesive Solutions

- Companies are increasingly investing in bio-based and solvent-free adhesive formulations to meet stricter environmental regulations and consumer demand for sustainability. Water-based adhesives represent the fastest-growing sub-segment with a projected CAGR of 9.1%, driven by the focus on environmentally friendly solutions and reduced VOC emissions. Leading adhesive manufacturers increased their R&D spending by 15% in 2023 to develop eco-friendly alternatives, with several companies launching solvent-free products in response to European regulatory requirements.

- The transition to green adhesives is supported by both regulatory incentives and market opportunity expansion in emerging markets. Companies investing in bio-based adhesives can differentiate themselves while meeting the growing consumer awareness of environmental issues. This trend aligns with global regulatory movements toward stricter VOC emissions controls, prompting manufacturers to accelerate their shift to water-based formulations.

Integration of Multifunctional Properties in Adhesive Formulations

- Adhesive manufacturers are transitioning from single-function bonding materials to multifunctional formulations that integrate adhesion with thermal conductivity, electrical insulation, EMI shielding, and environmental protection capabilities. This trend is particularly evident in high-power applications such as electric vehicle inverters, onboard chargers, and renewable energy power conversion systems where heat flux, voltage, and operating temperatures are escalating.

- Silicone adhesives are experiencing the highest compound annual growth rate throughout the forecast period due to their superior temperature resistance, flexibility, and long-term stability required for demanding thermal environments. Recent industry developments, such as Dow's introduction of high-temperature silicone gel for next-generation IGBT modules, exemplify the focus on advanced thermal-management and protection-first adhesive solutions that meet the requirements of increasingly complex electronic systems.

Miniaturization of Electronic Components and Advanced Packaging Solutions

- The shift towards miniaturization of electronic components is driving increased adoption of adhesives as alternatives to traditional soldering in various applications. The proliferation of smartphones, tablets, wearable devices, and smart home technologies is boosting demand for adhesives that provide reliable performance and durability at smaller scales. As electronic devices become more compact, the use of resin components and film-like materials is steadily increasing.

- The semiconductor packaging segment is expected to grow at the fastest CAGR, driven by increasing semiconductor production and escalating adoption of advanced packaging solutions. Underfills, encapsulants, and die-attach materials are becoming crucial for protecting fine-pitch interconnects and managing increased thermal loads. The World Semiconductor Trade Statistics forecasts continuous semiconductor market growth, supporting sustained demand for specialized adhesive materials in advanced packaging applications.

Electronic Adhesives Market Segment Analysis:

Electronic Adhesives Market is Segmented on the basis of By Product Type, By Form, By Resin Type

By Product Type, Thermally Conductive Adhesives segment is expected to dominate the market during the forecast period

- Thermally Conductive Adhesives dominate due to rising demand for heat dissipation in high-performance electronics like LEDs, CPUs, and power modules in compact devices.

- Growth in EVs, 5G infrastructure, and data centers requires superior thermal management, where these adhesives enhance device reliability and lifespan by over 30%.

By Form, Liquid segment is expected to dominate the market during the forecast period

- Liquid adhesives lead because of their versatility in electronics assembly, enabling uniform coating, fast curing, and automation compatibility in high-volume production.

- They are ideal for intricate SMD assemblies and conformal coatings, supporting miniaturization trends in consumer electronics and automotive sectors.

By Resin Type, Epoxy segment is expected to dominate the market during the forecast period

- Epoxy resins dominate due to their exceptional mechanical strength, high thermal stability, and resistance to chemicals, making them essential for PCBs and semiconductor bonding.

- Advancements in epoxy formulations support harsh environment applications in automotive electronics and aerospace, capturing over 40% of structural adhesive needs.

By Application, Surface Mount Devices (SMDs) segment is expected to dominate the market during the forecast period

- SMDs lead as they are fundamental to compact electronic assemblies in smartphones, wearables, and PCBs, driven by miniaturization and high-density mounting.

- The shift to lead-free soldering and surface mount technology has increased SMD adhesive usage by 25% annually in consumer and automotive electronics.

By End-User Industry, Consumer Electronics segment is expected to dominate the market during the forecast period

- Consumer electronics dominate fueled by explosive growth in smartphones, tablets, IoT devices, and wearables requiring reliable bonding in miniaturized designs.

- Annual shipments exceeding 1.5 billion units globally, combined with 5G and AI integration, drive over 50% adhesive consumption in this segment.

Electronic Adhesives Market Regional Insights:

Asia Pacific Dominates the Electronic Adhesives Market

- Asia Pacific dominates the electronic adhesives market, holding over 40% of the global share in 2025 and the largest share in 2024 at USD 6.46 billion. Key countries like China, Japan, South Korea, India, and others drive this leadership through massive electronics manufacturing hubs. China alone is projected to reach USD 3.13 billion in 2026, fueled by its scale in production and exports.

- The region's dominance stems from its concentration of semiconductor assembly, consumer electronics manufacturing, and export-oriented supply chains, supported by robust infrastructure and investments in EVs, 5G, and power electronics. Favorable government policies, R&D investments, and integrated supply chains from resins to automated lines ensure cost leadership and rapid growth. This positions Asia Pacific as the primary demand center over the forecast period.

- Major players benefit from expansions in China, Thailand, and Vietnam, with recent foreign investments redirecting assembly due to tariff exemptions and state grants for advanced packaging. Countries like Japan and South Korea lead in technological innovations for high-performance adhesives in miniaturized components. Ongoing developments in EV powertrains and charging infrastructure further boost demand for specialized products like silicone gels and thermal adhesives.

Active Key Players in the Electronic Adhesives Market:

- Henkel AG & Co. KGaA (Germany)

- 3M Company (USA)

- H.B. Fuller Company (USA)

- Dow Inc. (USA)

- Sika AG (Switzerland)

- Arkema S.A. (France)

- BASF SE (Germany)

- Pidilite Industries Ltd. (India)

- Evonik Industries AG (Germany)

- Dymax Corporation (USA)

- Huntsman Corporation (USA)

- Ashland Global Holdings Inc. (USA)

- Bostik SA (France)

- LORD Corporation (USA)

- Permabond LLC (USA)

- Master Bond Inc. (USA)

- DELO Industrial Adhesives (Germany)

- Shin-Etsu Chemical (Japan)

- Wacker Chemie AG (Germany)

- Other Active Players

|

Electronic Adhesives Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 5.4 Billion |

|

Forecast Period 2024-2035 CAGR: |

5.8 % |

Market Size in 2035: |

USD 9.5 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Form |

|

||

|

By Resin Type |

|

||

|

By Application |

|

||

|

By End-User Industry |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Electronic Adhesives Market by Product Type (2017-2035)

4.1 Electronic Adhesives Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Thermally Conductive Adhesives

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Electrically Conductive Adhesives

4.5 UV Curing Adhesives

4.6 Others

Chapter 5: Electronic Adhesives Market by Form (2017-2035)

5.1 Electronic Adhesives Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Liquid

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Paste

5.5 Solid

5.6 Film

Chapter 6: Electronic Adhesives Market by Resin Type (2017-2035)

6.1 Electronic Adhesives Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Epoxy

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Silicone

6.5 Acrylic

6.6 Polyurethane

Chapter 7: Electronic Adhesives Market by Application (2017-2035)

7.1 Electronic Adhesives Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Surface Mount Devices (SMDs)

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Conformal Coatings

7.5 Encapsulation

7.6 Potting and Coating

Chapter 8: Electronic Adhesives Market by End-User Industry (2017-2035)

8.1 Electronic Adhesives Market Snapshot and Growth Engine

8.2 Market Overview

8.3 Consumer Electronics

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

8.3.3 Key Market Trends, Growth Factors, and Opportunities

8.3.4 Geographic Segmentation Analysis

8.4 Automotive

8.5 Communications

8.6 Industrial

Chapter 9: Company Profiles and Competitive Analysis

9.1 Competitive Landscape

9.1.1 Competitive Benchmarking

9.1.2 Electronic Adhesives Market Share by Manufacturer/Service Provider (2024)

9.1.3 Industry BCG Matrix

9.1.4 Partnerships, Mergers & Acquisitions

9.2 HENKEL AG & CO. KGAA

9.2.1 Company Overview

9.2.2 Key Executives

9.2.3 Company Snapshot

9.2.4 Role of the Company in the Market

9.2.5 Sustainability and Social Responsibility

9.2.6 Operating Business Segments

9.2.7 Product Portfolio

9.2.8 Business Performance

9.2.9 Recent News & Developments

9.2.10 SWOT Analysis

9.3 3M COMPANY

9.4 H.B. FULLER COMPANY

9.5 DOW INC.

9.6 SIKA AG

9.7 ARKEMA S.A.

9.8 BASF SE

9.9 PIDILITE INDUSTRIES LTD.

9.10 EVONIK INDUSTRIES AG

9.11 DYMAX CORPORATION

9.12 HUNTSMAN CORPORATION

9.13 ASHLAND GLOBAL HOLDINGS INC.

9.14 BOSTIK SA

9.15 LORD CORPORATION

9.16 PERMABOND LLC

9.17 MASTER BOND INC.

9.18 DELO INDUSTRIAL ADHESIVES

9.19 SHIN-ETSU CHEMICAL

9.20 WACKER CHEMIE AG

Chapter 10: Global Electronic Adhesives Market By Region

10.1 Overview

10.2. North America Electronic Adhesives Market

10.2.1 Key Market Trends, Growth Factors and Opportunities

10.2.2 Top Key Companies

10.2.3 Historic and Forecasted Market Size by Segments

10.2.4 Historic and Forecast Market Size by Country

10.3. Eastern Europe Electronic Adhesives Market

10.3.1 Key Market Trends, Growth Factors and Opportunities

10.3.2 Top Key Companies

10.3.3 Historic and Forecasted Market Size by Segments

10.3.4 Historic and Forecast Market Size by Country

10.4. Western Europe Electronic Adhesives Market

10.4.1 Key Market Trends, Growth Factors and Opportunities

10.4.2 Top Key Companies

10.4.3 Historic and Forecasted Market Size by Segments

10.4.4 Historic and Forecast Market Size by Country

10.5. Asia Pacific Electronic Adhesives Market

10.5.1 Key Market Trends, Growth Factors and Opportunities

10.5.2 Top Key Companies

10.5.3 Historic and Forecasted Market Size by Segments

10.5.4 Historic and Forecast Market Size by Country

10.6. Middle East & Africa Electronic Adhesives Market

10.6.1 Key Market Trends, Growth Factors and Opportunities

10.6.2 Top Key Companies

10.6.3 Historic and Forecasted Market Size by Segments

10.6.4 Historic and Forecast Market Size by Country

10.7. South America Electronic Adhesives Market

10.7.1 Key Market Trends, Growth Factors and Opportunities

10.7.2 Top Key Companies

10.7.3 Historic and Forecasted Market Size by Segments

10.7.4 Historic and Forecast Market Size by Country

Chapter 11: Analyst Viewpoint and Conclusion

Chapter 12: Research Methodology

12.1 Research Process

12.2 Primary Research

12.3 Secondary Research

Chapter 13: Case Study

Chapter 14: Appendix

14.1 Sources

14.2 List of Tables and Figures

14.3 Short Forms and Citations

14.4 Assumption and Conversion

14.5 Disclaimer

|

Electronic Adhesives Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 5.4 Billion |

|

Forecast Period 2024-2035 CAGR: |

5.8 % |

Market Size in 2035: |

USD 9.5 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Form |

|

||

|

By Resin Type |

|

||

|

By Application |

|

||

|

By End-User Industry |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||