Luxury Wines and Spirits Market Synopsis

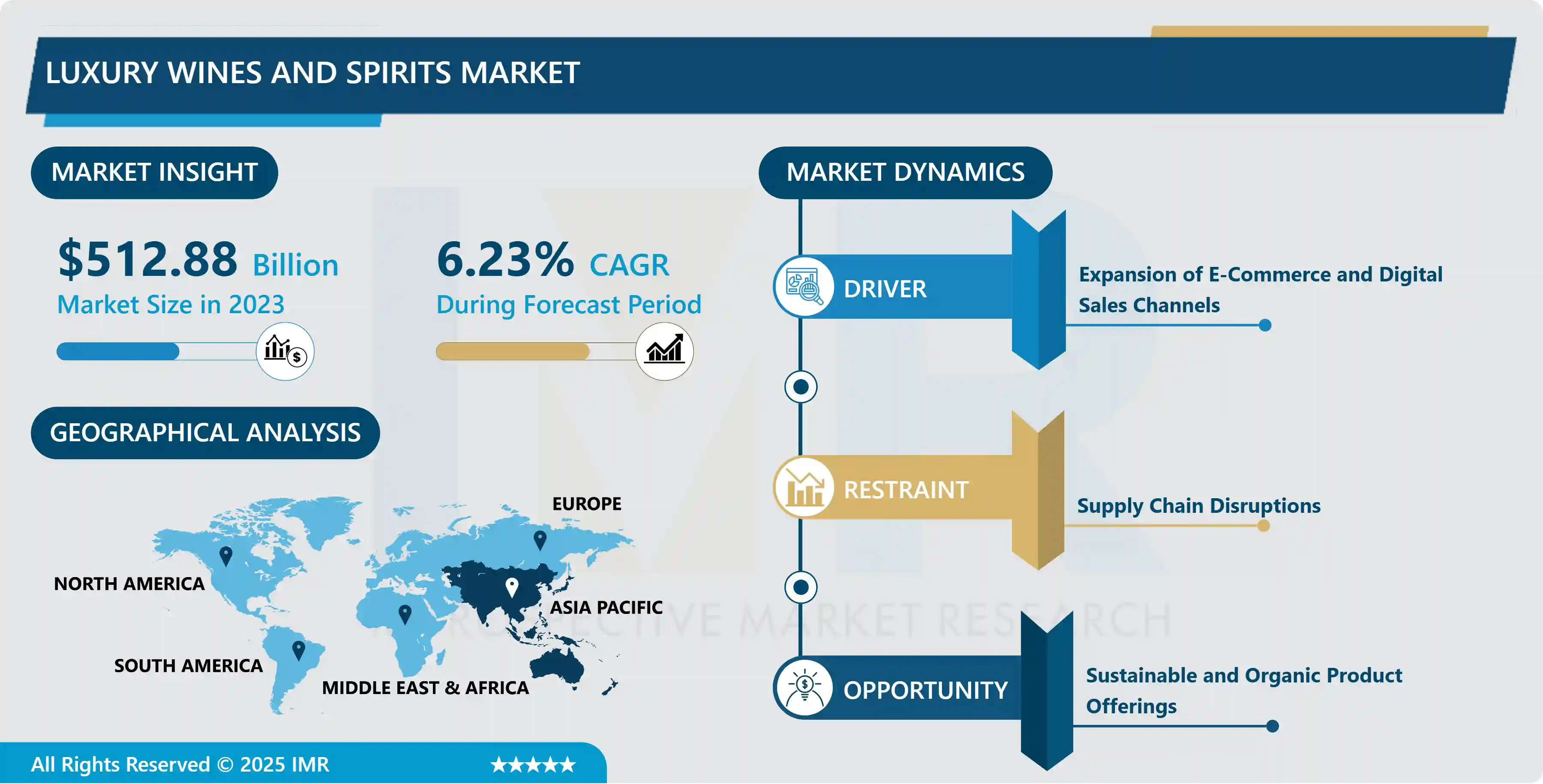

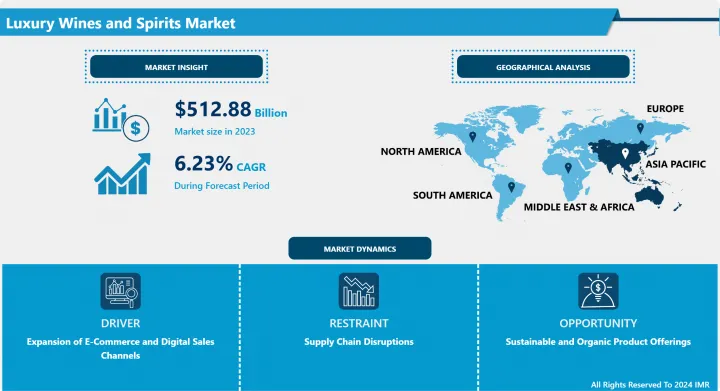

Luxury Wines and Spirits Market Size Was Valued at USD 512.88 Billion in 2023, and is Projected to Reach USD 883.57 Billion by 2032, Growing at a CAGR of 6.23% From 2024-2032.

The luxuries wines and spirits index includes alcoholic products that are of high quality, produced by premium standards and come along with the prestige of luxury brands. Such products may originate from famous vineyards or distilleries and are usually more expensive because of their rarity, taste, and quality. Many people connect them with noble meals, important occasions, as well as gourmet society.

The global luxury wines and spirits market has exhibited considerable growth trends in the recent past, been fed by high disposable incomes, escalating trends in premiumisation, and, not to mention shifting consumer consumption patterns. Customers are now more ready to spend large sum of money for branded, luxurious and classy products that define the status of the buyer. This comes in the wake of people wanting to make things better through quality and taste as those with more money look for something better. However, growth of the middle class, particularly in the developing world countries like China and India helped the market to grow. In these regions there is increasing demand for high quality wines and spirits, which comes with westernization of life styles and sperb consumption. Also, the millennial and Gen Z group is getting sophisticated with their choice and is willing to spend more in luxury brands that are close to their personality and belief. They are consuming and demanding wines and spirits that are organic, sustainable and made through ethical means in agreement with the current health and environmental trends. Furthermore, digitalification has been significant, through which through which consumers are able to access luxury goods easier through online platforms especially during the Covid-19 pandemic as more people shifted to online shopping. The change in market accessibility has hence opened the market up to a wider market inventory, basic items being overshadowed by premium market commodities.

There are three broad categories of alcoholic beverages: wines, spirits and champagne, which have all experienced an increasing trend in preference for the premium brands. In the wine segment, super premium segment comprising of wines, wine from vintages/limited editions and wines from well known vineyard are experiencing high demand. In the spirits sector, whiskey vodka, rum, and cognac are the most brilliant players in the luxury spirits segment providing brands, blends, aged products, and limited editions for elitist consumers. Of the alcoholic beverages, luxury whiskey has received much attention, due to the increasing demand of aged whiskey from popular Scotch, Japanese, and American brands as well as for champagne which remains a symbol of status and festivity. Of equal significance to the properties of the wines and spirits themselves are the branding and marketing that accompany these products. Market leaders in this segment like LVMH, Diageo, and Pernod Ricard employ elaborate marketing communication where emphasis is placed on the problems of prestige, uniqueness, and quality. Thus, storytelling, association with popular actors and actresses, organization of luxurious parties also continued to enhance the value of these brands.

From a geographical perspective, Europe continues to lead this market, more so with the leading players such as France, Italy, and Spain in production. The focus on developing wine and spirits industry for years has allowed the region to become a market leader due to brand awareness. However, the Asia Pacific market is getting defensive for the luxury wine and spirits due the growing rich class population in countries like China, Japan, and South Korea. For example, cognac and wines in china remain popular as gift products and symbol of status most Preferred imports of those valued brands therefore remain cognac and wines. Also, changing life styles due to urbanization, increase in the influence of western culture, and most importantly the increase in number of restaurants providing the food service have fuelled growth. The same is true for the market in North America, especially in the United States where customers increasingly demand higher shelf wines and spirits, many of which have been produced through craft and artisanal methods. The U.S. also boasts of a strong consumer base of collectors and investors who view wines and spirits, and in particular, fine, aged stock and specialty and limited edition releases, as an attractive investment.

It is becoming apparent that luxury wines and spirits leaps these kid factors of sustainability and innovation. Currently, consumers are turning into environmental sustainable, and subsequently, brands are focusing on sustainability in production and packaging. For instance, most quality wines are now being produced under organic or biodynamic farming methods, so that the impact of the wine on the environment is kept to a minimal and the green consumers are assured. Likewise, consumers expect better packaging solutions that are sustainable, and businesses are aiming at using better packaging material produced fewer emissions. Digital innovation is another area of growth as blockchain finds application in the market to improve its credibility and fight the issue of counterfeit products. This does not only increase confidence among the consumers but also maintain the nature and part exclusivity of luxury products. Furthermore, the concept of direct selling through the internet has expanded the frequent touch points that the luxury brands can interact with their customers and share memorable experiences enhancing loyalty.

The trend in luxury wines and spirits is expected to gain further momentum in the near future with inklings of premiumization, rising affluence globally, and changing consumer sentiment. Wine and spirits, and champagne market’s segmentation give brands great room to innovate, become environmentally conscious and exclusive. Right now Europe is retaining its dominance of the market of power tools, while the Asia Pacific declares itself a region of high growth. They will have to keep focused on storytelling, sustainability, and as the adaptation to a more sophisticated and pluralistic consumer public, a digital agenda.

Luxury Wines and Spirits Market Trend Analysis

Growing Demand for Premiumization and Craft Spirits

- The overall global market for luxury wines and spirits is set for another year of sublime growth due to the growing trend of Premiumization and a quickly ascending interest in craft spirits. The younger consumers including the millennial and young affluent groups are now emphasizing on an improved quality, small batches, and artisanal production that supports complex and superior taste sensory experiences and brand stories. Which is exasperated by advancement in disposable income, urbanization and aspiration to own luxury brands as status symbols that has seen the shift towards premium products. Craft spirits are noted to be on the rise since they have unique features of personalization, novelty and creativity, which hundreds of thousands of consumers search for, when purchasing this type of Spirits. There is also the issue of SCs offering organic and sustainably sourced ingredients which is responding to the aspects of both health conscious consumers and environmentally conscience consumers creating another premiumization trend for SCs to embrace.

- In order to meet such need, there are currently distinct market trends in the LWS Industry, especially among the major international players that are seeking to diversify and strengthen their position in craft and premium segments either through acquisitions of craft distilleries or through the introduction of super premium brands derived from their existing product portfolios. North America and Europe are expected to have the largest share of the market due to their penchant for expensive items, although Asia and Pacific markets are gradually gaining momentum due to growing rates of population wealth and increasing demand for luxury spirits among the middle and upper classes of society. Also, digital marketing, social media, celebrity endorsements are acting as driving force influencing younger generations to develop preference for premium and craft segment which is a rapid growth factor for this market.

Sustainable and Organic Product Offerings

- Global Luxury Wines and Spirits Market is now focusing on more organic products as customers are deviating more towards green products. Premium segments of the wine industry have adopted European viticulture methods that exclude the use of chemical pesticides and fertilizers for organic farming techniques that improve the quality of the wine. While this commitment to organic production is friendly to the conscience of environmentally aware consumers, it is also consistent with the nature of luxury brands as authentic and handcrafted. Also, sustainability is becoming a focus during manufacturing too, with many luxury wineries and distilleries turning to lightweight glass bottles, biodegradable materials etc., to effectively cut out their environmental impact.

- However, applying sustainability in product portfolios is increasingly emerging as a value proposition strategy in the luxury sector. Not only are brands promoting their organic certifications, but they are also telling stories that incorporate their environmentally friendly activities and background information. The factor bolstering this trend is increasing aspiration towards the better and healthier organic wines and spirits from premium brands that are considered to be crafted and made with more and better techniques. They believe that the current group of consumers is more conscious of the consequences of their purchases, and that is a significant reason why luxury brands that invest in sustainability and are honest about it are going to gain a competitive advantage. Both aim at quality and sustainable products to increases clients engagement with the brands and thus spurring growth in this premium segment.

Luxury Wines and Spirits Market Segment Analysis:

- Luxury Wines and Spirits Market Segmented based on Type, Application, and End User.

By Type, Wine segment is expected to dominate the market during the forecast period

- The luxury wines and spirits are featuring a rather vast category that may include all kinds of alcoholic drinks conforming to the tastes of demanding consumers. Wine continues to be an unyielding product in this market because of the growing demand on the retail, commercial, and local users of wines which are differentiated in line with the quality of the products and they originate from countries such as Bordeaux in France, Napa Valley in Usa, and Tuscany in Italy. The general whisky category has also expanded considerably over the decade, driven by single malts and craft distillers with Scotland, Japan and United States the key players. Consumers will look for specific tastes and increasing preference towards artisan crafted products, and rum and brandy manufacture spirits are witnessing changes due to the new innovations like effects of infusion techniques and new classy brands for vodka & gin to suite cocktail lovers market. The spirits originating from Mexican roots tequila is also experiencing a revival for luxury brands that focus more on the quality.

- As for the megatrends affecting the luxury wines & spirits market, one of the key ones is the shift towards experiential consumption, that is, the importance of getting unique tasting and exclusive, limited edition products. Purchasing is also influenced by sustainability and ethics in a way that forces such leading brands to open their sourcing to sustainable practices and indeed environmentally friendly packaging. Continued evolution of online retail outlets has also made luxury products more easily available to the buyers; they can now access and order different brands of Wines & Spirits online. Moreover, consumers’ awareness or attentiveness toward brands is even higher due to the social media’s impact on consumers’ purchase decisions, especially among millennials and Gen Z. Hence the luxury wines and spirits segment continues to grow forward with brands opting to redesign to capture the taste of a discerning segment.

By Distribution Channel, Food Retail segment held the largest share in 2023

- The Luxury Wines and Spirits Market segmented on the basis of the distribution channel Know these trends and difference between food retail format and food service format. The Food Retail segment consists of restaurants, premium grocery stores, and wine shops classified in the GAS with affluent customers who are purchasing products for their household consumption. This had led to increased direct to consumer sale through the internet ey due to the increased online purchasing coupled with increasing demand for enhancements in learning on wines and spirits. Supermarkets and other generalized stores are now sourcing products that are of exquisite quality, niche, special, or limited editions and which have a specialty niche of consumers that they appeal to. Also, increased quality of basic products and increased number of customers looking for premium products in every range also boosts the classy products required in the retail channel.

- On the flip side, the Food Service segment consists of elaborate eateries, pubs, and accommodation facilities that offer signature wine and spirited services to augment menu propositions. This channel profits from popularity of the idea of extreme consumption, according to which people are ready to spend more money to get a high quality and interesting suggestions on pairing,=R19=. Liquor-conscious food service establishments that consider employing the services of professional sommeliers and wine service programs are likely to attract the highest denomination of consumers of wines and spirits. Also, as more people are heading back into restaurants and other eating establishments, once again the Food Service segment is gaining momentum and consumers are willing to spend more on better quality beverages when they dine out. This dualism of retail and food service channels shows how elaborate strategies are required for brands to navigate the viscose arena of luxury W&S sector.

Luxury Wines and Spirits Market Regional Insights:

Asia Pacific is Expected to Dominate the Market Over the Forecast period

- An emerging trend in the Luxury Wines and Spirits Market includes the Asia Pacific region to grow during the forecast period owing to the factors such as increase in disposable income, changing in consumers’ preferences, and enhancement of the quality of the wines and spirits. Whereas three years ago there was a growing market in the ‘second world’, today China, Japan and India have a emerging middle class willing to spend on fine wine and spirits as status symbols. Also, the shifting customer consumption pattern from mass products towards the luxury alcoholic beverages sector, along with the expansion of the e-commerce channel for products, boosts market demand.

- In the same respect, the Asia Pacific market is defined by the shifting trend in drinking profiles with the young people more willing to try out different brands and flavours in the premium segment. This change is supported by the growing impact of social media and digital marketing, while the latter remains to be an essential factor in advertising luxury wines and spirits to those using the latest technologies. In addition, leading names are turning their attention to niche marketing techniques and localised products. Thus, the Asia Pacific region is poised to exert the most significant influence on the Luxury Wines and Spirits Market and prove itself to be a major player in the global consumables market for the affluen.

Active Key Players in the Luxury Wines and Spirits Market

- Diageo (UK)

- LVMH (France)

- Pernod Ricard (France)

- Bacardi (Bermuda)

- Edrington (UK)

- Suntory Holdings Limited (Japan)

- Brown-Forman (USA)

- United Spirits (India)

- Thai Beverage Public Limited Company (Thailand)

- Hitejinro Co. Ltd. (South Korea)

- Davide Campari-Milano S.p.A (Italy)

- Others Key Player

Key Industry Developments in the Luxury Wines and Spirits Market

- In January 2024, Free AF, a U.S.-based brand specializing in alcohol-free beverages, announced the launch of its new non-alcoholic Sparkling Rosé, now available at Sprouts Farmers Market locations across the United States.

- In 2023, Mionetto, a drink company, introduced a new line of non-alcoholic sparkling wine, expanding its portfolio to cater to the growing demand for alcohol-free alternatives. This innovative product aims to provide the same celebratory experience as traditional sparkling wine, making it an excellent choice for those seeking a sophisticated beverage without the alcohol content.

- In 2023, Giesen, a New Zealand-based provider of non-alcoholic wine, unveiled its latest offering, Giesen 0% Sparkling Brut. This addition enhances Giesen's diverse non-alcoholic wine range, which also includes options such as 0% Sauvignon Blanc, Pinot Grigio, Riesling, Rosé, and Premium Red.

- In 2022,On St. Patrick's Day Jameson unveiled an exciting new addition to its portfolio: a citrus-flavored whisky that promises to delight fans of both traditional and innovative spirits. These unique whisky features undertones of vanilla and almonds, evoking the classic flavors found in an Old-Fashioned cocktail, making it a versatile choice for various occasions.

|

Global Luxury Wines and Spirits Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 512.88 Bn. |

|

Forecast Period 2024-32 CAGR: |

6.23% |

Market Size in 2032: |

USD 883.57 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Distribution Channel |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Luxury Wines and Spirits Market by Type (2018-2032)

4.1 Luxury Wines and Spirits Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Wine

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Whisky

4.5 Rum

4.6 Brandy

4.7 Vodka

4.8 Gin

4.9 Tequila

4.10 Others

Chapter 5: Luxury Wines and Spirits Market by Distribution Channel (2018-2032)

5.1 Luxury Wines and Spirits Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Food Retail

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Food Service

Chapter 6: Company Profiles and Competitive Analysis

6.1 Competitive Landscape

6.1.1 Competitive Benchmarking

6.1.2 Luxury Wines and Spirits Market Share by Manufacturer (2024)

6.1.3 Industry BCG Matrix

6.1.4 Heat Map Analysis

6.1.5 Mergers and Acquisitions

6.2 DIAGEO (UK)

6.2.1 Company Overview

6.2.2 Key Executives

6.2.3 Company Snapshot

6.2.4 Role of the Company in the Market

6.2.5 Sustainability and Social Responsibility

6.2.6 Operating Business Segments

6.2.7 Product Portfolio

6.2.8 Business Performance

6.2.9 Key Strategic Moves and Recent Developments

6.2.10 SWOT Analysis

6.3 LVMH (FRANCE)

6.4 PERNOD RICARD (FRANCE)

6.5 BACARDI (BERMUDA)

6.6 EDRINGTON (UK)

6.7 SUNTORY HOLDINGS LIMITED (JAPAN)

6.8 BROWN-FORMAN (USA)

6.9 UNITED SPIRITS (INDIA)

6.10 THAI BEVERAGE PUBLIC LIMITED COMPANY (THAILAND)

6.11 HITEJINRO CO. LTD. (SOUTH KOREA)

6.12 DAVIDE CAMPARI-MILANO S.P.A (ITALY)

6.13 OTHERS KEY PLAYER

Chapter 7: Global Luxury Wines and Spirits Market By Region

7.1 Overview

7.2. North America Luxury Wines and Spirits Market

7.2.1 Key Market Trends, Growth Factors and Opportunities

7.2.2 Top Key Companies

7.2.3 Historic and Forecasted Market Size by Segments

7.2.4 Historic and Forecasted Market Size by Type

7.2.4.1 Wine

7.2.4.2 Whisky

7.2.4.3 Rum

7.2.4.4 Brandy

7.2.4.5 Vodka

7.2.4.6 Gin

7.2.4.7 Tequila

7.2.4.8 Others

7.2.5 Historic and Forecasted Market Size by Distribution Channel

7.2.5.1 Food Retail

7.2.5.2 Food Service

7.2.6 Historic and Forecast Market Size by Country

7.2.6.1 US

7.2.6.2 Canada

7.2.6.3 Mexico

7.3. Eastern Europe Luxury Wines and Spirits Market

7.3.1 Key Market Trends, Growth Factors and Opportunities

7.3.2 Top Key Companies

7.3.3 Historic and Forecasted Market Size by Segments

7.3.4 Historic and Forecasted Market Size by Type

7.3.4.1 Wine

7.3.4.2 Whisky

7.3.4.3 Rum

7.3.4.4 Brandy

7.3.4.5 Vodka

7.3.4.6 Gin

7.3.4.7 Tequila

7.3.4.8 Others

7.3.5 Historic and Forecasted Market Size by Distribution Channel

7.3.5.1 Food Retail

7.3.5.2 Food Service

7.3.6 Historic and Forecast Market Size by Country

7.3.6.1 Russia

7.3.6.2 Bulgaria

7.3.6.3 The Czech Republic

7.3.6.4 Hungary

7.3.6.5 Poland

7.3.6.6 Romania

7.3.6.7 Rest of Eastern Europe

7.4. Western Europe Luxury Wines and Spirits Market

7.4.1 Key Market Trends, Growth Factors and Opportunities

7.4.2 Top Key Companies

7.4.3 Historic and Forecasted Market Size by Segments

7.4.4 Historic and Forecasted Market Size by Type

7.4.4.1 Wine

7.4.4.2 Whisky

7.4.4.3 Rum

7.4.4.4 Brandy

7.4.4.5 Vodka

7.4.4.6 Gin

7.4.4.7 Tequila

7.4.4.8 Others

7.4.5 Historic and Forecasted Market Size by Distribution Channel

7.4.5.1 Food Retail

7.4.5.2 Food Service

7.4.6 Historic and Forecast Market Size by Country

7.4.6.1 Germany

7.4.6.2 UK

7.4.6.3 France

7.4.6.4 The Netherlands

7.4.6.5 Italy

7.4.6.6 Spain

7.4.6.7 Rest of Western Europe

7.5. Asia Pacific Luxury Wines and Spirits Market

7.5.1 Key Market Trends, Growth Factors and Opportunities

7.5.2 Top Key Companies

7.5.3 Historic and Forecasted Market Size by Segments

7.5.4 Historic and Forecasted Market Size by Type

7.5.4.1 Wine

7.5.4.2 Whisky

7.5.4.3 Rum

7.5.4.4 Brandy

7.5.4.5 Vodka

7.5.4.6 Gin

7.5.4.7 Tequila

7.5.4.8 Others

7.5.5 Historic and Forecasted Market Size by Distribution Channel

7.5.5.1 Food Retail

7.5.5.2 Food Service

7.5.6 Historic and Forecast Market Size by Country

7.5.6.1 China

7.5.6.2 India

7.5.6.3 Japan

7.5.6.4 South Korea

7.5.6.5 Malaysia

7.5.6.6 Thailand

7.5.6.7 Vietnam

7.5.6.8 The Philippines

7.5.6.9 Australia

7.5.6.10 New Zealand

7.5.6.11 Rest of APAC

7.6. Middle East & Africa Luxury Wines and Spirits Market

7.6.1 Key Market Trends, Growth Factors and Opportunities

7.6.2 Top Key Companies

7.6.3 Historic and Forecasted Market Size by Segments

7.6.4 Historic and Forecasted Market Size by Type

7.6.4.1 Wine

7.6.4.2 Whisky

7.6.4.3 Rum

7.6.4.4 Brandy

7.6.4.5 Vodka

7.6.4.6 Gin

7.6.4.7 Tequila

7.6.4.8 Others

7.6.5 Historic and Forecasted Market Size by Distribution Channel

7.6.5.1 Food Retail

7.6.5.2 Food Service

7.6.6 Historic and Forecast Market Size by Country

7.6.6.1 Turkiye

7.6.6.2 Bahrain

7.6.6.3 Kuwait

7.6.6.4 Saudi Arabia

7.6.6.5 Qatar

7.6.6.6 UAE

7.6.6.7 Israel

7.6.6.8 South Africa

7.7. South America Luxury Wines and Spirits Market

7.7.1 Key Market Trends, Growth Factors and Opportunities

7.7.2 Top Key Companies

7.7.3 Historic and Forecasted Market Size by Segments

7.7.4 Historic and Forecasted Market Size by Type

7.7.4.1 Wine

7.7.4.2 Whisky

7.7.4.3 Rum

7.7.4.4 Brandy

7.7.4.5 Vodka

7.7.4.6 Gin

7.7.4.7 Tequila

7.7.4.8 Others

7.7.5 Historic and Forecasted Market Size by Distribution Channel

7.7.5.1 Food Retail

7.7.5.2 Food Service

7.7.6 Historic and Forecast Market Size by Country

7.7.6.1 Brazil

7.7.6.2 Argentina

7.7.6.3 Rest of SA

Chapter 8 Analyst Viewpoint and Conclusion

8.1 Recommendations and Concluding Analysis

8.2 Potential Market Strategies

Chapter 9 Research Methodology

9.1 Research Process

9.2 Primary Research

9.3 Secondary Research

|

Global Luxury Wines and Spirits Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 512.88 Bn. |

|

Forecast Period 2024-32 CAGR: |

6.23% |

Market Size in 2032: |

USD 883.57 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Distribution Channel |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||