Key Market Highlights

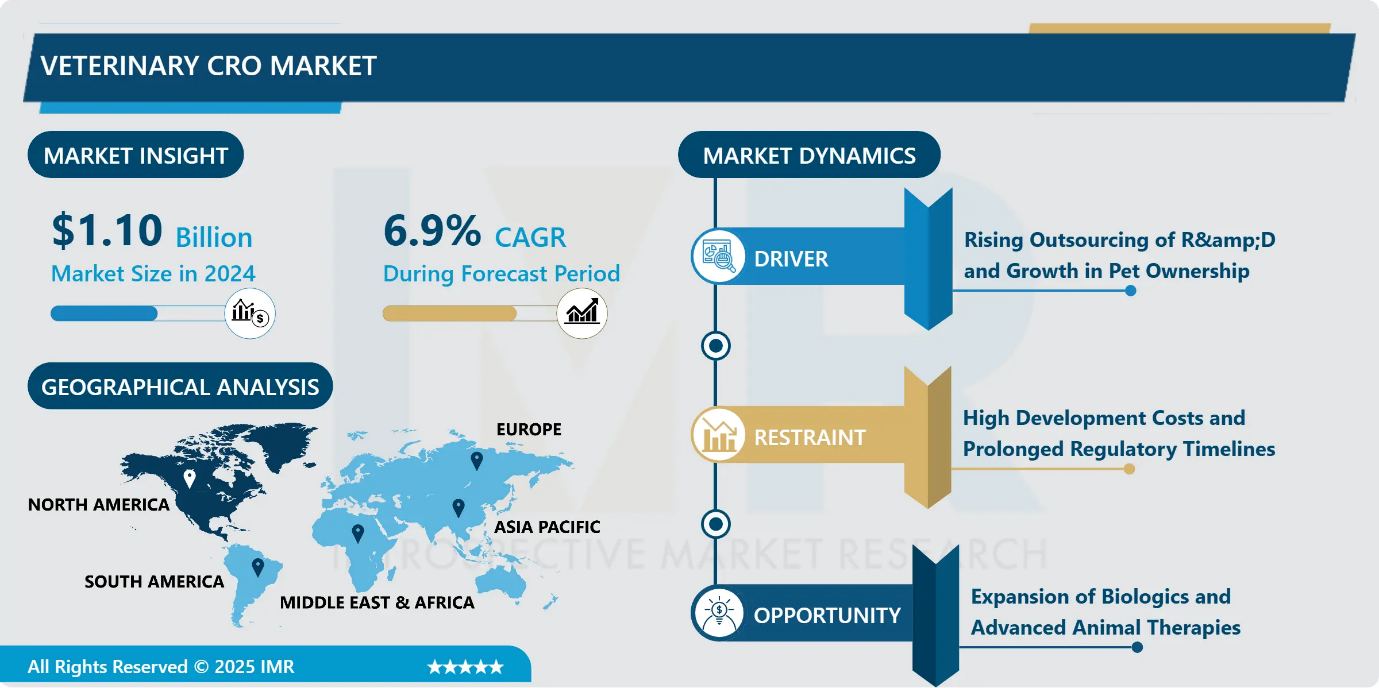

Veterinary CRO Market Size Was Valued at USD 1.10 Billion in 2024, and is Projected to Reach USD 2.29 Billion by 2035, Growing at a CAGR of 6.9% from 2025-2035.

- Market Size in 2024: USD 1.10 Billion

- Projected Market Size by 2035: USD 2.29 Billion

- CAGR (2025–2035): 6.9%

- Leading Market in 2024: North America

- Fastest-Growing Market: Asia-Pacific

- By Formulation Type: The Liquid segment is anticipated to lead the market by accounting for 27.2% of the market share throughout the forecast period.

- By End User: The Pharmaceutical and Biotechnology Companies segment is expected to capture 26.65% of the market share, thereby maintaining its dominance over the forecast period.

- By Region: North America region is projected to hold 32.9% of the market share during the forecast period.

- Active Players: Argenta (New Zealand), Aurigon Life Science (India), Avacta Animal Health (United Kingdom), Biovet (India), Charles River Laboratories (United States), Dopharma (Netherlands), and Other Active Players.

Veterinary CRO Market Synopsis:

The Veterinary CRO and CDMO Market represents a specialized outsourcing ecosystem that supports the research, development, regulatory approval, and manufacturing of animal health products. It includes contract research organizations providing preclinical studies, clinical trials, safety and efficacy testing, and regulatory consulting, alongside contract development and manufacturing organizations offering formulation development, scale-up, GMP manufacturing, and packaging services. The market is driven by rising R&D costs, growing expenditure on companion and livestock health, and increasingly stringent regulatory requirements. Sponsors are outsourcing to accelerate timelines, manage multi-country compliance, and access specialized capabilities such as vaccine challenge studies and pathogen handling. Rapid outsourcing adoption, digital trial tools, and innovation in biologics and gene-based therapies continue to expand market demand globally.

Veterinary CRO Market Dynamics and Trend Analysis:

Veterinary CRO Market Growth Driver - Rising Outsourcing of R&D and Growth in Pet Ownership

- The veterinary CRO and CDMO market is strongly driven by the increasing outsourcing of research, development, and manufacturing activities by animal health companies. Outsourcing allows sponsors to reduce capital expenditure, access specialized technical expertise, and navigate complex regulatory requirements more efficiently, thereby accelerating time to market.

- At the same time, rising global pet ownership is significantly boosting demand for advanced veterinary therapies and preventive care. As pet owners increasingly prioritize animal health and wellness, the need for innovative pharmaceuticals, biologics, and diagnostics continues to grow. This dual trend reinforces reliance on specialized CRO and CDMO partners to support scalable, cost-effective, and compliant veterinary product development.

Veterinary CRO Market Limiting Factor - High Development Costs and Prolonged Regulatory Timelines

- The veterinary CRO market faces a significant restraint due to escalating development costs and extended approval timelines for advanced animal health products, particularly biologics. Developing novel veterinary therapies requires substantial capital investment and long development cycles, driven by complex study designs, multi-site field trials, and stringent regulatory requirements. Livestock and companion-animal studies often involve high operational expenses, while extended post-approval monitoring further increases lifecycle costs. These financial and time-intensive processes limit participation by smaller innovators and concentrate project activity among well-funded sponsors. As a result, high entry barriers and prolonged timelines can slow innovation rates and constrain the overall expansion of the veterinary CRO market.

Veterinary CRO Market Expansion Opportunity - Expansion of Biologics and Advanced Animal Therapies

- The increasing development of biologics and advanced therapies in animal health presents a significant opportunity for the veterinary CRO and CDMO market. These next-generation treatments, including monoclonal antibodies, recombinant vaccines, and gene-based therapies, offer targeted and durable solutions for complex and chronic animal diseases. As the limitations of traditional small-molecule drugs become more apparent, animal health companies are increasingly relying on specialized outsourcing partners with expertise in biologics development, scale-up, and GMP manufacturing. Veterinary CROs and CDMOs play a critical role in supporting regulatory compliance, technical complexity, and innovation, creating sustained demand and long-term growth potential across companion and livestock animal segments.

Veterinary CRO Market Challenge and Risk - Limited Availability of Specialized Animal Research Infrastructure

- The veterinary CRO market faces a key challenge due to the limited availability of specialized research infrastructure required for complex animal studies. Advanced facilities capable of conducting large-animal trials under high biosafety and GLP-compliant conditions are scarce, particularly in emerging regions. This shortage often forces sponsors to relocate animals or studies across borders, increasing project timelines and operational costs.

- In addition, the high capital investment needed to establish pathogen-free herds and maintain specialized facilities discourages new infrastructure development. Limited access to advanced imaging and oncology equipment at veterinary institutions further restricts study capacity, constraining regional growth and slowing the expansion of outsourced veterinary research services.

Veterinary CRO Market Trend - Growing Emphasis on Animal Welfare and Ethical Research Practices

- The veterinary CRO market is increasingly shaped by a strong focus on animal welfare and ethical research standards. Evolving societal expectations and stricter regulatory oversight are encouraging the adoption of humane study designs, refined protocols, and ethical endpoints that minimize animal distress.

- Veterinary CROs are integrating alternative models, improved care practices, and responsible testing methodologies to align with these values. This trend is influencing study planning, execution, and client selection, as sponsors increasingly prefer partners that demonstrate ethical responsibility. CROs that prioritize animal welfare not only ensure regulatory compliance but also strengthen credibility, attract value-driven clients, and position themselves competitively in a more ethically conscious animal health research environment.

Veterinary CRO Market Segment Analysis:

Veterinary CRO Market is segmented based on into Service Type, Animal Type, Indication, Product Type, Formulation Type, End User, and Region

By Formulation Type, Liquid formulations segment is expected to dominate the market with around 27.2% share during the forecast period.

- Liquid formulations dominate the veterinary CRO market due to their ease of administration, precise dose adjustment, and broad applicability across companion and livestock animals. They are especially preferred for pets that resist solid dosage forms, improving treatment compliance and clinical outcomes. Liquid formats also simplify formulation development and stability testing, making them cost-effective for sponsors. Injectable formulations, while currently a smaller segment, are emerging rapidly driven by the growing use of biologics and the need for fast-acting therapies that bypass gastrointestinal absorption. Advances in injection technologies and rising infectious disease prevalence further support this trend. Despite injectables’ growth, liquid formulations remain dominant because of their versatility, patient compliance, and widespread clinical acceptance.

By End User, Pharmaceutical and biotechnology companies is expected to dominate with close to 26.65% market share during the forecast period.

- Pharmaceutical and biotechnology companies continued to dominate the veterinary CRO market in 2024, accounting for approximately 26.65% of total contract value. Their leadership is driven by strong financial capacity, consistent R&D pipelines, and the need to outsource complex development, regulatory, and manufacturing activities. However, academic and public research institutions are emerging as a fast-growing segment, supported by expanding One Health funding initiatives.

- These institutes are transitioning from exploratory research to conducting pivotal studies under recognized quality systems such as ISO 9001. Despite this rapid growth, industry sponsors remain dominant due to their scale, long-term outsourcing strategies, and higher volume of late-stage and commercial development projects.

Veterinary CRO Market Regional Insights:

North America region is estimated to lead the market with around 32.9% share during the forecast period.

- North America accounted for approximately 32.9% of market revenue in 2024, maintaining its dominant position due to its robust animal healthcare ecosystem. The region benefits from a dense network of GLP-certified facilities, high pet ownership levels, and strong demand for premium veterinary therapies. Favorable regulatory mechanisms, including the conditional-approval pathway offered by the U.S. Food and Drug Administration, encourage early-stage development and outsourcing.

- The presence of leading pharmaceutical and biotechnology companies, coupled with substantial R&D investments and advanced technological adoption, further strengthens market leadership. Although growth rates are moderating, entrenched infrastructure, regulatory clarity, and high spending on animal health ensure North America remains the largest and most influential regional market.

Veterinary CRO Market Active Players:

- Argenta (New Zealand)

- Aurigon Life Science (India)

- Avacta Animal Health (United Kingdom)

- Biovet (India)

- Charles River Laboratories (United States)

- Dopharma (Netherlands)

- Elanco Contract Manufacturing (United States)

- Evonik (Germany)

- Huvepharma (Bulgaria)

- LGC Group (United Kingdom)

- Lonza (Switzerland)

- MBV VET Research (Spain)

- Norbrook Laboratories (United Kingdom)

- Pharmgate (United States)

- Phibro Animal Health (United States)

- Other Active Players

Key Industry Developments in the Veterinary CRO Market:

- In January 2025, Argenta Limited announced a strategic realignment of its animal health CRO platform. The initiative is designed to strengthen end-to-end R&D and product development capabilities. It also aims to improve service integration and enhance value delivery for animal health clients.

- In April 2025, GemPharmatech expanded its U.S. footprint with the launch of a new facility in San Diego. This expansion reinforces the company’s commitment to the U.S. market. The move enhances regional preclinical research capacity and client support.

Veterinary CRO Market Technology Landscape: Preclinical, Clinical, and Regulatory Service Capabilities

- The veterinary CRO market is defined by a broad range of specialized technical capabilities supporting animal health research, development, and regulatory approval. Core services include preclinical pharmacology, toxicology, safety and efficacy studies, and clinical trials conducted across companion animals and livestock species. These studies are executed under stringent quality frameworks such as Good Laboratory Practice (GLP), Good Clinical Practice (GCP), and ISO-certified systems to meet regional and global regulatory requirements.

- Advanced study designs increasingly incorporate biomarker analysis, bioanalytical testing, digital data capture, and remote monitoring tools to improve data integrity and trial efficiency. Veterinary CROs also deploy specialized infrastructure for large-animal studies, biosafety containment, and vaccine challenge models. On the CDMO side, technical competencies extend to formulation development, process optimization, scale-up, aseptic manufacturing, and quality control testing. Ongoing adoption of biologics, gene-based therapies, and complex vaccines is further increasing technical sophistication and demand for specialized expertise across the veterinary CRO ecosystem.

|

Veterinary CRO Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2024 |

Market Size in 2024: |

USD 1.10 Bn. |

|

Forecast Period 2025-32 CAGR: |

6.9 % |

Market Size in 2035: |

USD 2.29 Bn. |

|

Segments Covered: |

By Service Type |

|

|

|

By Animal Type

|

|

||

|

By Indication |

|

||

|

By Product Type |

|

||

|

By Formulation Type |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Veterinary CRO Market by Service Type (2018-2035)

4.1 Veterinary CRO Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Clinical Trials and Others

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

Chapter 5: Veterinary CRO Market by Animal Type (2018-2035)

5.1 Veterinary CRO Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Companion Animals including Dogs

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Cats

5.5 and Other Companion Species

5.6 and Livestock including Cattle

5.7 Swine

5.8 Poultry

5.9 and Other Livestock

Chapter 6: Veterinary CRO Market by Indication (2018-2035)

6.1 Veterinary CRO Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Oncology and Others

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

Chapter 7: Veterinary CRO Market by Product Type (2018-2035)

7.1 Veterinary CRO Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Antimicrobials

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Anti-inflammatories

7.5 Vaccines

7.6 Parasite Control Products

7.7 and Nutritional Supplements

Chapter 8: Veterinary CRO Market by Formulation Type (2018-2035)

8.1 Veterinary CRO Market Snapshot and Growth Engine

8.2 Market Overview

8.3 Liquid

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

8.3.3 Key Market Trends, Growth Factors, and Opportunities

8.3.4 Geographic Segmentation Analysis

8.4 Powder

8.5 Tablet

8.6 Injectable

8.7 and Topical

Chapter 9: Veterinary CRO Market by End User (2018-2035)

9.1 Veterinary CRO Market Snapshot and Growth Engine

9.2 Market Overview

9.3 Pharmaceutical and Biotechnology Companies

9.3.1 Introduction and Market Overview

9.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

9.3.3 Key Market Trends, Growth Factors, and Opportunities

9.3.4 Geographic Segmentation Analysis

9.4 Veterinarians

9.5 Pet Owners

9.6 Farmers

9.7 Animal Hospitals

9.8 Research Institutions

9.9 and Others

Chapter 10: Company Profiles and Competitive Analysis

10.1 Competitive Landscape

10.1.1 Competitive Benchmarking

10.1.2 Veterinary CRO Market Share by Manufacturer/Service Provider(2024)

10.1.3 Industry BCG Matrix

10.1.4 PArtnerships, Mergers & Acquisitions

10.2 ARGENTA (NEW ZEALAND)

10.2.1 Company Overview

10.2.2 Key Executives

10.2.3 Company Snapshot

10.2.4 Role of the Company in the Market

10.2.5 Sustainability and Social Responsibility

10.2.6 Operating Business Segments

10.2.7 Product Portfolio

10.2.8 Business Performance

10.2.9 Recent News & Developments

10.2.10 SWOT Analysis

10.3 AURIGON LIFE SCIENCE (INDIA)

10.4 AVACTA ANIMAL HEALTH (UNITED KINGDOM)

10.5 BIOVET (INDIA)

10.6 CHARLES RIVER LABORATORIES (UNITED STATES)

10.7 DOPHARMA (NETHERLANDS)

10.8 ELANCO CONTRACT MANUFACTURING (UNITED STATES)

10.9 EVONIK (GERMANY)

10.10 HUVEPHARMA (BULGARIA)

10.11 LGC GROUP (UNITED KINGDOM)

10.12 LONZA (SWITZERLAND)

10.13 MBV VET RESEARCH (SPAIN)

10.14 NORBROOK LABORATORIES (UNITED KINGDOM)

10.15 PHARMGATE (UNITED STATES)

10.16 PHIBRO ANIMAL HEALTH (UNITED STATES)

10.17 AND OTHER ACTIVE PLAYERS.

Chapter 11: Global Veterinary CRO Market By Region

11.1 Overview

11.2. North America Veterinary CRO Market

11.2.1 Key Market Trends, Growth Factors and Opportunities

11.2.2 Top Key Companies

11.2.3 Historic and Forecasted Market Size by Segments

11.2.4 Historic and Forecast Market Size by Country

11.2.4.1 US

11.2.4.2 Canada

11.2.4.3 Mexico

11.3. Eastern Europe Veterinary CRO Market

11.3.1 Key Market Trends, Growth Factors and Opportunities

11.3.2 Top Key Companies

11.3.3 Historic and Forecasted Market Size by Segments

11.3.4 Historic and Forecast Market Size by Country

11.3.4.1 Russia

11.3.4.2 Bulgaria

11.3.4.3 The Czech Republic

11.3.4.4 Hungary

11.3.4.5 Poland

11.3.4.6 Romania

11.3.4.7 Rest of Eastern Europe

11.4. Western Europe Veterinary CRO Market

11.4.1 Key Market Trends, Growth Factors and Opportunities

11.4.2 Top Key Companies

11.4.3 Historic and Forecasted Market Size by Segments

11.4.4 Historic and Forecast Market Size by Country

11.4.4.1 Germany

11.4.4.2 UK

11.4.4.3 France

11.4.4.4 The Netherlands

11.4.4.5 Italy

11.4.4.6 Spain

11.4.4.7 Rest of Western Europe

11.5. Asia Pacific Veterinary CRO Market

11.5.1 Key Market Trends, Growth Factors and Opportunities

11.5.2 Top Key Companies

11.5.3 Historic and Forecasted Market Size by Segments

11.5.4 Historic and Forecast Market Size by Country

11.5.4.1 China

11.5.4.2 India

11.5.4.3 Japan

11.5.4.4 South Korea

11.5.4.5 Malaysia

11.5.4.6 Thailand

11.5.4.7 Vietnam

11.5.4.8 The Philippines

11.5.4.9 Australia

11.5.4.10 New Zealand

11.5.4.11 Rest of APAC

11.6. Middle East & Africa Veterinary CRO Market

11.6.1 Key Market Trends, Growth Factors and Opportunities

11.6.2 Top Key Companies

11.6.3 Historic and Forecasted Market Size by Segments

11.6.4 Historic and Forecast Market Size by Country

11.6.4.1 Turkiye

11.6.4.2 Bahrain

11.6.4.3 Kuwait

11.6.4.4 Saudi Arabia

11.6.4.5 Qatar

11.6.4.6 UAE

11.6.4.7 Israel

11.6.4.8 South Africa

11.7. South America Veterinary CRO Market

11.7.1 Key Market Trends, Growth Factors and Opportunities

11.7.2 Top Key Companies

11.7.3 Historic and Forecasted Market Size by Segments

11.7.4 Historic and Forecast Market Size by Country

11.7.4.1 Brazil

11.7.4.2 Argentina

11.7.4.3 Rest of SA

Chapter 12 Analyst Viewpoint and Conclusion

Chapter 13 Our Thematic Research Methodology

12.1 Research Process

12.2 Primary Research

12.3 Secondary Research

Chapter 14 Case Study

Chapter 15 Appendix

13.1 Sources

13.2 List of Tables and figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Veterinary CRO Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2024 |

Market Size in 2024: |

USD 1.10 Bn. |

|

Forecast Period 2025-32 CAGR: |

6.9 % |

Market Size in 2035: |

USD 2.29 Bn. |

|

Segments Covered: |

By Service Type |

|

|

|

By Animal Type

|

|

||

|

By Indication |

|

||

|

By Product Type |

|

||

|

By Formulation Type |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||