Statin Market Synopsis

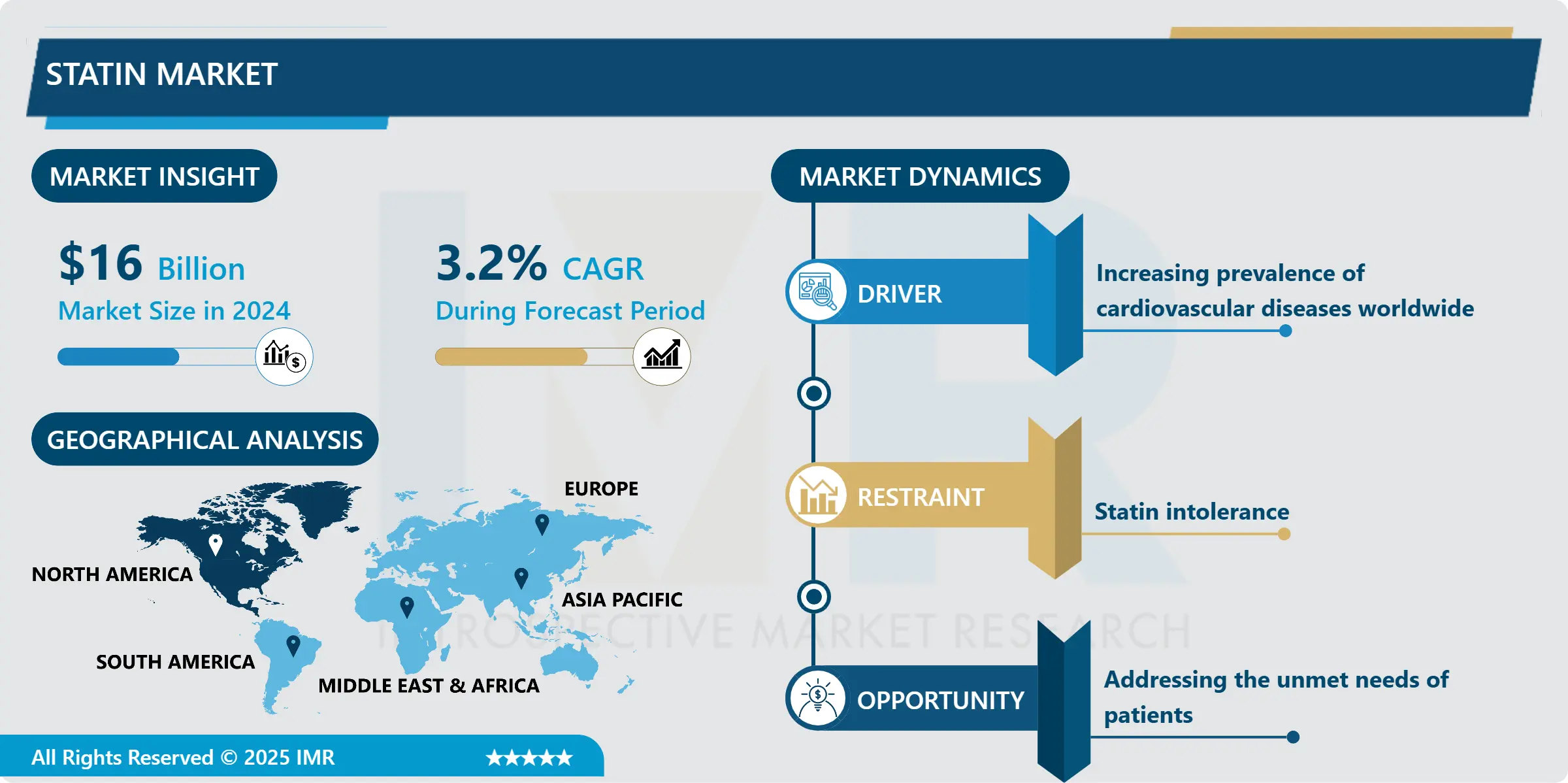

Statin Market Size Was Valued at USD 16 Billion in 2024, and is Projected to Reach USD 22.63 Billion by 2035, Growing at a CAGR of 3.2% From 2025-2035.

The statin market generates relationships to the pharmaceutical industry concerned to drug classes called statins, primarily used in the rationing of cholesterol. Statins are of the group HMG-CoA reductase inhibitors and work by inhibiting this enzyme in the liver because it triggers the manufacture of cholesterol. These drugs are usually prescribed to greatly reduce one’s risk to cardiovascular diseases such as heart attack as well as stroke most especially for patients with high cholesterol or with other cardiovascular risks. It would also be pertinent to note that statins are in constant demand, especially because of their ability to lower cholesterol levels, and as are now a part of many preventive health care programs. Some of Statin drugs include atorvastatin, simvastatin, rosuvastatin among others and is prescribed alongside diet and exercise to regulate amount of cholesterol.

Statin market can be considered one of the significant segments within the field of the pharmaceutical business that unites all the medications referred to as statins whose primary goal is to lower cholesterol level in blood. Their efficacy is not questionable in the degree to which they reduce the LDL cholesterol or the ‘bad’ cholesterol and a simultaneous rise in the HDL cholesterol or the ‘good’ cholesterol. They of these drugs suppress the cholesterolsterol synthesis in the liver by inhibiting the enzyme HMG CoA reductase. From the results of cholesterol level reduction, the statins reduce the instances of Cardiovascular ailments such as heart attacks and so forth; thus, statins are central to Cardiovascular care globally.

Market for statin is available statin drugs which have variation in its effectiveness and side effects that customers experience therefore the statin drugs can be grouped depending on the level of side effects it has. Currently, among them some are commonly used such as atorvastain like Lipitor, simvastatin like Zocor and rosuvastain like Crestor and others. This market is driven by such considerations as hypercholesterolemia and atherosclerosis are life-long diseases that call for lifetime treatments. However, it should be recalled that there are side effects of statin therapy which include myopathy; muscle pain and or weakness, liver enzyme elevation which always require periodic monitoring by the providers. Thus, based to the of the forecast on the continued use of statins due to global populations ageing and changes in lifestyle on preventive measures on morbidity and mortality of cardiovascular diseases.

Statin Market Trend Analysis

Increasing focus on personalized medicine and precision healthcare

- As for the strategic trends existing in the statin market, one can name the definite conclusion that the concept of the personalized approach and precision medicine will remain topical. Before, statin was only utilized according prognostic objectives by the management of cholesterol in certain ways. Statin side effects are big problem today, however new technologies concerning genetic test and biomarker analysis opens chance to formulate the opportunities of adverse effects and to bring statute dose to individual patient’s requirement. This style always considers factors such as heredities, cholesterol levels, and certain complications that may be attached to the providing of treatments.

- Furthermore, among patients there is a stabilization in utilizing statins both in combination with other preparations of the group, and with other preparations possessing impact on the pathogenetic mechanisms of atherosclerosis, as well as in terms of controlling the level of triglycerides and inflammation processes. These combinations are said to accommodate other aspects that are not well handled by statins in reducing cardiovascular risks. Research studies continue to carry forward new compounds with which to make statins so as to advance the stability and methods of delivery to enhance patients’ compliance and tolerance.

Addressing the unmet needs of patients

- In the market for statins there is a segment of the population that cannot tolerate statins or they have suboptimal response to available statin therapy. Statin intolerance which is evidenced by muscle pain or any other side effect makes the patient non-compliance or stop taking his treatment and the repercussions are very deadly to the cardiovascular system. As to this segment of patients, other formulations or new drugs which indeed have a definite cholesterol lowering effect and have fewer side effects than statins may be useful.

- Furthermore, the recent application of statins in a cholesterol management also throws open a possibility. From the data, what we have understood is that statins have other roles apart from having a hypolipidemic action such as anti-inflammatory action or having impact on other al chronic diseases. Pursuing these trails could reveal novel directions or leads regarding statins leading to both generating new categories of use and new types of indications for their usage.

Statin Market Segment Analysis:

Statin Market is Segmented on the basis of drug class and end-users.

By Drug Class, Astrovastatin segment is expected to dominate the market during the forecast period

- The atorvastatin segment has been identified as the key market driver in this market when considering the statin drug class in the subsequent years. Common types include atorvastatin, marketed under the name Lipitor it is used to lower cholesterol levels and reduce risk of cardiovascular diseases. And it is used for this purpose because a number of researches have clearly shown that it is more effective in reducing the levels of the LDL cholesterol and can be considered as safe overall. It means that atorvastatin has been present on the market since the primary years, and due to the large effectiveness confirmed by many trials and cheap generic products, many people can afford them. Moreover, new developments and improvements of better atorvastatin product forms and applications are most likely to solidify its reign on the statin market as the global population demand for effective CHD prevention escalates.

By End User, Hospitals segment expected to held the largest share

- Recommendations from the doctors and entry barriers could also mention that, based on the end user, the segment of the hospitals held majoline statin market share, if measured appropriately. Cardiovascular diseases are well-taken today, and treatment for such diseases requires hospitals where statin drugs are of importance. Knowing that hypercholesterolemia and atherosclerosis are not unique pathologies, many hospitals encounter patients who require statins and prevention of myocardial infarctions and strokes. Hospitals are great developed, complex systems in which qualified medical staff is appropriate for the recognition, treatment, and subsequent monitoring of such patients with severe and chronic CV diseases that may need statin therapy which is the main setting for initiation and regulation.

- Moreover, many hospitals are referred to as clinics or centres for physician and other health care professionals training, this changes the way that patients with hyperlipidemia are treated and develops new anti-statins therapies. Given that cardiovascular diseases continue to be one of the key and deadly threats to global population, the segment of hospitals still claims to be the key market driver of statins that ensure the patients will have an improved prognosis of the management of their cholesterol levels in case of a highly complex picture of the disease.

Statin Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

- It must be noted that North America will emerge as the largest consumer of statins in the course of the forecast period, backed by the following factors. This area has a good healthcare system and high levels of lipid profile awareness; people undergo screening and early detection of such ailments such as hypercholesterolemia. Also, the reimbursement policies are more favourable and insurance covers for the statin medications increase the rate of patients’ usage. The existence of fundamental firms of the pharmaceutical industry investing heavily in research and development is another positive factor for the market’s growth. Also, unstable demographic indicators, coupled with a tendency towards an aging population and a higher incidence of diseases related to improper nutrition, prove that there is a significant need for efficient management of cholesterol levels. Together these factors make North America one of the largest consumer of statin drugs, which is again expected to remain dominant in the future years.

Active Key Players in the Statin Market

- Abbott Laboratories (USA)

- Amgen Inc. (USA)

- AstraZeneca PLC (UK)

- Bayer AG (Germany)

- Bristol-Myers Squibb Company (USA)

- Daiichi Sankyo Company, Limited (Japan)

- GlaxoSmithKline plc (UK)

- Johnson & Johnson (USA)

- Merck & Co., Inc. (USA)

- Mylan N.V. (USA)

- Novartis AG (Switzerland)

- Pfizer Inc. (USA)

- Sanofi (France)

- Sun Pharmaceutical Industries Ltd. (India)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Other key Players

|

Statin Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 16 Bn. |

|

Forecast Period 2025-35 CAGR: |

3.2% |

Market Size in 2035: |

USD 22.63 Bn. |

|

Segments Covered: |

By Drug Class |

|

|

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Statin Market by Drug Class (2018-2035)

4.1 Statin Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Astrovastatin

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Fluvastatin

4.5 Lovastatin

4.6 Pravastatin

4.7 Simvastatin

4.8 Others

Chapter 5: Statin Market by End User (2018-2035)

5.1 Statin Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Hospitals

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Clinics

Chapter 6: Company Profiles and Competitive Analysis

6.1 Competitive Landscape

6.1.1 Competitive Benchmarking

6.1.2 Statin Market Share by Manufacturer (2024)

6.1.3 Industry BCG Matrix

6.1.4 Heat Map Analysis

6.1.5 Mergers and Acquisitions

6.2 ABBOTT LABORATORIES (USA)

6.2.1 Company Overview

6.2.2 Key Executives

6.2.3 Company Snapshot

6.2.4 Role of the Company in the Market

6.2.5 Sustainability and Social Responsibility

6.2.6 Operating Business Segments

6.2.7 Product Portfolio

6.2.8 Business Performance

6.2.9 Key Strategic Moves and Recent Developments

6.2.10 SWOT Analysis

6.3 AMGEN INC. (USA)

6.4 ASTRAZENECA PLC (UK)

6.5 BAYER AG (GERMANY)

6.6 BRISTOL-MYERS SQUIBB COMPANY (USA)

6.7 DAIICHI SANKYO COMPANY

6.8 LIMITED (JAPAN)

6.9 GLAXOSMITHKLINE PLC (UK)

6.10 JOHNSON & JOHNSON (USA)

6.11 MERCK & COINC. (USA)

6.12 MYLAN N.V. (USA)

6.13 NOVARTIS AG (SWITZERLAND)

6.14 PFIZER INC. (USA)

6.15 SANOFI (FRANCE)

6.16 SUN PHARMACEUTICAL INDUSTRIES LTD. (INDIA)

6.17 TEVA PHARMACEUTICAL INDUSTRIES LTD. (ISRAEL)

6.18 OTHER KEY PLAYERS

Chapter 7: Global Statin Market By Region

7.1 Overview

7.2. North America Statin Market

7.2.1 Key Market Trends, Growth Factors and Opportunities

7.2.2 Top Key Companies

7.2.3 Historic and Forecasted Market Size by Segments

7.2.4 Historic and Forecasted Market Size by Drug Class

7.2.4.1 Astrovastatin

7.2.4.2 Fluvastatin

7.2.4.3 Lovastatin

7.2.4.4 Pravastatin

7.2.4.5 Simvastatin

7.2.4.6 Others

7.2.5 Historic and Forecasted Market Size by End User

7.2.5.1 Hospitals

7.2.5.2 Clinics

7.2.6 Historic and Forecast Market Size by Country

7.2.6.1 US

7.2.6.2 Canada

7.2.6.3 Mexico

7.3. Eastern Europe Statin Market

7.3.1 Key Market Trends, Growth Factors and Opportunities

7.3.2 Top Key Companies

7.3.3 Historic and Forecasted Market Size by Segments

7.3.4 Historic and Forecasted Market Size by Drug Class

7.3.4.1 Astrovastatin

7.3.4.2 Fluvastatin

7.3.4.3 Lovastatin

7.3.4.4 Pravastatin

7.3.4.5 Simvastatin

7.3.4.6 Others

7.3.5 Historic and Forecasted Market Size by End User

7.3.5.1 Hospitals

7.3.5.2 Clinics

7.3.6 Historic and Forecast Market Size by Country

7.3.6.1 Russia

7.3.6.2 Bulgaria

7.3.6.3 The Czech Republic

7.3.6.4 Hungary

7.3.6.5 Poland

7.3.6.6 Romania

7.3.6.7 Rest of Eastern Europe

7.4. Western Europe Statin Market

7.4.1 Key Market Trends, Growth Factors and Opportunities

7.4.2 Top Key Companies

7.4.3 Historic and Forecasted Market Size by Segments

7.4.4 Historic and Forecasted Market Size by Drug Class

7.4.4.1 Astrovastatin

7.4.4.2 Fluvastatin

7.4.4.3 Lovastatin

7.4.4.4 Pravastatin

7.4.4.5 Simvastatin

7.4.4.6 Others

7.4.5 Historic and Forecasted Market Size by End User

7.4.5.1 Hospitals

7.4.5.2 Clinics

7.4.6 Historic and Forecast Market Size by Country

7.4.6.1 Germany

7.4.6.2 UK

7.4.6.3 France

7.4.6.4 The Netherlands

7.4.6.5 Italy

7.4.6.6 Spain

7.4.6.7 Rest of Western Europe

7.5. Asia Pacific Statin Market

7.5.1 Key Market Trends, Growth Factors and Opportunities

7.5.2 Top Key Companies

7.5.3 Historic and Forecasted Market Size by Segments

7.5.4 Historic and Forecasted Market Size by Drug Class

7.5.4.1 Astrovastatin

7.5.4.2 Fluvastatin

7.5.4.3 Lovastatin

7.5.4.4 Pravastatin

7.5.4.5 Simvastatin

7.5.4.6 Others

7.5.5 Historic and Forecasted Market Size by End User

7.5.5.1 Hospitals

7.5.5.2 Clinics

7.5.6 Historic and Forecast Market Size by Country

7.5.6.1 China

7.5.6.2 India

7.5.6.3 Japan

7.5.6.4 South Korea

7.5.6.5 Malaysia

7.5.6.6 Thailand

7.5.6.7 Vietnam

7.5.6.8 The Philippines

7.5.6.9 Australia

7.5.6.10 New Zealand

7.5.6.11 Rest of APAC

7.6. Middle East & Africa Statin Market

7.6.1 Key Market Trends, Growth Factors and Opportunities

7.6.2 Top Key Companies

7.6.3 Historic and Forecasted Market Size by Segments

7.6.4 Historic and Forecasted Market Size by Drug Class

7.6.4.1 Astrovastatin

7.6.4.2 Fluvastatin

7.6.4.3 Lovastatin

7.6.4.4 Pravastatin

7.6.4.5 Simvastatin

7.6.4.6 Others

7.6.5 Historic and Forecasted Market Size by End User

7.6.5.1 Hospitals

7.6.5.2 Clinics

7.6.6 Historic and Forecast Market Size by Country

7.6.6.1 Turkiye

7.6.6.2 Bahrain

7.6.6.3 Kuwait

7.6.6.4 Saudi Arabia

7.6.6.5 Qatar

7.6.6.6 UAE

7.6.6.7 Israel

7.6.6.8 South Africa

7.7. South America Statin Market

7.7.1 Key Market Trends, Growth Factors and Opportunities

7.7.2 Top Key Companies

7.7.3 Historic and Forecasted Market Size by Segments

7.7.4 Historic and Forecasted Market Size by Drug Class

7.7.4.1 Astrovastatin

7.7.4.2 Fluvastatin

7.7.4.3 Lovastatin

7.7.4.4 Pravastatin

7.7.4.5 Simvastatin

7.7.4.6 Others

7.7.5 Historic and Forecasted Market Size by End User

7.7.5.1 Hospitals

7.7.5.2 Clinics

7.7.6 Historic and Forecast Market Size by Country

7.7.6.1 Brazil

7.7.6.2 Argentina

7.7.6.3 Rest of SA

Chapter 8 Analyst Viewpoint and Conclusion

8.1 Recommendations and Concluding Analysis

8.2 Potential Market Strategies

Chapter 9 Research Methodology

9.1 Research Process

9.2 Primary Research

9.3 Secondary Research

|

Statin Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 16 Bn. |

|

Forecast Period 2025-35 CAGR: |

3.2% |

Market Size in 2035: |

USD 22.63 Bn. |

|

Segments Covered: |

By Drug Class |

|

|

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||