Semiconductor Manufacturing Equipment Market Synopsis:

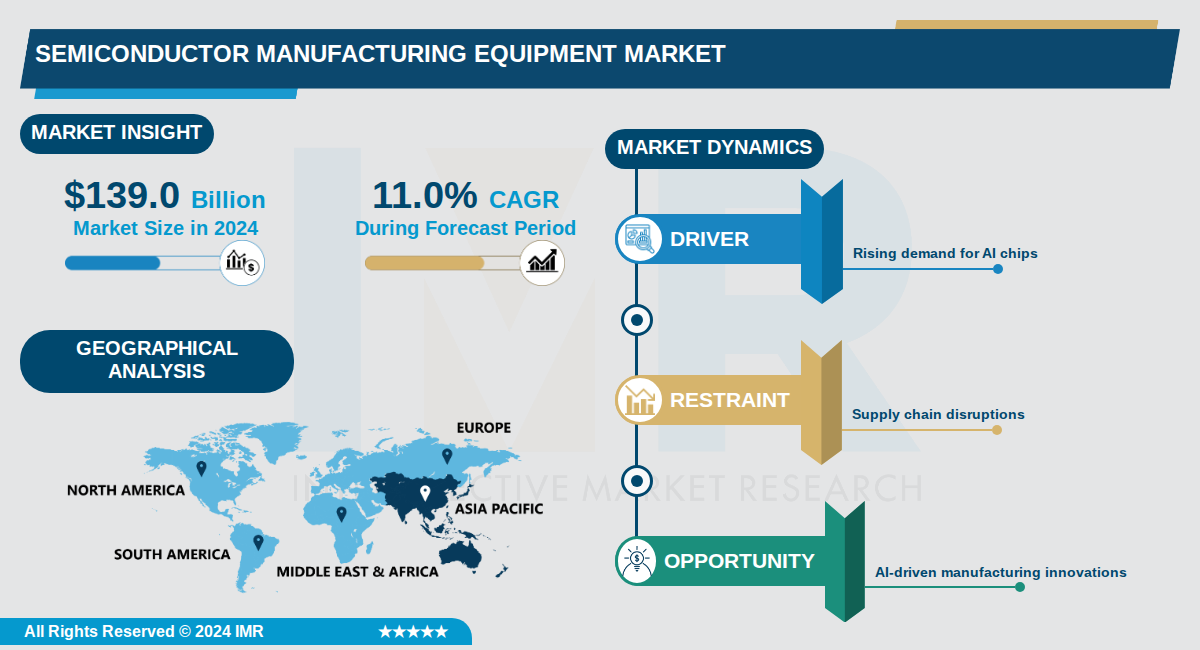

Semiconductor Manufacturing Equipment Market Size Was Valued at USD 139.0 Billion in 2024, and is Projected to Reach USD 466.0 Billion by 2035, Growing at a CAGR of 11.0% From 2024-2035.

The Semiconductor Manufacturing Equipment Market reached $139.0 billion in 2024 and is projected to expand to $466.0 billion by 2035, achieving a compound annual growth rate (CAGR) of 11.0%. This robust growth reflects the escalating global demand for advanced semiconductors driven by digital transformation, AI innovations, and the proliferation of high-performance computing applications.

Asia Pacific dominates the market, holding approximately 68% share in 2024, fueled by major exporters like China, Japan, and Korea, alongside a surge in semiconductor fabrication plants and outsourced assembly and test (OSAT) vendors. Front-end equipment leads by type, while semiconductor fabrication plants or foundries represent the largest application segment, underscoring the focus on wafer production and advanced node technologies.

Key trends include advancements in 3D integrated circuits, EUV lithography, and AI-driven manufacturing processes, with the United States bolstering domestic capabilities through investments in innovation and supply chain resilience. The market is segmented by front-end and back-end equipment, dimensions such as 2D/2.5D and 3D, and regions including North America, Europe, and emerging markets.

Semiconductor Manufacturing Equipment Market Trend Analysis:

Surge in High-Bandwidth Memory Equipment Demand

- High-bandwidth memory (HBM) production ramps are driving explosive growth in semiconductor equipment sales, with DRAM equipment projected to rise 15.4% to $22.5 billion in 2025 and continue with 15.1% growth in 2026. This surge exceeds earlier forecasts due to stronger-than-expected AI computing investments by companies like NVIDIA and AMD. South Korea, home to Samsung and SK Hynix, is leading this trend with equipment spending forecasted to jump 27.2% to $29.66 billion in 2026.

- HBM expansion is boosting demand for specialized equipment in lithography, atomic layer deposition (ALD), and hybrid bonding processes. Samsung's HBM3E production and SK Hynix's leadership in HBM supply for AI GPUs are key catalysts, fueling investments in deposition and etching tools. This shift supports the transition to DDR5 DRAM, enabling higher data throughput for data centers.

- Global OEM sales are set to hit a record $133 billion in 2025, with HBM-related investments pushing wafer fabrication equipment (WFE) to $115.7 billion, up 11% from 2024.

Rapid Adoption of Advanced Packaging Technologies

- Back-end equipment sales for assembly and packaging are surging 19.6% to $6.4 billion in 2025, driven by heterogeneous integration and advanced packaging for AI chips. Test equipment follows with a 48.1% jump to $11.2 billion, addressing the complexity of 3D stacking and high-density interconnects. Companies like TSMC are scaling CoWoS and InFO packaging to meet NVIDIA's GPU demands.

- Heterogeneous packaging enables stacking of logic, memory, and sensors, reducing latency for AI workloads. SEMI highlights this as a core driver offsetting softness in consumer and automotive segments. Applied Materials' initiatives, such as the ASCENT program in India, are accelerating equipment innovations for these processes.

- The trend supports front-end to back-end synergy, with overall equipment sales reaching $145 billion in 2026, as advanced packaging fuels three years of consecutive growth.

Shift to High-NA EUV Lithography for Sub-2nm Nodes

- ASML and imec launched a High-NA EUV lithography lab in June 2024 to pioneer sub-2nm processes, targeting gate-all-around (GAA) transistors at the 2nm node. This facility tests next-generation systems critical for Intel, TSMC, and Samsung's leading-edge logic fabs entering high-volume manufacturing. Front-end equipment, holding 71.7% market share, is expanding to support EUV for extreme miniaturization.

- Investments in extreme ultraviolet lithography support equipment, wafer inspection, and process control tools are accelerating, backed by U.S. CHIPS Act funding for domestic fabs. North America's fastest growth stems from reshoring, with grants enabling expansions like TSMC's Arizona facility requiring High-NA tools. This positions the market for sustained wafer fab equipment growth to $75.2 billion by 2027.

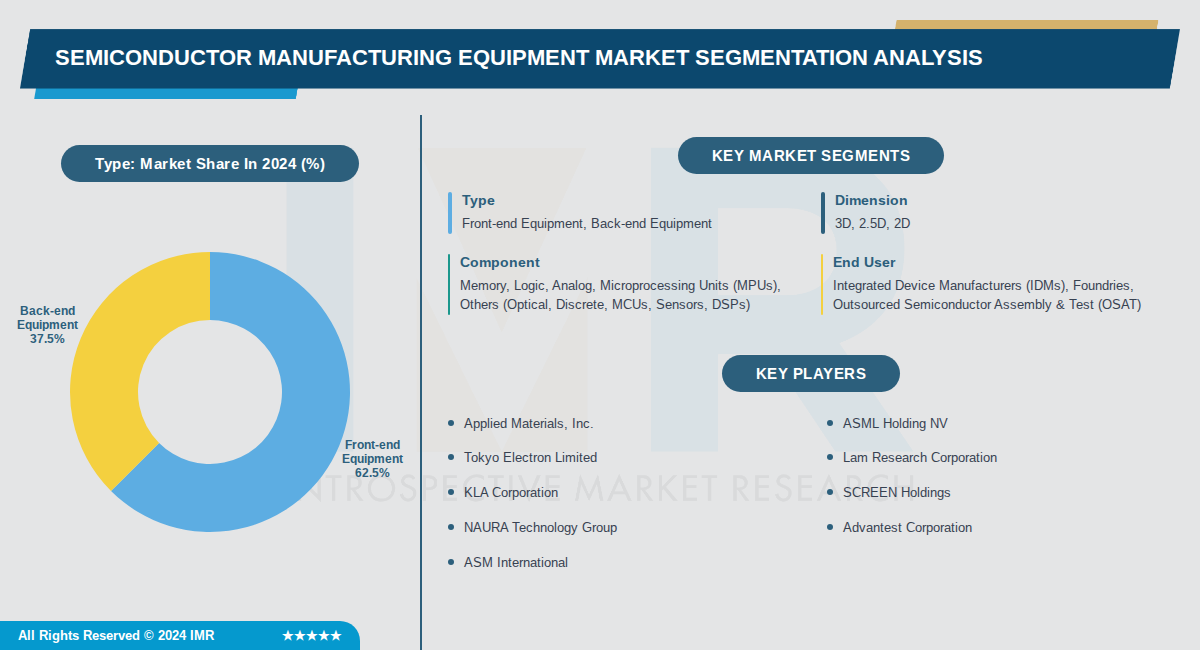

Semiconductor Manufacturing Equipment Market Segment Analysis:

Semiconductor Manufacturing Equipment Market is Segmented on the basis of By Type, By Dimension, By Component

By Type, Front-end Equipment segment is expected to dominate the market during the forecast period

- Front-end equipment dominates due to its critical role in wafer fabrication and lithography processes essential for advanced node semiconductors.

- It accounts for over 60% of the market driven by surging demand for AI chips and high-performance computing requiring precise front-end manufacturing.

By Dimension, 3D segment is expected to dominate the market during the forecast period

- 3D dimension leads due to increasing adoption for miniaturization, improved functionalities, and higher integration density in portable devices.

- It held the largest share in 2022 and grows fastest from demand for rapid prototyping and advanced packaging like chip stacking.

By Component, Memory segment is expected to dominate the market during the forecast period

- Memory segment dominates from high consumption in consumer electronics like smartphones, SSDs, and data centers requiring massive DRAM and NAND production.

- It captured the largest share in 2022 fueled by explosive growth in AI training models and cloud computing infrastructure.

By End User, Integrated Device Manufacturers (IDMs) segment is expected to dominate the market during the forecast period

- IDMs lead due to their vertical integration controlling design, fabrication, and assembly for high-volume consumer electronics.

- They held the largest share in 2022 from significant market presence and rising demand for design-foundry services.

Semiconductor Manufacturing Equipment Market Regional Insights:

Asia-Pacific Dominates the Semiconductor Manufacturing Equipment Market

- Asia-Pacific dominates the global semiconductor manufacturing equipment market, accounting for over 60% of demand, driven by key countries like South Korea, Taiwan, China, and Japan. Taiwan hosts TSMC's advanced facilities, while South Korea leverages Samsung's manufacturing scale. China's self-sufficiency efforts have spurred massive equipment investments despite export challenges.

- The region benefits from massive fab investments, government support, and integrated supply chains near electronics hubs. It leads in adopting cutting-edge technologies like EUV lithography, with foundries creating a cycle of innovation and prioritized deployments. Proximity enables rapid maintenance and process optimization.

- Major players like ASML, Applied Materials, and Lam Research focus on Asia-Pacific for new tools, with local support centers. Recent expansions include China's fab growth and Taiwan/South Korea's advanced node developments. North America grows via CHIPS Act but trails in manufacturing capacity.

Active Key Players in the Semiconductor Manufacturing Equipment Market:

- Applied Materials, Inc. (USA)

- ASML Holding NV (Netherlands)

- Tokyo Electron Limited (Japan)

- Lam Research Corporation (USA)

- KLA Corporation (USA)

- SCREEN Holdings (Japan)

- NAURA Technology Group (China)

- Advantest Corporation (Japan)

- ASM International (Netherlands)

- Hitachi High-Tech Corporation (Japan)

- Teradyne Inc. (USA)

- Lasertec Corporation (Japan)

- DISCO Corporation (Japan)

- Canon Inc. (Japan)

- Nikon Precision Inc. (Japan)

- AMEC (China)

- Piotech (China)

- Other Active Players

|

Semiconductor Manufacturing Equipment Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 139.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

11.0 % |

Market Size in 2035: |

USD 466.0 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Dimension |

|

||

|

By Component |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Semiconductor Manufacturing Equipment Market by Type (2017-2035)

4.1 Semiconductor Manufacturing Equipment Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Front-end Equipment

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Back-end Equipment

Chapter 5: Semiconductor Manufacturing Equipment Market by Dimension (2017-2035)

5.1 Semiconductor Manufacturing Equipment Market Snapshot and Growth Engine

5.2 Market Overview

5.3 3D

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 2.5D

5.5 2D

Chapter 6: Semiconductor Manufacturing Equipment Market by Component (2017-2035)

6.1 Semiconductor Manufacturing Equipment Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Memory

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Logic

6.5 Analog

6.6 Microprocessing Units (MPUs)

6.7 Others (Optical

6.8 Discrete

6.9 MCUs

6.10 Sensors

6.11 DSPs)

Chapter 7: Semiconductor Manufacturing Equipment Market by End User (2017-2035)

7.1 Semiconductor Manufacturing Equipment Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Integrated Device Manufacturers (IDMs)

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Foundries

7.5 Outsourced Semiconductor Assembly & Test (OSAT)

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Semiconductor Manufacturing Equipment Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 APPLIED MATERIALS

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 INC.

8.4 ASML HOLDING NV

8.5 TOKYO ELECTRON LIMITED

8.6 LAM RESEARCH CORPORATION

8.7 KLA CORPORATION

8.8 SCREEN HOLDINGS

8.9 NAURA TECHNOLOGY GROUP

8.10 ADVANTEST CORPORATION

8.11 ASM INTERNATIONAL

8.12 HITACHI HIGH-TECH CORPORATION

8.13 TERADYNE INC.

8.14 LASERTEC CORPORATION

8.15 DISCO CORPORATION

8.16 CANON INC.

8.17 NIKON PRECISION INC.

8.18 AMEC

8.19 PIOTECH

Chapter 9: Global Semiconductor Manufacturing Equipment Market By Region

9.1 Overview

9.2. North America Semiconductor Manufacturing Equipment Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Semiconductor Manufacturing Equipment Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Semiconductor Manufacturing Equipment Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Semiconductor Manufacturing Equipment Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Semiconductor Manufacturing Equipment Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Semiconductor Manufacturing Equipment Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Semiconductor Manufacturing Equipment Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 139.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

11.0 % |

Market Size in 2035: |

USD 466.0 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Dimension |

|

||

|

By Component |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||