Key Market Highlights

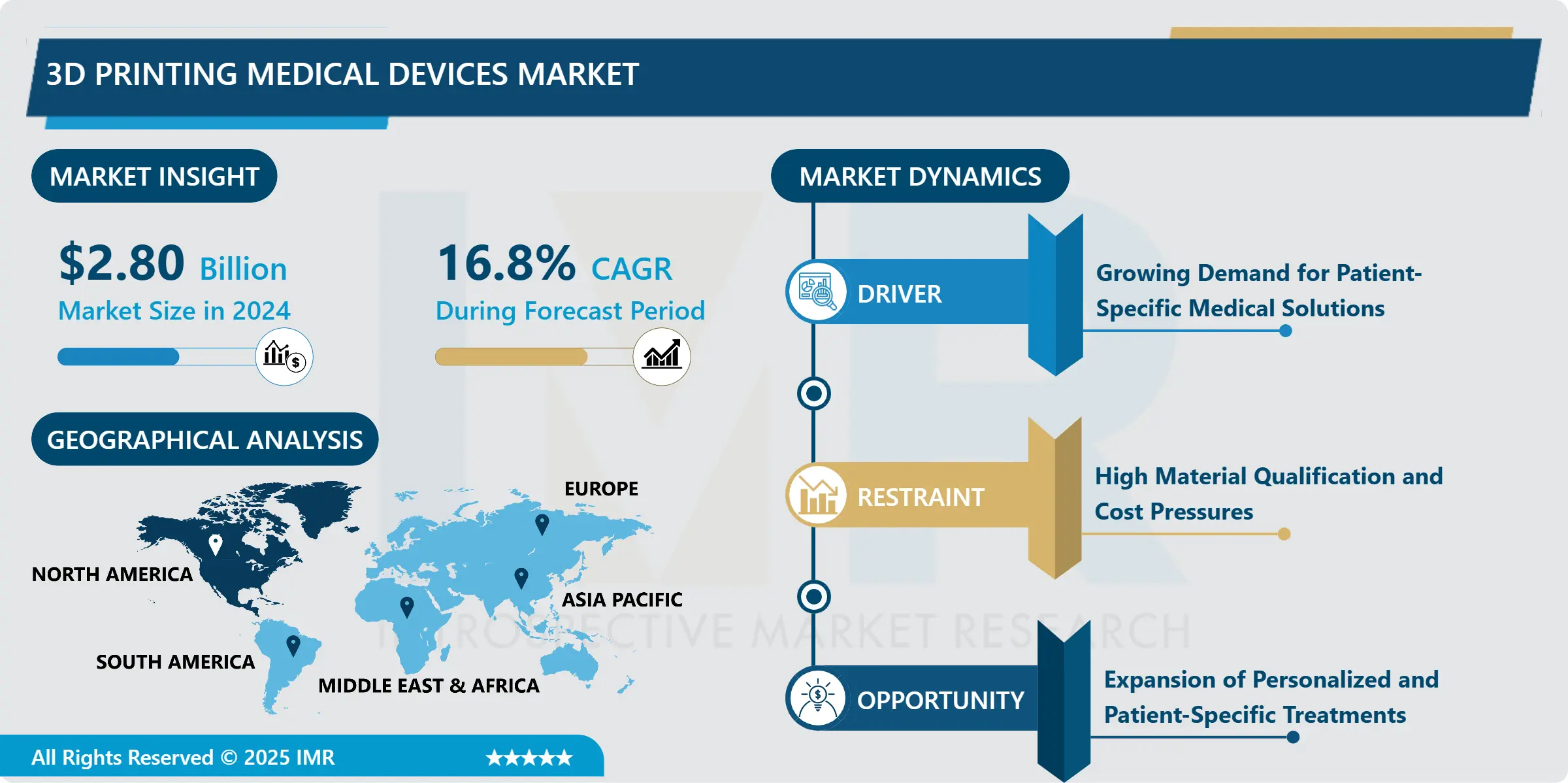

3D Printing Medical Devices Market Size Was Valued at USD 2.80 Billion in 2024, and is Projected to Reach USD 15.45 Billion by 2035, Growing at a CAGR of 16.8 % from 2025-2035.

- Market Size in 2024: USD 2.80 Billion

- Projected Market Size by 2035: USD 15.45 Billion

- CAGR (2025–2035): 16.8 %

- Leading Market in 2024: North America

- Fastest-Growing Market: Asia-Pacific

- By Technology: The Laser Beam Melting segment is anticipated to lead the market by accounting for 25.3% of the market share throughout the forecast period.

- By End User: The Hospitals and Surgical Centers segment is expected to capture 27.3% of the market share, thereby maintaining its dominance over the forecast period.

- By Region: North America region is projected to hold 31.9% of the market share during the forecast period.

- Active Players: 3D Systems, Inc. (U.S.), Anatomics Pty Ltd (Australia), Arcam AB (Sweden), Carbon, Inc. (U.S.), Concept Laser GmbH (Germany), and Other Active Players.

3D Printing Medical Devices Market Synopsis:

3D printing, also known as additive manufacturing, is a process that creates three-dimensional objects by depositing material layer by layer based on digital designs. In healthcare, this technology enables the production of patient-specific implants, surgical guides, anatomical models, and prosthetics, improving clinical precision and reducing surgery time. Hospitals increasingly adopt point-of-care 3D printing to enhance surgical planning, lower operating room costs, and minimize procedural risks. Advancements in material science, including high-performance polymers and metals, are expanding medical applications. Regulatory clarity for customized devices further supports adoption. While laser beam melting dominates implant manufacturing, binder jetting is gaining traction for scalable production. Market players are shifting toward software, automation, and consumables to sustain growth.

3D Printing Medical Devices Market Dynamics and Trend Analysis:

3D Printing Medical Devices Market Growth Driver - Growing Demand for Patient-Specific Medical Solutions

- The increasing need for personalized medical solutions is a key driver accelerating the adoption of 3D printing in healthcare. This technology enables the production of patient-specific implants, surgical instruments, and anatomical models using imaging data such as CT and MRI scans. Customization improves device fit, enhances surgical accuracy, and supports faster patient recovery. Healthcare providers increasingly use 3D-printed models for preoperative planning, leading to improved procedural outcomes. The dental and orthopedic segments are major adopters, leveraging mass customization for aligners and implants. Additionally, 3D printing shortens design-to-delivery cycles, reduces material waste, and supports rapid production in time-sensitive clinical scenarios, reinforcing its role in personalized healthcare delivery.

3D Printing Medical Devices Market Limiting Factor - High Material Qualification and Cost Pressures

- High material qualification costs remain a significant restraint in the 3D printing medical devices market. Each new medical-grade polymer or metal alloy must undergo extensive toxicity, sterility, and mechanical testing, often requiring high investments. Cost pressures intensified in 2024 due to sharp increases in raw material prices, including PEEK and titanium powders, driven by supply chain disruptions and geopolitical factors. These rising costs pose challenges for smaller manufacturers with limited production volumes, slowing material innovation. The situation is further complicated in bioprinting, where bio-inks require additional validation for sterility and biological compatibility, extending development timelines and regulatory documentation requirements.

3D Printing Medical Devices Market Expansion Opportunity - Expansion of Personalized and Patient-Specific Treatments

- The shift toward personalized and patient-specific healthcare presents a significant opportunity for the 3D printed medical devices market. Unlike conventional manufacturing, 3D printing enables customized implants, prosthetics, and surgical guides that improve clinical outcomes and reduce procedure times. Metal additive manufacturing is gaining traction in orthopedic, dental, and reconstructive applications, while advances in bioprinting and regenerative medicine are opening new avenues through bioresorbable implants and tissue scaffolds.

- Strategic collaborations among device manufacturers, research institutions, and 3D printing providers are accelerating innovation. Additionally, hospital-based, on-demand production lowers supply chain dependence, reduces costs, and improves access to care, particularly in remote regions. Continued progress in materials, AI-driven design, and automation is expected to further unlock market potential.

3D Printing Medical Devices Market Challenge and Risk - High Regulatory and Quality Compliance Burden

- The 3D printing medical devices market faces significant challenges due to stringent regulatory and quality compliance requirements. The highly customized nature of patient-specific devices limits standardization, as variations in design, materials, and production parameters require extensive validation and documentation. While regulatory bodies have issued guidance for additively manufactured medical devices, approval processes remain complex and time-consuming, often delaying commercialization.

- Hospital-based printing facilities encounter additional hurdles in maintaining consistent regulatory oversight across decentralized operations. Moreover, differences in printer technologies and material performance can lead to output variability, necessitating rigorous quality control measures. These compliance demands increase development costs, restrict scalability, and pose barriers to entry for smaller manufacturers, slowing widespread market adoption.

3D Printing Medical Devices Market Trend - 3D Printing Medical Devices Market

- The 3D printing medical devices market is undergoing rapid transformation, driven by technological innovation and expanding adoption across healthcare settings. A key trend is the growing emphasis on customization, enabling patient-specific prosthetics, implants, and surgical tools that improve comfort and clinical outcomes. Healthcare providers are increasingly integrating 3D printing into surgical planning and medical training, enhancing procedural accuracy and operational efficiency.

- Another notable trend is the focus on cost-effectiveness and sustainability, as additive manufacturing reduces material waste and supports on-demand production. This shift encourages localized manufacturing, strengthens supply chains, and aligns with healthcare systems’ efforts to balance quality care with cost containment, supporting continued market growth.

3D Printing Medical Devices Market Segment Analysis:

3D Printing Medical Devices Market is segmented based on Component, Technology, Product, Application, End User , and Region.

By Technology, Laser Beam Melting segment is expected to dominate the market with around 25.3% share during the forecast period.

- Laser Beam Melting (LBM) leads the 3D printed medical devices market due to its ability to consistently produce high-strength, pore-controlled metal components, particularly titanium implants used in orthopedic and spinal applications. Its dominance is supported by superior mechanical performance, biocompatibility, and precision required for load-bearing medical implants.

- LBM captured the largest market share in 2025 as it meets strict regulatory and quality standards while enabling complex geometries. In contrast, binder jetting is emerging as a high-growth technology because of faster production speeds and reduced post-processing needs. However, LBM remains dominant due to its proven clinical reliability, regulatory acceptance, and widespread use in critical implant manufacturing.

By End User, Hospitals and surgical centers is expected to dominate with close to 27.3% market share during the forecast period.

- Hospitals and surgical centers represent the largest end-user segment in the 3D printed medical devices market, driven by growing adoption of point-of-care manufacturing. In-house 3D printing laboratories allow hospitals to produce anatomical models, surgical guides, and customized implants, reducing surgery preparation time and improving procedural outcomes.

- This segment dominates due to strong capital resources, integrated clinical workflows, and direct surgeon involvement in design and validation. Hospitals also benefit from improved patient communication through physical models. While specialty clinics are growing rapidly due to agility and niche applications, hospitals remain dominant because of their scale, multidisciplinary capabilities, and higher procedural volumes that justify sustained investment in advanced 3D printing infrastructure.

3D Printing Medical Devices Market Regional Insights:

- North America remains the leading region in the healthcare 3D printing market, driven by early regulatory support, strong reimbursement frameworks, and substantial investments in hospital infrastructure. The region accounted for a significant share of global revenue, supported by widespread adoption of patient-specific devices, surgical models, and implants. Growth accelerated during the COVID-19 pandemic, when 3D printing was extensively used to produce critical medical supplies.

- The United States dominates the regional market due to its advanced healthcare ecosystem, strong R&D capabilities, and rapid technology adoption by hospitals and research institutions. Additionally, government funding, defense-backed innovation programs, and industry consolidation further strengthen North America’s leadership, making it the most mature and innovation-driven market globally.

3D Printing Medical Devices Market Active Players:

- 3D Systems, Inc. (U.S.)

- Anatomics Pty Ltd (Australia)

- Arcam AB (Sweden)

- Carbon, Inc. (U.S.)

- Concept Laser GmbH (Germany)

- Cyfuse Biomedical K.K. (Japan)

- EOS GmbH Electro Optical Systems (Germany)

- EnvisionTEC, Inc. (U.S.)

- GENERAL ELECTRIC COMPANY (U.S.)

- Materialise (Belgium)

- Organovo Holdings, Inc. (U.S.)

- Prodways Group (France)

- Renishaw plc (U.K.)

- SLM Solutions (Germany)

- Stratasys Ltd. (Israel)

- Other Active Players

Key Industry Developments in the 3D Printing Medical Devices Market:

- In April 2025: 3D Systems supported the successful development of the first MDR-compliant PEEK facial implant at University Hospital Base.This milestone highlights the use of advanced additive manufacturing for patient-specific craniofacial solutions.The achievement marks a significant step forward in regulatory-compliant 3D-printed medical implants.

- In March 2024: EOS GmbH launched the EOS M 290 1Kw, an enhanced version of its established M 290 platform.The upgraded Laser Powder Bed Fusion system is optimized for high-volume, serial manufacturing applications.It is specifically designed to process copper and copper alloys used in critical components such as heat exchangers and inductors.

Technical Perspective: 3D Printing Medical Devices Market

- The 3D Printing Medical Devices Market is underpinned by advanced additive manufacturing technologies that enable layer-by-layer fabrication of complex, patient-specific medical components directly from digital models. Key technologies include laser beam melting, electron beam melting, selective laser sintering, stereolithography, binder jetting, and fused deposition modeling, each selected based on material compatibility and application requirements. Medical-grade polymers such as PEEK, PLA, and resins, along with biocompatible metals like titanium and cobalt-chromium alloys, are widely used to meet mechanical strength, sterility, and regulatory standards.

- Integration with medical imaging modalities such as CT and MRI allows precise anatomical replication for implants and surgical guides. Post-processing steps including heat treatment, surface finishing, and sterilization are critical to ensuring clinical safety and performance. Continuous advances in material science, printer resolution, process automation, and AI-driven design optimization are enhancing scalability, repeatability, and regulatory compliance across medical applications.

|

3D Printing Medical Devices Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2024 |

Market Size in 2024: |

USD 2.80 Bn. |

|

Forecast Period 2025-32 CAGR: |

16.8% |

Market Size in 2035: |

USD 15.45 Bn. |

|

Segments Covered: |

By Component |

|

|

|

By Technology |

|

||

|

By Product |

|

||

|

By Application

|

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: 3D Printing Medical Devices Market by Component (2018-2035)

4.1 3D Printing Medical Devices Market Snapshot and Growth Engine

4.2 Market Overview

4.3 System and Others

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

Chapter 5: 3D Printing Medical Devices Market by Technology (2018-2035)

5.1 3D Printing Medical Devices Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Laser Beam Melting

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Photopolymerization

5.5 Extrusion-Based Technologies

5.6 Electron Beam Melting

5.7 Binder Jetting

5.8 and Others

Chapter 6: 3D Printing Medical Devices Market by Product (2018-2035)

6.1 3D Printing Medical Devices Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Equipment

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Materials

6.5 Services

6.6 and Software

Chapter 7: 3D Printing Medical Devices Market by Application (2018-2035)

7.1 3D Printing Medical Devices Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Prosthetics and Implants

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Surgical Guides and Instruments

7.5 Tissue-Engineered Products

7.6 Hearing Aids

7.7 and Wearable Medical Devices

Chapter 8: 3D Printing Medical Devices Market by End User (2018-2035)

8.1 3D Printing Medical Devices Market Snapshot and Growth Engine

8.2 Market Overview

8.3 Hospitals and Surgical Centers

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

8.3.3 Key Market Trends, Growth Factors, and Opportunities

8.3.4 Geographic Segmentation Analysis

8.4 Clinics

8.5 Academic & Research Institutions

8.6 and Pharma-Biotech & Medical Device Companies

Chapter 9: Company Profiles and Competitive Analysis

9.1 Competitive Landscape

9.1.1 Competitive Benchmarking

9.1.2 3D Printing Medical Devices Market Share by Manufacturer/Service Provider(2024)

9.1.3 Industry BCG Matrix

9.1.4 PArtnerships, Mergers & Acquisitions

9.2 3D SYSTEMS

9.2.1 Company Overview

9.2.2 Key Executives

9.2.3 Company Snapshot

9.2.4 Role of the Company in the Market

9.2.5 Sustainability and Social Responsibility

9.2.6 Operating Business Segments

9.2.7 Product Portfolio

9.2.8 Business Performance

9.2.9 Recent News & Developments

9.2.10 SWOT Analysis

9.3 INC. (U.S.)

9.4 ANATOMICS PTY LTD (AUSTRALIA)

9.5 ARCAM AB (SWEDEN)

9.6 CARBON

9.7 INC. (U.S.)

9.8 CONCEPT LASER GMBH (GERMANY)

9.9 CYFUSE BIOMEDICAL K.K. (JAPAN)

9.10 EOS GMBH ELECTRO OPTICAL SYSTEMS (GERMANY)

9.11 ENVISIONTEC

9.12 INC. (U.S.)

9.13 GENERAL ELECTRIC COMPANY (U.S.)

9.14 MATERIALISE (BELGIUM)

9.15 ORGANOVO HOLDINGS

9.16 INC. (U.S.)

9.17 PRODWAYS GROUP (FRANCE)

9.18 RENISHAW PLC (U.K.)

9.19 SLM SOLUTIONS (GERMANY)

9.20 STRATASYS LTD. (ISRAEL)

9.21 AND OTHER ACTIVE PLAYERS.

Chapter 10: Global 3D Printing Medical Devices Market By Region

10.1 Overview

10.2. North America 3D Printing Medical Devices Market

10.2.1 Key Market Trends, Growth Factors and Opportunities

10.2.2 Top Key Companies

10.2.3 Historic and Forecasted Market Size by Segments

10.2.4 Historic and Forecast Market Size by Country

10.2.4.1 US

10.2.4.2 Canada

10.2.4.3 Mexico

10.3. Eastern Europe 3D Printing Medical Devices Market

10.3.1 Key Market Trends, Growth Factors and Opportunities

10.3.2 Top Key Companies

10.3.3 Historic and Forecasted Market Size by Segments

10.3.4 Historic and Forecast Market Size by Country

10.3.4.1 Russia

10.3.4.2 Bulgaria

10.3.4.3 The Czech Republic

10.3.4.4 Hungary

10.3.4.5 Poland

10.3.4.6 Romania

10.3.4.7 Rest of Eastern Europe

10.4. Western Europe 3D Printing Medical Devices Market

10.4.1 Key Market Trends, Growth Factors and Opportunities

10.4.2 Top Key Companies

10.4.3 Historic and Forecasted Market Size by Segments

10.4.4 Historic and Forecast Market Size by Country

10.4.4.1 Germany

10.4.4.2 UK

10.4.4.3 France

10.4.4.4 The Netherlands

10.4.4.5 Italy

10.4.4.6 Spain

10.4.4.7 Rest of Western Europe

10.5. Asia Pacific 3D Printing Medical Devices Market

10.5.1 Key Market Trends, Growth Factors and Opportunities

10.5.2 Top Key Companies

10.5.3 Historic and Forecasted Market Size by Segments

10.5.4 Historic and Forecast Market Size by Country

10.5.4.1 China

10.5.4.2 India

10.5.4.3 Japan

10.5.4.4 South Korea

10.5.4.5 Malaysia

10.5.4.6 Thailand

10.5.4.7 Vietnam

10.5.4.8 The Philippines

10.5.4.9 Australia

10.5.4.10 New Zealand

10.5.4.11 Rest of APAC

10.6. Middle East & Africa 3D Printing Medical Devices Market

10.6.1 Key Market Trends, Growth Factors and Opportunities

10.6.2 Top Key Companies

10.6.3 Historic and Forecasted Market Size by Segments

10.6.4 Historic and Forecast Market Size by Country

10.6.4.1 Turkiye

10.6.4.2 Bahrain

10.6.4.3 Kuwait

10.6.4.4 Saudi Arabia

10.6.4.5 Qatar

10.6.4.6 UAE

10.6.4.7 Israel

10.6.4.8 South Africa

10.7. South America 3D Printing Medical Devices Market

10.7.1 Key Market Trends, Growth Factors and Opportunities

10.7.2 Top Key Companies

10.7.3 Historic and Forecasted Market Size by Segments

10.7.4 Historic and Forecast Market Size by Country

10.7.4.1 Brazil

10.7.4.2 Argentina

10.7.4.3 Rest of SA

Chapter 11 Analyst Viewpoint and Conclusion

Chapter 12 Our Thematic Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 13 Case Study

Chapter 14 Appendix

12.1 Sources

12.2 List of Tables and figures

12.3 Short Forms and Citations

12.4 Assumption and Conversion

12.5 Disclaimer

|

3D Printing Medical Devices Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2024 |

Market Size in 2024: |

USD 2.80 Bn. |

|

Forecast Period 2025-32 CAGR: |

16.8% |

Market Size in 2035: |

USD 15.45 Bn. |

|

Segments Covered: |

By Component |

|

|

|

By Technology |

|

||

|

By Product |

|

||

|

By Application

|

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||