Balsa Wood Market Synopsis:

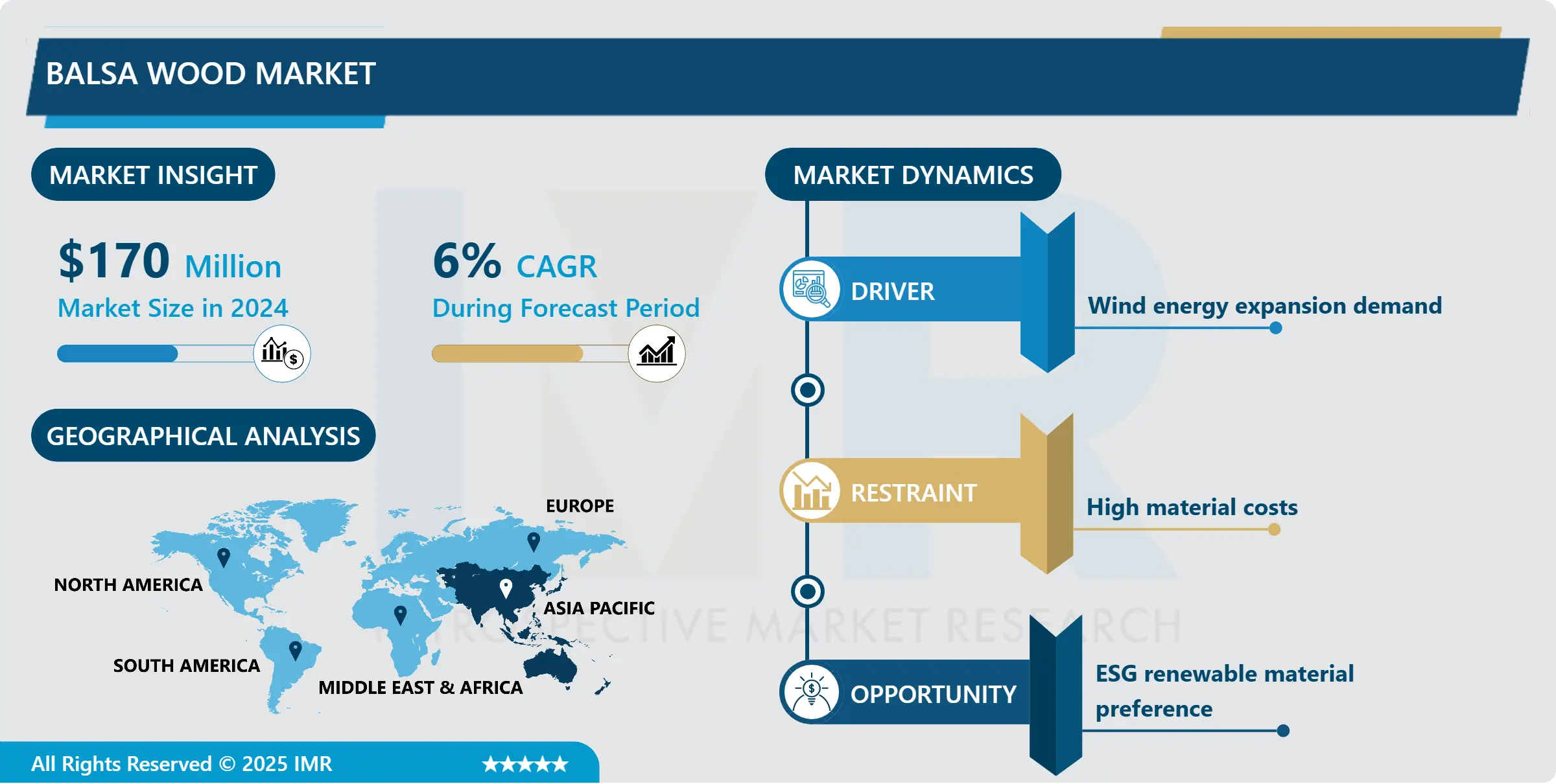

Balsa Wood Market Size Was Valued at USD 170.0 Million in 2024, and is Projected to Reach USD 322.8 Million by 2035, Growing at a CAGR of 6.0% From 2024-2035.

The global balsa wood market, valued at approximately $170 million in 2023, is a niche segment driven by its status as the lightest commercial timber, primarily sourced from plantations in Ecuador and Papua New Guinea. Balsa wood serves as a core material in structural sandwich panels for wind turbine blades, boats, aircraft, and aerospace applications, with demand fueled by its low density and fast growth characteristics.

Market projections vary across sources, but recent analyses indicate steady growth; for instance, the market is expected to reach $271 million by 2031 at a 6% CAGR, or $322.8 million by 2035 at 6.0% CAGR from a 2024 base of $170 million. Asia-Pacific dominates with over 37% share, led by China's wind turbine production and imports, while Europe benefits from offshore wind and marine sectors.

Key players include 3A Composites, Gurit, DIAB International, PNG Balsa Company, and Balsa USA, with grades like A and B catering to high-stiffness needs in blades and airframes. Regional dynamics show North America growing steadily due to renewables, and South America as a primary production hub.

Balsa Wood Market Trend Analysis:

Dominance of Wind Energy Applications

- Wind energy accounts for 51.35% of the balsa wood market in 2025, serving as the primary demand driver due to its use in turbine blades where longer designs and offshore installations require lightweight cores with high strength-to-weight ratios. Offshore wind projects are growing at an 8.08% CAGR, with companies like Vestas and Siemens Gamesa specifying Grade A balsa for blade root sections to handle harsher oceanic loads. North America leads with extensive installations in Texas and Iowa, supported by federal renewable energy initiatives that boosted U.S. wind capacity by over 10 GW in 2024.

- Asia-Pacific, holding 38.95% market share, imports 50% of global balsa volumes primarily for China's turbine manufacturing dominance, where Shandong Yulong Wood Industry processes imports for local blade production. Initiatives in Yunnan province target supplying 10% of domestic needs by 2024 to reduce overseas dependency amid rising turbine output. This trend sustains market growth projected from USD 270 million in 2025 to USD 366.55 million by 2031.

Surge in Sustainable Sourcing and Plantations

- Balsa USA and Pacific Balsa are leading initiatives in plantation-grown balsa to promote environmental sustainability, highlighted at the International Balsa Wood Conference 2023, addressing deforestation concerns from native Ecuadorian forests. These efforts meet rising demand for certified eco-friendly materials in green building standards, particularly in GCC countries where mega infrastructure projects emphasize alternatives to synthetics. Middle East imports from Latin America support a 15.5% regional share in 2025, driven by sustainable construction investments.

- Government policies in China and the U.S. encourage lightweight sustainable materials, with Gurit Holdings investing in supply chain partnerships for responsibly sourced balsa in renewable energy and automotive sectors. Innovations in wood treatment enhance durability, broadening use in hybrid composites while complying with tightening environmental regulations globally. North American preference for bio-based materials fuels adoption, with the region holding over 30% global revenue share.

Expansion in Aerospace and Defense Composites

- Aerospace and defense segments claim 42.7% market share in 2025, utilizing balsa's unmatched strength-to-weight ratio in aircraft components, missile systems, and eVTOL structures for fuel efficiency and load capacities. India's National Aerospace Program and U.S. investments in lightweight composites for satellite panels drive demand, with Grade A balsa at 42.60% share growing at 6.31% CAGR for high-stiffness applications.

- Key players like Gurit Holdings supply treated balsa cores for marine performance yachts and defense rail-car floors, where Grade C offers impact tolerance. U.S. composites manufacturing imports extensively from Latin America, supported by government sustainability programs enhancing structural performance in recreational boating and defense.

Balsa Wood Market Segment Analysis:

Balsa Wood Market is Segmented on the basis of By Type, By Application, By Region

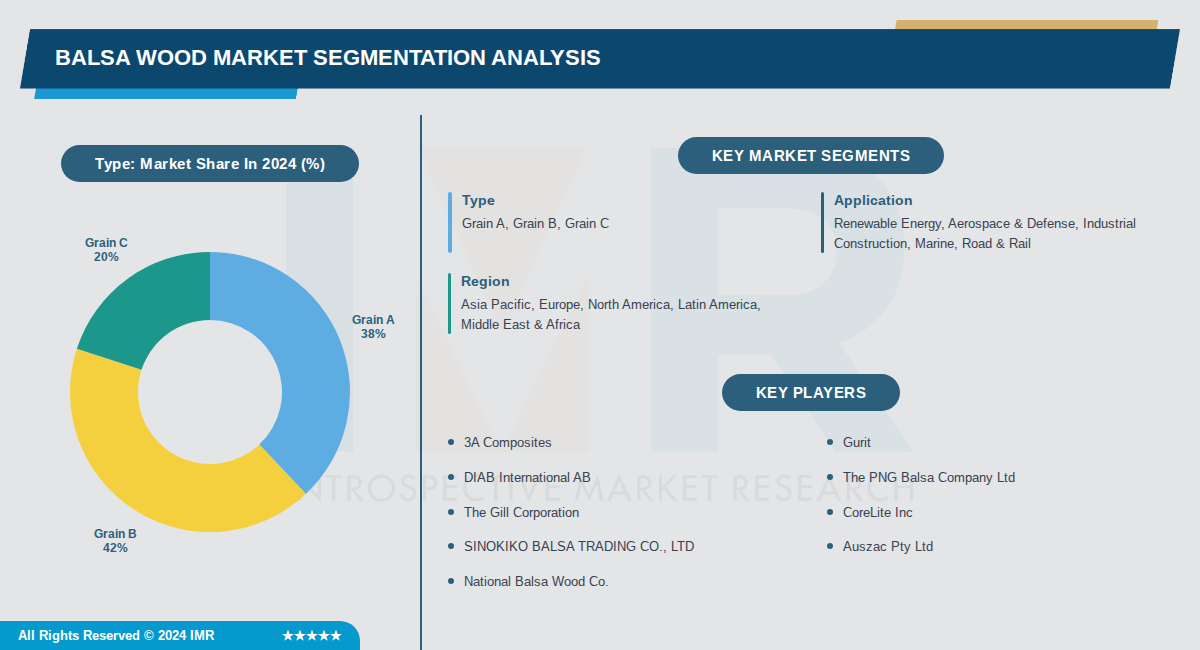

By Type, Grain B segment is expected to dominate the market during the forecast period

- Grain B dominates as it is classified as all-purpose balsa wood suitable for a wide range of applications including planks and general structural uses.

- Multiple reports confirm Grain B holds the largest share around 41-42% due to its versatility and high demand across industries like renewable energy and aerospace.

By Application, Renewable Energy segment is expected to dominate the market during the forecast period

- Renewable Energy, particularly wind energy turbine blades, dominates due to balsa wood's superior strength-to-weight ratio and insulation properties essential for lightweight cores.

- Wind energy segment accounted for the largest revenue share of 45.1% as global capacity expansions drive massive demand for balsa sandwich composites.

By Region, Asia Pacific segment is expected to dominate the market during the forecast period

- Asia Pacific leads with shares around 37-39% driven by rapid wind energy installations in China and expanding manufacturing bases.

- The region's dominance stems from high renewable energy investments and proximity to key balsa suppliers in South America facilitating supply chains.

Balsa Wood Market Regional Insights:

Asia Pacific Dominates the Balsa Wood Market with Over 67% Share

- Asia Pacific commands the largest market share at 67.9% in 2025, driven by key countries like China, India, Japan, South Korea, and Indonesia. China leads in turbine production and imports around 50% of global balsa volumes, while rapid industrialization boosts demand across the region. This dominance stems from the region's position as a hub for renewable energy and lightweight material applications.

- The region benefits from low-cost labor, fast-growing economies, and suitability for balsa cultivation, with increasing processors emerging. Infrastructure supports expanding industries like wind energy and aerospace, while government initiatives in areas like China's Yunnan province aim to meet domestic needs and reduce import reliance. These factors, combined with urbanization and industrial expansion, propel sustained market leadership.

- Major developments include scaling of trimming and lamination facilities in Vietnam and Indonesia for export chains, alongside India's National Aerospace Program increasing composite use. Key players focus on regional supply chains feeding Asian blade factories, with projections for 5.48% annual growth through 2031. Recent plantation expansions and processing investments solidify Asia Pacific's position.

Active Key Players in the Balsa Wood Market:

- 3A Composites (Switzerland)

- Gurit (Spain)

- DIAB International AB (Sweden)

- The PNG Balsa Company Ltd (Papua New Guinea)

- The Gill Corporation (USA)

- CoreLite Inc (USA)

- SINOKIKO BALSA TRADING CO., LTD (China)

- Auszac Pty Ltd (Australia)

- National Balsa Wood Co. (USA)

- Specialized Balsa LLC (USA)

- Sig Manufacturing (USA)

- Lone Star Balsa (USA)

- Schweiter Technologies AG (Switzerland)

- 3A Composites GmbH (Switzerland)

- Balsa Wood Panama S.A. (Panama)

- Greenlight Balsa (Ecuador)

- Baltek Corporation (USA)

- Other Active Players

|

Balsa Wood Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 170.0 Million |

|

Forecast Period 2024-2035 CAGR: |

6.0 % |

Market Size in 2035: |

USD 322.8 Million |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Balsa Wood Market by Type (2017-2035)

4.1 Balsa Wood Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Grain A

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Grain B

4.5 Grain C

Chapter 5: Balsa Wood Market by Application (2017-2035)

5.1 Balsa Wood Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Renewable Energy

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Aerospace & Defense

5.5 Industrial Construction

5.6 Marine

5.7 Road & Rail

Chapter 6: Balsa Wood Market by Region (2017-2035)

6.1 Balsa Wood Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Asia Pacific

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Europe

6.5 North America

6.6 Latin America

6.7 Middle East & Africa

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Balsa Wood Market Share by Manufacturer/Service Provider (2024)

7.1.3 Industry BCG Matrix

7.1.4 Partnerships, Mergers & Acquisitions

7.2 3A COMPOSITES

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Recent News & Developments

7.2.10 SWOT Analysis

7.3 GURIT

7.4 DIAB INTERNATIONAL AB

7.5 THE PNG BALSA COMPANY LTD

7.6 THE GILL CORPORATION

7.7 CORELITE INC

7.8 SINOKIKO BALSA TRADING CO.

7.9 LTD

7.10 AUSZAC PTY LTD

7.11 NATIONAL BALSA WOOD CO.

7.12 SPECIALIZED BALSA LLC

7.13 SIG MANUFACTURING

7.14 LONE STAR BALSA

7.15 SCHWEITER TECHNOLOGIES AG

7.16 3A COMPOSITES GMBH

7.17 BALSA WOOD PANAMA S.A.

7.18 GREENLIGHT BALSA

7.19 BALTEK CORPORATION

Chapter 8: Global Balsa Wood Market By Region

8.1 Overview

8.2. North America Balsa Wood Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecast Market Size by Country

8.3. Eastern Europe Balsa Wood Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecast Market Size by Country

8.4. Western Europe Balsa Wood Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecast Market Size by Country

8.5. Asia Pacific Balsa Wood Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecast Market Size by Country

8.6. Middle East & Africa Balsa Wood Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecast Market Size by Country

8.7. South America Balsa Wood Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecast Market Size by Country

Chapter 9: Analyst Viewpoint and Conclusion

Chapter 10: Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

Chapter 11: Case Study

Chapter 12: Appendix

12.1 Sources

12.2 List of Tables and Figures

12.3 Short Forms and Citations

12.4 Assumption and Conversion

12.5 Disclaimer

|

Balsa Wood Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 170.0 Million |

|

Forecast Period 2024-2035 CAGR: |

6.0 % |

Market Size in 2035: |

USD 322.8 Million |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||