Global Oncology Drugs Market Synopsis

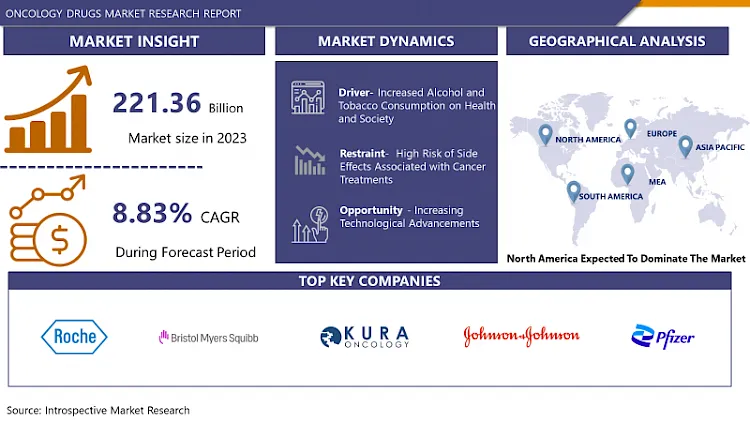

Global Oncology Drugs Market Size Was Valued at USD 221.36 Billion in 2023 and is Projected to Reach USD 474.06 Billion by 2032, Growing at a CAGR of 8.83% From 2024-2032.

Oncology is the branch of medicine that includes cancer prevention, diagnosis, treatment, and study. Cancer describes the irregular growth of cells that results in a huge mass known as a tumour.

Oncology drugs are therapeutics used to treat cancer, a group of diseases caused by uncontrolled growth and division of abnormal cells. Oncology drugs contain a range of different types of medicines, for instance, chemotherapy agents, targeted therapies, immunotherapies, and hormone therapies. Different types of drugs are also existing to support treat the side effects of oncology drugs.

An oncologist is a healthcare provider who specializes in diagnosing and treating cancer. Oncologists manage cancer treatment throughout the illness. Healthcare workers treat cancer using chemotherapy, hormonal therapies, immunotherapy, and other targeted treatments. People often think of the medical oncologist as their primary cancer specialist. Most medical oncologists also specify hematology.

Paediatric oncology is a vital medical field that treats pediatric cancer types, including serious lymphocytic leukemia, neuroblastoma, and brain and other central nervous system tumors. Treatment often changes from adult oncology. Pediatric oncology treatment may contain surgery, chemotherapy, radiation therapy, immunotherapy, and stem cell transplant.

Oncologists specialize in managing drug treatments for people with primary and advanced cancers that affect the tissues, muscles, bones, and connective tissue. Early-stage cancers may be treated with surgery or radiation therapy alone and may not essential the care of an oncologist.

Global Oncology Drugs Market Trend Analysis

Increased Alcohol and Tobacco Consumption on Health and Society

- Alcohol and tobacco use are related to several adverse health significances, including an increased risk of certain types of cancer. For instance, epidemiological studies initiate that alcohol drinking can increase the risk for cancers of the higher aerodigestive tract, stomach, large bowel, liver, and breast, with advanced levels of consumption leading to greater growth in risk.

- Cigarettes contain amounts of chemicals, with many known carcinogens. The carcinogenic role of cigarettes contrasts depending on the cigarette product. The chemical products of alcohol absorption are also explored to be toxic and assumed to cause DNA modifications that main to cancers.

- Alcohol increases the carcinogenic significance of tobacco. For example, it might increase the synthesis of specific enzymes that chance the chemical tobacco tar is created by burning tobacco into carcinogens.

- Every alcoholic drink covers ethanol. When consuming alcohol, the body breaks down the ethanol into acetaldehyde and other chemicals. Acetaldehyde damages DNA and stops bodies from restoring the damage. That damage over time may be responsible for cancer.

- Smoking causes cancer by damaging the DNA of private cells. When individuals inhale tobacco smoke into their lungs the smoke also touches the nose, mouth, voice box, throat, and gullet. The hazardous chemicals in tobacco smoke can also injury organs that are not in the route because they are absorbed into the circulation in the lungs.

Increasing Technological Advancements

- An increase in the rate of cancer rate worldwide combined with improved mortality in some of the malignancies endures poses a challenge to the biomedical scientific community for the actual administration of cancer. Prevention being a realistic prospect only in a few types of cancers, technological advancements in cancer diagnostics with accurate determination of location, size, stage, and molecular features, are immediately needed for cancer treatment, due to a worldwide increase in cancer-related mortality.

- The method for diagnosis as a part of the clinical management of cancer contains a physical inspection for irregularities in various anatomical locations and a battery of laboratory inquiries using blood and urine combined with a combination of radiologic and nuclear medicine-based non-invasive imaging modalities like electronic X-ray scan ultrasonography, magnetic resonance imaging (MRI), bone scan, positron emission tomography followed by minimally invasive biopsy or invasive (surgical) biopsy joined with histo-pathological inspection to found the identity and stage of the cancer.

- Cancer diagnosis is quickly evolving due to constant developments in knowledge of the disease and enhancements in technology that growth the feasibility of consistent diagnostic approaches. There are numerous cancer diagnostic modalities such as 2D and 3D imaging of tumors using positron emission tomography (PET), MRI, single photon emission computed tomography (SPECT), computed tomography (CT), X-ray imaging, and analysis of molecular (metabolic, proteomic, genomic, and transcriptomic) signatures of cancer cells, thus leveraging the cancer diagnosis and management.

Global Oncology Drugs Market Segment Analysis:

Global Oncology Drugs Market is Segmented on the basis of Diagnostics & Treatment, Treatment, Drugs Class, Dosage Form, Indication, Distribution Channel, And End-user.

By Diagnostics & Treatment, the Treatment segment is expected to dominate the market during the forecast period

- Cancer treatment for patients for many years which includes surgery, radiation therapy, and chemotherapy as only treatments in combination. But newly, many ways involved in cancer therapy progression and targeted enhanced intensely, with combinatorial strategies, connecting multiple targeted therapies or “traditional” chemotherapeutics, such as the taxanes and platinum compounds, originating to have a synergistic effect. such as drugs, biological molecules, and immune-mediated therapies, are being used for treatment even if the included therapy level has not stretched struggles the humanity rate and declines the prolonged survival time for metastatic cancer.

- The creation of a new uprising in neoplastic cancer or targeting drugs depends on the pathways and characteristics of diverse tumor objects. Chemotherapy is measured as the most effective and broadly used modality in treating cancers as used without help and in combination with radiotherapy. Genotoxicity is chemotherapy drugs target the tumor cells mostly making reactive oxygen species that largely abolish tumor cells.

- Chemotherapy drugs to destroy cancer cells. This specific cancer therapy, cancer cells are prohibited from increasing, dividing, and generating new cells. Numerous cancers can be treated by chemotherapy. Doctors may state chemotherapy as normal chemotherapy, conventional chemotherapy, or cytotoxic chemotherapy. The medication chemotherapy has an overall body-wide impact. This indicates that it circulates through the body via the circulation. Chemotherapy comes in a variety of forms.

By Application, the Lung Cancer segment held the largest share in 2023

- Lung cancer is one of the most common cancers and a huge number of people die of this disease each year. The disease is often exposed in a late stage, but also in previous stages lung cancer patients have inferior outcomes than patients with other cancers. Even without dispersion to other tissues, during stage I, the existence rate of lung cancer is under 70%. For instance, in breast cancer, there is 95% existence in the stage.

- Lung cancer is the unrestrained growing of irregular cells that starts in one or both lungs. These irregular cells do not transmit out the roles of normal lung cells and do not change into healthy lung tissue. The abnormal cells start to form tumors that inhibit the working of the lung.

- A diagnosis of lung cancer is serious, but treatments have enhanced extremely in recent years. People with lung cancer do improve if diagnosed with early-stage disease, so identifying lung cancer symptoms is significant. Lung cancer can frequently be present without indications, lung cancer screening is also an important tool to detect lung cancer initially in people who are at high risk.

Global Oncology Drugs Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

- North America has a developed healthcare system, which includes hospitals, specialized cancer centers, research institutions, and medical universities. The strong healthcare system in the area allows for effective identification, care, and control of a range of illnesses, such as cancer.

- North America spends a significant amount on healthcare, showing a strong focus on healthcare services and advancements. This investment in finances supports the growth and acceptance of new technologies, state-of-the-art therapies, and advanced treatment choices.

- The region is recognized for its significant contributions in oncology research, clinical trials, and drug development which give North America an upper hand in the market.

- The region has been an early adopter of technological advancements in the healthcare sector due to this North America has witnessed remarkable progress in precision medicine, genomic profiling, molecular diagnostics, imaging technologies, and targeted therapies.

Active Key Players in the Global Oncology Drugs Market

- Roche Holding AG (Switzerland)

- Bristol Myers Squibb (U.S.)

- Kura Oncology, Inc. (U.S.)

- Johnson & Johnson (U.S.)

- Pfizer Inc. (U.S.)

- AstraZeneca (U.K.)

- Merck & Co., Inc. (U.S.)

- Novartis AG (Switzerland)

- AbbVie Inc. (U.S.)

- Abbott Laboratorie (U.S.)

- Amgen Inc. (U.S.)

- Sanofi SA - France

- Bristol-Myers Squibb Company (U.S.)

- Gilead Sciences Inc (U.S.)

- Vertex Pharmaceuticals Inc. (U.S.)

- Regeneron Pharmaceuticals Inc. (U.S.)

- GSK plc. (U.K.)

- Daiichi Sankyo Company Ltd. Japan

- Takeda Pharmaceutical Company Ltd. (Japan)

- Moderna Inc (U.S.)

- Biogen Inc. (U.S.)

- BioNTech SE (Germany)

- Astellas Pharma Inc. (Japan)

- Illumina Inc. ((U.S.))

- Beigene Ltd. (China)

- Otsuka Pharmaceutical Ltd. (Japan)

- Incyte Corporation ((U.S.))

- Teva Pharmaceutical Industries Ltd. (Israel)

- Dr. Reddy’s Laboratories Limited (India)

- Jazz Pharmaceuticals plc (Ireland)

- Oncology Convergence, Inc ((U.S.))

- Oncology Systems Limited (U.K.)

- GenesisCare USA, Inc. ((U.S.))

- Integrated Oncology Centres (Hong Kong)

- Tennessee Oncology ((U.S.))

- Maryland Oncology Hematology ((U.S.))

- Minnesota Oncology ((U.S.))

- Arizona Oncology ((U.S.))

- Highlands Oncology ((U.S.))

- GenPath Oncology ((U.S.))

- HCG Manavata Oncology LLP (India)

- New York Oncology Hematology ((U.S.))

- McGill Oncology (Canada)

- NeoGenomics Laboratories, Inc. ((U.S.))

- Valley Health System ((U.S.))

- Jupiter Medical Center ((U.S.))

- GBMC HealthCare ((U.S.))

- Duly Health and Care ((U.S.))

- Alliance Healthcare Services, Inc. ((U.S.)) and other Active Players.

Key Industry Developments in the Global Oncology Drugs Market:

- In March 2024, Roche Pharma India launched Vabysmo, a medication for neovascular age-related macular degeneration and diabetic macular edema in India. The drug is cost-effective and collaborates with government and insurance companies for patient access. Vabysmo achieves global sales and offers durable treatment for retinal vision loss.

- In January 2024, BDR Pharmaceuticals has, in a global first, introduced the prostate cancer drug enzalutam

|

Global Oncology Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 221.36 Bn. |

|

Forecast Period 2024-32 CAGR: |

8.83 % |

Market Size in 2032: |

USD 474.06 Bn. |

|

Segments Covered: |

By Diagnostics & Treatment |

|

|

|

By Drugs Class |

|

||

|

By Dosage Form |

|

||

|

By Indication |

|

||

|

By Distribution Channel |

|

||

|

By End-user |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Oncology Drugs Market by Diagnostics & Treatment (2018-2032)

4.1 Oncology Drugs Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Diagnostics

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Biopsy

4.5 Imaging

4.6 Immunohistochemistry

4.7 Tumour Biomarkers Test

4.8 In Situ Hybridization

4.9 Liquid Biopsy

4.10 Treatment

4.11 Targeted Therapy

4.12 Chemotherapy

4.13 Hormonal Therapy

4.14 Immunotherapy

Chapter 5: Oncology Drugs Market by Drugs Class (2018-2032)

5.1 Oncology Drugs Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Cytotoxic Drugs

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Targeted Drugs

5.5 Hormonal Drugs

5.6 Immunomodulatory Drugs

Chapter 6: Oncology Drugs Market by Dosage Form (2018-2032)

6.1 Oncology Drugs Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Solid

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Liquid

6.5 Injectable

Chapter 7: Oncology Drugs Market by Indication (2018-2032)

7.1 Oncology Drugs Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Lungs Cancer

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Colorectal Cancer

7.5 Breast Cancer

7.6 Liver Cancer

7.7 Bladder Cancer

7.8 Others (Head & Neck Cancer

7.9 Prostate Cancer

7.10 Thyroid Cancer)

Chapter 8: Oncology Drugs Market by Distribution Channel (2018-2032)

8.1 Oncology Drugs Market Snapshot and Growth Engine

8.2 Market Overview

8.3 Hospital Pharmacies

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

8.3.3 Key Market Trends, Growth Factors, and Opportunities

8.3.4 Geographic Segmentation Analysis

8.4 Retail Pharmacies

8.5 Online Pharmacies

Chapter 9: Oncology Drugs Market by End-user (2018-2032)

9.1 Oncology Drugs Market Snapshot and Growth Engine

9.2 Market Overview

9.3 Hospitals

9.3.1 Introduction and Market Overview

9.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

9.3.3 Key Market Trends, Growth Factors, and Opportunities

9.3.4 Geographic Segmentation Analysis

9.4 Diagnostic Laboratories

9.5 Diagnostic Imaging Centres

9.6 Academia

9.7 Specialty Clinics

Chapter 10: Company Profiles and Competitive Analysis

10.1 Competitive Landscape

10.1.1 Competitive Benchmarking

10.1.2 Oncology Drugs Market Share by Manufacturer (2024)

10.1.3 Industry BCG Matrix

10.1.4 Heat Map Analysis

10.1.5 Mergers and Acquisitions

10.2 ACTIVISION BLIZZARD INCALIPAY

10.2.1 Company Overview

10.2.2 Key Executives

10.2.3 Company Snapshot

10.2.4 Role of the Company in the Market

10.2.5 Sustainability and Social Responsibility

10.2.6 Operating Business Segments

10.2.7 Product Portfolio

10.2.8 Business Performance

10.2.9 Key Strategic Moves and Recent Developments

10.2.10 SWOT Analysis

10.3 BOKU

10.4 ENTERCASH

10.5 SECURIONPAY

10.6 WORLDPAY

10.7 XSOLLA

10.8 NCSOFT

10.9 RIOT GAMES INCNEXON CO. LTDSMILEGATE (CROSSFIRE)

10.10 WARGAMING.NET

10.11 NETEASE INCVALVE CORPORATION

10.12 EPAY

10.13 FAMEHYPE AND OTHERS

Chapter 11: Global Oncology Drugs Market By Region

11.1 Overview

11.2. North America Oncology Drugs Market

11.2.1 Key Market Trends, Growth Factors and Opportunities

11.2.2 Top Key Companies

11.2.3 Historic and Forecasted Market Size by Segments

11.2.4 Historic and Forecasted Market Size by Diagnostics & Treatment

11.2.4.1 Diagnostics

11.2.4.2 Biopsy

11.2.4.3 Imaging

11.2.4.4 Immunohistochemistry

11.2.4.5 Tumour Biomarkers Test

11.2.4.6 In Situ Hybridization

11.2.4.7 Liquid Biopsy

11.2.4.8 Treatment

11.2.4.9 Targeted Therapy

11.2.4.10 Chemotherapy

11.2.4.11 Hormonal Therapy

11.2.4.12 Immunotherapy

11.2.5 Historic and Forecasted Market Size by Drugs Class

11.2.5.1 Cytotoxic Drugs

11.2.5.2 Targeted Drugs

11.2.5.3 Hormonal Drugs

11.2.5.4 Immunomodulatory Drugs

11.2.6 Historic and Forecasted Market Size by Dosage Form

11.2.6.1 Solid

11.2.6.2 Liquid

11.2.6.3 Injectable

11.2.7 Historic and Forecasted Market Size by Indication

11.2.7.1 Lungs Cancer

11.2.7.2 Colorectal Cancer

11.2.7.3 Breast Cancer

11.2.7.4 Liver Cancer

11.2.7.5 Bladder Cancer

11.2.7.6 Others (Head & Neck Cancer

11.2.7.7 Prostate Cancer

11.2.7.8 Thyroid Cancer)

11.2.8 Historic and Forecasted Market Size by Distribution Channel

11.2.8.1 Hospital Pharmacies

11.2.8.2 Retail Pharmacies

11.2.8.3 Online Pharmacies

11.2.9 Historic and Forecasted Market Size by End-user

11.2.9.1 Hospitals

11.2.9.2 Diagnostic Laboratories

11.2.9.3 Diagnostic Imaging Centres

11.2.9.4 Academia

11.2.9.5 Specialty Clinics

11.2.10 Historic and Forecast Market Size by Country

11.2.10.1 US

11.2.10.2 Canada

11.2.10.3 Mexico

11.3. Eastern Europe Oncology Drugs Market

11.3.1 Key Market Trends, Growth Factors and Opportunities

11.3.2 Top Key Companies

11.3.3 Historic and Forecasted Market Size by Segments

11.3.4 Historic and Forecasted Market Size by Diagnostics & Treatment

11.3.4.1 Diagnostics

11.3.4.2 Biopsy

11.3.4.3 Imaging

11.3.4.4 Immunohistochemistry

11.3.4.5 Tumour Biomarkers Test

11.3.4.6 In Situ Hybridization

11.3.4.7 Liquid Biopsy

11.3.4.8 Treatment

11.3.4.9 Targeted Therapy

11.3.4.10 Chemotherapy

11.3.4.11 Hormonal Therapy

11.3.4.12 Immunotherapy

11.3.5 Historic and Forecasted Market Size by Drugs Class

11.3.5.1 Cytotoxic Drugs

11.3.5.2 Targeted Drugs

11.3.5.3 Hormonal Drugs

11.3.5.4 Immunomodulatory Drugs

11.3.6 Historic and Forecasted Market Size by Dosage Form

11.3.6.1 Solid

11.3.6.2 Liquid

11.3.6.3 Injectable

11.3.7 Historic and Forecasted Market Size by Indication

11.3.7.1 Lungs Cancer

11.3.7.2 Colorectal Cancer

11.3.7.3 Breast Cancer

11.3.7.4 Liver Cancer

11.3.7.5 Bladder Cancer

11.3.7.6 Others (Head & Neck Cancer

11.3.7.7 Prostate Cancer

11.3.7.8 Thyroid Cancer)

11.3.8 Historic and Forecasted Market Size by Distribution Channel

11.3.8.1 Hospital Pharmacies

11.3.8.2 Retail Pharmacies

11.3.8.3 Online Pharmacies

11.3.9 Historic and Forecasted Market Size by End-user

11.3.9.1 Hospitals

11.3.9.2 Diagnostic Laboratories

11.3.9.3 Diagnostic Imaging Centres

11.3.9.4 Academia

11.3.9.5 Specialty Clinics

11.3.10 Historic and Forecast Market Size by Country

11.3.10.1 Russia

11.3.10.2 Bulgaria

11.3.10.3 The Czech Republic

11.3.10.4 Hungary

11.3.10.5 Poland

11.3.10.6 Romania

11.3.10.7 Rest of Eastern Europe

11.4. Western Europe Oncology Drugs Market

11.4.1 Key Market Trends, Growth Factors and Opportunities

11.4.2 Top Key Companies

11.4.3 Historic and Forecasted Market Size by Segments

11.4.4 Historic and Forecasted Market Size by Diagnostics & Treatment

11.4.4.1 Diagnostics

11.4.4.2 Biopsy

11.4.4.3 Imaging

11.4.4.4 Immunohistochemistry

11.4.4.5 Tumour Biomarkers Test

11.4.4.6 In Situ Hybridization

11.4.4.7 Liquid Biopsy

11.4.4.8 Treatment

11.4.4.9 Targeted Therapy

11.4.4.10 Chemotherapy

11.4.4.11 Hormonal Therapy

11.4.4.12 Immunotherapy

11.4.5 Historic and Forecasted Market Size by Drugs Class

11.4.5.1 Cytotoxic Drugs

11.4.5.2 Targeted Drugs

11.4.5.3 Hormonal Drugs

11.4.5.4 Immunomodulatory Drugs

11.4.6 Historic and Forecasted Market Size by Dosage Form

11.4.6.1 Solid

11.4.6.2 Liquid

11.4.6.3 Injectable

11.4.7 Historic and Forecasted Market Size by Indication

11.4.7.1 Lungs Cancer

11.4.7.2 Colorectal Cancer

11.4.7.3 Breast Cancer

11.4.7.4 Liver Cancer

11.4.7.5 Bladder Cancer

11.4.7.6 Others (Head & Neck Cancer

11.4.7.7 Prostate Cancer

11.4.7.8 Thyroid Cancer)

11.4.8 Historic and Forecasted Market Size by Distribution Channel

11.4.8.1 Hospital Pharmacies

11.4.8.2 Retail Pharmacies

11.4.8.3 Online Pharmacies

11.4.9 Historic and Forecasted Market Size by End-user

11.4.9.1 Hospitals

11.4.9.2 Diagnostic Laboratories

11.4.9.3 Diagnostic Imaging Centres

11.4.9.4 Academia

11.4.9.5 Specialty Clinics

11.4.10 Historic and Forecast Market Size by Country

11.4.10.1 Germany

11.4.10.2 UK

11.4.10.3 France

11.4.10.4 The Netherlands

11.4.10.5 Italy

11.4.10.6 Spain

11.4.10.7 Rest of Western Europe

11.5. Asia Pacific Oncology Drugs Market

11.5.1 Key Market Trends, Growth Factors and Opportunities

11.5.2 Top Key Companies

11.5.3 Historic and Forecasted Market Size by Segments

11.5.4 Historic and Forecasted Market Size by Diagnostics & Treatment

11.5.4.1 Diagnostics

11.5.4.2 Biopsy

11.5.4.3 Imaging

11.5.4.4 Immunohistochemistry

11.5.4.5 Tumour Biomarkers Test

11.5.4.6 In Situ Hybridization

11.5.4.7 Liquid Biopsy

11.5.4.8 Treatment

11.5.4.9 Targeted Therapy

11.5.4.10 Chemotherapy

11.5.4.11 Hormonal Therapy

11.5.4.12 Immunotherapy

11.5.5 Historic and Forecasted Market Size by Drugs Class

11.5.5.1 Cytotoxic Drugs

11.5.5.2 Targeted Drugs

11.5.5.3 Hormonal Drugs

11.5.5.4 Immunomodulatory Drugs

11.5.6 Historic and Forecasted Market Size by Dosage Form

11.5.6.1 Solid

11.5.6.2 Liquid

11.5.6.3 Injectable

11.5.7 Historic and Forecasted Market Size by Indication

11.5.7.1 Lungs Cancer

11.5.7.2 Colorectal Cancer

11.5.7.3 Breast Cancer

11.5.7.4 Liver Cancer

11.5.7.5 Bladder Cancer

11.5.7.6 Others (Head & Neck Cancer

11.5.7.7 Prostate Cancer

11.5.7.8 Thyroid Cancer)

11.5.8 Historic and Forecasted Market Size by Distribution Channel

11.5.8.1 Hospital Pharmacies

11.5.8.2 Retail Pharmacies

11.5.8.3 Online Pharmacies

11.5.9 Historic and Forecasted Market Size by End-user

11.5.9.1 Hospitals

11.5.9.2 Diagnostic Laboratories

11.5.9.3 Diagnostic Imaging Centres

11.5.9.4 Academia

11.5.9.5 Specialty Clinics

11.5.10 Historic and Forecast Market Size by Country

11.5.10.1 China

11.5.10.2 India

11.5.10.3 Japan

11.5.10.4 South Korea

11.5.10.5 Malaysia

11.5.10.6 Thailand

11.5.10.7 Vietnam

11.5.10.8 The Philippines

11.5.10.9 Australia

11.5.10.10 New Zealand

11.5.10.11 Rest of APAC

11.6. Middle East & Africa Oncology Drugs Market

11.6.1 Key Market Trends, Growth Factors and Opportunities

11.6.2 Top Key Companies

11.6.3 Historic and Forecasted Market Size by Segments

11.6.4 Historic and Forecasted Market Size by Diagnostics & Treatment

11.6.4.1 Diagnostics

11.6.4.2 Biopsy

11.6.4.3 Imaging

11.6.4.4 Immunohistochemistry

11.6.4.5 Tumour Biomarkers Test

11.6.4.6 In Situ Hybridization

11.6.4.7 Liquid Biopsy

11.6.4.8 Treatment

11.6.4.9 Targeted Therapy

11.6.4.10 Chemotherapy

11.6.4.11 Hormonal Therapy

11.6.4.12 Immunotherapy

11.6.5 Historic and Forecasted Market Size by Drugs Class

11.6.5.1 Cytotoxic Drugs

11.6.5.2 Targeted Drugs

11.6.5.3 Hormonal Drugs

11.6.5.4 Immunomodulatory Drugs

11.6.6 Historic and Forecasted Market Size by Dosage Form

11.6.6.1 Solid

11.6.6.2 Liquid

11.6.6.3 Injectable

11.6.7 Historic and Forecasted Market Size by Indication

11.6.7.1 Lungs Cancer

11.6.7.2 Colorectal Cancer

11.6.7.3 Breast Cancer

11.6.7.4 Liver Cancer

11.6.7.5 Bladder Cancer

11.6.7.6 Others (Head & Neck Cancer

11.6.7.7 Prostate Cancer

11.6.7.8 Thyroid Cancer)

11.6.8 Historic and Forecasted Market Size by Distribution Channel

11.6.8.1 Hospital Pharmacies

11.6.8.2 Retail Pharmacies

11.6.8.3 Online Pharmacies

11.6.9 Historic and Forecasted Market Size by End-user

11.6.9.1 Hospitals

11.6.9.2 Diagnostic Laboratories

11.6.9.3 Diagnostic Imaging Centres

11.6.9.4 Academia

11.6.9.5 Specialty Clinics

11.6.10 Historic and Forecast Market Size by Country

11.6.10.1 Turkiye

11.6.10.2 Bahrain

11.6.10.3 Kuwait

11.6.10.4 Saudi Arabia

11.6.10.5 Qatar

11.6.10.6 UAE

11.6.10.7 Israel

11.6.10.8 South Africa

11.7. South America Oncology Drugs Market

11.7.1 Key Market Trends, Growth Factors and Opportunities

11.7.2 Top Key Companies

11.7.3 Historic and Forecasted Market Size by Segments

11.7.4 Historic and Forecasted Market Size by Diagnostics & Treatment

11.7.4.1 Diagnostics

11.7.4.2 Biopsy

11.7.4.3 Imaging

11.7.4.4 Immunohistochemistry

11.7.4.5 Tumour Biomarkers Test

11.7.4.6 In Situ Hybridization

11.7.4.7 Liquid Biopsy

11.7.4.8 Treatment

11.7.4.9 Targeted Therapy

11.7.4.10 Chemotherapy

11.7.4.11 Hormonal Therapy

11.7.4.12 Immunotherapy

11.7.5 Historic and Forecasted Market Size by Drugs Class

11.7.5.1 Cytotoxic Drugs

11.7.5.2 Targeted Drugs

11.7.5.3 Hormonal Drugs

11.7.5.4 Immunomodulatory Drugs

11.7.6 Historic and Forecasted Market Size by Dosage Form

11.7.6.1 Solid

11.7.6.2 Liquid

11.7.6.3 Injectable

11.7.7 Historic and Forecasted Market Size by Indication

11.7.7.1 Lungs Cancer

11.7.7.2 Colorectal Cancer

11.7.7.3 Breast Cancer

11.7.7.4 Liver Cancer

11.7.7.5 Bladder Cancer

11.7.7.6 Others (Head & Neck Cancer

11.7.7.7 Prostate Cancer

11.7.7.8 Thyroid Cancer)

11.7.8 Historic and Forecasted Market Size by Distribution Channel

11.7.8.1 Hospital Pharmacies

11.7.8.2 Retail Pharmacies

11.7.8.3 Online Pharmacies

11.7.9 Historic and Forecasted Market Size by End-user

11.7.9.1 Hospitals

11.7.9.2 Diagnostic Laboratories

11.7.9.3 Diagnostic Imaging Centres

11.7.9.4 Academia

11.7.9.5 Specialty Clinics

11.7.10 Historic and Forecast Market Size by Country

11.7.10.1 Brazil

11.7.10.2 Argentina

11.7.10.3 Rest of SA

Chapter 12 Analyst Viewpoint and Conclusion

12.1 Recommendations and Concluding Analysis

12.2 Potential Market Strategies

Chapter 13 Research Methodology

13.1 Research Process

13.2 Primary Research

13.3 Secondary Research

|

Global Oncology Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 221.36 Bn. |

|

Forecast Period 2024-32 CAGR: |

8.83 % |

Market Size in 2032: |

USD 474.06 Bn. |

|

Segments Covered: |

By Diagnostics & Treatment |

|

|

|

By Drugs Class |

|

||

|

By Dosage Form |

|

||

|

By Indication |

|

||

|

By Distribution Channel |

|

||

|

By End-user |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||