Ocular Implant Market Synopsis:

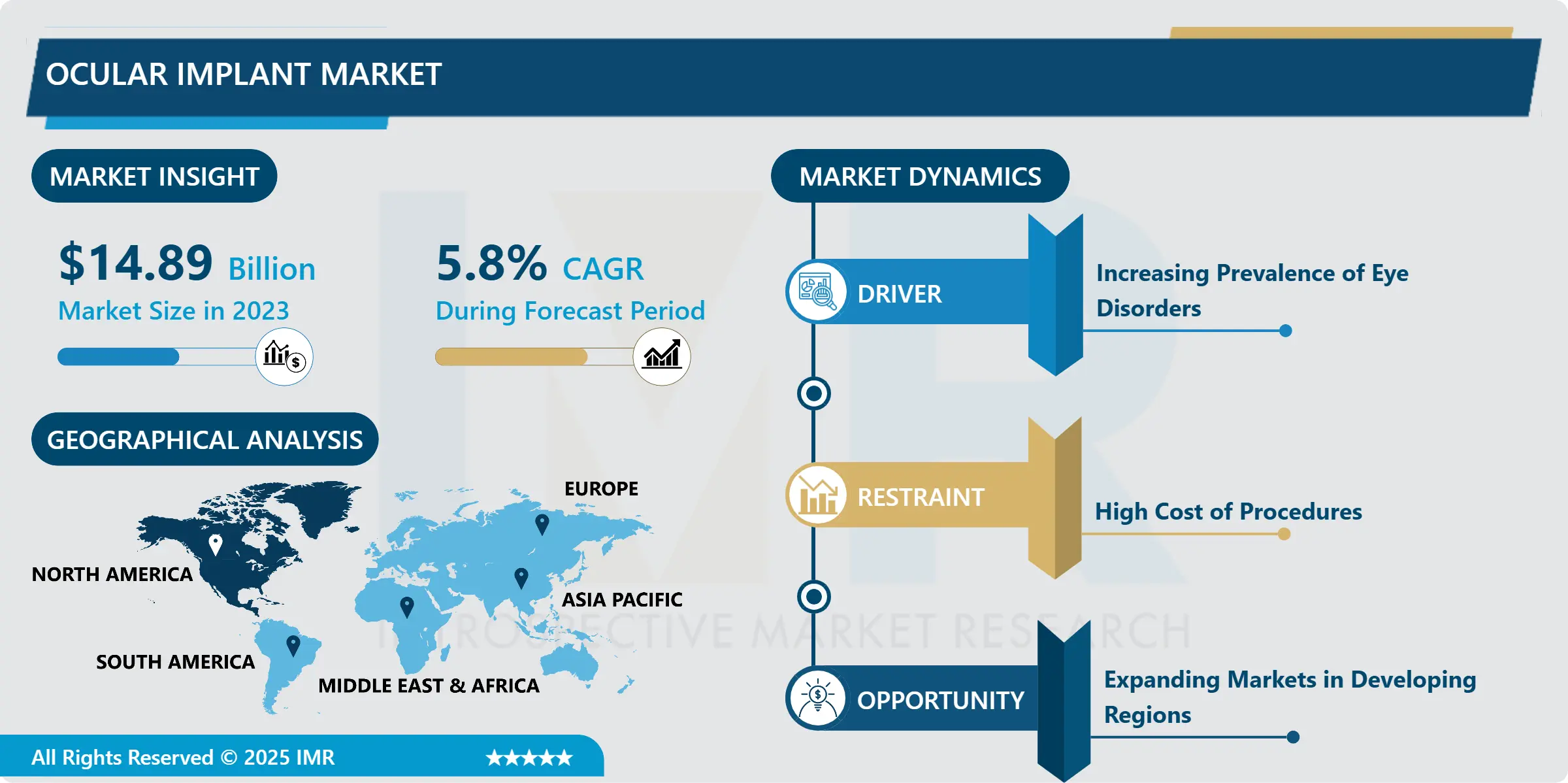

Ocular Implant Market Size Was Valued at USD 14.89 Billion in 2023, and is Projected to Reach USD 24.73 Billion by 2032, Growing at a CAGR of 5.80% From 2024-2032.

The global ocular implant market has witnessed significant growth in recent years due to the increasing prevalence of eye-related disorders and advancements in ophthalmic surgeries. Ocular implants are medical devices that are surgically placed within the eye to restore or improve vision. These implants are primarily used for cataract surgery, retinal diseases, glaucoma, and corneal repair. With the rising number of aging populations and an increasing burden of ocular diseases, the demand for these implants has seen a steady rise, propelling market expansion worldwide.

The major drivers of the ocular implant market is the growing prevalence of age-related eye conditions, such as cataracts and macular degeneration. Cataracts, in particular, have been a significant contributor to the high demand for intraocular lenses (IOLs), which are used to replace the clouded lens in cataract surgeries. Furthermore, advancements in implant technology, such as foldable IOLs and custom-designed lenses, have enhanced the outcomes of ocular surgeries, attracting a larger patient base. Additionally, increasing awareness of eye health and technological innovations in diagnostic devices have improved early detection and treatment of eye diseases.

The aging population is one of the primary factors fueling the growth of the ocular implant market. As the global population ages, the incidence of age-related macular degeneration, glaucoma, and cataracts continues to rise, driving the demand for ocular implants. In addition, ongoing technological innovations, such as the development of smart retinal implants and minimally invasive surgical procedures, are contributing to market growth. These advancements improve the safety and efficacy of ocular surgeries, making them more accessible and effective for patients.

There are significant growth opportunities in emerging economies, where improvements in healthcare infrastructure are increasing access to ocular treatments. Furthermore, the growing focus on personalized medicine, including customized ocular implants, is expected to provide lucrative opportunities for market players to expand their product offerings and cater to a broader range of patient needs.

Ocular Implant Market Trend Analysis:

Rising Demand for Advanced Ocular Implants Driven by Prevalence of Eye Disorders and Minimally Invasive Surgeries

-

The rising demand for advanced ocular implants is largely driven by the increasing prevalence of eye disorders, particularly age-related conditions such as cataracts, glaucoma, and macular degeneration. With a growing global aging population, the incidence of these eye conditions has surged, leading to a higher demand for ocular implants like intraocular lenses (IOLs) and retinal implants. As the number of people requiring surgical intervention for vision correction increases, the market for advanced ocular implants has expanded significantly. These implants offer patients improved visual outcomes and faster recovery times, which are key factors contributing to their growing adoption in ophthalmic procedures.

- The shift toward minimally invasive surgeries has played a significant role in driving the demand for advanced ocular implants. Techniques such as laser-assisted cataract surgery and small-incision surgeries reduce the risk of complications and shorten recovery times compared to traditional surgical methods. These advancements have made ocular implants more accessible to a broader patient population, further fueling market growth. Minimally invasive procedures also reduce healthcare costs, making ocular implant surgeries a more attractive option for both patients and healthcare providers, particularly in regions with growing demand for efficient, cost-effective treatments.

Rising Adoption of Advanced Ocular Implants and the Impact of an Aging Population

-

The rising adoption of advanced ocular implants is closely linked to the growing prevalence of eye disorders, particularly among the aging population. As individuals age, the likelihood of developing conditions like cataracts, macular degeneration, and glaucoma increases, creating a strong demand for ocular implants. Advanced implants, such as intraocular lenses (IOLs) and retinal implants, have revolutionized the treatment landscape by offering enhanced visual outcomes and improving the quality of life for elderly patients. With the aging population projected to increase globally, the demand for these implants is expected to rise, making them an essential part of modern ophthalmic care.

- The aging population not only drives demand for ocular implants but also influences the types of treatments sought. Older adults are more likely to opt for advanced, minimally invasive procedures that promise quicker recovery times and less post-surgical discomfort. As a result, healthcare providers are increasingly adopting state-of-the-art ocular implants to meet these preferences. The growing focus on patient-centered care and the desire to preserve or restore vision as people age has made advanced ocular implants an integral part of ophthalmic treatments. This trend is expected to continue, as the global population ages, further accelerating the adoption of these innovative solutions in the market.

Ocular Implant Market Segment Analysis:

Ocular Implant Market is Segmented on the basis of By Type, Application, End-use, and Region.

By Type, Intraocular Lens segment is expected to dominate the market during the forecast period

-

The Intraocular Lens (IOL) segment is expected to dominate the ocular implant market during the forecast period, primarily due to its widespread use in cataract surgery. Cataracts are one of the most common age-related eye conditions, leading to clouding of the eye's natural lens. IOLs are implanted during cataract surgery to replace the clouded lens, restoring vision. With cataract surgery being one of the most frequently performed procedures worldwide, the demand for IOLs remains consistently high. Advancements in IOL technology, such as the development of foldable and customizable lenses, have further expanded their adoption, enabling better visual outcomes and quicker recovery times for patients.

- The growing aging population and the rising number of cataract cases worldwide are significant factors contributing to the dominance of the IOL segment. As the global population continues to age, the incidence of cataracts is expected to increase, driving further demand for IOLs. The availability of various types of IOLs, such as monofocal, multifocal, and toric lenses, offers patients a range of options tailored to their specific needs, further enhancing the appeal of this segment. As a result, the Intraocular Lens segment is poised to maintain its leadership in the ocular implant market throughout the forecast period.

By End-use, Hospitals segment expected to held the largest share

-

The Hospitals segment is expected to hold the largest share of the ocular implant market due to their central role in performing complex ocular surgeries, such as cataract surgeries and retinal implant procedures. Hospitals have the necessary infrastructure, specialized medical staff, and advanced surgical equipment to support a wide range of ophthalmic surgeries. As the primary settings for these high-volume procedures, hospitals are the largest consumers of ocular implants, especially intraocular lenses (IOLs) and retinal implants. The increasing number of cataract surgeries and advancements in surgical techniques within hospital settings contribute to the dominant position of this segment.

- Furthermore, hospitals benefit from the availability of specialized departments, including ophthalmology units equipped to handle both routine and advanced ocular implant procedures. The growing adoption of minimally invasive surgical techniques in hospitals also enhances the appeal of ocular implants, as they are associated with quicker recovery times and fewer complications. As healthcare systems continue to prioritize quality care and improve access to ophthalmic treatments, hospitals are expected to remain the primary end-users of ocular implants, further solidifying their dominance in the market throughout the forecast period.

Ocular Implant Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

-

North America has the most developed market for ocular implants give a good number of factors including the local medical care systems, superior re-imbursing policies and a superior advertising of modern technologies. The growth of the market is due to the ageing populace who fell prey to macular degeneration, cataracts and glaucoma-related eye ailments. This aged society is gradually leading to increased need for ocular implants especially IOLs and Retinal implants. Also, the region has a robust base of prominent market participants who remain involved in the process of research and development (R&D) to launch new solutions to the market. Such factors combined with a greater patient–level awareness of vision care drive the growth of the ocular implant market.

- The share of North American countries is significant in the ocular implant market dominated by the United States. This is mainly due to sustained innovation spending of the private sector firms and university researchers to create advanced implant technologies. Furthermore, increasing patient literacy of vision care and expanded availability of adequate treatments to implant ocular has contributed to the higher adoption ratio among patient categories. A positive attitude to form new implants also reinforces the leadership of the US in the region, owing to the helpful partnership between public and private sectors and helpful regulations.

Active Key Players in the Ocular Implant Market:

-

Alcon, Inc.

- Bausch & Lomb, Inc.

- Carl Zeiss AG

- Glaukos Corporation

- Hoya Corporation

- Johnson & Johnson

- Morcher GmbH

- STAAR Surgical Company, and Other Active Players

|

Global Ocular Implant Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 14.89 Billion |

|

Forecast Period 2024-32 CAGR: |

5.80% |

Market Size in 2032: |

USD 24.73 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By End-use |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Ocular Implant Market by Type

4.1 Ocular Implant Market Snapshot and Growth Engine

4.2 Ocular Implant Market Overview

4.3 Intraocular Lens

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.3.3 Key Market Trends, Growth Factors and Opportunities

4.3.4 Intraocular Lens: Geographic Segmentation Analysis

4.4 Corneal Implants

4.4.1 Introduction and Market Overview

4.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.4.3 Key Market Trends, Growth Factors and Opportunities

4.4.4 Corneal Implants: Geographic Segmentation Analysis

4.5 Orbital Implants

4.5.1 Introduction and Market Overview

4.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.5.3 Key Market Trends, Growth Factors and Opportunities

4.5.4 Orbital Implants: Geographic Segmentation Analysis

4.6 Glaucoma Implants

4.6.1 Introduction and Market Overview

4.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.6.3 Key Market Trends, Growth Factors and Opportunities

4.6.4 Glaucoma Implants: Geographic Segmentation Analysis

4.7 Ocular Prosthesis and Others

4.7.1 Introduction and Market Overview

4.7.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.7.3 Key Market Trends, Growth Factors and Opportunities

4.7.4 Ocular Prosthesis and Others: Geographic Segmentation Analysis

Chapter 5: Ocular Implant Market by Application

5.1 Ocular Implant Market Snapshot and Growth Engine

5.2 Ocular Implant Market Overview

5.3 Glaucoma Surgery

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.3.3 Key Market Trends, Growth Factors and Opportunities

5.3.4 Glaucoma Surgery: Geographic Segmentation Analysis

5.4 Oculoplasty

5.4.1 Introduction and Market Overview

5.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.4.3 Key Market Trends, Growth Factors and Opportunities

5.4.4 Oculoplasty: Geographic Segmentation Analysis

5.5 Drug Delivery

5.5.1 Introduction and Market Overview

5.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.5.3 Key Market Trends, Growth Factors and Opportunities

5.5.4 Drug Delivery: Geographic Segmentation Analysis

5.6 Age-related Macular Degeneration and Aesthetic Purpose

5.6.1 Introduction and Market Overview

5.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.6.3 Key Market Trends, Growth Factors and Opportunities

5.6.4 Age-related Macular Degeneration and Aesthetic Purpose: Geographic Segmentation Analysis

Chapter 6: Ocular Implant Market by End-use

6.1 Ocular Implant Market Snapshot and Growth Engine

6.2 Ocular Implant Market Overview

6.3 Hospitals

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.3.3 Key Market Trends, Growth Factors and Opportunities

6.3.4 Hospitals: Geographic Segmentation Analysis

6.4 Specialty Eye Institutes and Clinics

6.4.1 Introduction and Market Overview

6.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.4.3 Key Market Trends, Growth Factors and Opportunities

6.4.4 Specialty Eye Institutes and Clinics: Geographic Segmentation Analysis

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Ocular Implant Market Share by Manufacturer (2023)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 ALCON INC BAUSCH & LOMB INC CARL ZEISS AG

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 JOHNSON & JOHNSON

7.4 STAAR SURGICAL COMPANY

7.5 MORCHER GMBH

7.6 HOYA CORPORATION

7.7 GLAUKOS CORPORATION

7.8 OTHER ACTIVE PLAYERS

Chapter 8: Global Ocular Implant Market By Region

8.1 Overview

8.2. North America Ocular Implant Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size By Type

8.2.4.1 Intraocular Lens

8.2.4.2 Corneal Implants

8.2.4.3 Orbital Implants

8.2.4.4 Glaucoma Implants

8.2.4.5 Ocular Prosthesis and Others

8.2.5 Historic and Forecasted Market Size By Application

8.2.5.1 Glaucoma Surgery

8.2.5.2 Oculoplasty

8.2.5.3 Drug Delivery

8.2.5.4 Age-related Macular Degeneration and Aesthetic Purpose

8.2.6 Historic and Forecasted Market Size By End-use

8.2.6.1 Hospitals

8.2.6.2 Specialty Eye Institutes and Clinics

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Ocular Implant Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size By Type

8.3.4.1 Intraocular Lens

8.3.4.2 Corneal Implants

8.3.4.3 Orbital Implants

8.3.4.4 Glaucoma Implants

8.3.4.5 Ocular Prosthesis and Others

8.3.5 Historic and Forecasted Market Size By Application

8.3.5.1 Glaucoma Surgery

8.3.5.2 Oculoplasty

8.3.5.3 Drug Delivery

8.3.5.4 Age-related Macular Degeneration and Aesthetic Purpose

8.3.6 Historic and Forecasted Market Size By End-use

8.3.6.1 Hospitals

8.3.6.2 Specialty Eye Institutes and Clinics

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Ocular Implant Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size By Type

8.4.4.1 Intraocular Lens

8.4.4.2 Corneal Implants

8.4.4.3 Orbital Implants

8.4.4.4 Glaucoma Implants

8.4.4.5 Ocular Prosthesis and Others

8.4.5 Historic and Forecasted Market Size By Application

8.4.5.1 Glaucoma Surgery

8.4.5.2 Oculoplasty

8.4.5.3 Drug Delivery

8.4.5.4 Age-related Macular Degeneration and Aesthetic Purpose

8.4.6 Historic and Forecasted Market Size By End-use

8.4.6.1 Hospitals

8.4.6.2 Specialty Eye Institutes and Clinics

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Ocular Implant Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size By Type

8.5.4.1 Intraocular Lens

8.5.4.2 Corneal Implants

8.5.4.3 Orbital Implants

8.5.4.4 Glaucoma Implants

8.5.4.5 Ocular Prosthesis and Others

8.5.5 Historic and Forecasted Market Size By Application

8.5.5.1 Glaucoma Surgery

8.5.5.2 Oculoplasty

8.5.5.3 Drug Delivery

8.5.5.4 Age-related Macular Degeneration and Aesthetic Purpose

8.5.6 Historic and Forecasted Market Size By End-use

8.5.6.1 Hospitals

8.5.6.2 Specialty Eye Institutes and Clinics

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Ocular Implant Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size By Type

8.6.4.1 Intraocular Lens

8.6.4.2 Corneal Implants

8.6.4.3 Orbital Implants

8.6.4.4 Glaucoma Implants

8.6.4.5 Ocular Prosthesis and Others

8.6.5 Historic and Forecasted Market Size By Application

8.6.5.1 Glaucoma Surgery

8.6.5.2 Oculoplasty

8.6.5.3 Drug Delivery

8.6.5.4 Age-related Macular Degeneration and Aesthetic Purpose

8.6.6 Historic and Forecasted Market Size By End-use

8.6.6.1 Hospitals

8.6.6.2 Specialty Eye Institutes and Clinics

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Ocular Implant Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size By Type

8.7.4.1 Intraocular Lens

8.7.4.2 Corneal Implants

8.7.4.3 Orbital Implants

8.7.4.4 Glaucoma Implants

8.7.4.5 Ocular Prosthesis and Others

8.7.5 Historic and Forecasted Market Size By Application

8.7.5.1 Glaucoma Surgery

8.7.5.2 Oculoplasty

8.7.5.3 Drug Delivery

8.7.5.4 Age-related Macular Degeneration and Aesthetic Purpose

8.7.6 Historic and Forecasted Market Size By End-use

8.7.6.1 Hospitals

8.7.6.2 Specialty Eye Institutes and Clinics

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Global Ocular Implant Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 14.89 Billion |

|

Forecast Period 2024-32 CAGR: |

5.80% |

Market Size in 2032: |

USD 24.73 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By End-use |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||