Anal Cancer Market Synopsis

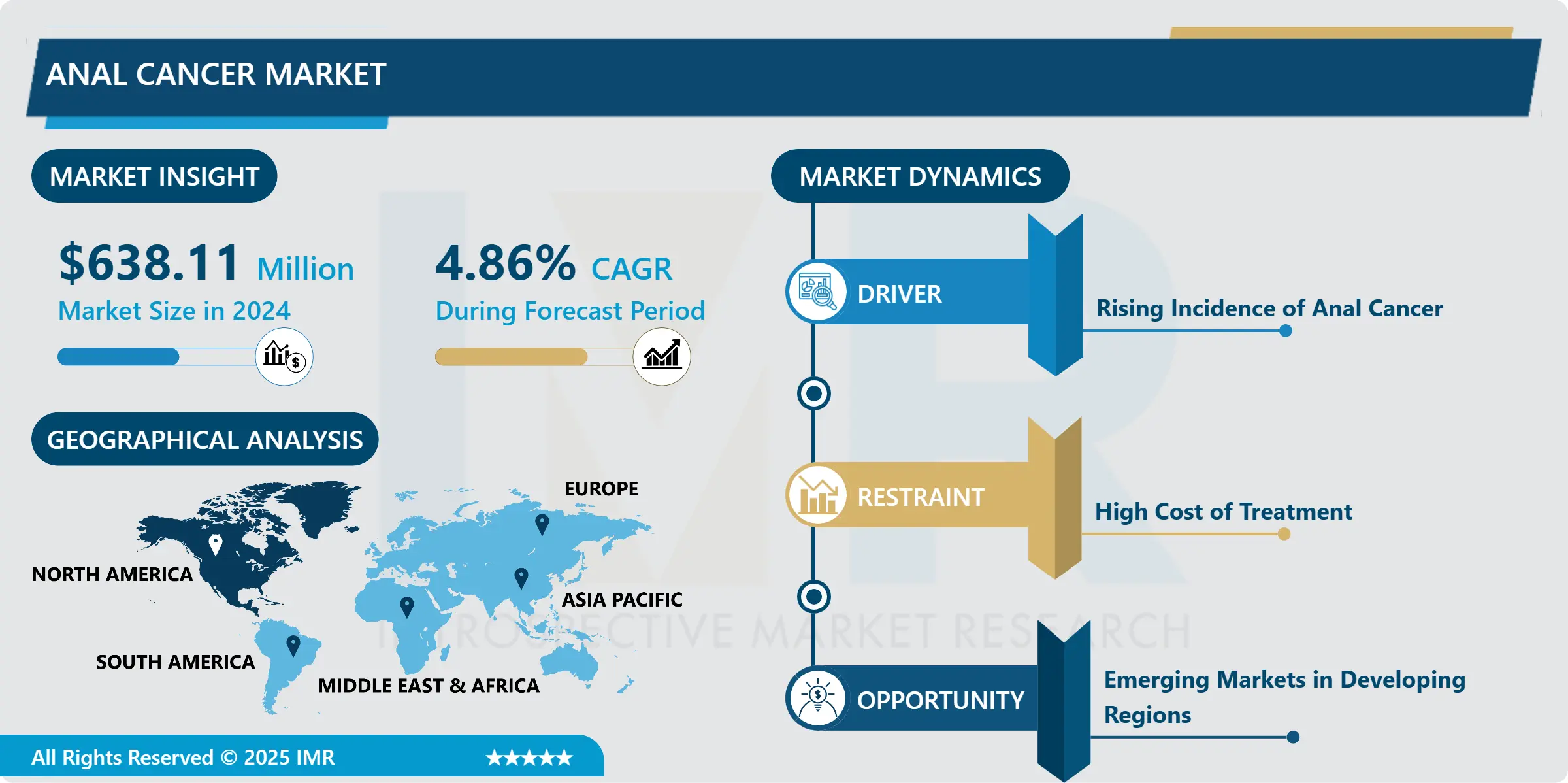

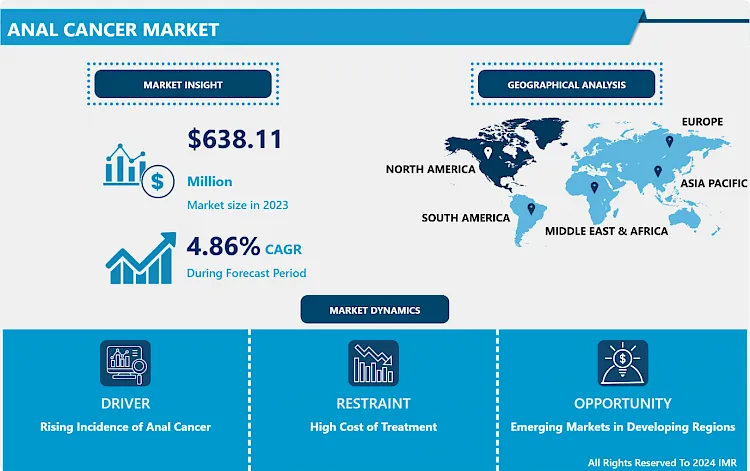

Anal Cancer Market Size was valued at USD 638.11 Million in 2024, and is Projected to Reach USD 978.10 Million by 2035, Growing at a CAGR of 4.86% From 2025-2035.

The anal cancer market is involved with products such as treatments and diagnostic services that can be utilized with anal cancer, which is a type of cancer that begins in the tissues of the anus. They include surgery, radiation therapy, chemotherapy, immunotherapy and targeted therapy with an aim of treating patients diagnosed with anal cancer. The main driving force is growing incidence of anal cancer, improvement in diagnostic methods, as well as the emergence of new therapeutic strategies.

Drugs for anal cancer has steadily grown over the years because there is continual increase in the global prevalence of anal cancer, and the utilization of new diagnostic techniques and therapeutic approaches. Cancer of the anus is rare, but incidence has been increasing, especially among immunocompromised persons, including those with human immunodeficiency virus (HIV) infection. The need to increase the efficiency and accessibility of intervention has become a need as such. The market is, therefore, polarized by both traditional therapies such as surgery and chemotherapy and modern therapies such as immunotherapy and precision medicine. It is apparent that there is great competition in the market since many pharmaceutical industry players, as well as healthcare centers, design and synthesize drugs, vaccines, or diagnostic devices due to the constantly increasing demand in the presence of treatments.

The market has been revolutionized through technological development in imaging and diagnostic procedure which have enhanced early diagnosis. In addition, the appearance of molecular or personally tailored medicine, where therapy is adapted in accordance with a patient’s genetic characteristics, has offered more work for improved treatment methods. Even so, there are significant trends in the anal cancer market such as escalating treatment costs, low public awareness of anal cancer, and social stigmatization of the disease, which may slow down the chances of diagnosis and treatment. But there are expectations that activities from the side of public health organizations as well as cancer advocacy organizations will reduce some of these problems in future.

The market is also investing and research in new therapeutic products to make an advanced impact on health and narrow the harming effects on the patient. The two forms of therapy, immunotherapy and targeted therapy, have received enhanced funding in the field of cancer and this has resulted to entry of a number of new drug candidates in the market. In addition, close corporation between academic institutions, biotechnology firms and pharmaceutical industries may shape the future of anal cancer treatment. Due to the increasing emphasis on increasing rates of survival and enhancing the quality of life in all patients, the anal cancer market should also demonstrate further development in the next few years, in both emerging and developed countries.

Anal Cancer Market Trend Analysis:

Adoption of Immunotherapy

- Immunotherapy has become one of the prominent trends within the anal cancer treatment. This cancer treatment strategy is considered to have an immune system mobilizing effect because it triggers the body’s immune system to target the cancer cells. Recent studies have reported relative effectiveness of immune checkpoint inhibitors, including pembrolizumab and nivolumab, in the treatment of non-IHC evaluable advanced anal cancer in patients who have not had success with standard treatments. Immunotherapy as a clinical treatment modality has recently received considerable attention and can enhance the prognosis of anal cancer patients considerably.

- Therefore, enhancing the emergence and adoption of immunotherapeutic drugs has attracted the attention of pharmaceutical firms. This trend is anticipated to intensify when clinical trials are complete, and when more clinical studies of immunotherapy combined with other therapy forms such as chemotherapy and radiation are conducted. Immunotherapy may be a game changer in anal cancer treatment when less toxic and more targeted treatment approaches are sought as a means of enhancing patients’ survival.

Emerging Markets in Developing Regions

- Another advantage of the anal cancer market is that the treatment and networks are being advanced in developing nations. With enhancement in the health standards of the developing countries the judicial access to the sophisticated cancer therapy, even in the case of anal cancer is being enhanced. This trend shall therefore help see an increase in cases of anal cancer in areas which were not commonly diagnosed with the disease or that utilized wrong treatment techniques. The rise in popularity of relatively new forms of treatment like immunotherapy and precision medicine, creates novel opportunities for pharma companies to build a market in these locations.

- Furthermore, elevating consciousness of cancer in developing area owing to government and global health organization’s campagnes is also enhancing the demand of Anal cancer treatment. In this regard, as the healthcare capacities of these regions increase, there will be a demand for the anal cancer market. As a result, companies can look forward to address those regions with affordable and easily accessible treatments, cater to the increased patient population and provide treatments of better quality to patients who need it the most all in an under saturated market.

Anal Cancer Market Segment Analysis:

Anal Cancer Market is segmented on the basis of Type, Treatment Type, Distribution Channel, End User, and Region.

By Type, Squamous Cell Carcinoma segment is expected to dominate the market during the forecast period

- Most anal cancers are SCC, which makes up about 90 % of the cancers of the anus globally. For this reason, it typically develops in the squamous cells that form the lining of the anal canal. SCC is closely associated with HPV infections that are primary risk factors for the development of this cancer. Squamous cell carcinoma has surgical treatment, chemotherapy, radiation therapy, and immunotherapy for the treatment depending on the stage of the tumour as well as the area of the body affected. There are chances for such anal cancers to have therapeutic strategies based on blockade of the pathways responsive to HPV.

- Adenocarcinoma of the anus is much less common than squamous cell carcinoma but nonetheless accounts for a significant portion of the anal cancer business. This type of cancer begins in the glandular cells lining the anal canal. Adenocarcinoma is thus a more challenging diagnosis and managing as it has commonly been diagnosed at later stages than squamous cell carcinoma. Adenocarcinoma can only be cured through surgery, radiotherapy and or chemotherapy just like the other adenocarcinomas. In future the biomolecular and hereditary differentiation might enhance the treatment of adenocarcinoma patients.

By End User, Hospitals segment expected to held the largest share

- Anticipating that the numbers would grow in the future, hospitals are the primary consumer of anal cancer treatments which includes diagnosis and treatment. As a result of the involvement of many specialists, health centres are in a position to organisations to manage the treatment of anal cancer which may composure surgery, chemotherapy and radiation therapy. While the rate at which the disease is developing has risen, patients can still rely on hospitals in receiving optimal anal cancer treatment and access to some of the newest latest technologies.

- Efforts toward the understanding of anal cancer and the discovery of new therapies for the disease are all made possible by cancer research institutes. These institutions are centred on investigating new treatments which are immunotherapy and targeted treatment among others. Relationships between the pharmaceutical industry and research institutes, specialised healthcare providers, are critical for the development of new therapies, and these institutes are capacitative in the further development of anal cancer market through executions of clinical trials and research.

Anal Cancer Market Regional Insights:

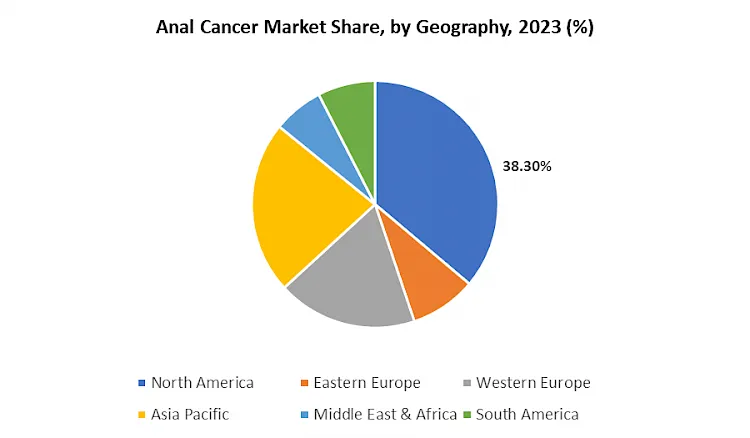

North America is Expected to Dominate the Market Over the Forecast period

- North America is considered to be the market leader in the anal cancer hemisphere at the moment. This is primarily because the area has well-developed medical systems and qualified healthcare; people in this region have early access to modern treatments; and cancer rates are rapidly increasing due to regular health checks. The United State and Canada are still the gallop in terms of advancement with Immunotherapy and Personalized medicine. The high level of healthcare spend across the North American population has made it possible for patients to access state-of-art therapies which have suppressed the regional market for cancer treatments.

- Also, activities such driving voluntary HPV vaccinations and detecting anal cancer in its early stages contribute to decreased incidences of late-stage discoveries and improved patients’ prognosis. The prospects of major suppliers in North America coupled with high investment in cancer research are expected to further support the market growth. This region’s lead is expected to be sustained by continuous developments in the diagnostic procedures and the existing diverse treatment methods.

Active Key Players in the Anal Cancer Market

- Bristol Myers Squibb (United States)

- Merck & Co. (United States)

- Sanofi (France)

- Amgen (United States)

- Gilead Sciences (United States)

- Bayer AG (Germany)

- Novartis (Switzerland)

- Pfizer Inc. (United States)

- Eli Lilly and Company (United States)

- Roche (Switzerland)

- AbbVie Inc. (United States)

- Johnson & Johnson (United States)

- Other Active Players

Key Industry Developments in Anal Cancer Market:

- In September 2024, Incyte announced that its Phase 3 POD1UM-303/InterAACT2 trial of retifanlimab (Zynyz®), in combination with platinum-based chemotherapy, met its primary endpoint of progression-free survival (PFS) in patients with squamous cell anal carcinoma (SCAC). Results, presented at the ESMO Congress 2024, showed a 37% reduction in the risk of progression or death, with a median PFS of 9.3 months for the treatment group. Incyte plans to file a supplemental Biologics License Application for retifanlimab in SCAC by year-end 2024.

- In February 2024. Oncolytics Biotech® Inc. announced an expansion of enrollment for the anal cancer cohort of the GOBLET study, evaluating pelareorep in combination with atezolizumab (Tecentriq®) for patients with unresectable squamous cell carcinoma of the anal canal. This decision follows promising Stage 1 data presented at the IMACC 2023, showing a 37.5% objective response rate, including a long-lasting complete response, significantly exceeding previous checkpoint inhibitor therapy results.

|

Anal Cancer Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 638.11 Million |

|

Forecast Period 2025-35 CAGR: |

4.86% |

Market Size in 2035: |

USD 978.10 Million |

|

Segments Covered: |

By Type |

|

|

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Anal Cancer Market by Type (2018-2035)

4.1 Anal Cancer Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Squamous Cell Carcinoma

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Adenocarcinoma

4.5 Others

Chapter 5: Anal Cancer Market by End User (2018-2035)

5.1 Anal Cancer Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Hospitals

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Cancer Research Institutes

5.5 Specialty Clinics

5.6 Others

Chapter 6: Company Profiles and Competitive Analysis

6.1 Competitive Landscape

6.1.1 Competitive Benchmarking

6.1.2 Anal Cancer Market Share by Manufacturer (2024)

6.1.3 Industry BCG Matrix

6.1.4 Heat Map Analysis

6.1.5 Mergers and Acquisitions

6.2 BRISTOL MYERS SQUIBB (UNITED STATES)

6.2.1 Company Overview

6.2.2 Key Executives

6.2.3 Company Snapshot

6.2.4 Role of the Company in the Market

6.2.5 Sustainability and Social Responsibility

6.2.6 Operating Business Segments

6.2.7 Product Portfolio

6.2.8 Business Performance

6.2.9 Key Strategic Moves and Recent Developments

6.2.10 SWOT Analysis

6.3 MERCK & CO. (UNITED STATES)

6.4 SANOFI (FRANCE)

6.5 AMGEN (UNITED STATES)

6.6 GILEAD SCIENCES (UNITED STATES)

6.7 BAYER AG (GERMANY)

6.8 NOVARTIS (SWITZERLAND)

6.9 PFIZER INC. (UNITED STATES)

6.10 ELI LILLY AND COMPANY (UNITED STATES)

6.11 ROCHE (SWITZERLAND)

6.12 ABBVIE INC. (UNITED STATES)

6.13 JOHNSON & JOHNSON (UNITED STATES)

Chapter 7: Global Anal Cancer Market By Region

7.1 Overview

7.2. North America Anal Cancer Market

7.2.1 Key Market Trends, Growth Factors and Opportunities

7.2.2 Top Key Companies

7.2.3 Historic and Forecasted Market Size by Segments

7.2.4 Historic and Forecasted Market Size by Type

7.2.4.1 Squamous Cell Carcinoma

7.2.4.2 Adenocarcinoma

7.2.4.3 Others

7.2.5 Historic and Forecasted Market Size by End User

7.2.5.1 Hospitals

7.2.5.2 Cancer Research Institutes

7.2.5.3 Specialty Clinics

7.2.5.4 Others

7.2.6 Historic and Forecast Market Size by Country

7.2.6.1 US

7.2.6.2 Canada

7.2.6.3 Mexico

7.3. Eastern Europe Anal Cancer Market

7.3.1 Key Market Trends, Growth Factors and Opportunities

7.3.2 Top Key Companies

7.3.3 Historic and Forecasted Market Size by Segments

7.3.4 Historic and Forecasted Market Size by Type

7.3.4.1 Squamous Cell Carcinoma

7.3.4.2 Adenocarcinoma

7.3.4.3 Others

7.3.5 Historic and Forecasted Market Size by End User

7.3.5.1 Hospitals

7.3.5.2 Cancer Research Institutes

7.3.5.3 Specialty Clinics

7.3.5.4 Others

7.3.6 Historic and Forecast Market Size by Country

7.3.6.1 Russia

7.3.6.2 Bulgaria

7.3.6.3 The Czech Republic

7.3.6.4 Hungary

7.3.6.5 Poland

7.3.6.6 Romania

7.3.6.7 Rest of Eastern Europe

7.4. Western Europe Anal Cancer Market

7.4.1 Key Market Trends, Growth Factors and Opportunities

7.4.2 Top Key Companies

7.4.3 Historic and Forecasted Market Size by Segments

7.4.4 Historic and Forecasted Market Size by Type

7.4.4.1 Squamous Cell Carcinoma

7.4.4.2 Adenocarcinoma

7.4.4.3 Others

7.4.5 Historic and Forecasted Market Size by End User

7.4.5.1 Hospitals

7.4.5.2 Cancer Research Institutes

7.4.5.3 Specialty Clinics

7.4.5.4 Others

7.4.6 Historic and Forecast Market Size by Country

7.4.6.1 Germany

7.4.6.2 UK

7.4.6.3 France

7.4.6.4 The Netherlands

7.4.6.5 Italy

7.4.6.6 Spain

7.4.6.7 Rest of Western Europe

7.5. Asia Pacific Anal Cancer Market

7.5.1 Key Market Trends, Growth Factors and Opportunities

7.5.2 Top Key Companies

7.5.3 Historic and Forecasted Market Size by Segments

7.5.4 Historic and Forecasted Market Size by Type

7.5.4.1 Squamous Cell Carcinoma

7.5.4.2 Adenocarcinoma

7.5.4.3 Others

7.5.5 Historic and Forecasted Market Size by End User

7.5.5.1 Hospitals

7.5.5.2 Cancer Research Institutes

7.5.5.3 Specialty Clinics

7.5.5.4 Others

7.5.6 Historic and Forecast Market Size by Country

7.5.6.1 China

7.5.6.2 India

7.5.6.3 Japan

7.5.6.4 South Korea

7.5.6.5 Malaysia

7.5.6.6 Thailand

7.5.6.7 Vietnam

7.5.6.8 The Philippines

7.5.6.9 Australia

7.5.6.10 New Zealand

7.5.6.11 Rest of APAC

7.6. Middle East & Africa Anal Cancer Market

7.6.1 Key Market Trends, Growth Factors and Opportunities

7.6.2 Top Key Companies

7.6.3 Historic and Forecasted Market Size by Segments

7.6.4 Historic and Forecasted Market Size by Type

7.6.4.1 Squamous Cell Carcinoma

7.6.4.2 Adenocarcinoma

7.6.4.3 Others

7.6.5 Historic and Forecasted Market Size by End User

7.6.5.1 Hospitals

7.6.5.2 Cancer Research Institutes

7.6.5.3 Specialty Clinics

7.6.5.4 Others

7.6.6 Historic and Forecast Market Size by Country

7.6.6.1 Turkiye

7.6.6.2 Bahrain

7.6.6.3 Kuwait

7.6.6.4 Saudi Arabia

7.6.6.5 Qatar

7.6.6.6 UAE

7.6.6.7 Israel

7.6.6.8 South Africa

7.7. South America Anal Cancer Market

7.7.1 Key Market Trends, Growth Factors and Opportunities

7.7.2 Top Key Companies

7.7.3 Historic and Forecasted Market Size by Segments

7.7.4 Historic and Forecasted Market Size by Type

7.7.4.1 Squamous Cell Carcinoma

7.7.4.2 Adenocarcinoma

7.7.4.3 Others

7.7.5 Historic and Forecasted Market Size by End User

7.7.5.1 Hospitals

7.7.5.2 Cancer Research Institutes

7.7.5.3 Specialty Clinics

7.7.5.4 Others

7.7.6 Historic and Forecast Market Size by Country

7.7.6.1 Brazil

7.7.6.2 Argentina

7.7.6.3 Rest of SA

Chapter 8 Analyst Viewpoint and Conclusion

8.1 Recommendations and Concluding Analysis

8.2 Potential Market Strategies

Chapter 9 Research Methodology

9.1 Research Process

9.2 Primary Research

9.3 Secondary Research

|

Anal Cancer Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 638.11 Million |

|

Forecast Period 2025-35 CAGR: |

4.86% |

Market Size in 2035: |

USD 978.10 Million |

|

Segments Covered: |

By Type |

|

|

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||