Value-Based Healthcare Market Synopsis:

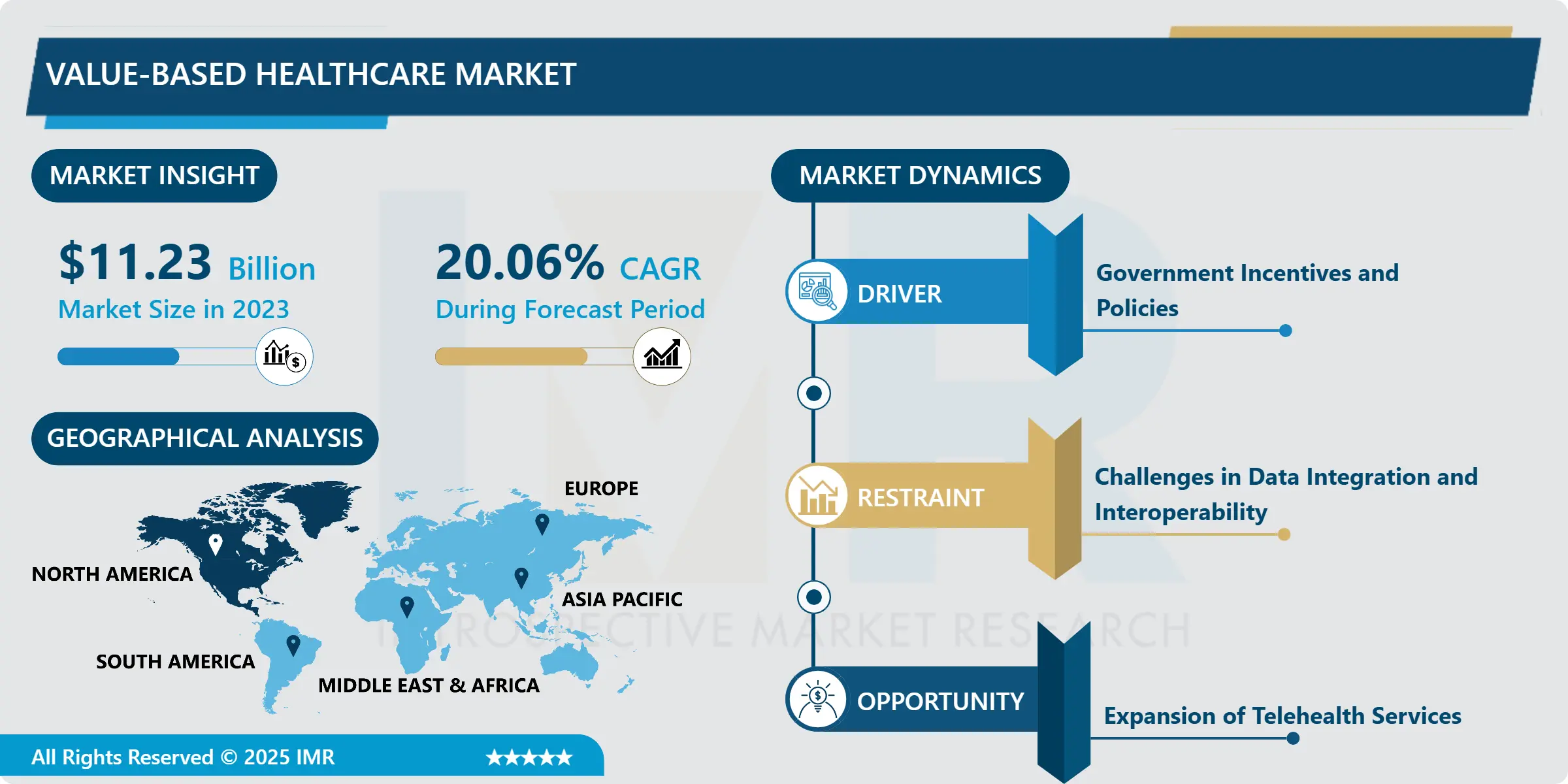

Value-Based Healthcare Market Size Was Valued at USD 11.23 Billion in 2023, and is Projected to Reach USD 58.21 Billion by 2032, Growing at a CAGR of 20.06% From 2024-2032.

Value-Based Healthcare (VBHC) is one of the models of providing medical care that involves payment for the delivered medical services depending on patients’ health improvement rather than service delivery. This approach was intended to increase the quality of care, increase patient satisfaction and reduce healthcare costs by ensuring that providers provide better health outcomes for their patients.

The Value-Based Healthcare Market means challenging concepts in the context of providing and paying for health care. The fee for-service reimbursement schemes are productivity based and hence promote over-use of services by providers due to financial incentives. On the other hand, VBHC concentrates on the efficiency and quality of the outcomes which the patient gets, the providers therefore are motivated to provide the best of the services. This model is consistent with patient-centered care and is consistent with ongoing changes in data acquisition and health IT that allow practitioners to track and enhance the effectiveness of patient care in ways previously impossible.

In this growing healthcare system field, different stakeholders adopt VBHC. Hospitals, clinics, insurance companies and government are gradually adopting value-based ordering systems as a way of enhancing the co-ordination of the health system and enhancing the engagement of patient. An increasing number of patients suffering from chronic diseases and, equally importantly, an aging population, which is the concrete reality, demand a more coordinated style of healthcare. This leads to effective implementation of value-based health care as a means of managing cost and increasing the quality of delivery. This particular market is predicted to grow in the future due to a growing demand for effective health care services and the shift towards different reimbursement models.

Value-Based Healthcare Market Trend Analysis:

Shift Towards Digital Health Solutions

- Digital health solution is one of the major trends identified in the Value-Based Healthcare Market. Tele-health care methods such as tele-medicine, smart phone health applications and remote tracking technologies are revolutionizing the way care is being delivered and how providers interact with consumers. It allows providers to track patients’ ordinary health status and to intercede at an early stage in the event of a problem. This change towards digital health is not just beneficial to the patient but also to the provider as patients’ health status increases, and care delivery becomes more effective as time and repetition of hospital visits become minimized.

- Also, the use of artificial intelligence (AI) and big data in integrated digital health solutions is empowering customers to enhance knowledge of patient actions and the effectiveness of interventions. The use of these technologies by the providers makes it possible to detect patients with risky factors and adapt patient’s plan and resource use appropriately. Consequently, technology-enabled solutions are emerging as critical ingredients of the value-based models by shifting the health-care delivery business from reactive treatments to proactive prevention.

Expansion of Telehealth Services

- A market gap in the Value-Based Healthcare Market is the further development of telehealth services. In this paper, this means that due to the COVID-19 pandemic, many patients and practitioners began using telehealth more actively to replace face-to-face consultations. This trend will further persist and offers a strong future opportunity to the healthcare organizations to upgrade their service line. Incorporating telehealth in value based care, providers can enhance the patient centred care, the waiting time to get an appointment can be minimized and timely intervention can be made.

- Furthermore, iPhone services are useful for making appropriate care coordination as patients with certain chronic diseases would need constant monitoring. This happens because through tele health the patients are capacitated to take an active role in consulting the doctors and in monitoring their health conditions. Given the continuous appreciation of healthcare organizations with telehealth services in improving patinet experience and relevant outcomes, there is an entice for providers to incorporate and grow such services in their VBC models.

Value-Based Healthcare Market Segment Analysis:

Value-Based Healthcare Market Segmented on the basis of Type, Application, End User, and Region.

By Model, Patient-Centered Medical Home (PCMH) segment is expected to dominate the market during the forecast period

- It is worth noting that all the models within the Value-Based Healthcare framework are available to meet various healthcare implementation and operational needs. For example, ACOs stress the integration of care across a group of organizations, which would also share the responsibility for a patient. Using a more team-oriented approach can help to diminish wasting resources and to get a more exhaustive picture of the needs of patients and, accordingly, to work on increasing the outcomes of patient treatment. On the other hand, PCMH model highly values primary care and gives priority to the patient-physician, patient care team interaction. Increased patient satisfaction emanates from the provision of individualised care since treatment plans address the patient’s requirement.

- Likewise, the P4P and bundled payment models can be tied to financial treatment that focuses on the results offered to patients. Because the payment is tied to specific healthcare outcomes, these models enhance efficiency of care delivery and advance an emphasis on disease prevention and control of chronic illnesses. As the notion of the healthcare system continues to grow, the implementation of these models will be important as the drive from volume to value gains momentum.

By Application, Hospitals segment expected to held the largest share

- The models in the Value-Based Healthcare framework are as follows and they address various aspects of the system. For example, ACOs focus on collaboration between treatment delivery by several providers and implying equal responsibility among them for the patient’s condition. Coordinated care not only makes better use of available resources but also provides a more congenial idea about the essential requirements of the patient to enhance the standards of his or her health. On the other hand, the PCMH model greatly focuses on primary care and the patient as well as his or her healthcare team. This consideration of patient engagement ensures that the treatment offered is meets individual patient needs hence improving the patient satisfaction.

- Likewise, the P4P and the bundled payment model intervene and re-link the payment system with quality of care offers. As such, these models increase efficiencies in delivery and the use of both prevention and chronic disease management. In future, there could be a fine blend of these models to address the healthcare issues towards more of value-added organisation rather than bulky volume oriented healthcare delivery systems.

Value-Based Healthcare Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

- North America, especially the United States, takes up the largest market share in the global value-based healthcare market presently. The U.S has been in the frontline in the adoption of value-based care on account of the enforcement of reforms like the Affordable care act and different Medicare initiatives. These initiatives have led to promulgation of new care models of care delivery such as ACOs and bundled payment systems with the vision of improving patient care results and cost.

- Also, the North American region is leading in this market due to higher accessibility of advanced healthcare facilities, focuses more on technology implementation, and a higher investment in healthcare technology. With more healthcare providers taking up the cause of delivering more value-based and satisfying healthcare solutions it stands to reason that this region shall continue to play a defining role in determining the future of the healthcare system.

Active Key Players in the Value-Based Healthcare Market:

- Aetna Inc. (USA)

- Anthem, Inc. (USA)

- Blue Cross Blue Shield Association (USA)

- Centene Corporation (USA)

- Cigna (USA)

- Cleveland Clinic (USA)

- Humana Inc. (USA)

- Kaiser Permanente (USA)

- Mayo Clinic (USA)

- McKesson Corporation (USA)

- Providence Health & Services (USA)

- UnitedHealth Group (USA)

- Other Ative Players

Key Industry Developments in the Value-Based Healthcare Market:

- In April 2023, Kaiser Foundation Hospitals and Geisinger Health announced the launch of Risant Health, a non-profit organization aimed at advancing value-based care in varied community-based health systems that encompass multiple payers and providers. This initiative is designed to enhance healthcare delivery by fostering collaboration among various stakeholders and improving patient outcomes.

- In February 2023, Blue Cross and Blue Shield of Minnesota partnered with Homeward to establish a full-risk value-based care arrangement, specifically targeting the improvement of access to healthcare services in rural Minnesota, thereby addressing healthcare disparities in underserved areas.

|

Value-Based Healthcare Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 11.23 Billion |

|

Forecast Period 2024-32 CAGR: |

20.06% |

Market Size in 2032: |

USD 58.21 Billion |

|

Segments Covered: |

By Model |

|

|

|

By Deployment |

|

||

|

By Platform |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Industry Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Strategic Pestle Overview

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Mapping

3.6 Regulatory Framework

3.7 Princing Trend Analysis

3.8 Patent Analysis

3.9 Technology Evolution

3.10 Investment Pockets

3.11 Import-Export Analysis

Chapter 4: Value-Based Healthcare Market by Model

4.1 Value-Based Healthcare Market Snapshot and Growth Engine

4.2 Value-Based Healthcare Market Overview

4.3 Accountable Care Organization (ACO)

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.3.3 Accountable Care Organization (ACO): Geographic Segmentation Analysis

4.4 Patient-centred Medical Home (PCMH)

4.4.1 Introduction and Market Overview

4.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.4.3 Patient-centred Medical Home (PCMH): Geographic Segmentation Analysis

4.5 Pay for Performance (P4P)

4.5.1 Introduction and Market Overview

4.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.5.3 Pay for Performance (P4P): Geographic Segmentation Analysis

4.6 Bundled Payments

4.6.1 Introduction and Market Overview

4.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.6.3 Bundled Payments: Geographic Segmentation Analysis

4.7

4.7.1 Introduction and Market Overview

4.7.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.7.3 : Geographic Segmentation Analysis

Chapter 5: Value-Based Healthcare Market by Deployment

5.1 Value-Based Healthcare Market Snapshot and Growth Engine

5.2 Value-Based Healthcare Market Overview

5.3 Cloud-Based

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.3.3 Cloud-Based: Geographic Segmentation Analysis

5.4 On-Premise

5.4.1 Introduction and Market Overview

5.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.4.3 On-Premise: Geographic Segmentation Analysis

5.5 Platform

5.5.1 Introduction and Market Overview

5.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.5.3 Platform: Geographic Segmentation Analysis

5.6 Standalone

5.6.1 Introduction and Market Overview

5.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.6.3 Standalone: Geographic Segmentation Analysis

5.7 Integrated

5.7.1 Introduction and Market Overview

5.7.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.7.3 Integrated: Geographic Segmentation Analysis

Chapter 6: Value-Based Healthcare Market by Application

6.1 Value-Based Healthcare Market Snapshot and Growth Engine

6.2 Value-Based Healthcare Market Overview

6.3 Hospitals

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.3.3 Hospitals : Geographic Segmentation Analysis

6.4 Clinics

6.4.1 Introduction and Market Overview

6.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.4.3 Clinics: Geographic Segmentation Analysis

6.5 Insurance Companies

6.5.1 Introduction and Market Overview

6.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.5.3 Insurance Companies: Geographic Segmentation Analysis

6.6 Government)

6.6.1 Introduction and Market Overview

6.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.6.3 Government): Geographic Segmentation Analysis

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Value-Based Healthcare Market Share by Manufacturer (2023)

7.1.3 Concentration Ratio(CR5)

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 UNITEDHEALTH GROUP (USA)

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Operating Business Segments

7.2.5 Product Portfolio

7.2.6 Business Performance

7.2.7 Key Strategic Moves and Recent Developments

7.3 ANTHEM INC. (USA)

7.4 CIGNA (USA)

7.5 AETNA INC. (USA)

7.6 HUMANA INC. (USA)

7.7 BLUE CROSS BLUE SHIELD ASSOCIATION (USA)

7.8 CENTENE CORPORATION (USA)

7.9 MAYO CLINIC (USA)

7.10 CLEVELAND CLINIC (USA)

7.11 OTHER ACTIVE PLAYERS

Chapter 8: Global Value-Based Healthcare Market By Region

8.1 Overview

8.2. North America Value-Based Healthcare Market

8.2.1 Historic and Forecasted Market Size by Segments

8.2.2 Historic and Forecasted Market Size By Model

8.2.2.1 Accountable Care Organization (ACO)

8.2.2.2 Patient-centred Medical Home (PCMH)

8.2.2.3 Pay for Performance (P4P)

8.2.2.4 Bundled Payments

8.2.2.5

8.2.3 Historic and Forecasted Market Size By Deployment

8.2.3.1 Cloud-Based

8.2.3.2 On-Premise

8.2.3.3 Platform

8.2.3.4 Standalone

8.2.3.5 Integrated

8.2.4 Historic and Forecasted Market Size By Application

8.2.4.1 Hospitals

8.2.4.2 Clinics

8.2.4.3 Insurance Companies

8.2.4.4 Government)

8.2.5 Historic and Forecast Market Size by Country

8.2.5.1 US

8.2.5.2 Canada

8.2.5.3 Mexico

8.3. Eastern Europe Value-Based Healthcare Market

8.3.1 Historic and Forecasted Market Size by Segments

8.3.2 Historic and Forecasted Market Size By Model

8.3.2.1 Accountable Care Organization (ACO)

8.3.2.2 Patient-centred Medical Home (PCMH)

8.3.2.3 Pay for Performance (P4P)

8.3.2.4 Bundled Payments

8.3.2.5

8.3.3 Historic and Forecasted Market Size By Deployment

8.3.3.1 Cloud-Based

8.3.3.2 On-Premise

8.3.3.3 Platform

8.3.3.4 Standalone

8.3.3.5 Integrated

8.3.4 Historic and Forecasted Market Size By Application

8.3.4.1 Hospitals

8.3.4.2 Clinics

8.3.4.3 Insurance Companies

8.3.4.4 Government)

8.3.5 Historic and Forecast Market Size by Country

8.3.5.1 Bulgaria

8.3.5.2 The Czech Republic

8.3.5.3 Hungary

8.3.5.4 Poland

8.3.5.5 Romania

8.3.5.6 Rest of Eastern Europe

8.4. Western Europe Value-Based Healthcare Market

8.4.1 Historic and Forecasted Market Size by Segments

8.4.2 Historic and Forecasted Market Size By Model

8.4.2.1 Accountable Care Organization (ACO)

8.4.2.2 Patient-centred Medical Home (PCMH)

8.4.2.3 Pay for Performance (P4P)

8.4.2.4 Bundled Payments

8.4.2.5

8.4.3 Historic and Forecasted Market Size By Deployment

8.4.3.1 Cloud-Based

8.4.3.2 On-Premise

8.4.3.3 Platform

8.4.3.4 Standalone

8.4.3.5 Integrated

8.4.4 Historic and Forecasted Market Size By Application

8.4.4.1 Hospitals

8.4.4.2 Clinics

8.4.4.3 Insurance Companies

8.4.4.4 Government)

8.4.5 Historic and Forecast Market Size by Country

8.4.5.1 Germany

8.4.5.2 UK

8.4.5.3 France

8.4.5.4 Netherlands

8.4.5.5 Italy

8.4.5.6 Russia

8.4.5.7 Spain

8.4.5.8 Rest of Western Europe

8.5. Asia Pacific Value-Based Healthcare Market

8.5.1 Historic and Forecasted Market Size by Segments

8.5.2 Historic and Forecasted Market Size By Model

8.5.2.1 Accountable Care Organization (ACO)

8.5.2.2 Patient-centred Medical Home (PCMH)

8.5.2.3 Pay for Performance (P4P)

8.5.2.4 Bundled Payments

8.5.2.5

8.5.3 Historic and Forecasted Market Size By Deployment

8.5.3.1 Cloud-Based

8.5.3.2 On-Premise

8.5.3.3 Platform

8.5.3.4 Standalone

8.5.3.5 Integrated

8.5.4 Historic and Forecasted Market Size By Application

8.5.4.1 Hospitals

8.5.4.2 Clinics

8.5.4.3 Insurance Companies

8.5.4.4 Government)

8.5.5 Historic and Forecast Market Size by Country

8.5.5.1 China

8.5.5.2 India

8.5.5.3 Japan

8.5.5.4 South Korea

8.5.5.5 Malaysia

8.5.5.6 Thailand

8.5.5.7 Vietnam

8.5.5.8 The Philippines

8.5.5.9 Australia

8.5.5.10 New Zealand

8.5.5.11 Rest of APAC

8.6. Middle East & Africa Value-Based Healthcare Market

8.6.1 Historic and Forecasted Market Size by Segments

8.6.2 Historic and Forecasted Market Size By Model

8.6.2.1 Accountable Care Organization (ACO)

8.6.2.2 Patient-centred Medical Home (PCMH)

8.6.2.3 Pay for Performance (P4P)

8.6.2.4 Bundled Payments

8.6.2.5

8.6.3 Historic and Forecasted Market Size By Deployment

8.6.3.1 Cloud-Based

8.6.3.2 On-Premise

8.6.3.3 Platform

8.6.3.4 Standalone

8.6.3.5 Integrated

8.6.4 Historic and Forecasted Market Size By Application

8.6.4.1 Hospitals

8.6.4.2 Clinics

8.6.4.3 Insurance Companies

8.6.4.4 Government)

8.6.5 Historic and Forecast Market Size by Country

8.6.5.1 Turkey

8.6.5.2 Bahrain

8.6.5.3 Kuwait

8.6.5.4 Saudi Arabia

8.6.5.5 Qatar

8.6.5.6 UAE

8.6.5.7 Israel

8.6.5.8 South Africa

8.7. South America Value-Based Healthcare Market

8.7.1 Historic and Forecasted Market Size by Segments

8.7.2 Historic and Forecasted Market Size By Model

8.7.2.1 Accountable Care Organization (ACO)

8.7.2.2 Patient-centred Medical Home (PCMH)

8.7.2.3 Pay for Performance (P4P)

8.7.2.4 Bundled Payments

8.7.2.5

8.7.3 Historic and Forecasted Market Size By Deployment

8.7.3.1 Cloud-Based

8.7.3.2 On-Premise

8.7.3.3 Platform

8.7.3.4 Standalone

8.7.3.5 Integrated

8.7.4 Historic and Forecasted Market Size By Application

8.7.4.1 Hospitals

8.7.4.2 Clinics

8.7.4.3 Insurance Companies

8.7.4.4 Government)

8.7.5 Historic and Forecast Market Size by Country

8.7.5.1 Brazil

8.7.5.2 Argentina

8.7.5.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Value-Based Healthcare Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 11.23 Billion |

|

Forecast Period 2024-32 CAGR: |

20.06% |

Market Size in 2032: |

USD 58.21 Billion |

|

Segments Covered: |

By Model |

|

|

|

By Deployment |

|

||

|

By Platform |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||