Car Canopies Market Synopsis:

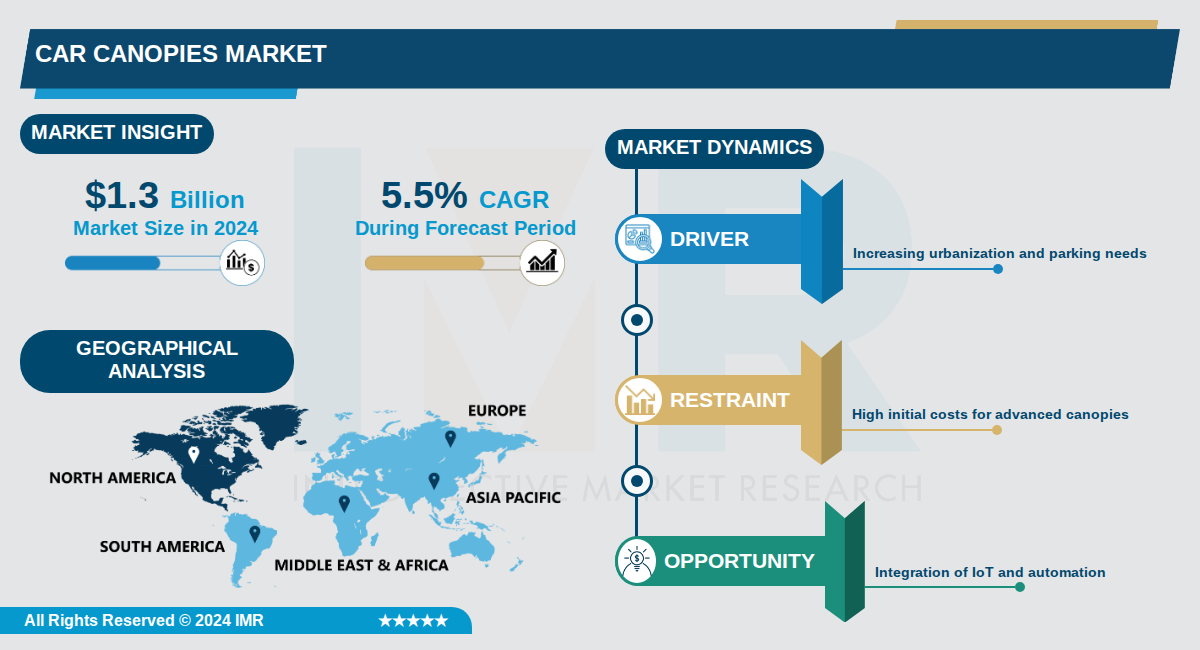

Car Canopies Market Size Was Valued at USD 1.3 Billion in 2024, and is Projected to Reach USD 2.5 Billion by 2035, Growing at a CAGR of 5.5% From 2024-2035.

The global Car Canopies Market, encompassing protective structures for vehicles such as truck and vehicle canopies, was valued at approximately $1.3 billion in 2024 and is projected to reach $2.5 billion by 2035, growing at a compound annual growth rate (CAGR) of 5.5%.

This market serves diverse applications including personal vehicle protection, commercial logistics, and recreational use, with key segments like wooden and PVC canopies showing notable shares, particularly for compact cars and pickup trucks/SUVs. North America and Europe lead due to high vehicle ownership and aftermarket demand, while Asia-Pacific experiences rapid growth from rising incomes and automotive expansion.

Major players such as ShelterLogic Group, ARE Corporation, Leer, and Snugtop dominate through strategies like product innovation, mergers, and portfolio expansion, amid a moderately concentrated landscape with both global leaders and regional niche providers.

Car Canopies Market Trend Analysis:

Integration of Smart Technologies

- Manufacturers like LEER Group and A.R.E. Mobile are incorporating remote locking systems, integrated lighting, and solar panels into vehicle canopies, enabling users to control access via smartphone apps for enhanced security during outdoor activities. In 2020, several companies launched models with these smart features, boosting adoption among pickup truck owners in North America where the market holds the highest concentration. This integration addresses growing e-commerce delivery needs by providing real-time monitoring of cargo protection.

- Truck Hero has expanded its portfolio with canopies featuring connectivity options that sync with vehicle telematics, improving fuel efficiency through aerodynamic smart adjustments. A 2023 development saw new manufacturing processes introduce durable sensors that withstand harsh weather, appealing to commercial users in Asia-Pacific where SUV popularity is rising. These advancements are projected to drive the market to over 35 million units by 2033 as consumers prioritize multifunctional accessories.

Adoption of Lightweight and Aerodynamic Designs

- Focus on aluminum and fiberglass materials has led to canopies that reduce vehicle weight by up to 20%, improving fuel efficiency for pickup trucks and SUVs, as seen in 2021 launches by major players targeting North American and Australian markets. These designs enhance handling and lower emissions, aligning with fluctuating fuel prices and regulations in Europe. LEER Group's lightweight models have captured significant share due to their cost-effectiveness and versatility.

- In 2023, innovations in high-strength composites allowed for aerodynamic shapes that cut wind resistance, popular among e-commerce fleets for secure goods transport in developing economies. A.R.E. Mobile reported increased sales from modular lightweight canopies adaptable to varying cargo sizes, supporting a CAGR of 3.1% toward a $2.15 billion market by 2025. This trend mitigates challenges like raw material costs by optimizing material use.

Rise of Sustainable and Customizable Canopies

- Manufacturers are shifting to recycled aluminum and eco-friendly fiberglass processes, with companies like Truck Hero introducing sustainable lines that appeal to environmentally conscious consumers in Europe and North America. Government incentives, such as U.S. EPA programs, support adoption of solar-powered retractable canopies made from high-quality PVC fabric, reducing energy costs for residential users. This focus addresses climate concerns while maintaining durability against storms.

- Customization options for modular designs allow personalization matching vehicle aesthetics, driving average selling prices upward as seen in LEER Group's bespoke offerings for SUVs. The trend supports outdoor recreation growth, with features like weather-resistant storage for camping gear, fueling demand in Australia where pickup markets are concentrated. By 2033, these eco-custom solutions are expected to contribute to the market reaching USD 2.5 billion at an 8.7% CAGR.

Car Canopies Market Segment Analysis:

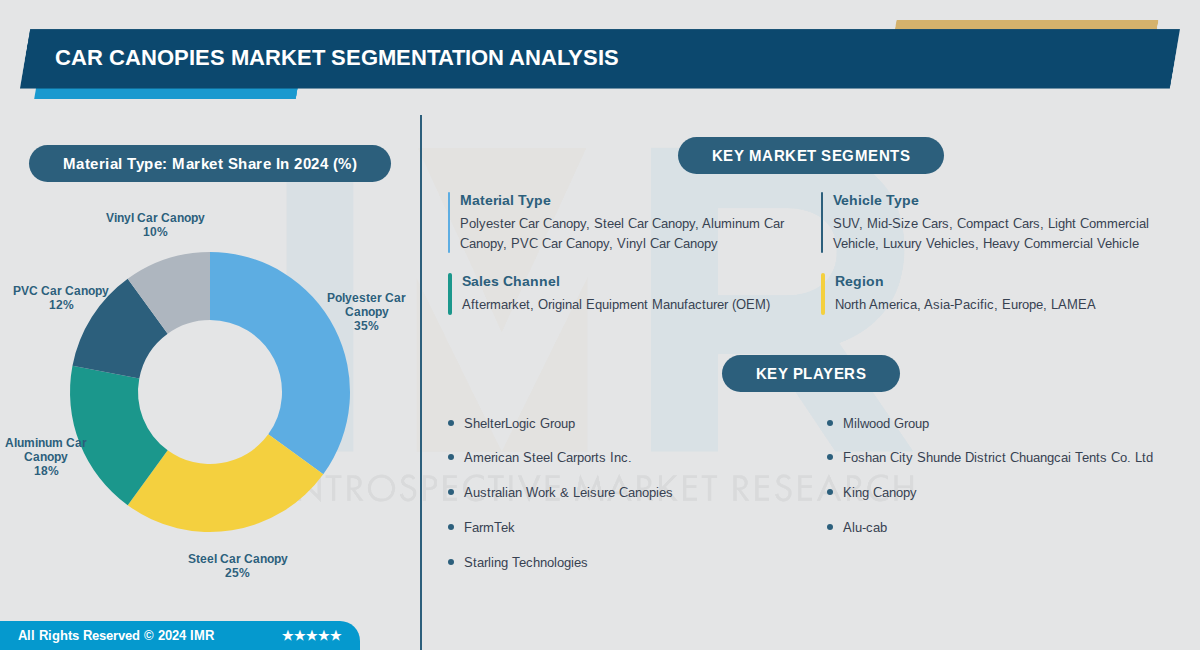

Car Canopies Market is Segmented on the basis of By Material Type, By Vehicle Type, By Sales Channel

By Material Type, Polyester Car Canopy segment is expected to dominate the market during the forecast period

- Polyester car canopies dominate due to their cost-effectiveness, versatility, and superior protection against UV rays and storms.

- They offer easy installation and economical pricing, driving higher adoption in both residential and commercial settings.

By Vehicle Type, SUV segment is expected to dominate the market during the forecast period

- SUVs lead due to their larger size requiring robust protection and popularity in regions with harsh weather conditions.

- High ownership rates of SUVs globally, combined with demand for durable outdoor shelters, boost their market dominance.

By Sales Channel, Aftermarket segment is expected to dominate the market during the forecast period

- Aftermarket dominates as consumers prefer customizable and affordable canopy options for existing vehicles.

- Rise in DIY installations and demand for portable solutions favor aftermarket over limited OEM integrations.

By Region, North America segment is expected to dominate the market during the forecast period

- North America leads due to high vehicle ownership, established manufacturers, and demand for weather protection.

- Well-developed automotive aftermarket and frequent extreme weather events drive significant canopy adoption.

Car Canopies Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast Period

- North America dominates the Car Canopies Market due to high pickup truck and SUV ownership, particularly in the United States, Canada, and Mexico. The region's strong aftermarket industry for customized vehicle accessories further solidifies its leadership position. This is complemented by a robust demand for vehicle protection in diverse climates.

- Well-developed infrastructure supports widespread vehicle usage, while favorable economic conditions and high disposable incomes enable consumers to invest in durable canopies. Regulations promoting fuel efficiency and light commercial vehicles also boost adoption. The automotive culture emphasizing personalization and outdoor activities drives consistent market growth.

- Key players like LEER Group, A.R.E. Mobile, and Truck Hero hold significant market share with innovative products featuring lightweight materials, lighting, and locking systems. Recent developments include advancements in canopy designs tailored for harsh weather in Canada and high customization in the U.S. These companies foster a competitive environment spurring further innovation.

Active Key Players in the Car Canopies Market:

- ShelterLogic Group (USA)

- Milwood Group (USA)

- American Steel Carports Inc. (USA)

- Foshan City Shunde District Chuangcai Tents Co. Ltd (China)

- Australian Work & Leisure Canopies (Australia)

- King Canopy (USA)

- FarmTek (USA)

- Alu-cab (South Africa)

- Starling Technologies (USA)

- Fleetline (USA)

- Peaktop (China)

- Caravan Canopy (USA)

- Lanmodo (China)

- Quictent (China)

- Abba Patio (USA)

- Yakima (USA)

- Roofnest (USA)

- 23Zero (Australia)

- Overland Vehicle Systems (USA)

- Other Active Players

|

Car Canopies Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 1.3 Billion |

|

Forecast Period 2024-2035 CAGR: |

5.5 % |

Market Size in 2035: |

USD 2.5 Billion |

|

Segments Covered: |

By Material Type |

|

|

|

By Vehicle Type |

|

||

|

By Sales Channel |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Car Canopies Market by Material Type (2017-2035)

4.1 Car Canopies Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Polyester Car Canopy

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Steel Car Canopy

4.5 Aluminum Car Canopy

4.6 PVC Car Canopy

4.7 Vinyl Car Canopy

Chapter 5: Car Canopies Market by Vehicle Type (2017-2035)

5.1 Car Canopies Market Snapshot and Growth Engine

5.2 Market Overview

5.3 SUV

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Mid-Size Cars

5.5 Compact Cars

5.6 Light Commercial Vehicle

5.7 Luxury Vehicles

5.8 Heavy Commercial Vehicle

Chapter 6: Car Canopies Market by Sales Channel (2017-2035)

6.1 Car Canopies Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Aftermarket

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Original Equipment Manufacturer (OEM)

Chapter 7: Car Canopies Market by Region (2017-2035)

7.1 Car Canopies Market Snapshot and Growth Engine

7.2 Market Overview

7.3 North America

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Asia-Pacific

7.5 Europe

7.6 LAMEA

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Car Canopies Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 SHELTERLOGIC GROUP

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 MILWOOD GROUP

8.4 AMERICAN STEEL CARPORTS INC.

8.5 FOSHAN CITY SHUNDE DISTRICT CHUANGCAI TENTS CO. LTD

8.6 AUSTRALIAN WORK & LEISURE CANOPIES

8.7 KING CANOPY

8.8 FARMTEK

8.9 ALU-CAB

8.10 STARLING TECHNOLOGIES

8.11 FLEETLINE

8.12 PEAKTOP

8.13 CARAVAN CANOPY

8.14 LANMODO

8.15 QUICTENT

8.16 ABBA PATIO

8.17 YAKIMA

8.18 ROOFNEST

8.19 23ZERO

8.20 OVERLAND VEHICLE SYSTEMS

Chapter 9: Global Car Canopies Market By Region

9.1 Overview

9.2. North America Car Canopies Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Car Canopies Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Car Canopies Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Car Canopies Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Car Canopies Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Car Canopies Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Car Canopies Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 1.3 Billion |

|

Forecast Period 2024-2035 CAGR: |

5.5 % |

Market Size in 2035: |

USD 2.5 Billion |

|

Segments Covered: |

By Material Type |

|

|

|

By Vehicle Type |

|

||

|

By Sales Channel |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||