Key Market Highlights

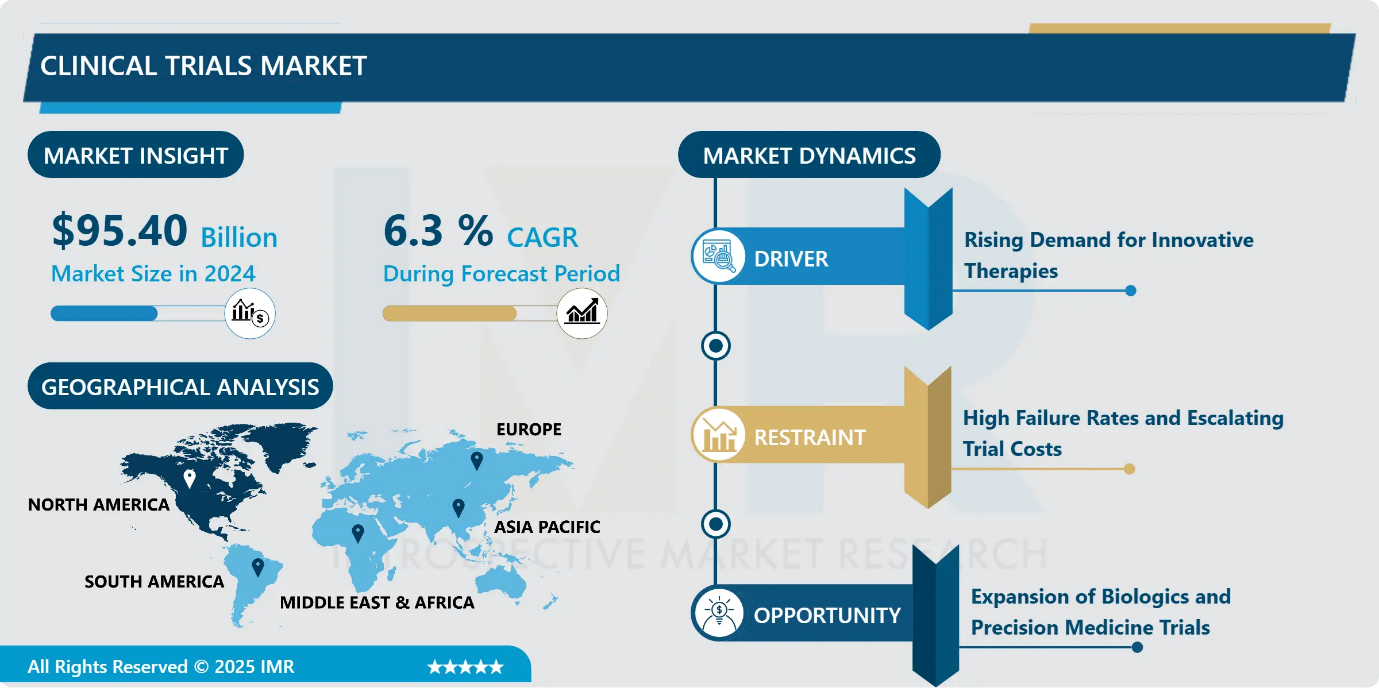

Clinical Trials Market Size Was Valued at USD 95.40 Billion in 2024, and is Projected to Reach USD 186.82 Billion by 2035, Growing at a CAGR of 6.3% from 2025-2035.

- Market Size in 2024: USD 95.40 Billion

- Projected Market Size by 2035: USD 186.82 Billion

- CAGR (2025–2035): 6.3%

- Leading Market in 2024: North America

- Fastest-Growing Market: Asia Pacific

- By Therapeutic Area: The Oncology segment is anticipated to lead the market by accounting for 31.2% of the market share throughout the forecast period.

- By Study Design: The Interventional segment is expected to capture 36.1% of the market share, thereby maintaining its dominance over the forecast period.

- By Region: North America region is projected to hold 30.4% of the market share during the forecast period.

- Active Players: Caidya (United States), Charles River Laboratories International, Inc. (United States), Eli Lilly and Company (United States), ICON plc (Ireland), IQVIA (United States), and Other Active Players.

Clinical Trials Market Synopsis:

Clinical trials are structured research studies conducted on human participants to evaluate the safety, efficacy, and performance of new interventions such as drugs, medical devices, biologics, and therapeutic diets. The market is expanding due to rising chronic disease prevalence, growing geriatric populations, globalization of drug development, and increasing outsourcing to clinical research organizations (CROs). Hybrid and decentralized trial models, AI-driven patient recruitment, adaptive study designs, and biomarker-based precision medicine are reshaping execution strategies. Phase II trials are gaining greater investment for proof-of-concept validation. However, high trial costs, lengthy regulatory approval timelines, and shortages of skilled professionals restrain growth. Despite these challenges, technological integration and geographic diversification into emerging regions continue to create significant market opportunities.

Clinical Trials Market Dynamics and Trend Analysis:

Clinical Trials Market Growth Driver

Rising Demand for Innovative Therapies

- The Clinical Trials Market is being strongly driven by the increasing demand for innovative and targeted therapies, particularly in oncology, neurology, and rare diseases. The growing global burden of chronic and complex conditions has intensified the need for safer, more effective, and personalized treatment options. As a result, pharmaceutical and biotechnology companies are significantly expanding their research and development investments, leading to a higher number of trial initiations, especially in precision medicine. This surge in innovation accelerates pipeline development and trial activity worldwide. Additionally, strategic collaborations among biopharmaceutical firms, contract research organizations, and academic institutions are further strengthening clinical development capabilities and market expansion.

Clinical Trials Market Limiting Factor

High Failure Rates and Escalating Trial Costs

- Elevated failure rates in late-stage clinical development are a major restraint on the Clinical Trials Market. Oncology Phase III studies continue to demonstrate high attrition due to tumor heterogeneity and increasingly stringent regulatory and payer requirements for overall survival evidence. Similarly, Alzheimer’s trials show substantial failure rates, leading to significant financial losses per unsuccessful program. These setbacks result in considerable sunk costs and extended development timelines. Additionally, stricter health technology assessment evaluations in key markets are compelling sponsors to adopt more rigorous endpoints, further increasing complexity, cost, and risk associated with advanced-stage clinical trials, thereby limiting overall market growth potential.

Clinical Trials Market Expansion Opportunity

Expansion of Biologics and Precision Medicine Trials

- The growing pipeline of biologics, cell and gene therapies, and precision medicines presents a significant opportunity for the Clinical Trials Market. With biologics accounting for a rising share of investigational assets, sponsors increasingly require complex, data-intensive, and longer-duration studies. The surge in oncology, neurology, and rare disease programs further accelerates demand for specialized trial designs and biomarker-driven approaches. Additionally, capacity constraints in advanced therapy manufacturing are encouraging greater outsourcing to contract research organizations (CROs). As pharmaceutical and biotechnology companies expand R&D investments to support personalized medicine, the need for advanced trial infrastructure, regulatory expertise, and innovative execution models continues to create substantial market growth opportunities.

Clinical Trials Market Challenge and Risk

Stringent Data Privacy Regulations

- Tightening global data privacy regulations present a significant challenge for the Clinical Trials Market by restricting cross-border data flows and increasing operational complexity. Compliance with evolving frameworks has extended study start-up timelines, delayed interim analyses, and required substantial investments in localized data infrastructure. Sponsors and contract research organizations must establish regional data storage systems, leading to higher capital and operational expenditures. Although emerging technologies such as blockchain-based consent management demonstrate potential to reduce compliance costs, adoption remains limited due to integration challenges and legacy system constraints. Collectively, these regulatory burdens slow multinational trial execution and increase overall development costs.

Clinical Trials Market Trend

Technological Advancements Transforming Clinical Trials

- Technological innovation is emerging as a key trend reshaping the Clinical Trials Market. The adoption of digital solutions such as electronic data capture (EDC), remote patient monitoring, decentralized trial platforms, and cloud-based systems is significantly improving operational efficiency and data accuracy. Furthermore, the growing integration of artificial intelligence (AI) and machine learning (ML) enables faster patient identification, predictive analytics, protocol optimization, and real-time data analysis. These advancements help reduce trial timelines, lower operational costs, and enhance decision-making processes. As sponsors increasingly embrace digital transformation, the market is witnessing accelerated trial execution and improved productivity across the clinical development lifecycle.

Clinical Trials Market Segment Analysis:

Clinical Trials Market is segmented based on Phase, End-User, Study Design, Service Type, Therapeutic Area, and Region.

By Therapeutic Area, Oncology segment is expected to dominate the market with around 31.2% share during the forecast period.

- Oncology continues to dominate the Clinical Trials Market, accounting for approximately 31.2% of total revenue, supported by a large pipeline of active mid- to late-stage programs. Its dominance is driven by the high global cancer burden, continuous innovation in targeted therapies, immuno-oncology, and precision medicine, as well as strong investment from pharmaceutical sponsors. Advanced trial designs such as basket and umbrella studies further strengthen oncology’s position. Meanwhile, neurology is emerging as a fast-growing segment, supported by improved diagnostic biomarkers that enhance patient selection and reduce sample sizes. Cardiovascular, metabolic, infectious disease, and immunology trials also contribute steadily to overall market expansion.

By Study Design, Interventional study designs is expected to dominate with close to 36.1% market share during the forecast period.

- Interventional study designs dominate the Clinical Trials Market, accounting for approximately 36.1% of total revenue in 2024. Their dominance stems from their critical role in establishing safety, efficacy, and regulatory approval for new therapies through controlled, randomized methodologies. These trials remain the gold standard for drug development and are essential for market authorization. However, observational and pragmatic studies are gaining traction as regulators increasingly recognize real-world evidence to support label expansions and post-marketing decisions. Expanded-access programs and large-scale pragmatic trials leveraging electronic health records are further improving cost efficiency and physician engagement, complementing traditional interventional models in the evolving clinical research landscape.

Clinical Trials Market Regional Insights:

North America region is estimated to lead the market with around 30.4% share during the forecast period.

- North America accounted for 30.4% of the global clinical trials market in 2024 maintaining its leading position. The region’s dominance is driven by strong R&D investments, rapid adoption of advanced technologies, and widespread implementation of decentralized and virtual trial models by companies such as IQVIA and ICON plc. Supportive regulatory incentives from the U.S. Food and Drug Administration and initiatives by the National Cancer Institute further enhance efficiency and enrollment. High site density, faster patient recruitment, strong infrastructure, and cross-border collaboration with Canada and Mexico collectively reinforce North America’s market dominance.

Clinical Trials Market Active Players:

- Caidya (United States)

- Charles River Laboratories International, Inc. (United States)

- Eli Lilly and Company (United States)

- ICON plc (Ireland)

- IQVIA (United States)

- Laboratory Corporation of America Holdings (United States)

- Medpace Holdings, Inc. (United States)

- Novo Nordisk A/S (Denmark)

- Parexel International Corporation (United States)

- Pfizer Inc. (United States)

- PPD, Inc. (United States)

- SGS SA (Switzerland)

- Syneos Health (United States)

- Thermo Fisher Scientific Inc. (United States)

- WuXi AppTec Co., Ltd. (China)

- Other Active Players

Key Industry Developments in the Clinical Trials Market:

- In March 2025: ICON plc became the first major clinical research organization to fully implement Medidata Clinical Data Studio across its operations. The integration is designed to improve clinical data management efficiency, accelerate data review cycles, and strengthen trial oversight. This strategic move reinforces ICON’s position as a frontrunner in adopting advanced digital solutions for clinical development.

- In June 2024: Charles River Laboratories International, Inc. acquired Vigene Biosciences for $292.5 million, with additional contingent payments of up to $57.5 million tied to performance milestones. The acquisition expands Charles River’s viral vector manufacturing capabilities and supports its strategic growth in the rapidly expanding cell and gene therapy sector.

Technical Framework and Operational Infrastructure of the Clinical Trials Market

- The Clinical Trials Market operates within a highly regulated, multi-phase development framework encompassing Phase I–IV studies designed to evaluate safety, dosage, efficacy, and post-marketing outcomes. Technically, the market is supported by advanced clinical data management systems (CDMS), electronic data capture (EDC), clinical trial management systems (CTMS), and eClinical platforms that enable real-time monitoring, centralized data integration, and regulatory compliance. Increasing adoption of decentralized trial models incorporates telemedicine, wearable devices, remote patient monitoring, and electronic patient-reported outcomes (ePRO).

- Artificial intelligence and machine learning algorithms are being deployed for protocol optimization, site selection, risk-based monitoring, and patient recruitment analytics. Biomarker-driven stratification and adaptive trial designs enhance statistical efficiency and reduce attrition rates. Additionally, compliance with global regulatory frameworks, including Good Clinical Practice (GCP) guidelines and data privacy regulations, requires robust validation, cybersecurity safeguards, and interoperable data architectures, ensuring data integrity, transparency, and accelerated drug development timelines across therapeutic areas.

|

Clinical Trials Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2024 |

Market Size in 2024: |

USD 95.40 Bn. |

|

Forecast Period 2025-32 CAGR: |

6.3 % |

Market Size in 2035: |

USD 186.82 Bn. |

|

Segments Covered: |

By Phase |

|

|

|

By End-User |

|

||

|

By Study Design |

|

||

|

By Service Type |

|

||

|

By Therapeutic Area |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Clinical Trials Market by Phase (2018-2035)

4.1 Clinical Trials Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Phase I

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Phase II

4.5 Phase III

4.6 and Phase IV

Chapter 5: Clinical Trials Market by End-User (2018-2035)

5.1 Clinical Trials Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Pharmaceutical & Biopharmaceutical Companies

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Clinical Research Organizations

5.5 and Healthcare Providers

Chapter 6: Clinical Trials Market by Study Design (2018-2035)

6.1 Clinical Trials Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Interventional/Treatment Studies and Observational Studies

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

Chapter 7: Clinical Trials Market by Service Type (2018-2035)

7.1 Clinical Trials Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Protocol Design & Feasibility

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Site Management

7.5 Patient Recruitment

7.6 Data Management

7.7 Regulatory & Compliance Services

7.8 and Others

Chapter 8: Clinical Trials Market by Therapeutic Area (2018-2035)

8.1 Clinical Trials Market Snapshot and Growth Engine

8.2 Market Overview

8.3 Oncology

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

8.3.3 Key Market Trends, Growth Factors, and Opportunities

8.3.4 Geographic Segmentation Analysis

8.4 Cardiology

8.5 Neurology

8.6 Infectious Diseases

8.7 and Others

Chapter 9: Company Profiles and Competitive Analysis

9.1 Competitive Landscape

9.1.1 Competitive Benchmarking

9.1.2 Clinical Trials Market Share by Manufacturer/Service Provider(2024)

9.1.3 Industry BCG Matrix

9.1.4 PArtnerships, Mergers & Acquisitions

9.2 CAIDYA (UNITED STATES)

9.2.1 Company Overview

9.2.2 Key Executives

9.2.3 Company Snapshot

9.2.4 Role of the Company in the Market

9.2.5 Sustainability and Social Responsibility

9.2.6 Operating Business Segments

9.2.7 Product Portfolio

9.2.8 Business Performance

9.2.9 Recent News & Developments

9.2.10 SWOT Analysis

9.3 CHARLES RIVER LABORATORIES INTERNATIONAL

9.4 INC. (UNITED STATES)

9.5 ELI LILLY AND COMPANY (UNITED STATES)

9.6 ICON PLC (IRELAND)

9.7 IQVIA (UNITED STATES)

9.8 LABORATORY CORPORATION OF AMERICA HOLDINGS (UNITED STATES)

9.9 MEDPACE HOLDINGS

9.10 INC. (UNITED STATES)

9.11 NOVO NORDISK A/S (DENMARK)

9.12 PAREXEL INTERNATIONAL CORPORATION (UNITED STATES)

9.13 PFIZER INC. (UNITED STATES)

9.14 PPD

9.15 INC. (UNITED STATES)

9.16 SGS SA (SWITZERLAND)

9.17 SYNEOS HEALTH (UNITED STATES)

9.18 THERMO FISHER SCIENTIFIC INC. (UNITED STATES)

9.19 WUXI APPTEC CO.

9.20 LTD. (CHINA)

9.21 AND OTHER ACTIVE PLAYERS.

Chapter 10: Global Clinical Trials Market By Region

10.1 Overview

10.2. North America Clinical Trials Market

10.2.1 Key Market Trends, Growth Factors and Opportunities

10.2.2 Top Key Companies

10.2.3 Historic and Forecasted Market Size by Segments

10.2.4 Historic and Forecast Market Size by Country

10.2.4.1 US

10.2.4.2 Canada

10.2.4.3 Mexico

10.3. Eastern Europe Clinical Trials Market

10.3.1 Key Market Trends, Growth Factors and Opportunities

10.3.2 Top Key Companies

10.3.3 Historic and Forecasted Market Size by Segments

10.3.4 Historic and Forecast Market Size by Country

10.3.4.1 Russia

10.3.4.2 Bulgaria

10.3.4.3 The Czech Republic

10.3.4.4 Hungary

10.3.4.5 Poland

10.3.4.6 Romania

10.3.4.7 Rest of Eastern Europe

10.4. Western Europe Clinical Trials Market

10.4.1 Key Market Trends, Growth Factors and Opportunities

10.4.2 Top Key Companies

10.4.3 Historic and Forecasted Market Size by Segments

10.4.4 Historic and Forecast Market Size by Country

10.4.4.1 Germany

10.4.4.2 UK

10.4.4.3 France

10.4.4.4 The Netherlands

10.4.4.5 Italy

10.4.4.6 Spain

10.4.4.7 Rest of Western Europe

10.5. Asia Pacific Clinical Trials Market

10.5.1 Key Market Trends, Growth Factors and Opportunities

10.5.2 Top Key Companies

10.5.3 Historic and Forecasted Market Size by Segments

10.5.4 Historic and Forecast Market Size by Country

10.5.4.1 China

10.5.4.2 India

10.5.4.3 Japan

10.5.4.4 South Korea

10.5.4.5 Malaysia

10.5.4.6 Thailand

10.5.4.7 Vietnam

10.5.4.8 The Philippines

10.5.4.9 Australia

10.5.4.10 New Zealand

10.5.4.11 Rest of APAC

10.6. Middle East & Africa Clinical Trials Market

10.6.1 Key Market Trends, Growth Factors and Opportunities

10.6.2 Top Key Companies

10.6.3 Historic and Forecasted Market Size by Segments

10.6.4 Historic and Forecast Market Size by Country

10.6.4.1 Turkiye

10.6.4.2 Bahrain

10.6.4.3 Kuwait

10.6.4.4 Saudi Arabia

10.6.4.5 Qatar

10.6.4.6 UAE

10.6.4.7 Israel

10.6.4.8 South Africa

10.7. South America Clinical Trials Market

10.7.1 Key Market Trends, Growth Factors and Opportunities

10.7.2 Top Key Companies

10.7.3 Historic and Forecasted Market Size by Segments

10.7.4 Historic and Forecast Market Size by Country

10.7.4.1 Brazil

10.7.4.2 Argentina

10.7.4.3 Rest of SA

Chapter 11 Analyst Viewpoint and Conclusion

Chapter 12 Our Thematic Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 13 Case Study

Chapter 14 Appendix

12.1 Sources

12.2 List of Tables and figures

12.3 Short Forms and Citations

12.4 Assumption and Conversion

12.5 Disclaimer

|

Clinical Trials Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2024 |

Market Size in 2024: |

USD 95.40 Bn. |

|

Forecast Period 2025-32 CAGR: |

6.3 % |

Market Size in 2035: |

USD 186.82 Bn. |

|

Segments Covered: |

By Phase |

|

|

|

By End-User |

|

||

|

By Study Design |

|

||

|

By Service Type |

|

||

|

By Therapeutic Area |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||