Key Market Highlights

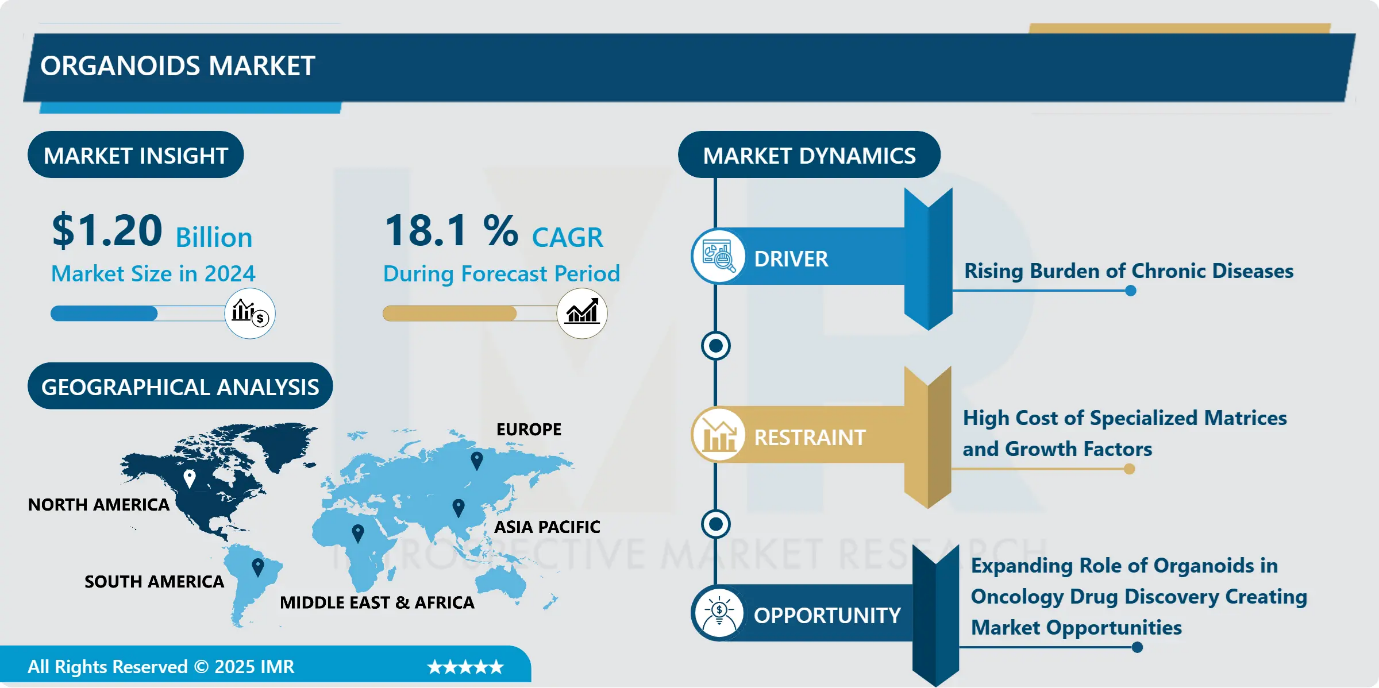

Organoids Market Size Was Valued at USD 1.20 Billion in 2024, and is Projected to Reach USD 7.48 Billion by 2035, Growing at a CAGR of 18.1% from 2025-2035.

- Market Size in 2024: USD 1.20 Billion

- Projected Market Size by 2035: USD 7.48 Billion

- CAGR (2025–2035): 18.1%

- Leading Market in 2024: North America

- Fastest-Growing Market: Asia Pacific

- By Application: The Drug Discovery & Screening segment is anticipated to lead the market by accounting for 31.9% of the market share throughout the forecast period.

- By End User: The Pharmaceutical & Biotechnology Companies segment is expected to capture 38.9% of the market share, thereby maintaining its dominance over the forecast period.

- By Region: North America region is projected to hold 30.2% of the market share during the forecast period.

- Active Players: Alveolix AG (Switzerland), Bio-Techne (United States), Charles River Laboratories (United States), Corning Incorporated (United States), Emulate Inc. (United States), and Other Active Players.

Organoids Market Synopsis:

The organoids market represents the commercial ecosystem focused on the development and application of three-dimensional (3D) stem cell-derived tissue cultures that replicate the structural and functional characteristics of human organs. These self-organizing cellular models provide advanced platforms for studying organ development, disease mechanisms, and therapeutic responses. Increasing demand for physiologically relevant in vitro models over traditional 2D cultures and animal testing is driving adoption across pharmaceutical, biotechnology, and academic research sectors. Organoids support drug discovery, toxicology testing, regenerative medicine, and precision medicine initiatives. Continuous advancements in stem cell biology, genome editing, and 3D bioprinting technologies are further strengthening market growth and expanding research and commercial opportunities globally.

Organoids Market Dynamics and Trend Analysis:

Organoids Market Growth Driver

Rising Burden of Chronic Diseases

- The increasing global incidence of chronic diseases such as cancer, diabetes, and neurodegenerative disorders is a major driver of the organoids market. Growing patient populations and long-term treatment requirements are placing significant pressure on healthcare systems worldwide. This has intensified the need for advanced and reliable preclinical models that can accurately replicate human disease conditions. Organoids provide physiologically relevant platforms for disease modeling, drug screening, and therapeutic validation, offering improved predictive outcomes compared to conventional models. As healthcare expenditures continue to rise globally, the demand for innovative research tools is accelerating, positioning organoids as critical enablers in next-generation therapeutic development.

Organoids Market Limiting Factor

High Cost of Specialized Matrices and Growth Factors

- The high cost of specialized matrices and growth factors represents a significant restraint on the organoids market. Commonly used extracellular matrices and recombinant proteins required for organoid culture are expensive and consumed in substantial volumes during large-scale screening studies. Frequent replenishment due to limited protein stability further increases operational costs. As a result, research budgets can escalate rapidly, limiting widespread adoption, particularly in small laboratories and emerging economies. Although suppliers are introducing synthetic, animal-free alternatives and bulk-pricing models, cost reductions remain gradual. These financial barriers restrict scalability and slow broader market penetration, especially in resource-constrained research environments.

Organoids Market Expansion Opportunity

Expanding Role of Organoids in Oncology Drug Discovery Creating Market Opportunities

- The growing integration of organoids in oncology drug discovery presents a significant market opportunity. Tumor-derived organoids have demonstrated strong predictive accuracy for chemotherapy response, outperforming conventional 2D cell lines and accelerating pharmaceutical adoption. Leading biopharmaceutical companies are increasingly building extensive patient-derived organoid biobanks to support lead optimization and precision oncology programs. Additionally, large-scale funding initiatives supporting tumor mapping and spatial transcriptomics are enhancing the value of organoid-based assays in designing targeted combination therapies. Reported reductions in preclinical development timelines and lower late-stage failure rates improve R&D productivity, strengthening the commercial and economic case for broader implementation of organoid platforms in oncology workflows.

Organoids Market Challenge and Risk

Lack of Standardized Reproducibility Protocols

- The absence of standardized reproducibility protocols poses a major challenge to the organoids market. Variability in morphology, gene expression, and functional outcomes across laboratories using similar methodologies undermines data consistency and confidence. Without harmonized quality control metrics and validated reference standards, regulatory submissions and cross-study comparisons become complex and time-consuming. Ongoing discussions among regulatory bodies and scientific organizations aim to address these gaps, but formal guidance frameworks are still evolving. Smaller laboratories often lack the resources to implement emerging best practices, further widening performance discrepancies. This lack of standardization constrains scalability, delays commercialization, and limits broader clinical integration.

Organoids Market Trend

Growing Integration of Organoids in Precision Medicine and Personalized Therapy Trials

- The expanding adoption of organoids in precision medicine trials represents a key market trend. Functional testing using patient-derived organoids is increasingly supporting treatment selection, demonstrating improved objective response rates in complex oncology cases. Regulatory advancements, including approvals of companion diagnostics based on patient-derived culture platforms, highlight growing institutional acceptance. Clinical trial designs such as basket studies are incorporating organoid assays to match patients with targeted therapies more efficiently, reducing screening time and recruitment costs. Moreover, as payers demand stronger clinical evidence, organoid-generated functional response data is strengthening reimbursement discussions, accelerating their integration into personalized therapeutic development frameworks.

Organoids Market Segment Analysis:

Organoids Market is segmented based on Source, Organ Type, Application, Technology, End User, and Region.

By Application, Drug discovery and screening segment is expected to dominate the market with around 31.9% share during the forecast period.

- Drug discovery and screening accounted for the largest revenue share in 2024, driven by strong pharmaceutical dependence on organoid platforms to streamline target validation and preclinical testing. Their dominance is attributed to the urgent need to reduce development timelines, improve predictive accuracy, and minimize late-stage clinical failures. While disease modeling and toxicology remain important segments, precision medicine is emerging as the fastest-growing application area. Increasing reimbursement support for organoid-guided therapy selection and regulatory acceptance of companion diagnostics are accelerating adoption. As healthcare systems prioritize outcome-based treatment strategies, organoids are becoming integral to personalized therapeutic decision-making and translational oncology research.

By End User, Pharmaceutical and biotechnology companies is expected to dominate with close to 38.9% market share during the forecast period.

- Pharmaceutical and biotechnology companies accounted for the largest share of organoids market spending in 2024, driven by their strong R&D capabilities, established infrastructure, and strategic focus on accelerating drug development. Their dominance is supported by extensive use of organoids for target validation, toxicity assessment, and precision medicine programs aimed at reducing late-stage clinical failures and improving return on investment.

- At the same time, CROs and CDMOs are witnessing the fastest growth due to rising outsourcing trends. Sponsors increasingly prefer external partners to access specialized organoid platforms without heavy capital investment. Outsourcing provides scalability, technical expertise, and operational flexibility, particularly as assay complexity and regulatory expectations continue to increase across global markets.

Organoids Market Regional Insights:

North America region is estimated to lead the market with around 30.2% share during the forecast period.

- North America holds a dominant position in the Organoids Market, accounting for over 30.2% of global revenue, driven by strong biotechnology capabilities, advanced research infrastructure, and substantial public and private funding. Support from agencies such as the National Institutes of Health and a favorable regulatory approach by the U.S. Food and Drug Administration accelerate innovation and commercialization. The region benefits from high venture capital activity in leading biotech hubs like Boston and the San Francisco Bay Area. Additionally, growing demand for personalized medicine, active collaborations between academia and industry, and expanding organoid-based drug discovery services collectively reinforce North America’s market dominance.

Organoids Market Active Players:

- Alveolix AG (Switzerland)

- Bio-Techne (United States)

- Charles River Laboratories (United States)

- Corning Incorporated (United States)

- Emulate Inc. (United States)

- Greiner Bio-One (Austria)

- Hubrecht Organoid Technology (HUB) (Netherlands)

- InSphero (Switzerland)

- Lonza (Switzerland)

- Merck KGaA (Germany)

- Molecular Devices, LLC (United States)

- Promega Corporation (United States)

- STEMCELL Technologies Inc. (Canada)

- Thermo Fisher Scientific, Inc. (United States)

- UPM Biomedicals (Finland)

- Other Active Players

Key Industry Developments in the Organoids Market:

- In February 2026: Bio-Techne Corporation introduced Cultrex Synthetic Hydrogel, a fully defined synthetic extracellular matrix (ECM). The product supports consistent and scalable 3D stem cell and organoid culture.This launch strengthens reproducibility and efficiency in advanced organoid-based research applications.

- In June 2024: Molecular Devices, LLC inaugurated a new advanced facility in Cardiff, UK, backed by a multimillion-pound investment. The site features cutting-edge bioprocessing workflows and next-generation bioreactor technologies.It is designed to enable large-scale production of patient-derived organoids (PDOs) under strict quality standards.

Technical Advancements and Platform Innovations in the Organoids Market

- The organoids market is technically driven by advancements in stem cell biology, biomaterials engineering, and three-dimensional (3D) cell culture systems. Organoids are generated from pluripotent stem cells (PSCs) or adult stem cells under defined culture conditions that promote self-organization, lineage specification, and spatial architecture resembling native tissues. Key technical components include extracellular matrices (such as natural or synthetic hydrogels), growth factor-enriched media, bioreactors, and microfluidic platforms that support nutrient diffusion and long-term viability. Integration with genome editing tools like CRISPR enables disease modeling through targeted genetic modifications.

- High-content imaging, automated screening systems, and single-cell sequencing further enhance analytical capabilities. Additionally, 3D bioprinting technologies facilitate spatial control and reproducibility in organoid fabrication. Standardization, scalability, and batch-to-batch consistency remain critical technical challenges. Continuous innovation in synthetic matrices, automation, and organ-on-chip integration is improving translational relevance, enabling broader adoption across drug discovery, toxicology testing, and precision medicine applications.

|

Organoids Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2024 |

Market Size in 2024: |

USD 1.20 Bn. |

|

Forecast Period 2025-32 CAGR: |

18.1 % |

Market Size in 2035: |

USD 7.48 Bn. |

|

Segments Covered: |

By Source |

|

|

|

By Organ Type |

|

||

|

By Application |

|

||

|

By Technology |

|

||

|

By End User

|

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Organoids Market by Source (2018-2035)

4.1 Organoids Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Pluripotent Stem-Cell-Derived

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Organ-Specific Adult Stem Cells

4.5 and Others

Chapter 5: Organoids Market by Organ Type (2018-2035)

5.1 Organoids Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Intestinal

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Liver

5.5 Brain

5.6 Kidney

5.7 Pancreas

5.8 Heart

5.9 and Others

Chapter 6: Organoids Market by Application (2018-2035)

6.1 Organoids Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Drug Discovery & Screening

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Developmental Biology Disease Modeling

6.5 Drug Testing

6.6 Personalized Medicine

6.7 and Others

Chapter 7: Organoids Market by Offering (2018-2035)

7.1 Organoids Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Consumables and Instruments

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

Chapter 8: Organoids Market by Technology (2018-2035)

8.1 Organoids Market Snapshot and Growth Engine

8.2 Market Overview

8.3 3-D Bioprinting-Assisted and Others

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

8.3.3 Key Market Trends, Growth Factors, and Opportunities

8.3.4 Geographic Segmentation Analysis

Chapter 9: Organoids Market by End User (2018-2035)

9.1 Organoids Market Snapshot and Growth Engine

9.2 Market Overview

9.3 Academic & Research Institutes

9.3.1 Introduction and Market Overview

9.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

9.3.3 Key Market Trends, Growth Factors, and Opportunities

9.3.4 Geographic Segmentation Analysis

9.4 Contract Research Organizations (CROs)

9.5 Pharmaceutical & Biotechnology Companies

9.6 and Others

Chapter 10: Company Profiles and Competitive Analysis

10.1 Competitive Landscape

10.1.1 Competitive Benchmarking

10.1.2 Organoids Market Share by Manufacturer/Service Provider(2024)

10.1.3 Industry BCG Matrix

10.1.4 PArtnerships, Mergers & Acquisitions

10.2 ALVEOLIX AG (SWITZERLAND)

10.2.1 Company Overview

10.2.2 Key Executives

10.2.3 Company Snapshot

10.2.4 Role of the Company in the Market

10.2.5 Sustainability and Social Responsibility

10.2.6 Operating Business Segments

10.2.7 Product Portfolio

10.2.8 Business Performance

10.2.9 Recent News & Developments

10.2.10 SWOT Analysis

10.3 BIO-TECHNE (UNITED STATES)

10.4 CHARLES RIVER LABORATORIES (UNITED STATES)

10.5 CORNING INCORPORATED (UNITED STATES)

10.6 EMULATE INC. (UNITED STATES)

10.7 GREINER BIO-ONE (AUSTRIA)

10.8 HUBRECHT ORGANOID TECHNOLOGY (HUB) (NETHERLANDS)

10.9 INSPHERO (SWITZERLAND)

10.10 LONZA (SWITZERLAND)

10.11 MERCK KGAA (GERMANY)

10.12 MOLECULAR DEVICES

10.13 LLC (UNITED STATES)

10.14 PROMEGA CORPORATION (UNITED STATES)

10.15 STEMCELL TECHNOLOGIES INC. (CANADA)

10.16 THERMO FISHER SCIENTIFIC

10.17 INC. (UNITED STATES)

10.18 UPM BIOMEDICALS (FINLAND).

10.19 AND OTHER ACTIVE PLAYERS.

Chapter 11: Global Organoids Market By Region

11.1 Overview

11.2. North America Organoids Market

11.2.1 Key Market Trends, Growth Factors and Opportunities

11.2.2 Top Key Companies

11.2.3 Historic and Forecasted Market Size by Segments

11.2.4 Historic and Forecast Market Size by Country

11.2.4.1 US

11.2.4.2 Canada

11.2.4.3 Mexico

11.3. Eastern Europe Organoids Market

11.3.1 Key Market Trends, Growth Factors and Opportunities

11.3.2 Top Key Companies

11.3.3 Historic and Forecasted Market Size by Segments

11.3.4 Historic and Forecast Market Size by Country

11.3.4.1 Russia

11.3.4.2 Bulgaria

11.3.4.3 The Czech Republic

11.3.4.4 Hungary

11.3.4.5 Poland

11.3.4.6 Romania

11.3.4.7 Rest of Eastern Europe

11.4. Western Europe Organoids Market

11.4.1 Key Market Trends, Growth Factors and Opportunities

11.4.2 Top Key Companies

11.4.3 Historic and Forecasted Market Size by Segments

11.4.4 Historic and Forecast Market Size by Country

11.4.4.1 Germany

11.4.4.2 UK

11.4.4.3 France

11.4.4.4 The Netherlands

11.4.4.5 Italy

11.4.4.6 Spain

11.4.4.7 Rest of Western Europe

11.5. Asia Pacific Organoids Market

11.5.1 Key Market Trends, Growth Factors and Opportunities

11.5.2 Top Key Companies

11.5.3 Historic and Forecasted Market Size by Segments

11.5.4 Historic and Forecast Market Size by Country

11.5.4.1 China

11.5.4.2 India

11.5.4.3 Japan

11.5.4.4 South Korea

11.5.4.5 Malaysia

11.5.4.6 Thailand

11.5.4.7 Vietnam

11.5.4.8 The Philippines

11.5.4.9 Australia

11.5.4.10 New Zealand

11.5.4.11 Rest of APAC

11.6. Middle East & Africa Organoids Market

11.6.1 Key Market Trends, Growth Factors and Opportunities

11.6.2 Top Key Companies

11.6.3 Historic and Forecasted Market Size by Segments

11.6.4 Historic and Forecast Market Size by Country

11.6.4.1 Turkiye

11.6.4.2 Bahrain

11.6.4.3 Kuwait

11.6.4.4 Saudi Arabia

11.6.4.5 Qatar

11.6.4.6 UAE

11.6.4.7 Israel

11.6.4.8 South Africa

11.7. South America Organoids Market

11.7.1 Key Market Trends, Growth Factors and Opportunities

11.7.2 Top Key Companies

11.7.3 Historic and Forecasted Market Size by Segments

11.7.4 Historic and Forecast Market Size by Country

11.7.4.1 Brazil

11.7.4.2 Argentina

11.7.4.3 Rest of SA

Chapter 12 Analyst Viewpoint and Conclusion

Chapter 13 Our Thematic Research Methodology

12.1 Research Process

12.2 Primary Research

12.3 Secondary Research

Chapter 14 Case Study

Chapter 15 Appendix

13.1 Sources

13.2 List of Tables and figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Organoids Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2024 |

Market Size in 2024: |

USD 1.20 Bn. |

|

Forecast Period 2025-32 CAGR: |

18.1 % |

Market Size in 2035: |

USD 7.48 Bn. |

|

Segments Covered: |

By Source |

|

|

|

By Organ Type |

|

||

|

By Application |

|

||

|

By Technology |

|

||

|

By End User

|

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||