Key Market Highlights

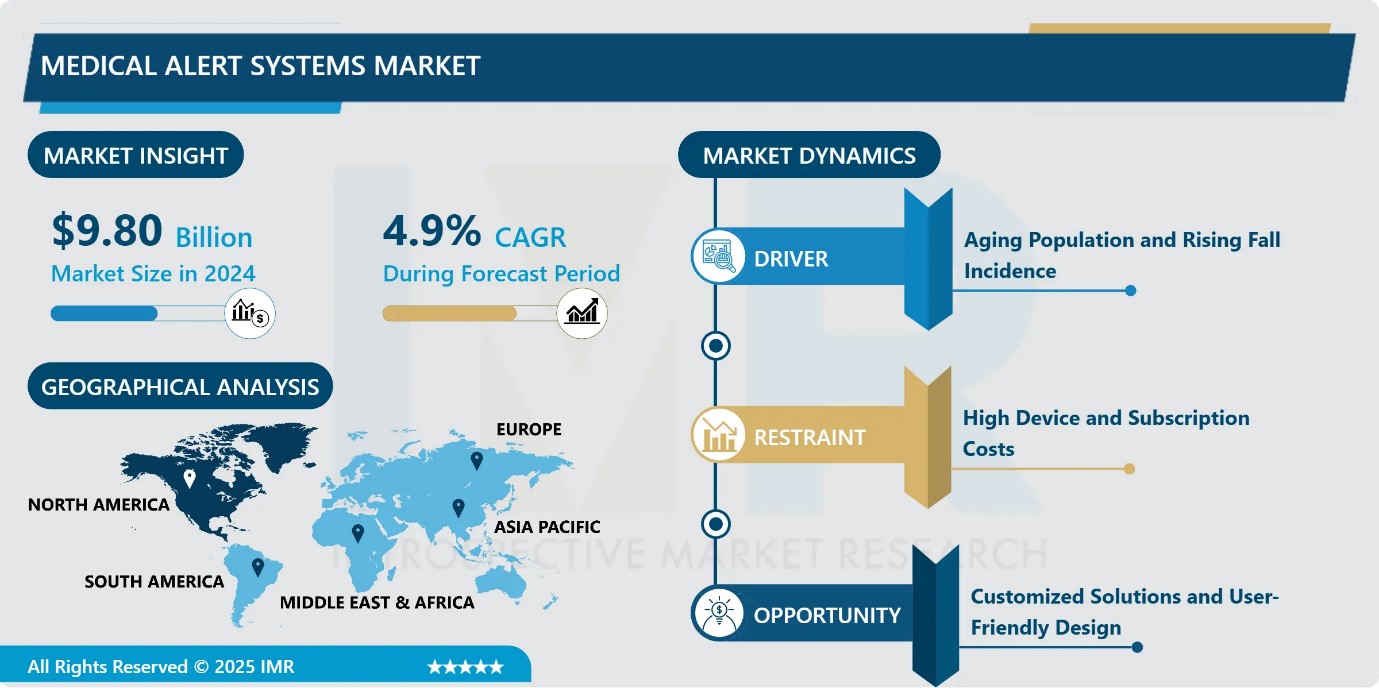

Medical Alert Systems Market Size Was Valued at USD 9.80 Billion in 2024, and is Projected to Reach USD 16.59 Billion by 2035, Growing at a CAGR of 4.9% from 2025-2035.

- Market Size in 2024: USD 9.80 Billion

- Projected Market Size by 2035: USD 16.59 Billion

- CAGR (2025–2035): 4.9%

- Leading Market in 2024: North America

- Fastest-Growing Market: Asia-Pacific

- By System Type: The Personal Emergency Response systems (PERS) segment is anticipated to lead the market by accounting for 36.4% of the market share throughout the forecast period.

- By End User: The Hospitals and Clinics segment is expected to capture 38.8% of the market share, thereby maintaining its dominance over the forecast period.

- By Region: North America region is projected to hold 31.20% of the market share during the forecast period.

- Active Players: ADT Health (United States), Alert1 (United States), AlertONE Services Inc. (United States), Bay Alarm Medical (United States), Connect America (United States), and Other Active Players.

Medical Alert Systems Market Synopsis:

Medical alert systems are devices designed to provide immediate assistance during emergencies, particularly for elderly individuals or those with health challenges living alone. Typically worn as a pendant or wristband with an activation button, these systems connect users to a 24/7 monitoring center that can dispatch help as needed. The rising elderly population and increasing preference for aging in place are driving demand, as falls and medical emergencies are common among adults aged 65 and above. Advanced features such as fall detection, GPS tracking, and geo-fencing for dementia patients enhance safety and independence. With over 55 million people affected by dementia globally, medical alert systems are essential for timely intervention, offering peace of mind to users and their caregivers while supporting independent living.

Medical Alert Systems Market Dynamics and Trend Analysis:

Medical Alert Systems Market Growth Driver-Aging Population and Rising Fall Incidence

- The growing population of adults aged 65 and above is driving demand for medical alert systems, as unintentional falls remain a leading cause of injury and mortality among seniors. Hospitals, insurers, and care institutions recognize the cost benefits of rapid emergency response, encouraging adoption of monitored devices in homes and healthcare facilities. Government regulations in developed economies link long-term-care reimbursements to fall-prevention measures, prompting hospitals to integrate alert systems into discharge protocols. Manufacturers are innovating wearable designs with tactile interfaces and loud audio prompts for hearing-impaired users, supporting recurring revenue through device replacements and upgrades.

Medical Alert Systems Market Limiting Factor-High Device and Subscription Costs

- The medical alert systems market faces challenges due to high device prices and recurring subscription fees, which remain prohibitive for low-income seniors, particularly in emerging markets. Limited or inconsistent public reimbursement forces many households to self-finance these solutions, restricting adoption. Rising semiconductor and component costs further increase manufacturing expenses, limiting the ability of vendors to offer discounts on advanced LTE-enabled devices. Although rental programs can reduce upfront costs, they have limited reach in rural or budget-sensitive regions. These economic barriers slow market penetration, especially among price-conscious consumers, and constrain growth in less affluent or underserved areas.

Medical Alert Systems Market Expansion Opportunity-Customized Solutions and User-Friendly Design

- The medical alert systems market is expanding through customization and user-centric design. Tailoring devices to manage specific chronic conditions such as diabetes, heart disease, or respiratory issues allows providers to deliver targeted, highly relevant solutions. Customization enhances effectiveness, making systems indispensable for ongoing health management and increasing adoption among specialized patient segments. Simultaneously, user-friendly designs with intuitive interfaces, large buttons, clear displays, and simple setup processes improve accessibility, particularly for elderly users. By addressing diverse health needs and reducing technological barriers, these innovations foster broader adoption, customer satisfaction, and loyalty, driving sustained growth and market expansion.

Medical Alert Systems Market Challenge and Risk-Privacy and Security Concerns

- Privacy and security issues present a significant challenge in the medical alert systems market, particularly in the U.S. The integration of devices with home networks, smartphones, or other connected systems raises concerns about data breaches, unauthorized access, and misuse of sensitive personal and health information. Complex configurations, cloud connectivity, and real-time monitoring features increase the potential vulnerability of user data. These concerns can hinder consumer confidence, limit adoption, and slow market growth. Manufacturers must implement robust encryption, secure authentication, and strict data protection measures to address these challenges and maintain trust among users and caregivers.

Medical Alert Systems Market Trend-Technological Advancements and Integration in Medical Alert Systems

- Advances in fall detection, GPS, and cellular technologies are transforming the medical alert systems market. Tri-axial accelerometers, edge-based machine-learning models, and multi-constellation GNSS chips enhance motion accuracy and reduce false alarms, while eSIM and dual-SIM designs improve connectivity in weak-signal areas. Features like indoor positioning, proactive check-ins, and two-way voice are becoming standard in mid-priced units, boosting mass-market adoption. Integration with remote patient monitoring via open APIs allows clinicians to correlate alerts with vital signs, optimize care delivery, and enable payers to subsidize devices under continuous monitoring programs, driving broader enterprise and home-based use.

Medical Alert Systems Market Segment Analysis:

Medical Alert Systems Market is segmented based on System Type, Technology, Application, and Region.

By System Type, Personal Emergency Response Systems (PERS) segment is expected to dominate the market with around 36.4% share during the forecast period.

- In 2024, the personal emergency response systems (PERS) segment dominated the U.S. medical alert systems market, accounting for the largest revenue share, driven by demand from seniors, individuals living alone, and workers in high-risk environments. Mobile PERS (mPERS) devices, lightweight and GPS-enabled, allow two-way communication and location tracking, enhancing rapid emergency response. VoIP-based PERS is expected to grow fastest due to portability, internet-based connectivity, and cost efficiency. Smart belts, equipped with fall detection, GPS, and biometric sensors, are gaining popularity for discreet monitoring. PERS dominance stems from widespread adoption, technological integration, and versatility across healthcare and workplace applications.

By End User, Hospitals and clinics is expected to dominate with close to 38.8% market share during the forecast period.

- Hospitals and clinics held 38.8% of the medical alert systems/PERS market share in 2024, driven by integration of devices into post-discharge care bundles to reduce readmissions. Emergency departments use alert buttons on inpatient beds to ensure rapid response, while value-based purchasing incentives further reinforce adoption. The segment remains dominant due to large-scale deployment capabilities, staff training, and integration with electronic health records for real-time monitoring. Senior housing and assisted living facilities are also growing, leveraging enterprise dashboards and bulk procurement. Institutional dominance is driven by the ability to manage high-acuity patients, ensure standardized care, and achieve operational efficiencies.

Medical Alert Systems Market Regional Insights:

North America region is estimated to lead the market with around 31.20% share during the forecast period.

- North America dominated the medical alert systems market with a revenue share of over 31.20% in 2024, driven by a rapidly aging population, advanced healthcare infrastructure, and high awareness of elderly care solutions. Technological innovations, such as AI-enabled fall detection, GPS-enabled wearables, and continuous health monitoring, have enhanced adoption. Favourable reimbursement policies and proactive safety initiatives further strengthen market growth. Rising incidences of dementia and Alzheimer’s disease in the U.S. have also increased demand for personal emergency response systems. While Asia Pacific is expected to register the fastest growth due to a growing geriatric population and expanding home-based healthcare programs, North America remains dominant due to its mature healthcare system, technological leadership, and widespread adoption of advanced, personalized emergency response solutions.

Medical Alert Systems Market Active Players:

- ADT Health (United States)

- AlertOne Services (United States)

- Bay Alarm Medical (United States)

- Connect America (United States)

- GreatCall / Lively (United States)

- Guardian Medical Monitoring (United States)

- Life Alert Emergency Response (United States)

- LifeFone (United States)

- LifeStation (United States)

- LogicMark (United States)

- Medical Guardian (United States)

- MobileHelp (United States)

- Nomo Smart Care (United States)

- Philips Lifeline (Netherlands)

- Valued Relationships Inc. (VRI) (United States)

- Other Active Players

Key Industry Developments in the Medical Alert Systems Market:

- In February 2025, LogicMark released the updated Guardian Alert 911 Plus medical alert device. The new version improves accessibility and safety for users in home and care settings. CEO Chia-Lin Simmons emphasized user-friendly, affordable technology with no monthly subscription fees.

- In January 2025, Nomo Smart Care introduced AI-powered technology to transform in-home care. The innovation provides intelligent monitoring without relying on cameras. This advancement enhances safety and convenience for elderly and at-risk individuals.

Technological Innovations, AI-Enabled Wearables, and Advanced Connectivity Driving the Global Medical Alert Systems Market

- The medical alert systems market is driven by advanced personal emergency response technologies designed to provide immediate assistance to seniors, individuals with chronic conditions, or those living alone. These systems integrate wearable devices such as pendants, wristbands, or smart belts with communication modules that connect to 24/7 monitoring centers. Key technologies include two-way voice systems, GPS-enabled location tracking, fall detection sensors, geo-fencing for dementia patients, and IP-based connectivity.

- Modern devices incorporate AI and IoT capabilities for real-time health monitoring, predictive alerts, and remote caregiver notifications. System reliability depends on factors such as battery life, network coverage, sensor accuracy, and low-latency communication protocols. Integration with mobile applications and cloud-based platforms enables personalized emergency response and data analytics for health trends. Additionally, advancements in wearable ergonomics, device miniaturization, and secure data transmission are enhancing usability, adoption, and overall effectiveness of medical alert systems globally.

|

Medical Alert Systems Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 9.80 Bn. |

|

Forecast Period 2025-32 CAGR: |

4.9% |

Market Size in 2035: |

USD 16.59 Bn. |

|

Segments Covered: |

By System Type |

|

|

|

Technology |

|

||

|

Application |

|

||

|

By End Users

|

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Medical Alert Systems Market by System Type (2018-2035)

4.1 Medical Alert Systems Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Personal Emergency Response Systems

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Nurse Calling Systems

4.5 Personal Emergency Response Systems (PERS)

4.6 and Other Types

Chapter 5: Medical Alert Systems Market by Technology (2018-2035)

5.1 Medical Alert Systems Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Two-way Voice Systems

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Unmonitored Medical Alert Systems

5.5 Medical Alert Alarm Button System

5.6 IP-based Systems

5.7 and Others

Chapter 6: Medical Alert Systems Market by Application (2018-2035)

6.1 Medical Alert Systems Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Home-Based Users

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Senior Living Facilities/Senior Care Centers

6.5 Assisted Living Facilities

6.6 Hospitals and Clinics

6.7 and Others

Chapter 7: Medical Alert Systems Market by End User (2018-2035)

7.1 Medical Alert Systems Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Home-Based Users

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Assisted Living Facilities

7.5 Hospitals and Clinics

7.6 and Others

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Medical Alert Systems Market Share by Manufacturer/Service Provider(2024)

8.1.3 Industry BCG Matrix

8.1.4 PArtnerships, Mergers & Acquisitions

8.2 ADT HEALTH (UNITED STATES)

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 ALERTONE SERVICES (UNITED STATES)

8.4 BAY ALARM MEDICAL (UNITED STATES)

8.5 CONNECT AMERICA (UNITED STATES)

8.6 GREATCALL / LIVELY (UNITED STATES)

8.7 GUARDIAN MEDICAL MONITORING (UNITED STATES)

8.8 LIFE ALERT EMERGENCY RESPONSE (UNITED STATES)

8.9 LIFEFONE (UNITED STATES)

8.10 LIFESTATION (UNITED STATES)

8.11 LOGICMARK (UNITED STATES)

8.12 MEDICAL GUARDIAN (UNITED STATES)

8.13 MOBILEHELP (UNITED STATES)

8.14 NOMO SMART CARE (UNITED STATES)

8.15 PHILIPS LIFELINE (NETHERLANDS)

8.16 VALUED RELATIONSHIPS INC. (VRI) (UNITED STATES)

8.17 AND OTHER ACTIVE PLAYERS.

Chapter 9: Global Medical Alert Systems Market By Region

9.1 Overview

9.2. North America Medical Alert Systems Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.2.4.1 US

9.2.4.2 Canada

9.2.4.3 Mexico

9.3. Eastern Europe Medical Alert Systems Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.3.4.1 Russia

9.3.4.2 Bulgaria

9.3.4.3 The Czech Republic

9.3.4.4 Hungary

9.3.4.5 Poland

9.3.4.6 Romania

9.3.4.7 Rest of Eastern Europe

9.4. Western Europe Medical Alert Systems Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.4.4.1 Germany

9.4.4.2 UK

9.4.4.3 France

9.4.4.4 The Netherlands

9.4.4.5 Italy

9.4.4.6 Spain

9.4.4.7 Rest of Western Europe

9.5. Asia Pacific Medical Alert Systems Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.5.4.1 China

9.5.4.2 India

9.5.4.3 Japan

9.5.4.4 South Korea

9.5.4.5 Malaysia

9.5.4.6 Thailand

9.5.4.7 Vietnam

9.5.4.8 The Philippines

9.5.4.9 Australia

9.5.4.10 New Zealand

9.5.4.11 Rest of APAC

9.6. Middle East & Africa Medical Alert Systems Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.6.4.1 Turkiye

9.6.4.2 Bahrain

9.6.4.3 Kuwait

9.6.4.4 Saudi Arabia

9.6.4.5 Qatar

9.6.4.6 UAE

9.6.4.7 Israel

9.6.4.8 South Africa

9.7. South America Medical Alert Systems Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

9.7.4.1 Brazil

9.7.4.2 Argentina

9.7.4.3 Rest of SA

Chapter 10 Analyst Viewpoint and Conclusion

Chapter 11 Our Thematic Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12 Case Study

Chapter 13 Appendix

13.1 Sources

13.2 List of Tables and figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Medical Alert Systems Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 9.80 Bn. |

|

Forecast Period 2025-32 CAGR: |

4.9% |

Market Size in 2035: |

USD 16.59 Bn. |

|

Segments Covered: |

By System Type |

|

|

|

Technology |

|

||

|

Application |

|

||

|

By End Users

|

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||