Medical Device Testing Market Synopsis

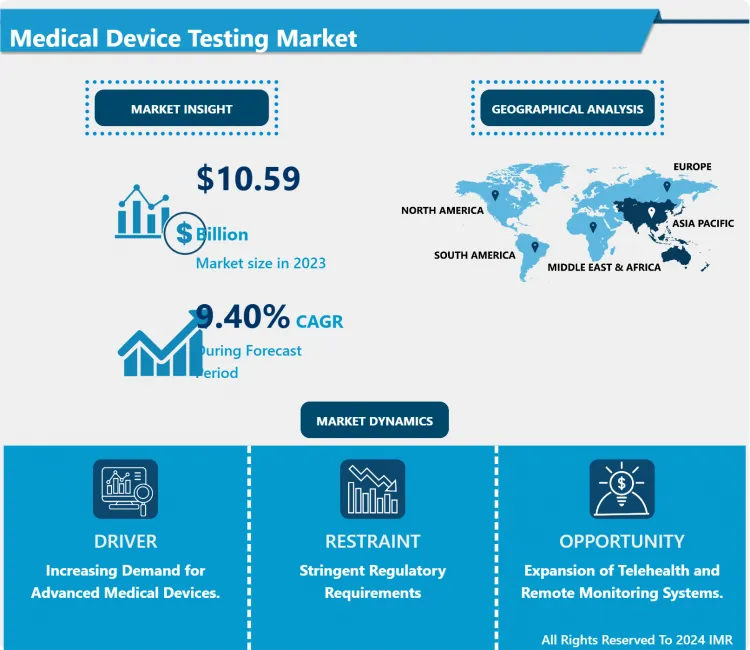

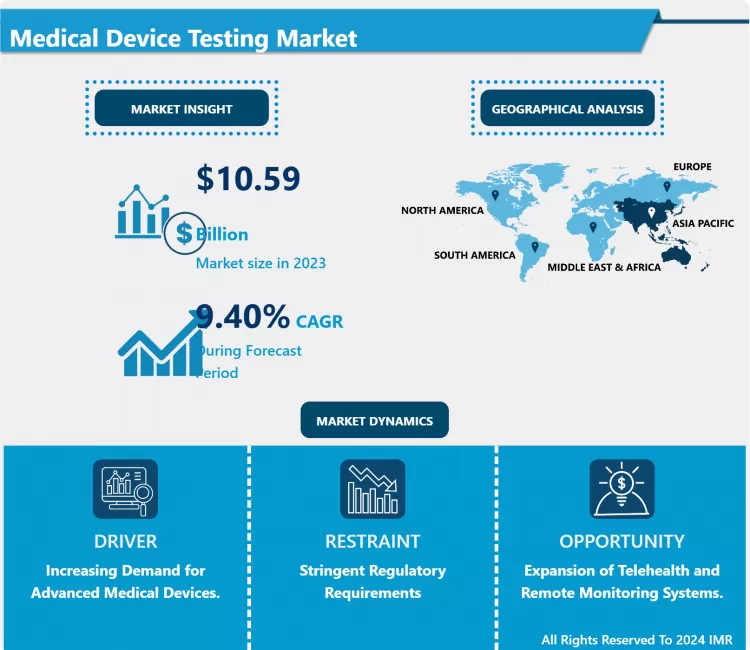

Medical Device Testing Market Size is Valued at USD 10.59 Billion in 2023 and is Projected to Reach USD 23.81 Billion by 2032, Growing at a CAGR of 9.40% From 2024-2032.

The Medical Device Testing Market includes solutions and activities aimed at assessing and verifying medical devices’ reliability and conformity with the required standards. This market comprises performance testing, safety testing, and biocompatibility testing with very wide applicability across diverse diagnostic, therapeutic, and monitoring devices. It is a process done by manufacturers of medical devices, research companies, hospitals, and other facilities to fulfil the requirements in the legal norms and the increase of dependability. This has been brought by increase in use of associated medical technology, increased regulation on the medical devices, and increase market demand of newer and better medical gadgets.

- The prime load drivers of the global Medical Device Testing Market include the growing regulatory compliances and high safety and effectiveness norms for the medical devices. With an increase in innovation and the enhancements in various aspects of medical devices, most of the organizations such as FDA (Food and Drug Administration), EMA (European Medicines Agency) and ISO (International Organization for Standardization) have set various exam and approvals to warrant for its safety, reliability and functionality. This pressure creates the need to perform various tests to meet the set standards, thus increasing the market for specialized testing.

- Moreover, increase in incidence of chronic diseases and the global population’s aging are increasing the requirement for new-generation medical devices that, in turn, are driving the testing services market for medical devices. In addition, progress in technology is clearly seen in the growth of the market due to incorporation of digital health as wears well as other devices while new methods and protocols are carried out for testing. Some of the prime reasons that are causing the Medical Device Testing Market to unfold are the constant advancements of medical technologies and the necessity to preserve and achieve high quality and safety standards.

Medical Device Testing Market Trend Analysis

How Telemedicine is Influencing the Medical Device Testing Market

- The demand of medical device testing market is growing continually due to the development of advanced features in medical devices and rigorous standards set by the health agencies. New tools and software including the AI and machine learning are progressively improving the testing methods and processes. Such a trend results in advanced testing solutions regarding performance, safety, and biocompatibility, which are critical factors to make new and inspiring medical devices efficient and reliable.

- Further, there has been increased awareness on the application of personalization in the medical sector and advancement in health monitoring gadgets leading to the need for testing specialist services in the market. Even in telemedicine services and remote monitoring devices there is the need to do several tests to determine the level of safety or effectiveness of the developed technologies within certain circumstances. Due to the competition and growth of requirements and standards in the health and medical device industry, manufacturers are relying more on sophisticated testing techniques and outsourcing such testing services.

Advancements and Opportunities in the Medical Device Testing Market

- The Medical Device Testing Market is characterized by significant opportunities because of the ongoing growth of technology and focus on safety and compliance. Poppel Siegel 2001 believes that as medical devices become ‘smarter’ there is need to do extensive tests so that one can be sure of the device’s performance, safety and effectiveness. This is compounded by new and more stringent rules affixed by health-enforcing bodies worldwide resulting into a large market for testing solutions across the various device types and uses. New directions in healthcare products, especially in wearable solutions, modern practices like the administration of individualized medicine or minimally invasive procedures, are considered to be the growth opportunities for the market players as they create demand for selective testing solutions.

- Moreover, the enhancement of healthcare facilities in up-and-coming global markets and increasing incidence of lifestyle diseases is driving the demand for innovative medical devices, consequently the necessity for elaborate testing services. Patients’ safety concerns and the need to fulfill the international requirements for the certification of devices prompt the manufacturers to spend much on testing strategies. This environment gives a chance to both, traditional testing companies and new entrants that can introduce new testing solutions, utilize progressive technologies, and develop more extensive service portfolios as the medical device industry’s needs change.

Medical Device Testing Market Segment Analysis:

Medical Device Testing Market Segmented on the basis of Testing Type, Device Type, Application and End User.

By Testing Type, Performance Testing segment is expected to dominate the market during the forecast period

- However, it is significant to understand that the Medical Device Testing Market comprises performance Testing, required Testing for Safety of the users, and Testing of how Medical Devices interact with the biological system. Sterilization validation confirms that a device complies with the sterilization processes and electrical safety testing is used where there are potential risks associated with electrical parts of the device. Environmental testing evaluates how a device performs under various environmental conditions, while other test kinds are not sorted under the primary categories.

By Application, Cardiovascular segment held the largest share in 2024

- The Medical Device Testing Market has various applications is some of these are cardiovascular devices include those used in diagnosis or treatment of heart related diseases; respiratory devices that are used in diagnosing and treating lung and breathing related issues; and orthopedic devices are used in provision of skeletal support and repair. They also include neurological devices for neurological diseases, oncology devices for diagnosis and management of cancers, and urological devices for genitourinary conditions. Moreover, testing services include other separate categories that are not included in these main ones, but perform specific functions.

Medical Device Testing Market Regional Insights:

Asia Pacific is Expected to Dominate the Market Over the Forecast period

- The testing of medical devices has been steadily increasing in Asia-Pacfic market especially due to expansion of healthcare facilities, growth in expenditure on healthcare, and shifting concern towards the safety and performance of the medical devices. Leaders are countries like China, India, and Japan which are doing a lot of investment on advanced testing technologies and facilities to fulfill new demands of qualified medical devices. The emerging population of the region along with the increasing cases of chronic disease is additionally establishing a significance for efficient medical device testing to meet international standards and patient safety.

- Moreover, the APAC market has been strengthened by the favourable policies and legislative framework along with the growing affiliations between the medical device makers and CROs. Among the reasons that have led to the growth of the market, one can uncover the transition to higher requirements and standards, the use of innovative approaches in the framework of testing methodologies. Further, the medical device testing activities are rising in the emerging countries within the region as they are integrating themselves to the international markets.

Active Key Players in the Medical Device Testing Market

- SGS SA (Switzerland)

- TÜV SÜD (Germany)

- Intertek Group plc (United Kingdom)

- Bureau Veritas (France)

- UL LLC (United States)

- NSF International (United States)

- Eurofins Scientific (Luxembourg)

- DEKRA SE (Germany)

- MDSAP (Medical Device Single Audit Program) Registrars (Multiple countries)

- AEMTEK, Inc. (United States)

- Medpace, Inc. (United States)

- Certify Global (United States)

- Pall Corporation (United States)

- Kiwa Group (Netherlands)

- Emerson Electric Co. (United States)

- Others

|

Global Medical Device Testing Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 10.59 Bn. |

|

Forecast Period 2024-32 CAGR: |

9.42 % |

Market Size in 2032: |

USD 23.81 Bn. |

|

Segments Covered: |

By Testing Type |

|

|

|

By Device Type |

|

||

|

By Application |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Medical Device Testing Market by Testing Type (2018-2032)

4.1 Medical Device Testing Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Performance Testing

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Safety Testing

4.5 Biocompatibility Testing

4.6 Sterilization Validation

4.7 Electrical Safety Testing

4.8 Environmental Testing

4.9 Others

Chapter 5: Medical Device Testing Market by Device Type (2018-2032)

5.1 Medical Device Testing Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Diagnostic Devices

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Therapeutic Devices

5.5 Monitoring Devices

5.6 Surgical Instruments

5.7 Orthopedic Devices

5.8 Neurological Devices

5.9 Others

Chapter 6: Medical Device Testing Market by Application (2018-2032)

6.1 Medical Device Testing Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Cardiovascular

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Respiratory

6.5 Orthopedics

6.6 Neurology

6.7 Oncology

6.8 Urology

6.9 Others

Chapter 7: Medical Device Testing Market by End User (2018-2032)

7.1 Medical Device Testing Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Medical Device Manufacturers

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Contract Research Organizations (CROs)

7.5 Hospitals

7.6 Diagnostic Laboratories

7.7 Research Institutions

7.8 Others

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Medical Device Testing Market Share by Manufacturer (2024)

8.1.3 Industry BCG Matrix

8.1.4 Heat Map Analysis

8.1.5 Mergers and Acquisitions

8.2 SGS SA (SWITZERLAND)

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Key Strategic Moves and Recent Developments

8.2.10 SWOT Analysis

8.3 TÜV SÜD (GERMANY)

8.4 INTERTEK GROUP PLC (UNITED KINGDOM)

8.5 BUREAU VERITAS (FRANCE)

8.6 UL LLC (UNITED STATES)

8.7 NSF INTERNATIONAL (UNITED STATES)

8.8 EUROFINS SCIENTIFIC (LUXEMBOURG)

8.9 DEKRA SE (GERMANY)

8.10 MDSAP (MEDICAL DEVICE SINGLE AUDIT PROGRAM) REGISTRARS (MULTIPLE COUNTRIES)

8.11 AEMTEK INC. (UNITED STATES)

8.12 MEDPACE INC. (UNITED STATES)

8.13 CERTIFY GLOBAL (UNITED STATES)

8.14 PALL CORPORATION (UNITED STATES)

8.15 KIWA GROUP (NETHERLANDS)

8.16 EMERSON ELECTRIC CO. (UNITED STATES)

8.17 OTHERS

8.18

8.19

Chapter 9: Global Medical Device Testing Market By Region

9.1 Overview

9.2. North America Medical Device Testing Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecasted Market Size by Testing Type

9.2.4.1 Performance Testing

9.2.4.2 Safety Testing

9.2.4.3 Biocompatibility Testing

9.2.4.4 Sterilization Validation

9.2.4.5 Electrical Safety Testing

9.2.4.6 Environmental Testing

9.2.4.7 Others

9.2.5 Historic and Forecasted Market Size by Device Type

9.2.5.1 Diagnostic Devices

9.2.5.2 Therapeutic Devices

9.2.5.3 Monitoring Devices

9.2.5.4 Surgical Instruments

9.2.5.5 Orthopedic Devices

9.2.5.6 Neurological Devices

9.2.5.7 Others

9.2.6 Historic and Forecasted Market Size by Application

9.2.6.1 Cardiovascular

9.2.6.2 Respiratory

9.2.6.3 Orthopedics

9.2.6.4 Neurology

9.2.6.5 Oncology

9.2.6.6 Urology

9.2.6.7 Others

9.2.7 Historic and Forecasted Market Size by End User

9.2.7.1 Medical Device Manufacturers

9.2.7.2 Contract Research Organizations (CROs)

9.2.7.3 Hospitals

9.2.7.4 Diagnostic Laboratories

9.2.7.5 Research Institutions

9.2.7.6 Others

9.2.8 Historic and Forecast Market Size by Country

9.2.8.1 US

9.2.8.2 Canada

9.2.8.3 Mexico

9.3. Eastern Europe Medical Device Testing Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecasted Market Size by Testing Type

9.3.4.1 Performance Testing

9.3.4.2 Safety Testing

9.3.4.3 Biocompatibility Testing

9.3.4.4 Sterilization Validation

9.3.4.5 Electrical Safety Testing

9.3.4.6 Environmental Testing

9.3.4.7 Others

9.3.5 Historic and Forecasted Market Size by Device Type

9.3.5.1 Diagnostic Devices

9.3.5.2 Therapeutic Devices

9.3.5.3 Monitoring Devices

9.3.5.4 Surgical Instruments

9.3.5.5 Orthopedic Devices

9.3.5.6 Neurological Devices

9.3.5.7 Others

9.3.6 Historic and Forecasted Market Size by Application

9.3.6.1 Cardiovascular

9.3.6.2 Respiratory

9.3.6.3 Orthopedics

9.3.6.4 Neurology

9.3.6.5 Oncology

9.3.6.6 Urology

9.3.6.7 Others

9.3.7 Historic and Forecasted Market Size by End User

9.3.7.1 Medical Device Manufacturers

9.3.7.2 Contract Research Organizations (CROs)

9.3.7.3 Hospitals

9.3.7.4 Diagnostic Laboratories

9.3.7.5 Research Institutions

9.3.7.6 Others

9.3.8 Historic and Forecast Market Size by Country

9.3.8.1 Russia

9.3.8.2 Bulgaria

9.3.8.3 The Czech Republic

9.3.8.4 Hungary

9.3.8.5 Poland

9.3.8.6 Romania

9.3.8.7 Rest of Eastern Europe

9.4. Western Europe Medical Device Testing Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecasted Market Size by Testing Type

9.4.4.1 Performance Testing

9.4.4.2 Safety Testing

9.4.4.3 Biocompatibility Testing

9.4.4.4 Sterilization Validation

9.4.4.5 Electrical Safety Testing

9.4.4.6 Environmental Testing

9.4.4.7 Others

9.4.5 Historic and Forecasted Market Size by Device Type

9.4.5.1 Diagnostic Devices

9.4.5.2 Therapeutic Devices

9.4.5.3 Monitoring Devices

9.4.5.4 Surgical Instruments

9.4.5.5 Orthopedic Devices

9.4.5.6 Neurological Devices

9.4.5.7 Others

9.4.6 Historic and Forecasted Market Size by Application

9.4.6.1 Cardiovascular

9.4.6.2 Respiratory

9.4.6.3 Orthopedics

9.4.6.4 Neurology

9.4.6.5 Oncology

9.4.6.6 Urology

9.4.6.7 Others

9.4.7 Historic and Forecasted Market Size by End User

9.4.7.1 Medical Device Manufacturers

9.4.7.2 Contract Research Organizations (CROs)

9.4.7.3 Hospitals

9.4.7.4 Diagnostic Laboratories

9.4.7.5 Research Institutions

9.4.7.6 Others

9.4.8 Historic and Forecast Market Size by Country

9.4.8.1 Germany

9.4.8.2 UK

9.4.8.3 France

9.4.8.4 The Netherlands

9.4.8.5 Italy

9.4.8.6 Spain

9.4.8.7 Rest of Western Europe

9.5. Asia Pacific Medical Device Testing Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecasted Market Size by Testing Type

9.5.4.1 Performance Testing

9.5.4.2 Safety Testing

9.5.4.3 Biocompatibility Testing

9.5.4.4 Sterilization Validation

9.5.4.5 Electrical Safety Testing

9.5.4.6 Environmental Testing

9.5.4.7 Others

9.5.5 Historic and Forecasted Market Size by Device Type

9.5.5.1 Diagnostic Devices

9.5.5.2 Therapeutic Devices

9.5.5.3 Monitoring Devices

9.5.5.4 Surgical Instruments

9.5.5.5 Orthopedic Devices

9.5.5.6 Neurological Devices

9.5.5.7 Others

9.5.6 Historic and Forecasted Market Size by Application

9.5.6.1 Cardiovascular

9.5.6.2 Respiratory

9.5.6.3 Orthopedics

9.5.6.4 Neurology

9.5.6.5 Oncology

9.5.6.6 Urology

9.5.6.7 Others

9.5.7 Historic and Forecasted Market Size by End User

9.5.7.1 Medical Device Manufacturers

9.5.7.2 Contract Research Organizations (CROs)

9.5.7.3 Hospitals

9.5.7.4 Diagnostic Laboratories

9.5.7.5 Research Institutions

9.5.7.6 Others

9.5.8 Historic and Forecast Market Size by Country

9.5.8.1 China

9.5.8.2 India

9.5.8.3 Japan

9.5.8.4 South Korea

9.5.8.5 Malaysia

9.5.8.6 Thailand

9.5.8.7 Vietnam

9.5.8.8 The Philippines

9.5.8.9 Australia

9.5.8.10 New Zealand

9.5.8.11 Rest of APAC

9.6. Middle East & Africa Medical Device Testing Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecasted Market Size by Testing Type

9.6.4.1 Performance Testing

9.6.4.2 Safety Testing

9.6.4.3 Biocompatibility Testing

9.6.4.4 Sterilization Validation

9.6.4.5 Electrical Safety Testing

9.6.4.6 Environmental Testing

9.6.4.7 Others

9.6.5 Historic and Forecasted Market Size by Device Type

9.6.5.1 Diagnostic Devices

9.6.5.2 Therapeutic Devices

9.6.5.3 Monitoring Devices

9.6.5.4 Surgical Instruments

9.6.5.5 Orthopedic Devices

9.6.5.6 Neurological Devices

9.6.5.7 Others

9.6.6 Historic and Forecasted Market Size by Application

9.6.6.1 Cardiovascular

9.6.6.2 Respiratory

9.6.6.3 Orthopedics

9.6.6.4 Neurology

9.6.6.5 Oncology

9.6.6.6 Urology

9.6.6.7 Others

9.6.7 Historic and Forecasted Market Size by End User

9.6.7.1 Medical Device Manufacturers

9.6.7.2 Contract Research Organizations (CROs)

9.6.7.3 Hospitals

9.6.7.4 Diagnostic Laboratories

9.6.7.5 Research Institutions

9.6.7.6 Others

9.6.8 Historic and Forecast Market Size by Country

9.6.8.1 Turkiye

9.6.8.2 Bahrain

9.6.8.3 Kuwait

9.6.8.4 Saudi Arabia

9.6.8.5 Qatar

9.6.8.6 UAE

9.6.8.7 Israel

9.6.8.8 South Africa

9.7. South America Medical Device Testing Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecasted Market Size by Testing Type

9.7.4.1 Performance Testing

9.7.4.2 Safety Testing

9.7.4.3 Biocompatibility Testing

9.7.4.4 Sterilization Validation

9.7.4.5 Electrical Safety Testing

9.7.4.6 Environmental Testing

9.7.4.7 Others

9.7.5 Historic and Forecasted Market Size by Device Type

9.7.5.1 Diagnostic Devices

9.7.5.2 Therapeutic Devices

9.7.5.3 Monitoring Devices

9.7.5.4 Surgical Instruments

9.7.5.5 Orthopedic Devices

9.7.5.6 Neurological Devices

9.7.5.7 Others

9.7.6 Historic and Forecasted Market Size by Application

9.7.6.1 Cardiovascular

9.7.6.2 Respiratory

9.7.6.3 Orthopedics

9.7.6.4 Neurology

9.7.6.5 Oncology

9.7.6.6 Urology

9.7.6.7 Others

9.7.7 Historic and Forecasted Market Size by End User

9.7.7.1 Medical Device Manufacturers

9.7.7.2 Contract Research Organizations (CROs)

9.7.7.3 Hospitals

9.7.7.4 Diagnostic Laboratories

9.7.7.5 Research Institutions

9.7.7.6 Others

9.7.8 Historic and Forecast Market Size by Country

9.7.8.1 Brazil

9.7.8.2 Argentina

9.7.8.3 Rest of SA

Chapter 10 Analyst Viewpoint and Conclusion

10.1 Recommendations and Concluding Analysis

10.2 Potential Market Strategies

Chapter 11 Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

|

Global Medical Device Testing Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 10.59 Bn. |

|

Forecast Period 2024-32 CAGR: |

9.42 % |

Market Size in 2032: |

USD 23.81 Bn. |

|

Segments Covered: |

By Testing Type |

|

|

|

By Device Type |

|

||

|

By Application |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||