Packaged Food Market Synopsis

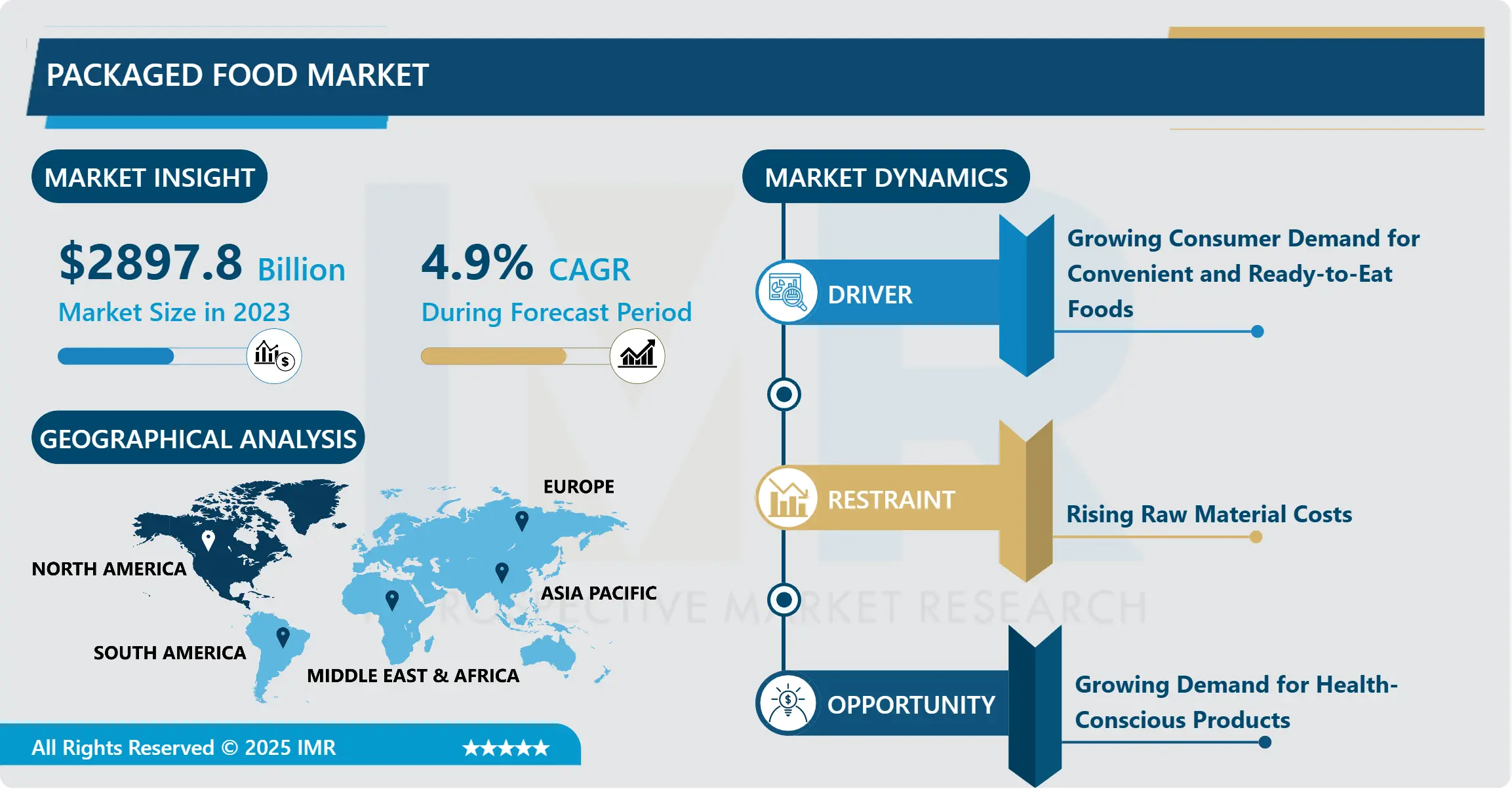

Packaged Food Market Size Was Valued at USD 2,897.80 Billion in 2023, and is Projected to Reach USD 4,457.05 Billion by 2032, Growing at a CAGR of 4.90% From 2024-2032.

Packaged foods are the foods that are processed, packed and sealed before being sold in food packages with the aim of facilitating its storage and handling. This category revolves around foods that are easy to store and consume, and they include; snacks, frozen foods, canned foods and ready to cook foods.

The packaged food market has been through a lot of changes in the last few years due to the increased rates of urbanization and change in meal habits. With the increasing cases of people taking busy schedules in their work and other everyday activities, convenience food and easy to prepare food products are on high demand. It has been realized that this generation especially the millennials and the Generation Z have become more inclined to purchase ready to eat foods that are convenient to prepare without having to compromise on quality. Therefore, there has been an advancement in the manufacturers’ type of products that they deliver to the market, especially packaged foods that are characteristic of todays’ consumers’ preferences including plant-based and organic foods. Further, the increasing market of e- shopping and food delivery services have accelerated the market growth for the packed foods as people can also purchase their foods online. Opportunity to select various stored products among international cuisines and specialized foods has influenced consumers to select new flavors and brands thus widening the market coverage.

The trends in joining the proactive health and wellness movement have also impacted on the packaged foods segment. Safety consciousness has become high and thus consumers prefer to have foods that are nutrient dense and have good labels. The food processing companies are also changing their strategies by decreasing sugar, sodium, artificial components and at the same time improving the nutritional value of the packag FlatButton[1[4]. Besides, the clean label movement, which focuses on the origin of the used ingredients, has evolved, and companies started to declare product origins and its positive effects on health. Another factor that has shifted the clients’ eating habits is the increased publicity regarding food hygiene and the environment; the clients have preferred products packed in environmentally friendly ways and use ingredients sourced in a sustainable manner. Therefore, those brands adopting environmental and transparency characteristics to their products will help them set more market share.

Therefore I say that the packaged food market and the market in general is not without challenges. As far as potential threats are concerned, manufacturers may be confronted with risks associated with supply chain, supplies and raw material prices Instability, and emergence of new competitors. However, the regulatory forces in preserving food safety and labeling laws force companies to be responsive and to be conformant periodically meaning that they need to invest some of their capital in improving quality and legal conformity measures. It would be vital to maintain competitive advantage owing to the challenges identified above, innovation will play a critical role. The brands that will employ state-of-the-art technologies like artificial intelligence and data analytics to solve client tastes for products and services while streamlining their operations stand to benefit from the increase in market information.

The global market for packaged food is steadily changing due to consumers’ desire for easy, healthy, and environmentally friendly food options. While the existing trends unravel, there are possibilities of new trends arising as consumers’ preferences today dictate the market in the future. It is important for firms to increase innovation invest in transparency, and maintaining high quality to meet the demands of they consumers due to the stiff competition and the ever emergent market forces. It will be quite interesting to understand how the consumer tendencies of named trends evolve during the market’s development and how the companies adapt to them and orient the experience of packaged food consumers.

Packaged Food Market Trend Analysis

Convenience and On-the-Go Options

- The global Packaged Food Market segmented into Convenience and On-the-Go Options has experienced a remarkable growth due to the shift in customer preference in virtue of their hectic schedules for which they are inclined toward convenience food products. Today’s consumers especially the working people and families with many responsibilities, they are more interested in convenient foods because they have little time and energy preparing meals due to their tight schedules hence the increased demand for processed foods that are easy to carry and prepare. This market comprises products such as single-serve meals, snacks and fully cooked products which are oriented to different segment such as health conscious. Such products also continue to enjoy support from growing e-commerce and online grocery business that enhances the buying habits of consumers.

- As a result of this increasing demand, producers are constantly changing their products, for instance by making them healthier, e. g through use of better packaging materials and a variety of flavors. Special categories of products like plant based or organic products are coming up that is in line with the direction that the consumer wants foods that are healthy for consumption but easy to get. Furthermore, marketing aspects are shifting towards the perceived benefits and stuff, given the fact that people have little time at their disposal to bother with a proper diet. Therefore, the Convenience and On-the-Go Options Packaged Food Market is projected to grow further as brands undertake new research and innovation to conform to consumer demands.

Growing Demand for Health-Conscious Products

- The changing trends in the global marketplace are quickly taking into consideration the global increase in the demand for a healthier food product in the packed food market. This means today’s consumers are labeling conscious, eating foods with little or no added sugar, high in protein, organic, and no additives. It is most evident in the purchases made by the younger population that tends to value the quality and the nutritional value of the food products. Therefore, food producers and makers are changing existing products and creating new ones that are in line with such heath-conscious demands. This shift is also seen in functional foods that are food products that are manufactured to have health benefits over and above the basic nutrition, thus enhancing the overall market.

- Besides, due to the COVID-19 pandemic began in 2020, consumers shifted their focus on health, paying attention to immune-boosting components and overall wellness. Businesses are leveraging on clean label agenda and sustainability in order to meet the demands of consumers with a conscience who are willing to spend more on foods and beverages that have little processing and packaging that is friendly to the environment. Market players are also coming up with new advanced technologies to support them in product development through accumulation of data resulting in identification of trends and consumer preferences. With the growth of packaged food market, it is believed that the focus on health and wellness will remain prevalent across the packaged food market, manufacturers, marketer and retailers would continue to innovate in formulation, positioning and placements.

Packaged Food Market Segment Analysis:

Packaged Food Market Segmented based on Type, Packaging Type and Distribution Channel.

By Type, Snacks segment is expected to dominate the market during the forecast period

- The Packaged Food Market, based on type, encompasses several different categories that fulfill the different needs and wants of customers. The Dairy product category comprises products like milk, cheese, and yogurt and accounts for a large portion of the market due to their dietary importance and nutrient value to humans. Confectionery products like chocolates, candies, or sweets flourish on consumers' indulgences in them and on seasonality. Beers, both nonbeverage and beverages, have shown dynamic growth due to flavor innovations and products that are friendly to healthy livers. Bakery products-bread and cakes-record stable market shares because these are staple dietary, even as snack items like potato chips and energy bars respond to the consumer demand for on-the-go consumption. The meat, poultry, and seafood categories also respond to this consumer trend, with business registering most interest in packaged convenience.

- The growth in the market for breakfast cereals and ready meals is apparent based on the desire of the consumers to find quick and healthy meals while innovations in flavor and nutritional content also are improving such offerings. Ready meals, for instance, have become more popular than ever as such lifestyles in cities are saving time. Other categories comprising frozen and organic foods merely depict the diversification of consumer preferences, especially those relating to health and sustainability. Overall market size will continue to trend upwards as packaged food manufacturers innovate by way of offering diversity, upgradation in quality, and adherence to dietary restrictions, be it gluten-free, organic, or vegan.

By Packaging Type , Tetra Pack segment held the largest share in 2023

- The food packaging market can mainly be divided by the packing type for the packaged food and the major driving forces behind this market are the convenience, preservation, and sustainability. Most singularly yet still ahead of the curve are plastic packagings by their flexibility to shape and to need of food, and the price it costs, in their function of protecting food from contamination. It is applied predominantly in the dairy products, snack food and beverages industry, however awareness of environment and ecological issues is posing pressure on manufacturers to seek environmentally friendly material. Long shelf life of Tetra Packs , commonly used for milk and juice enhances their consumption in areas with minimal refrigeration facilities especially in the under developed.

- The package has a selling point for environmentally aware consumers due to the recyclable aspect of the packag.Metal cans are preferred as they do not accommodate any form of decay of foods such as meat, fish and meals due to dintinuity of the metal cans and thus are suitable for preserving foods for longer duration. Used extensively in long life products, endows them with enough strength to cope with competition despite the acceptance of lightweight ones. The “Others” category comprises of creative materials, including biodegradable packaging, and glasses, in which consumers and manufacturers are equally adopting change for sustainability. With increasing consciousness on going green, new ways by which firms carry out packaging material which is sustainably is set to define future growth of the packaged food industry.

Packaged Food Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

- According to the Packaged Food Market research study, North America is projected to lead within the forecast period because of escalating demand of Packaged foods due to shift in customer’s preference, demand for convenience, and soaring food processing techniques. The rising trend of convenience food, snacking, and healthy foods including organic and gluten-free products has driven the market. The convenience owing to busy lifestyles and increase in overall disposable income have also played a role in increasing the demand of packaged foods in developed countries such as the United States and Canada. Further, developing retail systems and constant growth of online grocery shops that allow consumers easily buying various types of packaged foods bolster the regional market foremost position.

- Furthermore, diversification of packaging materials with increased attention to sustainable packaging solutions in the North American region is on the rise due to growing concerns of the environment. The leading market players are oriented to invest more money in the development of new products in the packed food industry as the consumer preference is shifting to healthier, convenient, and green products. The growth of food manufacturing companies and legal control of food hygiene in North America are expected to maintain region’s strong market position in the global packaged food market in the near future.

Active Key Players in the Packaged Food Market

- Conagra Brands Inc. (United States)

- Danone S.A. (France)

- General Mills Inc. (United States)

- Hormel Foods Corporation (United States)

- JBS S.A. (Brazil)

- Kellogg Company (United States)

- Maple Leaf Foods Inc. (Canada)

- Nestlé S.A. (Switzerland)

- PepsiCo Inc. (United States)

- The Coca-Cola Company (United States)

- The Kraft Heinz Company (United States)

- Tyson Foods Inc. (United States)

- WH Group Limited (China)

- Others Key Player

Key Industry Developments in the Packaged Food Market

- In June 2021, Tyson Foods introduced new plant-based products under the brand of First Pride™ catering to Asia’s expanding market. Post the launch. This line has been available on eCommerce channels and select retail markets across Asia Pacific.

- In May 2023, Reliance Consumer Products Ltd reportedly entered the western snacking category with the debut of General Mills’ Alan’s Bugles brand of chips in the India market. This move is set to give tight competition to ITC and PepsiCo.

- In August 2023, General Mills announced that it would release and test its newest brand, Yumble, a DTC delivery service that intends to give a stress-free spin to lunch and snack time for parents by offering customizable lunch kits.

Global Packaged Food Market Scope:

|

Global Packaged Food Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 2,897.80 Bn. |

|

Forecast Period 2024-32 CAGR: |

4.90% |

Market Size in 2032: |

USD 4,457.05 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Packaging Type |

|

||

|

By Distribution Channel |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Packaged Food Market by Type (2018-2032)

4.1 Packaged Food Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Dairy Products

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Confectionery

4.5 Beverage

4.6 Bakery

4.7 Snacks

4.8 Meat

4.9 Poultry and Seafood

4.10 Breakfast Cereals

4.11 Ready Meals

4.12 Others

Chapter 5: Packaged Food Market by Packaging Type (2018-2032)

5.1 Packaged Food Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Plastic Packaging

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Tetra Pack

5.5 Metal Cans

5.6 Others

Chapter 6: Packaged Food Market by Distribution Channel (2018-2032)

6.1 Packaged Food Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Supermarkets/Hypermarkets

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Specialty Stores

6.5 Convenience Stores

6.6 Online Retail Stores

6.7 Others

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Packaged Food Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 CONAGRA BRANDS INC. (UNITED STATES)

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 DANONE S.A. (FRANCE)

7.4 GENERAL MILLS INC. (UNITED STATES)

7.5 HORMEL FOODS CORPORATION (UNITED STATES)

7.6 JBS S.A. (BRAZIL)

7.7 KELLOGG COMPANY (UNITED STATES)

7.8 MAPLE LEAF FOODS INC. (CANADA)

7.9 NESTLÉ S.A. (SWITZERLAND)

7.10 PEPSICO INC. (UNITED STATES)

7.11 THE COCA-COLA COMPANY (UNITED STATES)

7.12 THE KRAFT HEINZ COMPANY (UNITED STATES)

7.13 TYSON FOODS INC. (UNITED STATES)

7.14 WH GROUP LIMITED (CHINA)

7.15 OTHERS KEY PLAYER

Chapter 8: Global Packaged Food Market By Region

8.1 Overview

8.2. North America Packaged Food Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size by Type

8.2.4.1 Dairy Products

8.2.4.2 Confectionery

8.2.4.3 Beverage

8.2.4.4 Bakery

8.2.4.5 Snacks

8.2.4.6 Meat

8.2.4.7 Poultry and Seafood

8.2.4.8 Breakfast Cereals

8.2.4.9 Ready Meals

8.2.4.10 Others

8.2.5 Historic and Forecasted Market Size by Packaging Type

8.2.5.1 Plastic Packaging

8.2.5.2 Tetra Pack

8.2.5.3 Metal Cans

8.2.5.4 Others

8.2.6 Historic and Forecasted Market Size by Distribution Channel

8.2.6.1 Supermarkets/Hypermarkets

8.2.6.2 Specialty Stores

8.2.6.3 Convenience Stores

8.2.6.4 Online Retail Stores

8.2.6.5 Others

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Packaged Food Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size by Type

8.3.4.1 Dairy Products

8.3.4.2 Confectionery

8.3.4.3 Beverage

8.3.4.4 Bakery

8.3.4.5 Snacks

8.3.4.6 Meat

8.3.4.7 Poultry and Seafood

8.3.4.8 Breakfast Cereals

8.3.4.9 Ready Meals

8.3.4.10 Others

8.3.5 Historic and Forecasted Market Size by Packaging Type

8.3.5.1 Plastic Packaging

8.3.5.2 Tetra Pack

8.3.5.3 Metal Cans

8.3.5.4 Others

8.3.6 Historic and Forecasted Market Size by Distribution Channel

8.3.6.1 Supermarkets/Hypermarkets

8.3.6.2 Specialty Stores

8.3.6.3 Convenience Stores

8.3.6.4 Online Retail Stores

8.3.6.5 Others

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Packaged Food Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size by Type

8.4.4.1 Dairy Products

8.4.4.2 Confectionery

8.4.4.3 Beverage

8.4.4.4 Bakery

8.4.4.5 Snacks

8.4.4.6 Meat

8.4.4.7 Poultry and Seafood

8.4.4.8 Breakfast Cereals

8.4.4.9 Ready Meals

8.4.4.10 Others

8.4.5 Historic and Forecasted Market Size by Packaging Type

8.4.5.1 Plastic Packaging

8.4.5.2 Tetra Pack

8.4.5.3 Metal Cans

8.4.5.4 Others

8.4.6 Historic and Forecasted Market Size by Distribution Channel

8.4.6.1 Supermarkets/Hypermarkets

8.4.6.2 Specialty Stores

8.4.6.3 Convenience Stores

8.4.6.4 Online Retail Stores

8.4.6.5 Others

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Packaged Food Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size by Type

8.5.4.1 Dairy Products

8.5.4.2 Confectionery

8.5.4.3 Beverage

8.5.4.4 Bakery

8.5.4.5 Snacks

8.5.4.6 Meat

8.5.4.7 Poultry and Seafood

8.5.4.8 Breakfast Cereals

8.5.4.9 Ready Meals

8.5.4.10 Others

8.5.5 Historic and Forecasted Market Size by Packaging Type

8.5.5.1 Plastic Packaging

8.5.5.2 Tetra Pack

8.5.5.3 Metal Cans

8.5.5.4 Others

8.5.6 Historic and Forecasted Market Size by Distribution Channel

8.5.6.1 Supermarkets/Hypermarkets

8.5.6.2 Specialty Stores

8.5.6.3 Convenience Stores

8.5.6.4 Online Retail Stores

8.5.6.5 Others

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Packaged Food Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size by Type

8.6.4.1 Dairy Products

8.6.4.2 Confectionery

8.6.4.3 Beverage

8.6.4.4 Bakery

8.6.4.5 Snacks

8.6.4.6 Meat

8.6.4.7 Poultry and Seafood

8.6.4.8 Breakfast Cereals

8.6.4.9 Ready Meals

8.6.4.10 Others

8.6.5 Historic and Forecasted Market Size by Packaging Type

8.6.5.1 Plastic Packaging

8.6.5.2 Tetra Pack

8.6.5.3 Metal Cans

8.6.5.4 Others

8.6.6 Historic and Forecasted Market Size by Distribution Channel

8.6.6.1 Supermarkets/Hypermarkets

8.6.6.2 Specialty Stores

8.6.6.3 Convenience Stores

8.6.6.4 Online Retail Stores

8.6.6.5 Others

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Packaged Food Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size by Type

8.7.4.1 Dairy Products

8.7.4.2 Confectionery

8.7.4.3 Beverage

8.7.4.4 Bakery

8.7.4.5 Snacks

8.7.4.6 Meat

8.7.4.7 Poultry and Seafood

8.7.4.8 Breakfast Cereals

8.7.4.9 Ready Meals

8.7.4.10 Others

8.7.5 Historic and Forecasted Market Size by Packaging Type

8.7.5.1 Plastic Packaging

8.7.5.2 Tetra Pack

8.7.5.3 Metal Cans

8.7.5.4 Others

8.7.6 Historic and Forecasted Market Size by Distribution Channel

8.7.6.1 Supermarkets/Hypermarkets

8.7.6.2 Specialty Stores

8.7.6.3 Convenience Stores

8.7.6.4 Online Retail Stores

8.7.6.5 Others

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

Global Packaged Food Market Scope:

|

Global Packaged Food Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 2,897.80 Bn. |

|

Forecast Period 2024-32 CAGR: |

4.90% |

Market Size in 2032: |

USD 4,457.05 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Packaging Type |

|

||

|

By Distribution Channel |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||