Drug Infusion System Market Synopsis:

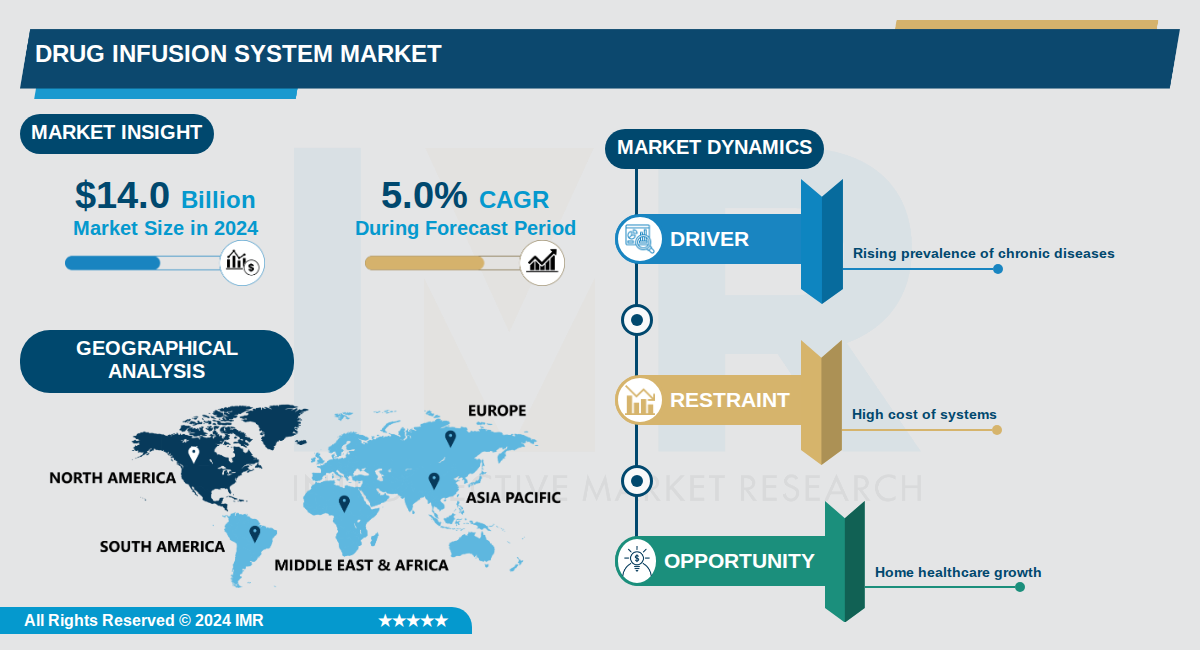

Drug Infusion System Market Size Was Valued at USD 14.0 Billion in 2024, and is Projected to Reach USD 26.0 Billion by 2035, Growing at a CAGR of 5.0% From 2024-2035.

The Drug Infusion System Market, valued at $14.0 billion in 2024, is projected to reach $26.0 billion by 2035, reflecting a compound annual growth rate (CAGR) of 5.0%. This growth trajectory aligns with recent market data indicating strong expansion, with the global market growing from $12.8 billion in 2023 to $13.78 billion in 2024 at a CAGR of 7.6%, and forecasted to hit $18.74 billion by 2028 at 8.0% CAGR.

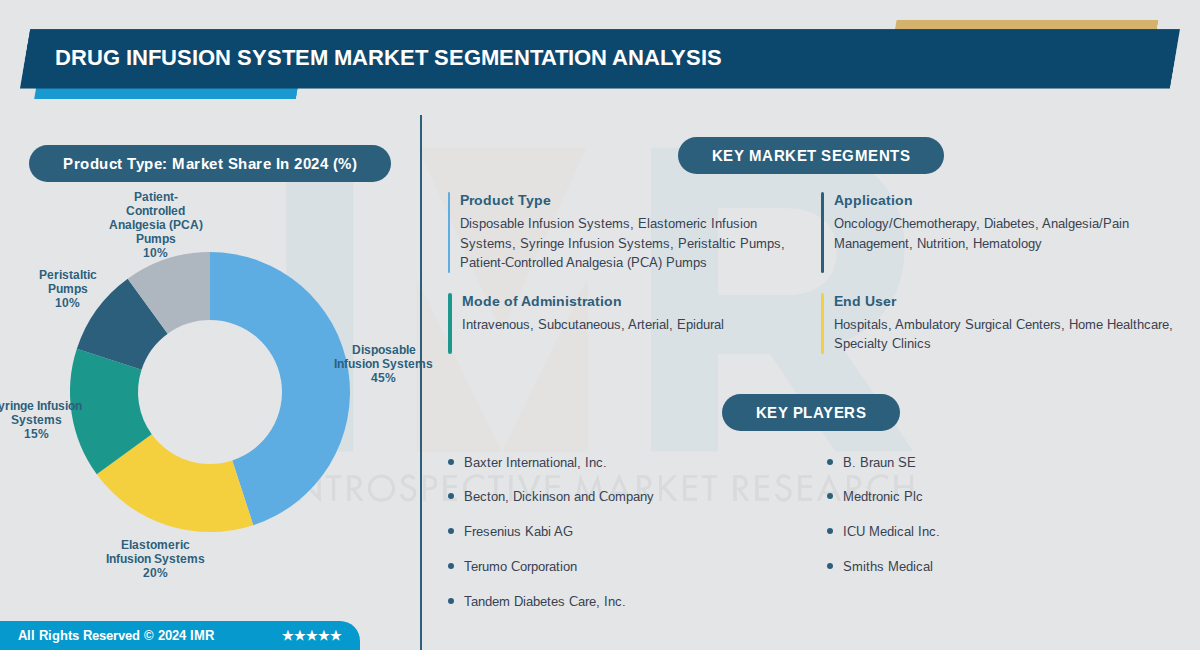

Drug infusion systems encompass a variety of products including elastomeric, disposable, syringe, peristaltic, multi-channel, patient-controlled analgesia (PCA), insulin, and implantable infusion systems. These are administered via routes such as intravenous, subcutaneous, arterial, and epidural, serving applications in oncology, diabetes, analgesia, nutrition, hematology, pediatrics, and more. End users primarily include hospitals, ambulatory surgical centers, and diagnostic centers.

Major players driving the market include Medtronic plc, Baxter International Inc., ICU Medical Inc., Becton Dickinson and Company, Smiths Group plc, and others. Key trends feature advanced drug delivery technologies like smart infusion systems with wireless connectivity, remote monitoring, EHR integration, and personalized dosing, exemplified by Ivenix's 2021 launch of an informatics-integrated pump.

Drug Infusion System Market Trend Analysis:

Adoption of Smart Infusion Pumps

- Smart infusion pumps equipped with automated dose error reduction software are witnessing rapid adoption across hospitals and intensive care units, significantly reducing human error by alerting professionals about dosage inconsistencies or potential drug interactions. Companies like B. Braun and ICU Medical have launched models such as the BBraun Infusomat Space and ICU Medical's Plum 360, which integrate drug libraries and real-time monitoring to enhance medication accuracy. This trend is driven by rising safety concerns, with hospitals replacing traditional pumps to comply with protocols amid increasing medication error reports.

- Integration with electronic medical record platforms and wireless connectivity allows for seamless data sharing, enabling predictive maintenance and improved patient outcomes. For instance, BD's Alaris system supports interoperability with hospital systems, reducing equipment downtime by up to 30% according to user reports. North America leads this adoption due to high healthcare expenditure and regulatory emphasis on patient safety.

- The market for smart pumps is projected to contribute significantly to the overall infusion pump market growth from $15.73 billion in 2025 to $25.01 billion by 2030 at a CAGR of 9.8%, fueled by chronic disease management needs in diabetes and oncology.

Rise of Ambulatory and Home-Based Infusion Devices

- Ambulatory infusion pumps are gaining traction due to patient preference for mobility during treatments like chemotherapy and pain management, with home healthcare emerging as the fastest-growing application segment. Portable devices such as elastomeric pumps from Baxter's Intermate and electronic ambulatory pumps from Moog's Curlin allow continuous drug delivery outside hospitals, reducing hospital visits by enabling self-administration. The U.S. home infusion therapy market, valued at $22.55 billion in 2025, is projected to reach $48.23 billion by 2035, driven by cost savings and convenience.

- Wearable and smart infusion pumps are making self-administration safer, with features like remote monitoring appealing to aging populations and chronic illness patients. Companies like Tandem Diabetes Care offer t:slim X2 pumps for insulin delivery at home, supporting the shift toward outpatient care. This trend aligns with healthcare digitization, where rising diabetes and cancer cases boost demand for insulin and chemotherapy systems.

- Ambulatory surgical centers are adopting elastomeric pumps as the second-fastest-growing end-use, offering portable solutions for post-op pain management with shorter recovery times and favorable reimbursements.

Expansion of Wireless Connectivity in Infusion Systems

- Wireless connectivity and remote monitoring are becoming standard in new devices, enabling real-time data analytics and integration with cloud platforms for enhanced oversight. Manufacturers like Smiths Medical with CADD-Solis and Fresenius Kabi with Agilia pumps incorporate Bluetooth and Wi-Fi for connectivity to hospital information systems, reducing errors and supporting predictive maintenance. This feature addresses cybersecurity concerns while improving efficiency in ICUs and home settings.

- Healthcare digitization initiatives are accelerating interoperability, with pumps linking to EMRs for automated programming, particularly in North America where technological leadership drives adoption. The trend supports personalized medicine in oncology, where precise biologics dosing requires connected systems, contributing to market growth amid rising surgical procedures.

Drug Infusion System Market Segment Analysis:

Drug Infusion System Market is Segmented on the basis of By Product Type, By Application, By Mode of Administration

By Product Type, Disposable Infusion Systems segment is expected to dominate the market during the forecast period

- Disposable infusion systems dominate due to their single-use design which minimizes cross-contamination risks in high-volume hospital settings like hydration and blood transfusions.

- Hospitals prefer disposables for routine procedures such as chemotherapy and surgical care, driving over 45% market share amid rising infection control standards.

By Application, Oncology/Chemotherapy segment is expected to dominate the market during the forecast period

- Oncology/chemotherapy leads because infusion systems ensure precise delivery of anticancer drugs, targeted therapies, and immunotherapies to cancer patients.

- High global cancer prevalence and the need for controlled dosing in chemotherapy protocols position this segment as the largest revenue contributor.

By Mode of Administration, Intravenous segment is expected to dominate the market during the forecast period

- Intravenous administration dominates as it enables rapid and precise drug delivery directly into the bloodstream, suitable for most acute and chronic therapies.

- IV is the standard for critical applications like chemotherapy, hydration, and emergency care, accounting for the majority of hospital infusion procedures.

By End User, Hospitals segment is expected to dominate the market during the forecast period

- Hospitals lead due to their high procurement power, large patient volumes, and capacity for complex procedures requiring advanced infusion systems.

- Equipped with trained staff and comprehensive care for chemotherapy, ICU, and surgery, hospitals hold the largest share at over 50%.

Drug Infusion System Market Regional Insights:

North America Dominates the Drug Infusion Systems Market with Strongest Market Position

- Point 1: North America was the largest region in the drug infusion systems market in 2025, commanding a significant share of the global market. The United States leads this dominance due to well-established healthcare infrastructures, robust reimbursement frameworks, and value-based care initiatives that incentivize adoption of advanced infusion technologies and precision dosing solutions.

- Point 2: The North American market benefits from superior medical device technology improvements, higher diabetes diagnosis and treatment rates, increased use of ambulatory pumps, and excellent reimbursement policies that accelerate product adoption. These structural advantages create strong barriers to entry and maintain the region's competitive lead in advanced infusion system deployment across hospitals and outpatient settings.

- Point 3: While Asia-Pacific is emerging as the fastest-growing region during the forecast period, North America's mature healthcare ecosystem, established supply chains, and concentrated presence of major medical device manufacturers ensure continued market dominance. Canada and Mexico contribute to regional strength, though the United States remains the primary growth engine with state-level markets in California, Florida, Texas, New York, and Pennsylvania showing particularly strong demand.

Active Key Players in the Drug Infusion System Market:

- Baxter International, Inc. (USA)

- B. Braun SE (Germany)

- Becton, Dickinson and Company (USA)

- Medtronic Plc (Ireland)

- Fresenius Kabi AG (Germany)

- ICU Medical Inc. (USA)

- Terumo Corporation (Japan)

- Smiths Medical (USA)

- Tandem Diabetes Care, Inc. (USA)

- Insulet Corporation (USA)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Ypsomed AG (Switzerland)

- Moog, Inc. (USA)

- Teleflex Incorporated (USA)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

- Eitan Medical (Israel)

- IRADIMED CORPORATION (USA)

- Ivenix Inc. (USA)

- Other Active Players

|

Drug Infusion System Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 14.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

5.0 % |

Market Size in 2035: |

USD 26.0 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Application |

|

||

|

By Mode of Administration |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Drug Infusion System Market by Product Type (2017-2035)

4.1 Drug Infusion System Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Disposable Infusion Systems

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Elastomeric Infusion Systems

4.5 Syringe Infusion Systems

4.6 Peristaltic Pumps

4.7 Patient-Controlled Analgesia (PCA) Pumps

Chapter 5: Drug Infusion System Market by Application (2017-2035)

5.1 Drug Infusion System Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Oncology/Chemotherapy

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Diabetes

5.5 Analgesia/Pain Management

5.6 Nutrition

5.7 Hematology

Chapter 6: Drug Infusion System Market by Mode of Administration (2017-2035)

6.1 Drug Infusion System Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Intravenous

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Subcutaneous

6.5 Arterial

6.6 Epidural

Chapter 7: Drug Infusion System Market by End User (2017-2035)

7.1 Drug Infusion System Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Hospitals

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Ambulatory Surgical Centers

7.5 Home Healthcare

7.6 Specialty Clinics

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Drug Infusion System Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 BAXTER INTERNATIONAL

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 INC.

8.4 B. BRAUN SE

8.5 BECTON

8.6 DICKINSON AND COMPANY

8.7 MEDTRONIC PLC

8.8 FRESENIUS KABI AG

8.9 ICU MEDICAL INC.

8.10 TERUMO CORPORATION

8.11 SMITHS MEDICAL

8.12 TANDEM DIABETES CARE

8.13 INC.

8.14 INSULET CORPORATION

8.15 F. HOFFMANN-LA ROCHE LTD

8.16 YPSOMED AG

8.17 MOOG

8.18 INC.

8.19 TELEFLEX INCORPORATED

8.20 SHENZHEN MINDRAY BIO-MEDICAL ELECTRONICS CO.

8.21 LTD.

8.22 EITAN MEDICAL

8.23 IRADIMED CORPORATION

8.24 IVENIX INC.

Chapter 9: Global Drug Infusion System Market By Region

9.1 Overview

9.2. North America Drug Infusion System Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Drug Infusion System Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Drug Infusion System Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Drug Infusion System Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Drug Infusion System Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Drug Infusion System Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Drug Infusion System Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 14.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

5.0 % |

Market Size in 2035: |

USD 26.0 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Application |

|

||

|

By Mode of Administration |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||