Global Non-protein Nitrogen in Feed Market Overview

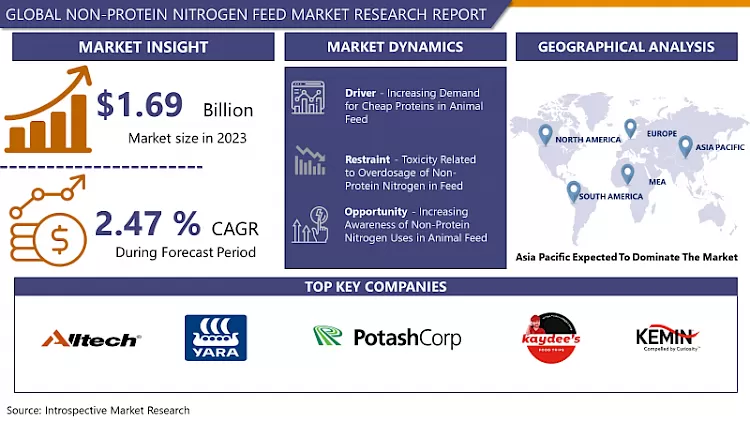

Non-protein Nitrogen in Feed Market Size Was Valued at USD 1.69 Billion in 2023 and is Projected to Reach USD 2.47 Billion by 2032, Growing at a CAGR of 4.29% From 2024-2032

Compounds that provide nitrogen other than protein form are called non-protein nitrogen (NPN) compounds. Non-protein nitrogen is a form of inactive protein which converts into an active protein form in the gut of animals. Non-protein nitrogen (NPN) is a less expensive form of protein that is recently being used in animal nutrition as feed. These are non-protein components thereof no use for humans but microbiota present in the gut of animals helps them to convert these non-protein components in protein form and are then absorbed. Proteins play an important role in development, improvising metabolism, and hormone and DNA production in the animal body. Moreover, they are also required to replace damaged and dead animal cells. NPN is also used to increase crude protein values artificially. Crude protein values are measured based on the presence of nitrogen content as protein. Furthermore, crude proteins have both true proteins and other nitrogenous products yet only true proteins are digested and then absorbed by animals. Ruminants are the only animals that can digest NPN while other digestive systems are not designed to digest NPN.

Market Dynamics And Factors in Non-protein Nitrogen In Feed Market

Drivers:

Increasing Demand For Cheap Proteins In Animal Feed

The growing dairy industry, increased demand for eggs, and meat will boost the non-protein nitrogen market growth during the forecast period. Non-protein animal feed is economically favorable compared to proteins derived from plant and animal sources thus strengthening farmers financially by cutting costs on the purchase of premium protein brands for animal feed. Moreover, the ability of micro-organisms presents in the gut of ruminants to convert non-protein into protein is overwhelming, this converted protein is utilized by animals to produce milk and meat thus promoting the use of NPN in animal feed as nutrition. Urea is the major commercial source of non-protein nitrogen in the ruminant diet. Plant-derived proteins such as soybean meal are high priced this promotes the use of urea as a protein supplement in ruminant diets. It has been discovered that the use of urea in small amounts of sorghum reduced body weight loss, enhanced birth weight of calves, higher milk yields, and improvised calf growth rate these factors are promoting livestock growers to add NPN as a major nutrition source in animal feed. Innovations in the use of NPN as a protein source and increasing investment in research and development of the animal feed industry is boosting the NPN feed market.

Moreover, other sources of NPN are biuret, poultry litter or manure, ammonium hydroxide, uric acid, and other ammonia-containing compounds. Biuret is a compound derived from the condensation of two urea molecules. It is the most discussed topic owing to its potential source of NPN as well as its solubility and slow rate of degradation. Furthermore, it is slowly degraded in rumen thus providing a continuous source of ammonia. There is an adaptation period of two weeks to two months required for the gut bacteria to carry out maximin utilization of NPN before using biuret as the main source of NPN in animal feed. The main advantage of BIUTRET is a large amount of it can be consumed by animals safely without causing any complications thus promoting the growth of the NPN feed market. The use of poultry litter or manure as a source of NPN feed is becoming popular attributed to the utilization of waste products generated by the poultry industry and decreasing feed costs thus helping the Non-Protein Nitrogen feed market to flourish in the forecast period. Poultry litter added as NPN.

Restraints:

Toxicity Related To Overdosage Of Non-Protein Nitrogen In Feed

When NPN is given in higher amounts its causes poisoning. Urea poisoning is the most common toxicity found in ruminants. Moreover, biuret poisoning is not observed as it is slowly degraded but it’s cost of production is a matter of concern as it is economically unfavorable thus hampering the growth of the market in the forecast period. Poisoning may also occur when a ruminant animal is not adapted to non-protein nitrogen sources, feed is not properly mixed, and high urea concentration is present in low energy, and high roughage diets. Moreover, NPN feed should be given to those animals having a functional rumen, it should not be given to young calves and monogastric animals. Monogastric is a term used for animals having only one stomach or a stomach with only one digestive chamber. Biuret doesn't have any nutritional advantage over urea as well it is commercially unavailable thus restricting the use of biuret as NPN feed. Furthermore, it is debated that microorganisms like Salmonella and Proteus are present in fresh poultry litter thus generating drawbacks for animal health and eventually restraining its use in animal feed. Additionally, any nutrient deficiency which negatively impacts the activity of microorganisms present in the gut or decreases dry matter digestibility will likely reduce urea utilization in animals.

Opportunities:

Increasing Awareness Of Non-Protein Nitrogen Uses In Animal Feed

The increasing demand for milk and milk-derived products, ready-to-eat processed meat and nutrition enriched animal feed is going to provide opportunities for market players. Moreover, NPN like Urea, biuret and poultry manure are nutritionally incompetent thus adding other supplements will make them nutrition-rich and then these can be used to feed animals. As NPN feed is economically favorable there has been an unprecedented rise in demand instigating market players to increase the production of NPN feed. Moreover, urea is the most commonly used NPN source as it is cheap and easily available for consumption. Attributed to the advantages of urea as NPN source market players have invested in its research and development to make urea less harmful and to reduce its degradation speed. Providing packets that can be readily mixed and fed to animals is a vital opportunity as it can avoid errors in calculating the amount of urea to add in proportionate with water or other supplements.

Challenges:

Quality Control And Increasing Demand For Non-Protein Nitrogen In Animal Feed

Providing livestock with proper nutrition and at an affordable price is the biggest challenge for market players. Diseases associated with the use of poultry litter or manure are the most debated topic as use of it as an NPN source can cause harmful effects on animal health and performance thus, finding an alternative way of using poultry litter or manure is one of the challenges. To eliminate the chances of urea poisoning there should be strict quality control on urea addition thus, strict and proper quality control is needed. The shortage of global protein supplies is spreading uncertainty in producers and the feed industry to think about protein supply and where it will come from. Moreover, ever-increasing pressure on market players to meet the growing global demand for milk and meat while also reducing their environmental impact and remaining financially viable.

Market Segmentation

Segmentation Analysis of Non-protein Nitrogen in Feed Market:

Based on Sources, the non-protein nitrogen in the feed market is going to expand during the forecast period attributed to an everyday increasing population of livestock and demand for livestock's proper nutrition. Urea is the most common source of NPN because of its low cost and ease of availability. Moreover, urea provides other necessary nutrition required for the growth of animals that are not found in other sources of non-protein nitrogen. Urea dissolves at a rapid rate in rumen thus providing ammonia to microflora to synthesize amino acids.

Based on Form, dry segment such as powder and pellets or granules is going to have a maximum share of non-protein nitrogen in feed market during the forecast period. The convenience in availability and packaging is the main advantage of a dry segment.

Based on Livestock, animals like cattle, swine, and buffaloes are the major consumers of non-protein nitrogen. To increase the yield of milk in cattle and buffaloes NPN is used, it also increases their performance owing to which NPN is widely used to feed animals. Consequently, high protein deficiency in cows due to the low quality of fodder is increasing the demand for this segment during the forecast period. Swine are the only non-ruminants in which NPN is used as feed.

Regional Analysis of Non-Protein Nitrogen in Feed Market:

Geographically, Non-protein nitrogen in the feed market is segmented into Asia Pacific, Europe, Middle East, Latin America, North America, and.

Asia Pacific region is expected to dominate the market, owing to high consumption of non-protein nitrogen feed because of its high population of cattle, buffaloes, and sheep. The economies like India and China are the highest consumers of meat and milk owing to their denser populations. To meet the growing demand adoption of non-protein nitrogen in feed is going to propel the market growth in the Asia Pacific region during the forecast period.

North America region is expected to significantly grow when it comes to manufacturing of non-protein nitrogen in feed. Moreover, the growth in the North American market is attributed to the presence of large manufacturing companies such as Cargill Inc, Land O'Lakes Inc, and others. An increase in research and development for innovation of newer products is going to boost the market growth in the forecast period.

Latin American market has profitable growth opportunities, increase in utilization and production of meat in Brazil and Mexico and increase in animal welfare expenditure is going to accelerate the market growth during the forecast period.

The Middle East region is going to grow at a slower rate owing to the government regulations and lack of awareness of non-protein nitrogen in feed among the livestock growers.

Players Covered in Non-protein Nitrogen in Feed Market are:

- Alltech (US)

- Yara International (Norway)

- The Potash Corporation of Saskatchewan (Canada)

- KAYDEEFEED (US)

- Kemin Industries Inc (US)

- Molatek (South Africa)

- Land O'Lakes Inc (US)

- Cargill Incorporated (US)

- Tyson Foods Inc (US)

- ADM Animal Nutrition (US)

- Southern States (US)

- Nutreco (Netherlands)

- Anipro Feeds (US) and other major players.

Key Industry Developments in Non-protein Nitrogen Feed Market

- In December 2023, ADM a global leader in human and animal nutrition, announced today that it has reached an agreement to acquire PT Trouw Nutrition Indonesia, a subsidiary of Nutreco and a leading provider of functional and nutritional solutions for livestock farming in Indonesia

- In May 2023, Alltech announced that it had acquired a majority interest in Agolin, an animal nutrition company based in Switzerland that has developed and produced plant-based nutrition solutions that improve livestock performance, profitability, and sustainability.

|

Global Non-protein Nitrogen in Feed Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2016 to 2022 |

Market Size in 2023: |

USD 1.69 Bn. |

|

Forecast Period 2024-32 CAGR: |

4.29% |

Market Size in 2032: |

USD 2.47 Bn. |

|

Segments Covered: |

By Source |

|

|

|

By Form |

|

||

|

By Livestock |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Non-protein Nitrogen in Feed Market by Source (2018-2032)

4.1 Non-protein Nitrogen in Feed Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Ammonia

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Urea

4.5 Biuret

4.6 Ammonium Salts

4.7 Others

Chapter 5: Non-protein Nitrogen in Feed Market by Form (2018-2032)

5.1 Non-protein Nitrogen in Feed Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Dry

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Powder

5.5 Pellets

5.6 Liquid

Chapter 6: Non-protein Nitrogen in Feed Market by Livestock (2018-2032)

6.1 Non-protein Nitrogen in Feed Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Cattle

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Swine

6.5 Sheep

6.6 Giraffe

6.7 Buffaloes

6.8 Other Ruminants

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Non-protein Nitrogen in Feed Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 ALLTECH (US)

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 YARA INTERNATIONAL (NORWAY)

7.4 THE POTASH CORPORATION OF SASKATCHEWAN (CANADA)

7.5 KAYDEEFEED (US)

7.6 KEMIN INDUSTRIES INC (US)

7.7 MOLATEK (SOUTH AFRICA)

7.8 LAND O'LAKES INC (US)

7.9 CARGILL INCORPORATED (US)

7.10 TYSON FOODS INC (US)

7.11 ADM ANIMAL NUTRITION (US)

7.12 SOUTHERN STATES (US)

7.13 NUTRECO (NETHERLANDS)

7.14 ANIPRO FEEDS (US)

Chapter 8: Global Non-protein Nitrogen in Feed Market By Region

8.1 Overview

8.2. North America Non-protein Nitrogen in Feed Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size by Source

8.2.4.1 Ammonia

8.2.4.2 Urea

8.2.4.3 Biuret

8.2.4.4 Ammonium Salts

8.2.4.5 Others

8.2.5 Historic and Forecasted Market Size by Form

8.2.5.1 Dry

8.2.5.2 Powder

8.2.5.3 Pellets

8.2.5.4 Liquid

8.2.6 Historic and Forecasted Market Size by Livestock

8.2.6.1 Cattle

8.2.6.2 Swine

8.2.6.3 Sheep

8.2.6.4 Giraffe

8.2.6.5 Buffaloes

8.2.6.6 Other Ruminants

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Non-protein Nitrogen in Feed Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size by Source

8.3.4.1 Ammonia

8.3.4.2 Urea

8.3.4.3 Biuret

8.3.4.4 Ammonium Salts

8.3.4.5 Others

8.3.5 Historic and Forecasted Market Size by Form

8.3.5.1 Dry

8.3.5.2 Powder

8.3.5.3 Pellets

8.3.5.4 Liquid

8.3.6 Historic and Forecasted Market Size by Livestock

8.3.6.1 Cattle

8.3.6.2 Swine

8.3.6.3 Sheep

8.3.6.4 Giraffe

8.3.6.5 Buffaloes

8.3.6.6 Other Ruminants

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Non-protein Nitrogen in Feed Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size by Source

8.4.4.1 Ammonia

8.4.4.2 Urea

8.4.4.3 Biuret

8.4.4.4 Ammonium Salts

8.4.4.5 Others

8.4.5 Historic and Forecasted Market Size by Form

8.4.5.1 Dry

8.4.5.2 Powder

8.4.5.3 Pellets

8.4.5.4 Liquid

8.4.6 Historic and Forecasted Market Size by Livestock

8.4.6.1 Cattle

8.4.6.2 Swine

8.4.6.3 Sheep

8.4.6.4 Giraffe

8.4.6.5 Buffaloes

8.4.6.6 Other Ruminants

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Non-protein Nitrogen in Feed Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size by Source

8.5.4.1 Ammonia

8.5.4.2 Urea

8.5.4.3 Biuret

8.5.4.4 Ammonium Salts

8.5.4.5 Others

8.5.5 Historic and Forecasted Market Size by Form

8.5.5.1 Dry

8.5.5.2 Powder

8.5.5.3 Pellets

8.5.5.4 Liquid

8.5.6 Historic and Forecasted Market Size by Livestock

8.5.6.1 Cattle

8.5.6.2 Swine

8.5.6.3 Sheep

8.5.6.4 Giraffe

8.5.6.5 Buffaloes

8.5.6.6 Other Ruminants

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Non-protein Nitrogen in Feed Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size by Source

8.6.4.1 Ammonia

8.6.4.2 Urea

8.6.4.3 Biuret

8.6.4.4 Ammonium Salts

8.6.4.5 Others

8.6.5 Historic and Forecasted Market Size by Form

8.6.5.1 Dry

8.6.5.2 Powder

8.6.5.3 Pellets

8.6.5.4 Liquid

8.6.6 Historic and Forecasted Market Size by Livestock

8.6.6.1 Cattle

8.6.6.2 Swine

8.6.6.3 Sheep

8.6.6.4 Giraffe

8.6.6.5 Buffaloes

8.6.6.6 Other Ruminants

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Non-protein Nitrogen in Feed Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size by Source

8.7.4.1 Ammonia

8.7.4.2 Urea

8.7.4.3 Biuret

8.7.4.4 Ammonium Salts

8.7.4.5 Others

8.7.5 Historic and Forecasted Market Size by Form

8.7.5.1 Dry

8.7.5.2 Powder

8.7.5.3 Pellets

8.7.5.4 Liquid

8.7.6 Historic and Forecasted Market Size by Livestock

8.7.6.1 Cattle

8.7.6.2 Swine

8.7.6.3 Sheep

8.7.6.4 Giraffe

8.7.6.5 Buffaloes

8.7.6.6 Other Ruminants

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Global Non-protein Nitrogen in Feed Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2016 to 2022 |

Market Size in 2023: |

USD 1.69 Bn. |

|

Forecast Period 2024-32 CAGR: |

4.29% |

Market Size in 2032: |

USD 2.47 Bn. |

|

Segments Covered: |

By Source |

|

|

|

By Form |

|

||

|

By Livestock |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Frequently Asked Questions :

The forecast period in the Non-protein Nitrogen in Feed Market research report is 2024-2032.

Alltech (US), Yara International (Norway), The Potash Corporation of Saskatchewan (Canada), Kaydeefeed (US), Kemin Industries Inc (US), Molatek (South Africa), Land O'Lakes Inc (US), Cargill Incorporated (US), Tyson Foods Inc (US), ADM Animal Nutrition (US), Southern States (US), Nutreco (Netherlands), Anipro Feeds (US), and other major players.

The Non-protein Nitrogen in Feed Market is segmented into source, form, livestock, and region. By Source, the market is categorized into Ammonia, Urea, Biuret, Ammonium Salts, and Others. By Form, the market is categorized into Dry {Powder, Pellets}, and Liquid. By Livestock, the market is categorized into Cattle, Swine, Sheep, Giraffe, Buffaloes, and Other Ruminants. By region, it is analyzed across North America (U.S.; Canada; Mexico), Europe (Germany; U.K.; France; Italy; Russia; Spain, etc.), Asia-Pacific (China; India; Japan; Southeast Asia, etc.), South America (Brazil; Argentina, etc.), Middle East & Africa (Saudi Arabia; South Africa, etc.).

Non-protein nitrogen (NPN) is a less expensive form of protein that is recently being used in animal nutrition as feed. These are non-protein components thereof no use for humans but microbiota present in the gut of animals helps them to convert these non-protein components in protein form and are then absorbed.

Non-protein Nitrogen in Feed Market Size Was Valued at USD 1.69 Billion in 2023 and is Projected to Reach USD 2.47 Billion by 2032, Growing at a CAGR of 4.29% From 2024-2032