Medical Implants Market Synopsis:

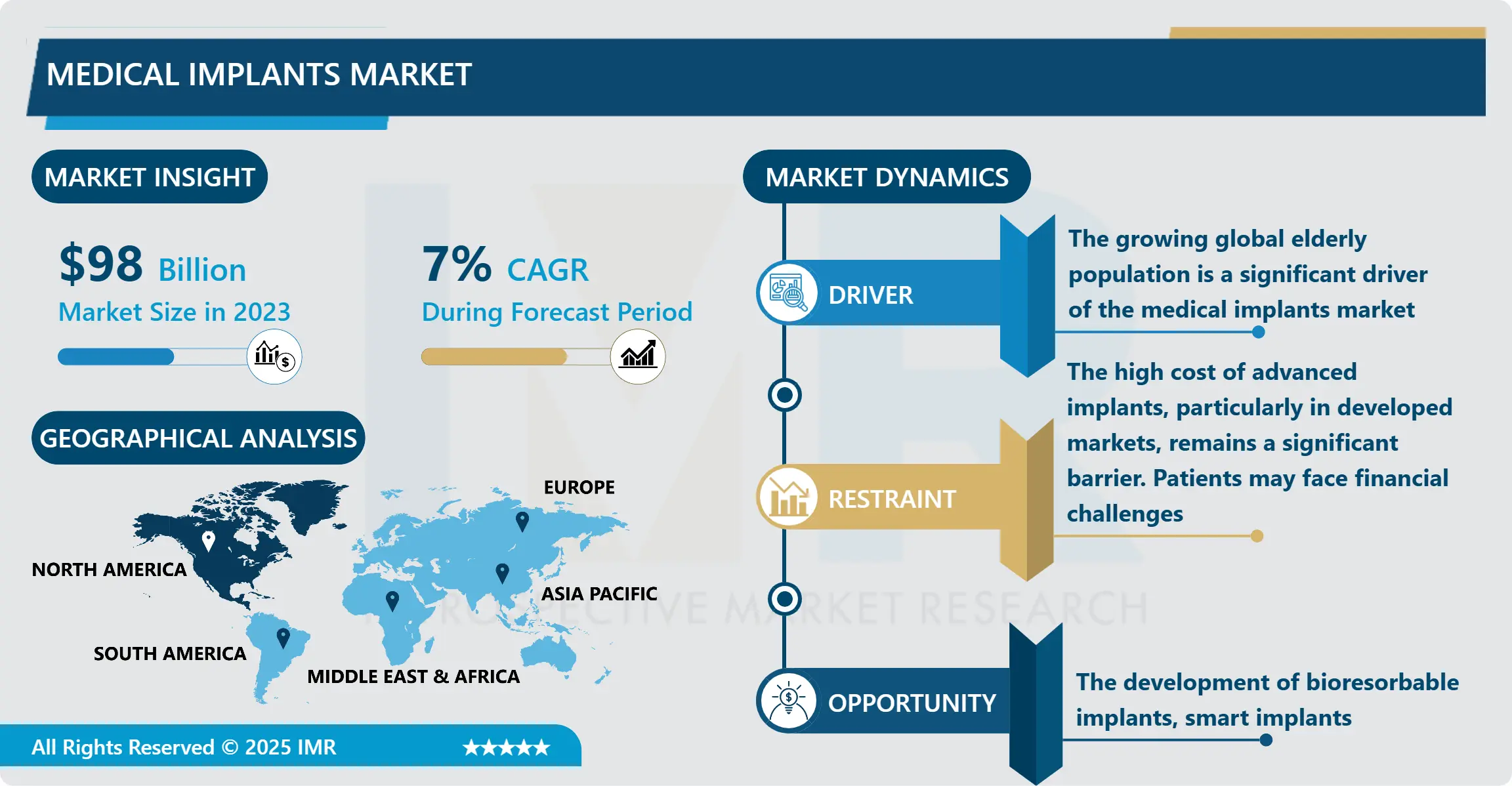

Medical Implants Market Size Was Valued at USD 98 Billion in 2023, and is Projected to Reach USD 199 Billion by 2032, Growing at a CAGR of 7% From 2024-2032.

This paper defines the medical implants market as the healthcare industry sub-sector that deals with the production and marketing of such medical devices that are intended to be implanted or placed inside the human body for the repair of tissues or organs. The implants are employed in cardiovascular, orthopedic, neurostimulation, spinal, ophthalmic, facial, dental, as well as breast surgery and any other field that may require an implant. These implants may be produced from a variety of biomaterials including ceramics, metals, polymers, and naturally occurring substances, all of which are chosen based on compatibility with the tissues of the human body, the ability to bear mechanical forces, their stability in the human body and their use in the body. New technologies and materials science have increased the opportunities for growth in the market for medical implants based on the increase in the incidence of chronic diseases, an increase in the average age of the population, the development of technologies for minimally invasive surgery and the use of 3D printing and bioengineering. The market also creates more effective and long-lasting solutions due to better implant design, individual approach, and better surgical intervention. Despite the higher costs, regulatory issues, and questions about the durability and biocompatibility of the longer devices, there are specific constraints still have an impact on market development. In general, the market for medical implant products is relevant to the development of healthcare all over the world and will only strengthen in the future in response to the focus on individualized, precision medicine.

Medical implants is an exciting segment in the healthcare industry experiencing growth globally due to increasing technological development, growing population, especially the older people, and the increased need for minimally invasive practices. Medical implants are medical devices intended to help restore or replace parts of the body that are either damaged or missing and include; cardiovascular implants like stents and heart valves, orthopedic implants like joint replacements and bone screws, neurostimulators, spinal implants, dental implants, breast implants and many others. These implants are intended for improvement of the quality of life of patients with chronic diseases, or those, who have injuries or congenital anomalies. The athinodization associated with the need to exhibit enhanced patient outcomes has made implant material that provide enhanced biocompatibility, durability and performance include ceramics, metals, polymers and all natural implant materials. Moreover, implement through 3D printing, individualized implant items and bioengineering technologies is improving the accuracy and performance of implants and thus earlier mentioned issues.

The increase in a number of medical implants is also attributed to a rising incidence of non-communicable diseases worldwide such as cardiovascular diseases, diabetes and musculoskeletal disorders charactersing a need for implants as well as surgeries. It is now apparent that there will always be a large number of elderly people in society today hence the need to have implants that are used in dealing with age related disorders such as joint diseases and bone fractures. However, the market should not be without challenges and that is why this research will explore the???However, the market should not be without challenges and that is why this research will explore the various challenges faced. Challenges include regulatory barriers, high costs associated with the production of the improved implants, other risks associated with different implant materiality both in the short-run and long-run. Furthermore, implant competition has heated up significantly because the leading brands continue to pump money into research in order to sustain an edge in a constantly evolving market. Nonetheless, the global medical implants market is anticipated to grow steadily due of constant advancements in biomaterials, production techniques, and surgical procedures; growth in a patient-centered model of care; and enhanced recovery results.

Medical Implants Market Trend Analysis:

3D Printing and Customization Revolutionize the Medical Implants Industry

-

The application of 3D printing technology in medical implants has revolutionized a number of ways in which implants are designed, produced and customized to meet specific requirements of the user. Conventional manufacturing techniques used in the production of implants does not fit the patient’s anatomy in this way as 3D printing allows the creation of implants that suits the specific patient in detail. This capability is very notable in surgeries like joint replacements, spine fixations, and cranial and facial restorations which require a nearly flawless fit of the implant for the likely success of the operation as well as future outcomes. By directly 3D printing such implants, there not only is better fit and comfort due to manufacture in a custom size, shape, and for functional load, but the risk of weak implants or failure, or having to revise the implants, is decreased. It is a general advantage because such customization maximizes the patient/implant compatibility as well as addresses individual medical conditions to make procedures work better and even reduce recovery time.

- Thus, beside increasing customizational capabilities, 3D printing helps create solutions which would be rather challenging to manufacture utilizing regular approaches. For instance, implants with open porous structures that help them bond closely with the adjoining bone can now be made with greater ease in terms of manufacturing, thereby resulting in faster healing and implant stability. Additionally, the technology of 3D printing helps increase the speed of producing both – the required medical implants and prototypes of new products altogether. Such an advancement is shaping the development of bio-printing and bio-compitable materials that can pave way for more advanced implant technologies especially in orthopedic, dental, and vascular specialties in the market. With the advancement in technology and material science it can be confidently stated that role of 3D printing in manufacturing cheap and customized medical implants for patients all over the world will keep on increasing.

Aging Population Creates Lucrative Market for Joint and Spinal Implants

-

The increase in average life span across the global populace offers the opportunity for growth within the medical implants sphere especially with regards to joint and spinal implants. With an increase in age, musculoskeletal disorders embrace osteoarthritis, degenerative disc disease, and spondylosis are more common. These conditions most times call for surgery hence increased demand of joint replacements (hip, knee, shoulder) and spinal implants (interbody cages, spinal rods, fusions devices). Arthritis and the increasing frequency of falls and consequent fractures in geriatrics patients are demanding a healthy application of implants to rehabilitate people for painless and productive lives. Also, disorders such as osteoporosis which make bones brittle and cause high incidences of fractures are raising the demand for orthopedic and spinal implants with greater stability and longevity.

- As the global population of the group of people with 65 years and older continues to grow, especially in North America, Europe and some parts of Asia-Pacific, there is anticipated rise in the uptake of age related treatments. The older persons are more inclined to receive surgical operations for such ailments as hip replacements, knee replacements as well as spinal fusion making the market for such implant more profitable for the manufacturers. However, benefits attained with improved implant materials and surgical procedures, including laparoscopic surgeries, and biocompatibility are enhancing patient results, decreasing patience’s healing period and expanding surgeries access. Currently, most healthcare organisations orient on better management of chronic diseases and cost reduction of long term care, which also means the focus on enhancing the quality of joints and spinal implants, it remains the main area where the medical implant market can develop qualitatively and expand further.

Medical Implants Market Segment Analysis:

Medical Implants Market is Segmented on the basis of type, Biomaterial, and Region

By Type, Orthopedic implants segment is expected to dominate the market during the forecast period

-

The orthopaedic implants segment is expected to experience high growth in the medical implants market throughout the forecast period due to many factors the worldwide increase in the geriatric population, rising incidences of chronic musculoskeletal diseases, and the increasing number of joint replacement & spinal surgeries across the world. Osteoarthritis, degenerative disc disease, and fracture are common in the elderly; these diseases are directly related to the aging process; thus as age increases the prevalence of the diseases also rises. Arthroplasties that are knee and hip replacements, spinal fusions, and shoulder replacements are on the rise as options for these diseases. These implants enhance mobility and relieve pain, and should remain fundamental to health management delivery for elderly persons within healthcare system plans. In addition, sustainability of delicate surgeries by employing minimally invasive techniques among others are also contributing to the growth of the orthopedic implant market: these innovations have enhanced implant designs and materials to produce better patient outcomes that are also faster recovery times.

- However, it is worth noting that apart from aging the trauma biology, sports injuries and spinal problems significantly fuel the demand for orthopedic implants. Other applications include spinal implants; interbody fusion devices, rods, and screws are expected to record higher growth because most people are complaining of back aches attributable to aging, lifestyle, and work-related stress. The ongoing trend to make procedures more delicate since it enables specific operations with a shorter post-surgery recover increases the need for orthopedic implants. Additionally, the progress in individualized implants design – patient-specific implant based on 3D printing – and application of sophisticated materials, namely, titanium alloys, polyethylene and bioactive ceramics widen the possibilities and outcomes of orthopedic implantations. Combined, these aspects make the orthopedic implants segment to be the key driver of the market; growth is expected as healthcare systems enhance, surgery enhancement and emerging necessity of orthopedic solutions.

By Biomateria, Metallic material segment expected to held the largest share

-

Metallic materials are expected to dominate the Medical Implants market in the forecast period as it is known for mechanical properties, high strength and good biocompatibility. Titanium, stainless steel and cobal-chromium alloys are common materials used in numerous medical implants including joint replacements and spinal implants, stents and even heart valves and dental implants. These materials can be easily selected because of their high strength to weight ratio, fatigue endurance and capability of handling high mechanical loads which implants experience in the body. Out of all the materials, titanium has been most recommended for use in joint replacement operations because it is resistant to corrosion, lightweight and easily forms an integrate structure with bone tissue. These characteristic therefore facilitates the prospects of metallic implants rendering them resistant to breakdown making them dominant in the market.

- Besides their advantages in structure, metallic implants are preferred for their simple process of fabrication as well as the precise manufacturing, which can be useful in spinal and cardiovascular operations. It is only possible with metal alloys to fine-tune properties enabling the device to be then used for implantation, to be strong and elastic, and to not provoke adverse effects from the body. The increasing need for less invasive surgeries, and new methods of robot-assisted surgeries also serves as a boost in the utilization of metallic materials because of their fine structure suitable when used in such operations. In addition, growing advances in bioactive metallic materials, which stimulate bone growth in the region of the implant, and decrease chances of rejection, are broadening metal uses to include areas such as bone grafting as well as dental implantation. Due to their generality, stability, and performance history, metallic biomaterials will continue to predominate the market and be the first choice for a majority of the total medical implants as surgical procedures and implant structures enhance.

Medical Implants Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

-

Out of all the regions, North America will continue to hold the largest share of medical implants market throughout the forecast period for several reasons; superior healthcare facilities, rising healthcare expenditure and the higher incidence of chronic diseases due to the increasing elderly population. First of all, the healthcare industry in the United States is most advanced in the world with additional infrastructure facilities of top medical technologies, adequately trained human resources involved in the sector including medical device manufacturing firms. With an aging population, there is an increasing need for use of femoral stems which are used in orthopedic applications, card cages used in cardiovascular and orthopedic applications, spinal implants and dental implants. Aging population in North America prefer joint replacements, spinal fusion, and heart valve replacement making the implantable devices more in demand. In addition, reimbursement policies are stable, and high levels of government support for healthcare development also contribute to the wide usage of modern healthcare technologies.

- In addition to these demographic factors, innovations in the implant technology, material used in implants, and advancement in techniques in implantology also contributes to market expand in North America. Increasing use of minimally invasive surgical procedures, the use of innovative technologies such as 3D printing for fabrication of customized implants, and the introduction of implantable devices with in-built sensors for monitoring of patients after surgery are leading to increased implantation across multiple medical specialties. North America also continues to be an important location for innovation in the medical implant industry with key players consisting of undertakings being undertaken in the development of more effective implantable products. Requirements for the sale of these devices are well established in the region thus promoting more investment and growth of the market. In addition, the growing emphasis on a preventative approach and long-term conditions in the area is driving surgery, specifically in the orthopaedics and cardiovascular sectors, where implants are especially significant. These factors put North America in a strategic to retain the largest share of the medical implants market by the end of the foreseen period.

Active Key Players in the Medical Implants Market:

-

Abbott Laboratories (USA)

- B. Braun Melsungen AG (Germany)

- Biomet, Inc. (USA)

- Boston Scientific Corporation (USA)

- Dentsply Sirona Inc. (USA)

- DePuy Synthes (USA) (a subsidiary of Johnson & Johnson)

- Heraeus Holding GmbH (Germany)

- Implant Direct (USA)

- Johnson & Johnson Services, Inc. (USA)

- Medtronic PLC (Ireland)

- NuVasive, Inc. (USA)

- Orthofix Medical, Inc. (USA)

- Osstem Implant Co., Ltd. (South Korea)

- Smith & Nephew plc (UK)

- Straumann Holding AG (Switzerland)

- Stryker Corporation (USA)

- Zimmer Biomet (USA)

- Zimmer Biomet Holdings, Inc. (USA)

- Other Active Players

|

Medical Implants Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 98 Billion |

|

Forecast Period 2024-32 CAGR: |

7 % |

Market Size in 2032: |

USD 199 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Biomaterial |

|

||

|

By Region

|

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Medical Implants Market by Product Type

4.1 Medical Implants Market Snapshot and Growth Engine

4.2 Medical Implants Market Overview

4.3 Cardiovascular

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.3.3 Key Market Trends, Growth Factors and Opportunities

4.3.4 Cardiovascular: Geographic Segmentation Analysis

4.4 Orthopedic

4.4.1 Introduction and Market Overview

4.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.4.3 Key Market Trends, Growth Factors and Opportunities

4.4.4 Orthopedic: Geographic Segmentation Analysis

4.5 Neurostimulators

4.5.1 Introduction and Market Overview

4.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.5.3 Key Market Trends, Growth Factors and Opportunities

4.5.4 Neurostimulators: Geographic Segmentation Analysis

4.6 Spinal

4.6.1 Introduction and Market Overview

4.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.6.3 Key Market Trends, Growth Factors and Opportunities

4.6.4 Spinal: Geographic Segmentation Analysis

4.7 Ophthalmic

4.7.1 Introduction and Market Overview

4.7.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.7.3 Key Market Trends, Growth Factors and Opportunities

4.7.4 Ophthalmic: Geographic Segmentation Analysis

4.8 Facial

4.8.1 Introduction and Market Overview

4.8.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.8.3 Key Market Trends, Growth Factors and Opportunities

4.8.4 Facial: Geographic Segmentation Analysis

4.9 Dental

4.9.1 Introduction and Market Overview

4.9.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.9.3 Key Market Trends, Growth Factors and Opportunities

4.9.4 Dental: Geographic Segmentation Analysis

4.10 Breast

4.10.1 Introduction and Market Overview

4.10.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.10.3 Key Market Trends, Growth Factors and Opportunities

4.10.4 Breast: Geographic Segmentation Analysis

Chapter 5: Medical Implants Market by Biomaterial

5.1 Medical Implants Market Snapshot and Growth Engine

5.2 Medical Implants Market Overview

5.3 Ceramic

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.3.3 Key Market Trends, Growth Factors and Opportunities

5.3.4 Ceramic: Geographic Segmentation Analysis

5.4 Metallic

5.4.1 Introduction and Market Overview

5.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.4.3 Key Market Trends, Growth Factors and Opportunities

5.4.4 Metallic: Geographic Segmentation Analysis

5.5 Polymers

5.5.1 Introduction and Market Overview

5.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.5.3 Key Market Trends, Growth Factors and Opportunities

5.5.4 Polymers: Geographic Segmentation Analysis

5.6 Natural

5.6.1 Introduction and Market Overview

5.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.6.3 Key Market Trends, Growth Factors and Opportunities

5.6.4 Natural: Geographic Segmentation Analysis

Chapter 6: Company Profiles and Competitive Analysis

6.1 Competitive Landscape

6.1.1 Competitive Benchmarking

6.1.2 Medical Implants Market Share by Manufacturer (2023)

6.1.3 Industry BCG Matrix

6.1.4 Heat Map Analysis

6.1.5 Mergers and Acquisitions

6.2 ABBOTT LABORATORIES (USA)

6.2.1 Company Overview

6.2.2 Key Executives

6.2.3 Company Snapshot

6.2.4 Role of the Company in the Market

6.2.5 Sustainability and Social Responsibility

6.2.6 Operating Business Segments

6.2.7 Product Portfolio

6.2.8 Business Performance

6.2.9 Key Strategic Moves and Recent Developments

6.2.10 SWOT Analysis

6.3 B. BRAUN MELSUNGEN AG (GERMANY)

6.4 BIOMET INC. (USA)

6.5 BOSTON SCIENTIFIC CORPORATION (USA)

6.6 DENTSPLY SIRONA INC. (USA)

6.7 DEPUY SYNTHES (USA

6.8 A SUBSIDIARY OF JOHNSON & JOHNSON)

6.9 HERAEUS HOLDING GMBH (GERMANY)

6.10 IMPLANT DIRECT (USA)

6.11 JOHNSON & JOHNSON SERVICES INC. (USA)

6.12 MEDTRONIC PLC (IRELAND)

6.13 AND NUVASIVE INC. (USA)

6.14 OTHER ACTIVE PLAYERS

Chapter 7: Global Medical Implants Market By Region

7.1 Overview

7.2. North America Medical Implants Market

7.2.1 Key Market Trends, Growth Factors and Opportunities

7.2.2 Top Key Companies

7.2.3 Historic and Forecasted Market Size by Segments

7.2.4 Historic and Forecasted Market Size By Product Type

7.2.4.1 Cardiovascular

7.2.4.2 Orthopedic

7.2.4.3 Neurostimulators

7.2.4.4 Spinal

7.2.4.5 Ophthalmic

7.2.4.6 Facial

7.2.4.7 Dental

7.2.4.8 Breast

7.2.5 Historic and Forecasted Market Size By Biomaterial

7.2.5.1 Ceramic

7.2.5.2 Metallic

7.2.5.3 Polymers

7.2.5.4 Natural

7.2.6 Historic and Forecast Market Size by Country

7.2.6.1 US

7.2.6.2 Canada

7.2.6.3 Mexico

7.3. Eastern Europe Medical Implants Market

7.3.1 Key Market Trends, Growth Factors and Opportunities

7.3.2 Top Key Companies

7.3.3 Historic and Forecasted Market Size by Segments

7.3.4 Historic and Forecasted Market Size By Product Type

7.3.4.1 Cardiovascular

7.3.4.2 Orthopedic

7.3.4.3 Neurostimulators

7.3.4.4 Spinal

7.3.4.5 Ophthalmic

7.3.4.6 Facial

7.3.4.7 Dental

7.3.4.8 Breast

7.3.5 Historic and Forecasted Market Size By Biomaterial

7.3.5.1 Ceramic

7.3.5.2 Metallic

7.3.5.3 Polymers

7.3.5.4 Natural

7.3.6 Historic and Forecast Market Size by Country

7.3.6.1 Russia

7.3.6.2 Bulgaria

7.3.6.3 The Czech Republic

7.3.6.4 Hungary

7.3.6.5 Poland

7.3.6.6 Romania

7.3.6.7 Rest of Eastern Europe

7.4. Western Europe Medical Implants Market

7.4.1 Key Market Trends, Growth Factors and Opportunities

7.4.2 Top Key Companies

7.4.3 Historic and Forecasted Market Size by Segments

7.4.4 Historic and Forecasted Market Size By Product Type

7.4.4.1 Cardiovascular

7.4.4.2 Orthopedic

7.4.4.3 Neurostimulators

7.4.4.4 Spinal

7.4.4.5 Ophthalmic

7.4.4.6 Facial

7.4.4.7 Dental

7.4.4.8 Breast

7.4.5 Historic and Forecasted Market Size By Biomaterial

7.4.5.1 Ceramic

7.4.5.2 Metallic

7.4.5.3 Polymers

7.4.5.4 Natural

7.4.6 Historic and Forecast Market Size by Country

7.4.6.1 Germany

7.4.6.2 UK

7.4.6.3 France

7.4.6.4 The Netherlands

7.4.6.5 Italy

7.4.6.6 Spain

7.4.6.7 Rest of Western Europe

7.5. Asia Pacific Medical Implants Market

7.5.1 Key Market Trends, Growth Factors and Opportunities

7.5.2 Top Key Companies

7.5.3 Historic and Forecasted Market Size by Segments

7.5.4 Historic and Forecasted Market Size By Product Type

7.5.4.1 Cardiovascular

7.5.4.2 Orthopedic

7.5.4.3 Neurostimulators

7.5.4.4 Spinal

7.5.4.5 Ophthalmic

7.5.4.6 Facial

7.5.4.7 Dental

7.5.4.8 Breast

7.5.5 Historic and Forecasted Market Size By Biomaterial

7.5.5.1 Ceramic

7.5.5.2 Metallic

7.5.5.3 Polymers

7.5.5.4 Natural

7.5.6 Historic and Forecast Market Size by Country

7.5.6.1 China

7.5.6.2 India

7.5.6.3 Japan

7.5.6.4 South Korea

7.5.6.5 Malaysia

7.5.6.6 Thailand

7.5.6.7 Vietnam

7.5.6.8 The Philippines

7.5.6.9 Australia

7.5.6.10 New Zealand

7.5.6.11 Rest of APAC

7.6. Middle East & Africa Medical Implants Market

7.6.1 Key Market Trends, Growth Factors and Opportunities

7.6.2 Top Key Companies

7.6.3 Historic and Forecasted Market Size by Segments

7.6.4 Historic and Forecasted Market Size By Product Type

7.6.4.1 Cardiovascular

7.6.4.2 Orthopedic

7.6.4.3 Neurostimulators

7.6.4.4 Spinal

7.6.4.5 Ophthalmic

7.6.4.6 Facial

7.6.4.7 Dental

7.6.4.8 Breast

7.6.5 Historic and Forecasted Market Size By Biomaterial

7.6.5.1 Ceramic

7.6.5.2 Metallic

7.6.5.3 Polymers

7.6.5.4 Natural

7.6.6 Historic and Forecast Market Size by Country

7.6.6.1 Turkiye

7.6.6.2 Bahrain

7.6.6.3 Kuwait

7.6.6.4 Saudi Arabia

7.6.6.5 Qatar

7.6.6.6 UAE

7.6.6.7 Israel

7.6.6.8 South Africa

7.7. South America Medical Implants Market

7.7.1 Key Market Trends, Growth Factors and Opportunities

7.7.2 Top Key Companies

7.7.3 Historic and Forecasted Market Size by Segments

7.7.4 Historic and Forecasted Market Size By Product Type

7.7.4.1 Cardiovascular

7.7.4.2 Orthopedic

7.7.4.3 Neurostimulators

7.7.4.4 Spinal

7.7.4.5 Ophthalmic

7.7.4.6 Facial

7.7.4.7 Dental

7.7.4.8 Breast

7.7.5 Historic and Forecasted Market Size By Biomaterial

7.7.5.1 Ceramic

7.7.5.2 Metallic

7.7.5.3 Polymers

7.7.5.4 Natural

7.7.6 Historic and Forecast Market Size by Country

7.7.6.1 Brazil

7.7.6.2 Argentina

7.7.6.3 Rest of SA

Chapter 8 Analyst Viewpoint and Conclusion

8.1 Recommendations and Concluding Analysis

8.2 Potential Market Strategies

Chapter 9 Research Methodology

9.1 Research Process

9.2 Primary Research

9.3 Secondary Research

|

Medical Implants Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 98 Billion |

|

Forecast Period 2024-32 CAGR: |

7 % |

Market Size in 2032: |

USD 199 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Biomaterial |

|

||

|

By Region

|

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||