Osteopenia Treatment Market Synopsis

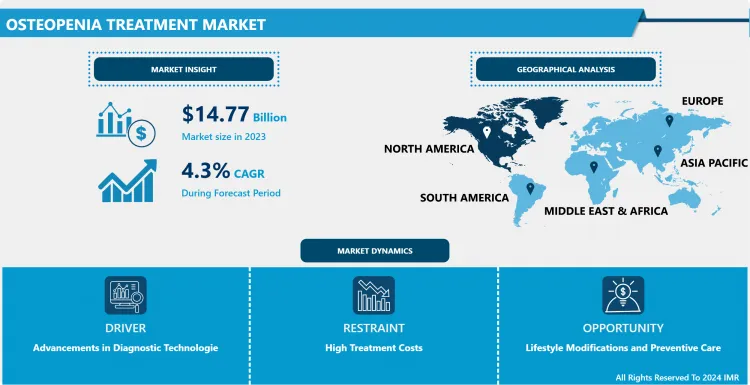

Osteopenia Treatment Market Size Was Valued at USD 14.77 Billion in 2023, and is Projected to Reach USD 21.57 Billion by 2032, Growing at a CAGR of 4.30% From 2024-2032.

The osteopenia treatment market refers to a series of therapeutic approaches designed to address and contain osteopenia, a condition in which bone mass is compromised, and a patient is at a greater risk of bone fractures. Available management strategies include prescribing medicines containing bisphosphonates, estrogen and other hormones, and calcium and vitamin D; other strategies are lifestyle changes, diet, and exercise to strengthen bones and general health. In light of the aging populace across the world and greater understanding of bone health concerns, there remains a signed for growth in this market due in part to further development of the management and treatment plans.

The osteopenia treatment market is rapidly growing due to the rising incidence of osteopenia and osteoporosis especially in growing elderly population. Lower levels of bone mass denseness is referred to as osteopenia and most often is a precursor to osteoporosis and therefore calls for early detection. More and more people have become aware of their bone health and what can be done to prevent such occurrences, placing healthcare professionals on the right track to finding the best treatment approaches. This has created more demand with regards to medications, supplements and therapeutically approached including ways of enhancing bone mass and diminishing the occurrence of bone fractures.

Pharmacological interventions such as bisphosphonates, estrogen therapy, other agents and new agents approved recently including denosumab and romosozumab are however promising since they can reduce the rate of bone loss. Besides this, market expansion is also due to the increased preference for dietary supplements like calcium and vitamin D products. The specific development of diversified healthcare systems also entails the focus for treatment with the individual patient characteristics. Moreover, new technologies and research are preparing the market for new methods helping to treat diseases and deliver the medicine, expanding the market even more.

Regionally, North America has a relatively high penetration for osteopenia treatment due to a strong established base healthcare and a more aware patient population. But there is growth and potential in regions including Europe and Asia-Pacific due to growing investment in health care and an ageing population base. The market is believed to go on developing under the priority of patient awareness and preventive approaches to osteopenia and the related conditions with the improvements of patients’ quality of life as the long-term goal of the market.

Osteopenia Treatment Market Trend Analysis

Emerging Dynamics in the Osteopenia Treatment Market

- Osteopenia has become more noticeable due to the aging population of the global population. This condition defined by low bone mass means that the individual is at a premium risk for fractures and osteoporosis. Due to a rising elderly population, healthcare providers around the world are focusing on fnidestThis is why there have been early interventlon and management strategies for osteopenia. Providers are coming to terms with the fact that early intervention planning can help avoid later complications such as osteoporosis, which requires significantly more extreme therapy. The proactive approach in managing such conditions is putting pressure to innovative treatment needs starting from a simple life alteration to the administration of drugs.

- Community enunciation endeavors stand out as vital mapping tools in improving awareness of osteopenia and its handling. Interventions targeted at healthcare providers and consumers focus be aware messages concerning screening and assessment of bone health. These initiatives actually involve educating people about factors that put them at risk, changes that they can make to eliminate those risks, and what they can do to prevent or treat bone disorders. Since patient awareness increases, they will be inclined to talk to their healthcare providers on means of preventing diseases and probable cures thus bolstering the market’s growth. Apart from helping to improve diagnosis rates, this has also made a way to a culture of prevention and thus helps to improve the patients’ condition and so assists in the growth of the osteopenia treatment market.

Innovations and Strategies in Osteopenia Treatment

- It has been observed that the osteopenia market has recently gained novel therapies, to treat the osteopenia condition. Hormones and bisphosphonates have been the main form of treatment of bone density problems in one’s twilight years for many years. However, from this section, there is clear evidence that latest realizations in pharmacotherapy such as hormone replacement therapies and monoclonal antibodies are beginning to present as viable solutions. These new agents are generically better in the scaled up efficacy profile and also exhibit a better safety and tolerance profile hence making them appealing to the patient as well as the treating physician. New therapies that were previously unpublished are slowly being incorporated into interventions because as knowledge and research on bone health progresses there are more ways to manage the condition for patients.

- However, the shift toward combination therapies is relatively growing in the osteopenia market. Subsequent research on multidisciplinary patient care approaches represents the notion of the effectiveness of combined treatment versus single methods. Pharmacological treatments of osteoporosis when supplemented with lifestyle modifications such as dietary adjustments and exercise regimes, the quality of life and overall beneficial effects on bone density may be improved. This evolution to towards the medical model reaffirms the need to make treatment delivery relevant to the patient. Specifically, in the overall treatment of osteopenia, integration of novel treatment modalities and combination therapeutic approach will significantly contribute to the delivery of advanced patient care and consequently drive the market growth.

Osteopenia Treatment Market Segment Analysis:

Osteopenia Treatment Market Segmented based on By Type, By Route of Administration, By Distribution Channel.

By Type, Bisphosphonates segment is expected to dominate the market during the forecast period

- Oral bisphosphonates are now seen as the standard first line therapy for Osteoporosis because of documented capabilities to slow down the occurrence of net bone loss and decrease the probability of bone fractures. The mode of action of these drugs is to reduce the activity of osteoclasts that control bone resorption: thus, when bone is broken down, there is a chance for bone-forming osteoblasts to strengthen the bone composition. This joint action is of great help in bringing normalcy to the bone remodeling process that tends to tilt in favour of bone loss in osteoporosis patients. Among bisphosphonates, alendronate and risedronate are most commonly used due to their effectiveness in raising bone density and decreasing the rate of hip and spinal fractures, in postmenopausal women and in patients with high risk of fracture, in particular. Most of them are taken per orally and thus have long acting formulas which may be taken for a weekly or monthly interval.

- Nevertheless, some crucial information about bisphosphonates should be taken into account: The medications are belong to specific protocols, and there are possible side effects of these. Patients are normally advised to swallow these drugs on an empty stomach and should avoid lying down for a least half an hour after taking them. It is associated with long-term side effects, which occur in most patients who receive it for more than five years and include osteonecrosis of the jaw or atypical femoral fracture that requires regular monitoring. However, the protective effect of bisphosphonates against severe fracture and favourable effects on bone strength prove them to be a valuable role in osteoporosis treatment, even though they ought to be adequately administered. Due to their long term use and efficiency they remain a popular therapeutic approach in primary as well as secondary osteoporosis interventions.

By Distribution Channel, Hospitals Pharmacies segment held the largest share in 2023

- The hospital pharmacy helps patients that need particular medications, especially for injectable or intravenous therapy for the treatment of osteoporosis. They ensure that patients can access high cost or those complicated prescription as soon as they are prescribed by the doctor in cases where they have not been recommended to retail pharmacies where they can be bought. This is more so for the people who use medicine such as denosumab or zoledronic acid that have to be administered professionally and then followed up. Besides distributing medicines, the hospital pharmacies also offer key components of caring for patient’s medicine including evaluating the response of the medicine, determining the efficiency of the treatment and reviewing doses of the medicines in relation to the utility of the patient. This makes it easy for pharmacists to consult with other healthcare practitioners like doctors or nursed hence making treatment specific to the patient’s needs especially when the case of osteoporosis is severe and may require complex treatment.

- Just like with retail pharmacies, hospital pharmacies play a very important role as they also act as connector between the inpatient and out patient management of the patient. For newly diagnosed patients or clients or patients who will need continued injectable therapies, these pharmacies offer comprehensive orientation on how to use medications and the significance of compliance to the ordered regimens. Many of the patients who need a long-term treatment for osteoporosis that include treatment with injections such as teriparatide or infusion of bisphosphonates, go back to hospital setting for their regular appointments. The pharmacists assist in organizing these follow up appointments and to assess for possible adverse reactions while patients are always endorsed by these healthcare professionals throughout the treatment process. This downstream care coordination supported by hospital pharmacies assumes an important role in the patients’ proper management of osteoporosis with reduced risks of fractures and other related complications.

Osteopenia Treatment Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

- With several factors considered North America leads the global osteopenia treatment market notably due to the United States. The prevalence of osteopenia is much higher in this region because the population is considerably old and the rate of bone density loss and fractures is much higher among the agers. Osteopenia is most prevalent among the elderly and as the US population ages with people 65 and over projected to tremendously grow there will be an increase in the need for osteopenia diagnosis and treatment. Diagnostic improvements such as the DEXA scans have proved useful in early diagnosis, thus earlier treatment. Further, effective government amplified along with patient awareness and early diagnosed concern regarding bone health. It stimulates the development of this market, as people search for timely diagnosis and have an opportunity to get therapeutic intervention.

- Pharmaceutical innovation also seems to drive the increase of the market in North America in a big way. Such medications as the bisphosphonates, SERMs and hormone replacement therapies for example form a right array which satisfies the patients’ different needs. These treatments involve are common, have positive re-imbursements which aids patient compliance with the treatments. Also, the raised demand for dietary supplements, especially for calcium and vitamin D, augments the market even more. They are usually prescribed in preventive measures and are readily available over the counter, and so many people with or without the disorder take these supplements. There is also constant research and improvement of products and services in bone health hence constant development of new therapies makes the U.S market continue to strengthen its position in the treatment of osteopenia.

Active Key Players in the Osteopenia Treatment Market

- Allergan Plc (Ireland)

- Amgen, Inc. (U.S.)

- Actavis Plc. (Ireland)

- Eli Lilly and Company (U.S.)

- F. Hoffmann La Roche Ltd. (Switzerland)

- GlaxoSmithKline Pharmaceutical Ltd. (U.K.)

- Merck & Co AG (Switzerland)

- Novartis AG (Switzerland)

- Novo Nordisk A/S (Denmark)

- Pfizer, Inc. (U.S.)

- Teva Pharmaceuticals Industries Ltd. (Israel)

- Other Key Players

Key Industry Developments in the Osteopenia Treatment Market:

- In March 2024, Bone Health Technologies (BHT) secured a $5 million funding round aimed at advancing care for individuals with low bone density. This funding round attracted investments from Esplanade Ventures, Berkeley Catalyst Fund, and Terumo Medical, a prominent figure in medical technology globally. The funding infusion comes at a pivotal moment as BHT approaches the final stages of obtaining de novo FDA clearance for its Osteoboost vibration wearable

- In January 2024, Bone Health Technologies, a leader in bone health solutions, unveiled Osteoboost following FDA clearance. This innovative device represents the first non-pharmacological prescription treatment for postmenopausal women diagnosed with osteopenia. The wearable belt administers precise, calibrated vibrations to the lumbar spine and hips, aiming to mitigate the decrease in bone strength and density. The approval of Osteoboost introduces a groundbreaking therapeutic option for low bone density, representing a milestone in women's health advancements

|

Global Osteopenia Treatment Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2024: |

USD 14.77 Bn. |

|

Forecast Period 2024-32 CAGR: |

4.30% |

Market Size in 2032: |

USD 21.57 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Route of Administration |

|

||

|

By Distribution Channel |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Osteopenia Treatment Market by Type (2018-2032)

4.1 Osteopenia Treatment Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Bisphosphonates

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Calcitonin

4.5 Hormone Therapy

4.6 Parathyroid Hormone Related Therapy (PTHrP) Analog

4.7 Selective Estrogen Receptor Modulator

4.8 Others

Chapter 5: Osteopenia Treatment Market by Route of Administration (2018-2032)

5.1 Osteopenia Treatment Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Oral

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Injectables

5.5 Others

Chapter 6: Osteopenia Treatment Market by Distribution Channel (2018-2032)

6.1 Osteopenia Treatment Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Hospitals Pharmacies

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Retail Pharmacies

6.5 Others

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Osteopenia Treatment Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 ALLERGAN PLC (IRELAND)

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 AMGEN INC. (U.S.)

7.4 ACTAVIS PLC. (IRELAND)

7.5 ELI LILLY AND COMPANY (U.S.)

7.6 F. HOFFMANN LA ROCHE LTD. (SWITZERLAND)

7.7 GLAXOSMITHKLINE PHARMACEUTICAL LTD. (U.K.)

7.8 MERCK & CO AG (SWITZERLAND)

7.9 NOVARTIS AG (SWITZERLAND)

7.10 NOVO NORDISK A/S (DENMARK)

7.11 PFIZER INC. (U.S.)

7.12 TEVA PHARMACEUTICALS INDUSTRIES LTD. (ISRAEL)

7.13 OTHER KEY PLAYERS

Chapter 8: Global Osteopenia Treatment Market By Region

8.1 Overview

8.2. North America Osteopenia Treatment Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size by Type

8.2.4.1 Bisphosphonates

8.2.4.2 Calcitonin

8.2.4.3 Hormone Therapy

8.2.4.4 Parathyroid Hormone Related Therapy (PTHrP) Analog

8.2.4.5 Selective Estrogen Receptor Modulator

8.2.4.6 Others

8.2.5 Historic and Forecasted Market Size by Route of Administration

8.2.5.1 Oral

8.2.5.2 Injectables

8.2.5.3 Others

8.2.6 Historic and Forecasted Market Size by Distribution Channel

8.2.6.1 Hospitals Pharmacies

8.2.6.2 Retail Pharmacies

8.2.6.3 Others

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Osteopenia Treatment Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size by Type

8.3.4.1 Bisphosphonates

8.3.4.2 Calcitonin

8.3.4.3 Hormone Therapy

8.3.4.4 Parathyroid Hormone Related Therapy (PTHrP) Analog

8.3.4.5 Selective Estrogen Receptor Modulator

8.3.4.6 Others

8.3.5 Historic and Forecasted Market Size by Route of Administration

8.3.5.1 Oral

8.3.5.2 Injectables

8.3.5.3 Others

8.3.6 Historic and Forecasted Market Size by Distribution Channel

8.3.6.1 Hospitals Pharmacies

8.3.6.2 Retail Pharmacies

8.3.6.3 Others

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Osteopenia Treatment Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size by Type

8.4.4.1 Bisphosphonates

8.4.4.2 Calcitonin

8.4.4.3 Hormone Therapy

8.4.4.4 Parathyroid Hormone Related Therapy (PTHrP) Analog

8.4.4.5 Selective Estrogen Receptor Modulator

8.4.4.6 Others

8.4.5 Historic and Forecasted Market Size by Route of Administration

8.4.5.1 Oral

8.4.5.2 Injectables

8.4.5.3 Others

8.4.6 Historic and Forecasted Market Size by Distribution Channel

8.4.6.1 Hospitals Pharmacies

8.4.6.2 Retail Pharmacies

8.4.6.3 Others

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Osteopenia Treatment Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size by Type

8.5.4.1 Bisphosphonates

8.5.4.2 Calcitonin

8.5.4.3 Hormone Therapy

8.5.4.4 Parathyroid Hormone Related Therapy (PTHrP) Analog

8.5.4.5 Selective Estrogen Receptor Modulator

8.5.4.6 Others

8.5.5 Historic and Forecasted Market Size by Route of Administration

8.5.5.1 Oral

8.5.5.2 Injectables

8.5.5.3 Others

8.5.6 Historic and Forecasted Market Size by Distribution Channel

8.5.6.1 Hospitals Pharmacies

8.5.6.2 Retail Pharmacies

8.5.6.3 Others

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Osteopenia Treatment Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size by Type

8.6.4.1 Bisphosphonates

8.6.4.2 Calcitonin

8.6.4.3 Hormone Therapy

8.6.4.4 Parathyroid Hormone Related Therapy (PTHrP) Analog

8.6.4.5 Selective Estrogen Receptor Modulator

8.6.4.6 Others

8.6.5 Historic and Forecasted Market Size by Route of Administration

8.6.5.1 Oral

8.6.5.2 Injectables

8.6.5.3 Others

8.6.6 Historic and Forecasted Market Size by Distribution Channel

8.6.6.1 Hospitals Pharmacies

8.6.6.2 Retail Pharmacies

8.6.6.3 Others

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Osteopenia Treatment Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size by Type

8.7.4.1 Bisphosphonates

8.7.4.2 Calcitonin

8.7.4.3 Hormone Therapy

8.7.4.4 Parathyroid Hormone Related Therapy (PTHrP) Analog

8.7.4.5 Selective Estrogen Receptor Modulator

8.7.4.6 Others

8.7.5 Historic and Forecasted Market Size by Route of Administration

8.7.5.1 Oral

8.7.5.2 Injectables

8.7.5.3 Others

8.7.6 Historic and Forecasted Market Size by Distribution Channel

8.7.6.1 Hospitals Pharmacies

8.7.6.2 Retail Pharmacies

8.7.6.3 Others

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Global Osteopenia Treatment Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2024: |

USD 14.77 Bn. |

|

Forecast Period 2024-32 CAGR: |

4.30% |

Market Size in 2032: |

USD 21.57 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Route of Administration |

|

||

|

By Distribution Channel |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||