Cold Chain Monitoring Market Synopsis:

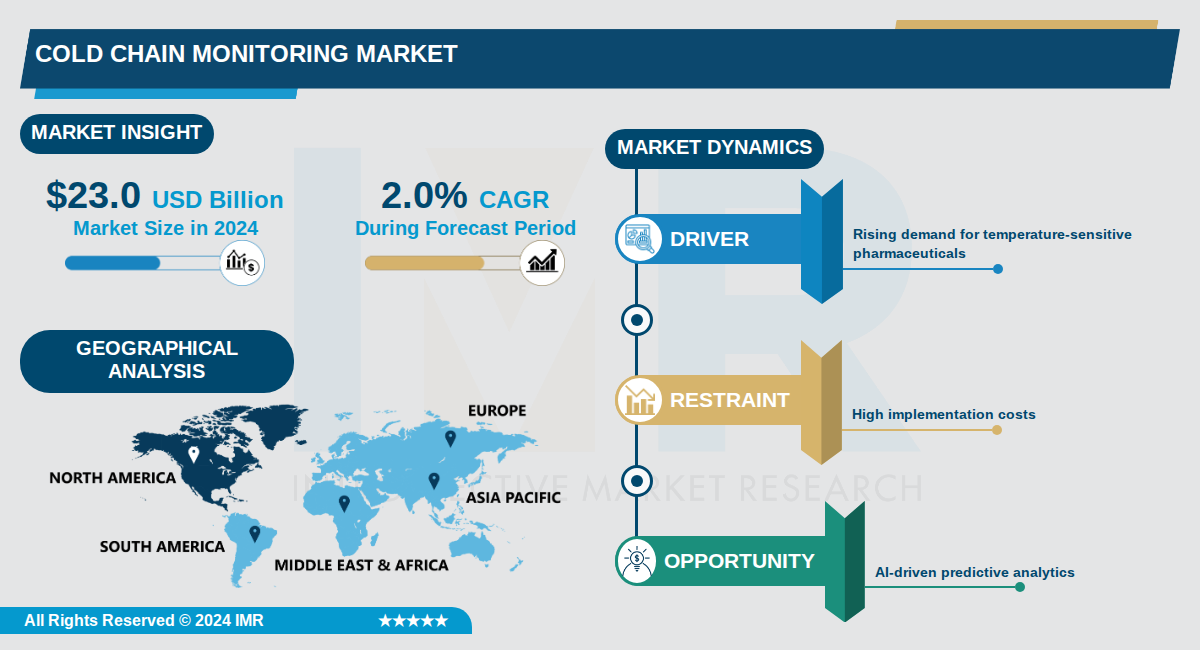

Cold Chain Monitoring Market Size Was Valued at USD 23.0 Billion in 2024, and is Projected to Reach USD 28.0 Billion by 2035, Growing at a CAGR of 2.0% From 2024-2035.

The Cold Chain Monitoring Market, valued at $23.0 billion in 2024, is projected to reach $28.0 billion by 2035, growing at a CAGR of 2.0%. This market encompasses technologies and solutions for tracking and monitoring temperature-sensitive products during storage and transportation, primarily serving pharmaceuticals, food & beverages, and other perishable goods.

Hardware components, including sensors, RFID devices, telematics, and networking equipment, dominate the market with over 78% revenue share in 2024, driven by their role in real-time data collection for temperature and location. The food & beverages application leads with approximately 77% market share, fueled by demand for processed foods and consumer preferences for fresh products.

North America holds the largest regional share at over 33% in 2024, supported by advanced infrastructure and stringent regulations, while Asia Pacific is poised for the fastest growth due to industrialization, rising demand for perishables, and investments in logistics.

Cold Chain Monitoring Market Trend Analysis:

Integration of AI for Predictive Analytics

- Advanced AI algorithms process data from cold chain sensors to forecast equipment failures and temperature excursions, shifting from reactive to proactive risk management. Logistics providers like those in the pharmaceutical sector use these tools to intervene before spoilage occurs, ensuring the integrity of biologics such as insulin and vaccines. This trend is gaining momentum as companies recognize predictive intelligence as essential for complex supply chains.

- AI enhances forecasting, route planning, and warehouse optimization by integrating real-time sensor data with machine learning. In 2025, Air Cargo Week reported a 62 percent year-on-year increase in cool goods air transport, underscoring the need for AI-driven predictions amid rising global air cargo demand of 11.3 percent in 2024 per IATA.

- Vendors offering AI-driven quality control are transforming monitoring into proactive systems, with cloud-based architectures becoming the backbone of modern cold chains as organizations scale digital operations.

Shift to Real-Time IoT and Cloud Monitoring

- The transition from passive data loggers to IoT-enabled sensors provides live environmental data, allowing immediate actions like rerouting shipments or equipment adjustments during transit. A September 2025 SeaVantage article noted that 57 percent of supply chain professionals cite lack of real-time visibility as their top challenge, accelerating adoption of these active systems.

- Cloud-based IoT ecosystems integrate sensor data with analytics for early risk detection and automated decisions, mandatory under global regulations like FDA's FSMA and GDP guidelines requiring continuous tracking. Companies in North America, with USD 2.3 billion US market revenue in 2025, lead in deploying these platforms across storage and transport.

- Amazon, Walmart, and Alibaba are expanding cold last-mile logistics with IoT monitoring in vans, bikes, and insulated boxes to meet rising e-commerce demands for fresh food and meal kits.

Rise of Last-Mile Cold Chain Monitoring

- Online grocery platforms and quick-commerce services like Meituan demand monitoring for urban routes with frequent door openings and varied packaging, using lightweight, tamper-aware sensors. This extends temperature control from long-haul to doorstep logistics, reducing waste in dairy, frozen items, and perishables amid booming e-commerce.

- In Asia Pacific, expected to grow at the highest CAGR through 2030, rapid urbanization and online delivery in China and India drive investments in smart logistics hubs with real-time monitoring. Governments and private players are building cold storage and reefer fleets to support vaccine exports and pharmaceutical production.

- Expansion by Amazon and Walmart into same-day cold shipments forces suppliers to integrate monitoring into micro-fulfillment centers, ensuring freshness as consumer expectations intensify.

Cold Chain Monitoring Market Segment Analysis:

Cold Chain Monitoring Market is Segmented on the basis of By Component, By Temperature Type, By Logistics

By Component, Hardware segment is expected to dominate the market during the forecast period

- Hardware dominates due to essential sensors, RFID devices, telematics, and networking equipment required for real-time data collection on temperature and location in cold chain facilities.

- It accounted for around 60% market share in 2025 and 78.1% in 2024, driven by high deployment in storage and transportation for compliance with stringent regulations.

By Temperature Type, Frozen segment is expected to dominate the market during the forecast period

- Frozen segment leads with 56% share in 2025 due to critical applications in meat, seafood, and pharmaceuticals requiring ultra-low temperatures for long-term preservation.

- Highest CAGR of 13.8% expected, fueled by expanding demand for frozen foods and vaccines in global supply chains.

By Logistics, Storage segment is expected to dominate the market during the forecast period

- Storage dominates as warehouses and distribution centers hold products longer, necessitating advanced monitoring for humidity and temperature compliance.

- Rising investments in cold storage infrastructure worldwide, especially in Asia Pacific, drive its leadership over transportation.

By End Use, Pharmaceutical & Healthcare segment is expected to dominate the market during the forecast period

- Pharmaceutical & healthcare leads with USD 5.3 billion valuation in 2025 due to strict regulatory needs for vaccines, biologics, and temperature-sensitive drugs.

- Stringent FDA and global compliance drives adoption of IoT monitoring to prevent spoilage in high-value shipments.

Cold Chain Monitoring Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast Period

- North America dominates the cold chain monitoring market due to its advanced infrastructure and stringent regulatory requirements, with the U.S. leading as the largest market in the region at USD 2.3 billion in 2025 revenue. Countries like the U.S. and Canada benefit from highly developed logistics networks supporting pharmaceuticals, food, and beverages. This positions North America ahead of faster-growing regions like Asia Pacific.

- The region features world-class refrigerated transport networks, widespread IoT and telematics adoption, and rigorous regulations such as FDA's FSMA, USDA standards, and GDP guidelines mandating continuous temperature tracking. These factors ensure high compliance and rapid deployment of real-time monitoring systems across storage, transport, and delivery. Strong technology readiness supports large-scale operations in this mature market.

- Major players thrive here due to the strong presence of pharmaceutical, biotech, and food industries driving demand for reliable solutions. Recent developments include expanded IoT-enabled monitoring and cloud-based platforms, with North America holding significant shares like 32.9% in 2024. U.S. dominance underscores ongoing innovations in the sector.

Active Key Players in the Cold Chain Monitoring Market:

- Carrier (USA)

- Testo SE & Co. KGaA (Germany)

- Cryoport Inc. (USA)

- Controlant hf. (Iceland)

- ORBCOMM (USA)

- Sensitech Inc. (USA)

- Berlinger & Co. AG (Switzerland)

- Monnit Corporation (USA)

- ELPRO-BUCHS AG (Switzerland)

- Infratab (USA)

- Zest Labs (USA)

- Klinge Corporation (USA)

- Lineage Logistics (USA)

- Americold Logistics (USA)

- United States Cold Storage (USA)

- Thermo King (USA)

- Honeywell International (USA)

- Envirotainer (Sweden)

- Other Active Players

|

Cold Chain Monitoring Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 23.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

2.0 % |

Market Size in 2035: |

USD 28.0 Billion |

|

Segments Covered: |

By Component |

|

|

|

By Temperature Type |

|

||

|

By Logistics |

|

||

|

By End Use |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Cold Chain Monitoring Market by Component (2017-2035)

4.1 Cold Chain Monitoring Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Hardware

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Software

4.5 Services

Chapter 5: Cold Chain Monitoring Market by Temperature Type (2017-2035)

5.1 Cold Chain Monitoring Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Frozen

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Chilled

Chapter 6: Cold Chain Monitoring Market by Logistics (2017-2035)

6.1 Cold Chain Monitoring Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Storage

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Transportation

Chapter 7: Cold Chain Monitoring Market by End Use (2017-2035)

7.1 Cold Chain Monitoring Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Pharmaceutical & Healthcare

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Food & Beverage

7.5 Logistics & Distribution

7.6 Chemical

7.7 Others

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Cold Chain Monitoring Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 CARRIER

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 TESTO SE & CO. KGAA

8.4 CRYOPORT INC.

8.5 CONTROLANT HF.

8.6 ORBCOMM

8.7 SENSITECH INC.

8.8 BERLINGER & CO. AG

8.9 MONNIT CORPORATION

8.10 ELPRO-BUCHS AG

8.11 INFRATAB

8.12 ZEST LABS

8.13 KLINGE CORPORATION

8.14 LINEAGE LOGISTICS

8.15 AMERICOLD LOGISTICS

8.16 UNITED STATES COLD STORAGE

8.17 THERMO KING

8.18 HONEYWELL INTERNATIONAL

8.19 ENVIROTAINER

Chapter 9: Global Cold Chain Monitoring Market By Region

9.1 Overview

9.2. North America Cold Chain Monitoring Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Cold Chain Monitoring Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Cold Chain Monitoring Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Cold Chain Monitoring Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Cold Chain Monitoring Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Cold Chain Monitoring Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Cold Chain Monitoring Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 23.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

2.0 % |

Market Size in 2035: |

USD 28.0 Billion |

|

Segments Covered: |

By Component |

|

|

|

By Temperature Type |

|

||

|

By Logistics |

|

||

|

By End Use |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||