Automotive Plastic Grille Market Synopsis:

Automotive Plastic Grille Market Size Was Valued at USD 11.0 Billion in 2024, and is Projected to Reach USD 15.0 Billion by 2035, Growing at a CAGR of 3.0% From 2024-2035.

The Automotive Plastic Grille Market is valued at $11.0 billion in 2024 and is projected to reach $15.0 billion by 2035, growing at a compound annual growth rate (CAGR) of 3.0%. This market encompasses plastic components used in vehicle front ends for aesthetic, aerodynamic, and functional purposes, with plastics favored for their lightweight properties over traditional metal alternatives.

Plastic grilles, primarily made from materials like ABS plastic, offer advantages in weight reduction, design flexibility, and cost-effectiveness, aligning with industry trends toward fuel efficiency and emission reductions. The market benefits from rising automotive production, particularly in passenger cars and SUVs, where prominent grille designs enhance brand identity and vehicle appeal.

Regionally, Asia Pacific leads due to its expansive manufacturing base in countries like China, Japan, and India, holding significant market share driven by high vehicle output and supportive policies for lightweight materials. North America and Europe follow, propelled by demand for customization, EVs, and advanced designs integrating sensors for ADAS.

Automotive Plastic Grille Market Trend Analysis:

Redesign of Grilles for Electric Vehicles

- With reduced need for massive airflow to a radiator, EV grilles are being fundamentally reimagined as sculptural and aerodynamic components. Some are completely sealed, featuring integrated lighting, sensors for ADAS systems, and display elements, effectively transforming the traditional grille area into a technology-focused design panel rather than a purely functional cooling component.

- The shift toward EV grille design is creating an entirely new product category with substantial market opportunity. As EV sales surge globally, manufacturers are developing innovative front-end designs that optimize aerodynamics to improve battery range while incorporating advanced sensing technologies for autonomous driving capabilities, with China leading this innovation as the world's largest EV market.

- This trend is expected to drive the fastest growth in the automotive grille market over the forecast period. The electric vehicle segment represents the single biggest opportunity, fundamentally altering the primary function of front-end modules from engine cooling to aerodynamic optimization and sensor integration.

Shift Toward Lightweight Materials and Advanced Composites

- Manufacturers are increasingly adopting lightweight materials like aluminum, carbon fiber-reinforced polymers (CFRP), and advanced injection-molded thermoplastics to reduce vehicle weight and improve fuel efficiency. Aluminum currently dominates due to its excellent strength-to-weight ratio and corrosion resistance, while carbon fiber grilles offer the ultimate in lightweighting and high-performance aesthetics for premium vehicle segments.

- Plastic grilles are gaining significant popularity due to their cost-effectiveness and design flexibility, particularly for electric vehicles where aerodynamic efficiency is critical. These advanced plastics can be painted and finished to high standards while offering greater weight savings and design freedom compared to traditional metallic options, making them especially attractive for the emerging EV segment.

- Lightweighting initiatives continue to gain momentum as a core strategy for meeting emissions regulations and improving vehicle performance. The pursuit of fuel efficiency and reduced emissions is pushing automakers to adopt these advanced materials across all vehicle segments, with plastic and composite grilles becoming increasingly common in both OEM production and aftermarket applications.

Customization and Personalization Through Aftermarket Innovation

- Consumers are increasingly seeking unique grille designs to personalize their vehicles, driving significant growth in the aftermarket segment. CNC-machined custom grilles, mesh designs, and chrome finishes are becoming popular choices, with manufacturers offering greater design flexibility to enhance the unique character of individual vehicles and support consumer expression.

- The aftermarket segment represents a significant and growing source of demand fueled by vehicle customization culture, replacement grille needs after collisions, and the desire to upgrade the aesthetic appearance of existing vehicles. North America remains a key market for bold designs and aftermarket customization, while personalization trends continue to expand globally.

- Advanced manufacturing technologies like CNC machining are enabling high-growth, higher-margin customization opportunities in the grille market. This trend offers manufacturers differentiation potential through tailored designs, premium material choices like carbon fiber, and integration of illuminated grille technology with advanced lighting and display elements.

Automotive Plastic Grille Market Segment Analysis:

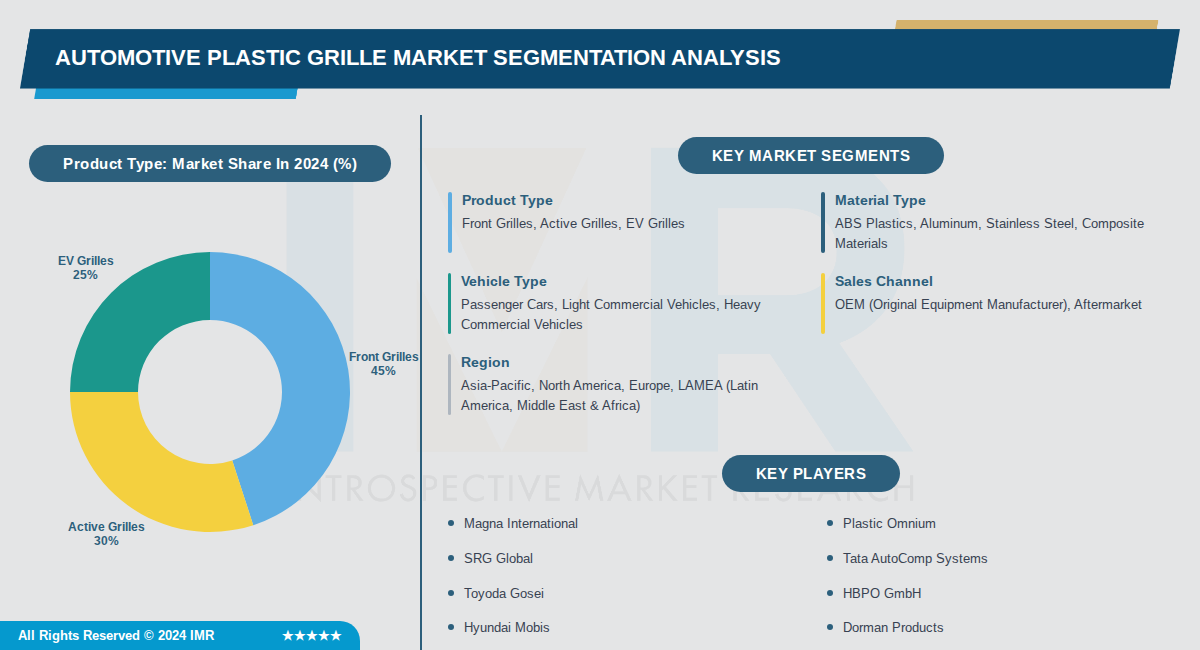

Automotive Plastic Grille Market is Segmented on the basis of By Product Type, By Material Type, By Vehicle Type

By Product Type, Front Grilles segment is expected to dominate the market during the forecast period

- Front grilles dominate the market as they remain the standard aesthetic and functional component for all vehicle types, with established manufacturing processes and widespread OEM adoption across passenger and commercial vehicles.

- The segment benefits from high production volumes in mass-market vehicles where plastic grilles provide optimal cost-effectiveness and design flexibility compared to metal alternatives.

By Material Type, ABS Plastics segment is expected to dominate the market during the forecast period

- ABS plastics dominate the automotive plastic grille market with 58% share due to their lightweight properties, cost-effectiveness, and superior design flexibility that allows manufacturers to innovate while maintaining affordability for mass-market vehicles.

- The plastic segment captures the majority of production because it enables fuel efficiency improvements and reduced carbon emissions—critical factors driving OEM adoption across electric and hybrid vehicle platforms.

By Vehicle Type, Passenger Cars segment is expected to dominate the market during the forecast period

- Passenger cars dominate with 62% market share driven by significantly higher global production volumes, increasing consumer demand supported by rising urbanization and improved disposable incomes across emerging markets.

- This segment benefits from continuous innovation in plastic grille designs for electric and hybrid platforms, where OEMs prioritize lightweight solutions to maximize battery efficiency and vehicle range.

By Sales Channel, OEM (Original Equipment Manufacturer) segment is expected to dominate the market during the forecast period

- OEM sales dominate with 78% share as automotive manufacturers require standardized plastic grille components integrated during vehicle production to meet design and cooling specifications for their platforms.

- The OEM segment sustains high volumes through long-term supply contracts with major automakers including Ford, General Motors, Toyota, Volkswagen, and Asian manufacturers capitalizing on growing electric vehicle production.

By Region, Asia-Pacific segment is expected to dominate the market during the forecast period

- Asia-Pacific leads with 38% market share driven by the highest automotive production volumes globally, particularly in China and India, combined with rapid adoption of electric vehicles and expanding vehicle manufacturing infrastructure.

- This region captures the fastest growth trajectory due to increasing e-commerce logistics demand driving commercial vehicle production, rising consumer vehicle ownership, and significant aftermarket opportunities as existing vehicle fleets require replacement components.

Automotive Plastic Grille Market Regional Insights:

Asia Pacific Dominates the Automotive Plastic Grille Market

- Asia Pacific commands the largest market share due to its position as the global hub for vehicle manufacturing, with China, India, and Japan leading production volumes. High sales of passenger cars and commercial vehicles, including electric models, create substantial demand for plastic grilles. Extensive aftermarket opportunities further bolster the region's dominance.

- Rapid urbanization, rising disposable incomes, and government initiatives promoting electric vehicles drive market growth. The shift toward aerodynamic designs for energy efficiency and sensor integration in EVs supports plastic grille adoption. Less stringent emissions norms compared to Europe still encourage innovations in cooling and aerodynamics.

- Major OEMs and suppliers have established R&D and manufacturing facilities in the region to meet surging demand. Companies focus on lightweight ABS plastics for better fuel efficiency and aesthetics. Recent developments include product evolution for electric mobility, with strong aftermarket presence in China and India.

Active Key Players in the Automotive Plastic Grille Market:

- Magna International (Canada)

- Plastic Omnium (France)

- SRG Global (USA)

- Tata AutoComp Systems (India)

- Toyoda Gosei (Japan)

- HBPO GmbH (Germany)

- Hyundai Mobis (South Korea)

- Dorman Products (USA)

- Putco (USA)

- T-Rex Truck Products (USA)

- Westin Automotive (USA)

- Roush Enterprises (USA)

- FALTEC Co. Ltd. (Japan)

- Lacks Enterprises (USA)

- Sakae Riken Kogyo (Japan)

- Samshin Chemical (South Korea)

- Hangzhou Yiyang Auto Parts (China)

- Zhejiang Ruitai Auto Parts (China)

- Other Active Players

|

Automotive Plastic Grille Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 11.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

3.0 % |

Market Size in 2035: |

USD 15.0 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Material Type |

|

||

|

By Vehicle Type |

|

||

|

By Sales Channel |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Automotive Plastic Grille Market by Product Type (2017-2035)

4.1 Automotive Plastic Grille Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Front Grilles

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Active Grilles

4.5 EV Grilles

Chapter 5: Automotive Plastic Grille Market by Material Type (2017-2035)

5.1 Automotive Plastic Grille Market Snapshot and Growth Engine

5.2 Market Overview

5.3 ABS Plastics

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Aluminum

5.5 Stainless Steel

5.6 Composite Materials

Chapter 6: Automotive Plastic Grille Market by Vehicle Type (2017-2035)

6.1 Automotive Plastic Grille Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Passenger Cars

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Light Commercial Vehicles

6.5 Heavy Commercial Vehicles

Chapter 7: Automotive Plastic Grille Market by Sales Channel (2017-2035)

7.1 Automotive Plastic Grille Market Snapshot and Growth Engine

7.2 Market Overview

7.3 OEM (Original Equipment Manufacturer)

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Aftermarket

Chapter 8: Automotive Plastic Grille Market by Region (2017-2035)

8.1 Automotive Plastic Grille Market Snapshot and Growth Engine

8.2 Market Overview

8.3 Asia-Pacific

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

8.3.3 Key Market Trends, Growth Factors, and Opportunities

8.3.4 Geographic Segmentation Analysis

8.4 North America

8.5 Europe

8.6 LAMEA (Latin America

8.7 Middle East & Africa)

Chapter 9: Company Profiles and Competitive Analysis

9.1 Competitive Landscape

9.1.1 Competitive Benchmarking

9.1.2 Automotive Plastic Grille Market Share by Manufacturer/Service Provider (2024)

9.1.3 Industry BCG Matrix

9.1.4 Partnerships, Mergers & Acquisitions

9.2 MAGNA INTERNATIONAL

9.2.1 Company Overview

9.2.2 Key Executives

9.2.3 Company Snapshot

9.2.4 Role of the Company in the Market

9.2.5 Sustainability and Social Responsibility

9.2.6 Operating Business Segments

9.2.7 Product Portfolio

9.2.8 Business Performance

9.2.9 Recent News & Developments

9.2.10 SWOT Analysis

9.3 PLASTIC OMNIUM

9.4 SRG GLOBAL

9.5 TATA AUTOCOMP SYSTEMS

9.6 TOYODA GOSEI

9.7 HBPO GMBH

9.8 HYUNDAI MOBIS

9.9 DORMAN PRODUCTS

9.10 PUTCO

9.11 T-REX TRUCK PRODUCTS

9.12 WESTIN AUTOMOTIVE

9.13 ROUSH ENTERPRISES

9.14 FALTEC CO. LTD.

9.15 LACKS ENTERPRISES

9.16 SAKAE RIKEN KOGYO

9.17 SAMSHIN CHEMICAL

9.18 HANGZHOU YIYANG AUTO PARTS

9.19 ZHEJIANG RUITAI AUTO PARTS

Chapter 10: Global Automotive Plastic Grille Market By Region

10.1 Overview

10.2. North America Automotive Plastic Grille Market

10.2.1 Key Market Trends, Growth Factors and Opportunities

10.2.2 Top Key Companies

10.2.3 Historic and Forecasted Market Size by Segments

10.2.4 Historic and Forecast Market Size by Country

10.3. Eastern Europe Automotive Plastic Grille Market

10.3.1 Key Market Trends, Growth Factors and Opportunities

10.3.2 Top Key Companies

10.3.3 Historic and Forecasted Market Size by Segments

10.3.4 Historic and Forecast Market Size by Country

10.4. Western Europe Automotive Plastic Grille Market

10.4.1 Key Market Trends, Growth Factors and Opportunities

10.4.2 Top Key Companies

10.4.3 Historic and Forecasted Market Size by Segments

10.4.4 Historic and Forecast Market Size by Country

10.5. Asia Pacific Automotive Plastic Grille Market

10.5.1 Key Market Trends, Growth Factors and Opportunities

10.5.2 Top Key Companies

10.5.3 Historic and Forecasted Market Size by Segments

10.5.4 Historic and Forecast Market Size by Country

10.6. Middle East & Africa Automotive Plastic Grille Market

10.6.1 Key Market Trends, Growth Factors and Opportunities

10.6.2 Top Key Companies

10.6.3 Historic and Forecasted Market Size by Segments

10.6.4 Historic and Forecast Market Size by Country

10.7. South America Automotive Plastic Grille Market

10.7.1 Key Market Trends, Growth Factors and Opportunities

10.7.2 Top Key Companies

10.7.3 Historic and Forecasted Market Size by Segments

10.7.4 Historic and Forecast Market Size by Country

Chapter 11: Analyst Viewpoint and Conclusion

Chapter 12: Research Methodology

12.1 Research Process

12.2 Primary Research

12.3 Secondary Research

Chapter 13: Case Study

Chapter 14: Appendix

14.1 Sources

14.2 List of Tables and Figures

14.3 Short Forms and Citations

14.4 Assumption and Conversion

14.5 Disclaimer

|

Automotive Plastic Grille Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 11.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

3.0 % |

Market Size in 2035: |

USD 15.0 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Material Type |

|

||

|

By Vehicle Type |

|

||

|

By Sales Channel |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||